Caleres (CAL)

Caleres faces an uphill battle. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Caleres Will Underperform

The owner of Dr. Scholl's, Caleres (NYSE:CAL) is a footwear company offering a range of styles.

- Sales trends were unexciting over the last five years as its 5.4% annual growth was below the typical consumer discretionary company

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- High net-debt-to-EBITDA ratio of 8× increases the risk of forced asset sales or dilutive financing if operational performance weakens

Caleres falls short of our quality standards. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Caleres

At $11.47 per share, Caleres trades at 7.5x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Caleres (CAL) Research Report: Q4 CY2025 Update

Footwear company Caleres (NYSE:CAL) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 8.7% year on year to $695.1 million. Its non-GAAP loss of $0.06 per share was 85.1% above analysts’ consensus estimates.

Caleres (CAL) Q4 CY2025 Highlights:

- Revenue: $695.1 million vs analyst estimates of $685.4 million (8.7% year-on-year growth, 1.4% beat)

- Adjusted EPS: -$0.06 vs analyst estimates of -$0.40 (85.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $1.50 at the midpoint, missing analyst estimates by 0.9%

- Operating Margin: -3.8%, down from 2.5% in the same quarter last year

- Free Cash Flow Margin: 6.6%, up from 2.8% in the same quarter last year

- Market Capitalization: $300.3 million

Company Overview

The owner of Dr. Scholl's, Caleres (NYSE:CAL) is a footwear company offering a range of styles.

The company started as a niche footwear manufacturer and retailer, Bryan-Brown Shoe Company, and has expanded over time by acquiring numerous brands including Naturalizer, Buster Brown, and LifeStride. In 2015, the company rebranded itself as Caleres in a strategic shift for global expansion and product diversification.

Caleres's brand acquisitions over its 100+ year history made it a major player in the shoe industry. Today, Caleres owns and operates Vince, Allen Edmonds, Dr. Scholls, and many other household names. The company's portfolio approach allows it to cater to a wide range of consumer preferences and market segments, from fashion-forward footwear to comfort and orthopedic options.

In addition to its shoemakers, Caleres owns Famous Footwear, a large retailer of popular athletic and casual shoes. Along with its own line of shoes, Famous Footwear carries popular brands like Nike and Adidas through its expansive retail store network and e-commerce platform.

4. Consumer Discretionary - Footwear

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Footwear companies design, manufacture, and market shoes across athletic, casual, and luxury segments. Tailwinds include the global athleisure trend, growing health and fitness awareness driving sneaker demand, and expanding direct-to-consumer digital channels that improve brand control and margins. However, headwinds are notable: the industry faces intense competition and brand-switching behavior, heavy marketing spend requirements to maintain relevance, and exposure to volatile raw material and freight costs. Tariff risk from concentrated overseas manufacturing, primarily in Asia, remains a persistent concern. Additionally, inventory management is challenging given seasonal and trend-driven demand, with markdowns eroding profitability when styles miss consumer expectations.

Caleres's shoe brands compete with Deckers Outdoor (NYSE:DECK) and VF Corp (NYSE:VFC) while Famous Footwear competes with retailers such as Foot Locker (NYSE:FL) and Designer Brands (NYSE:DBI).

5. Revenue Growth

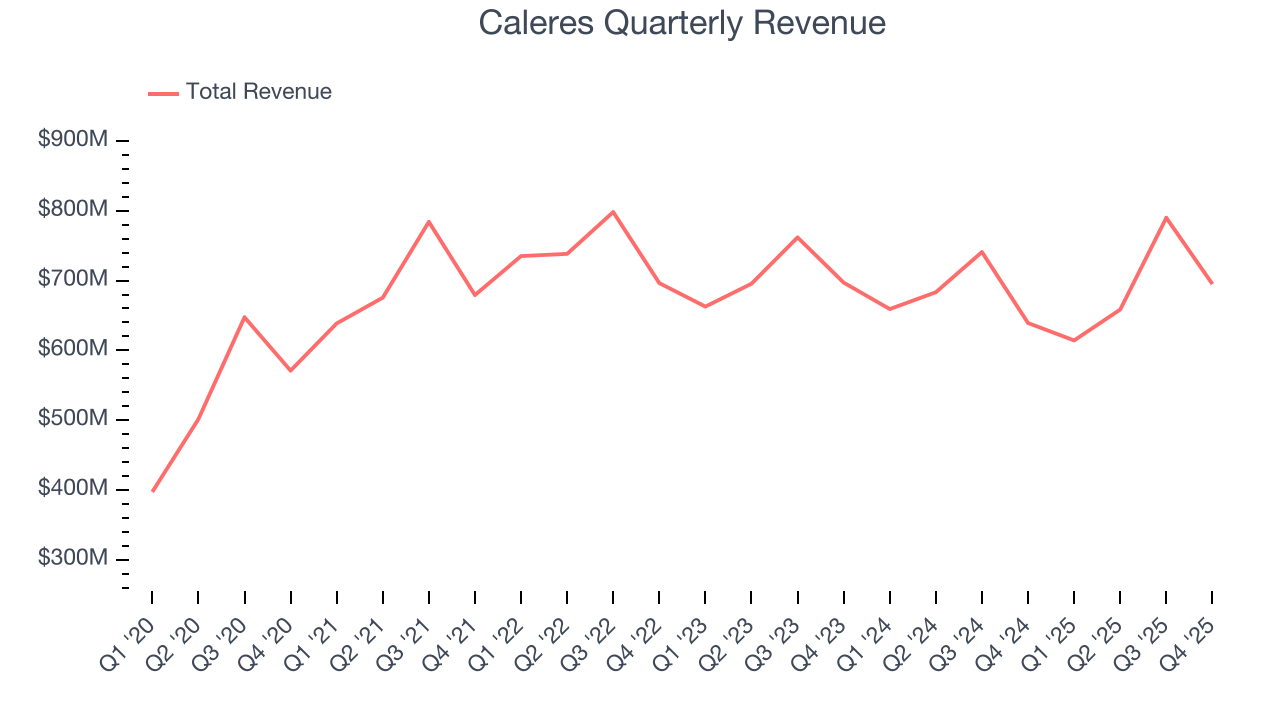

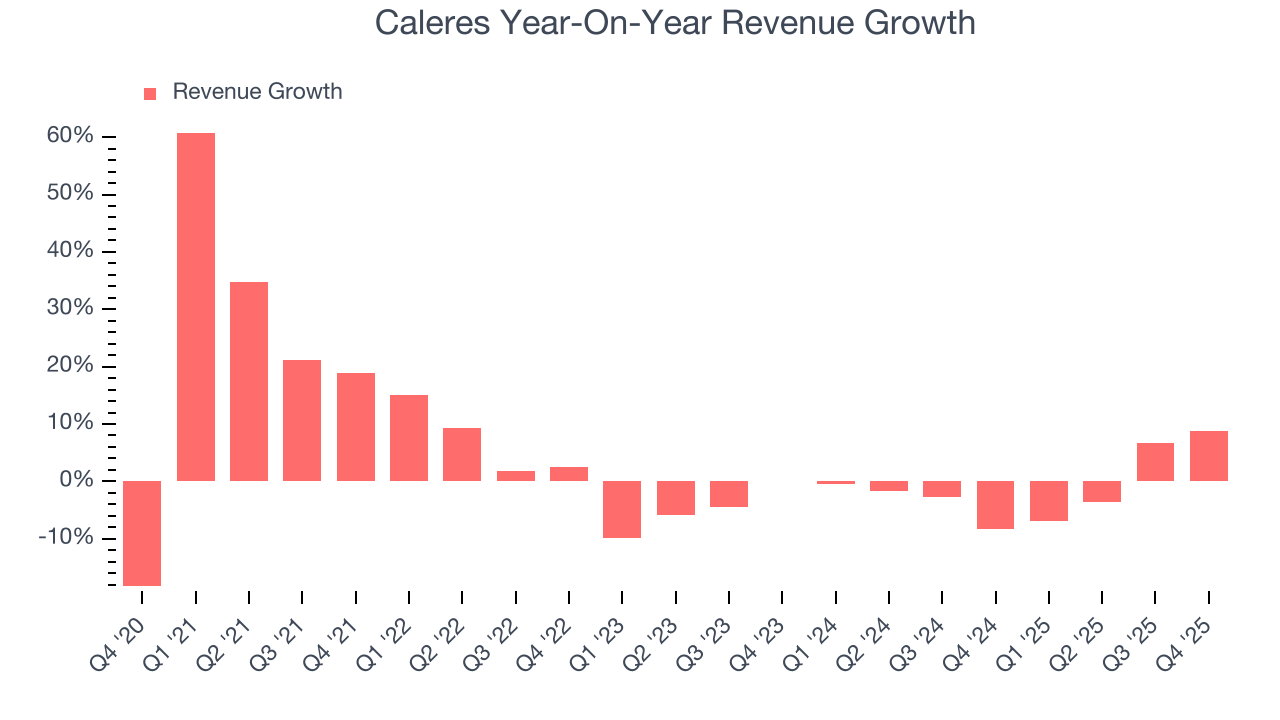

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Caleres grew its sales at a weak 5.4% compounded annual growth rate. This fell short of our benchmark for the consumer discretionary sector and is a poor baseline for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Caleres’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.1% annually.

This quarter, Caleres reported year-on-year revenue growth of 8.7%, and its $695.1 million of revenue exceeded Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 4.9% over the next 12 months. While this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

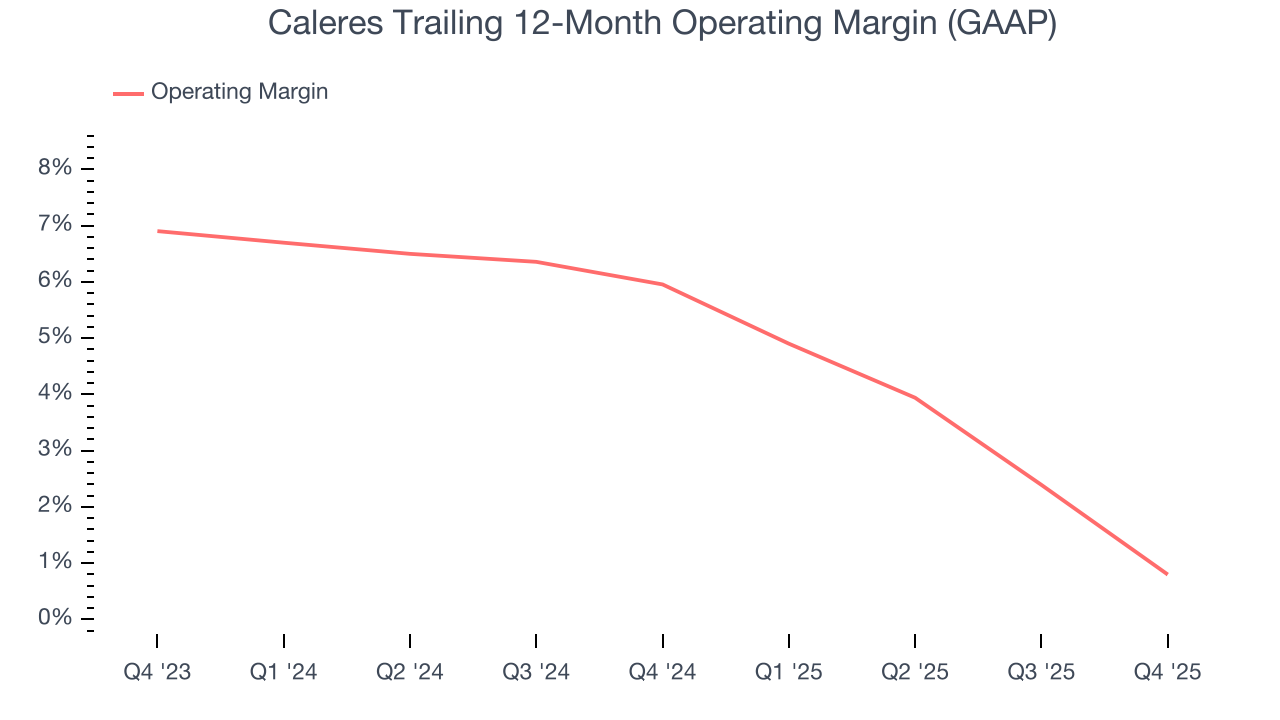

6. Operating Margin

Caleres’s operating margin has been trending down over the last 12 months and averaged 3.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, Caleres generated an operating margin profit margin of negative 3.8%, down 6.3 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

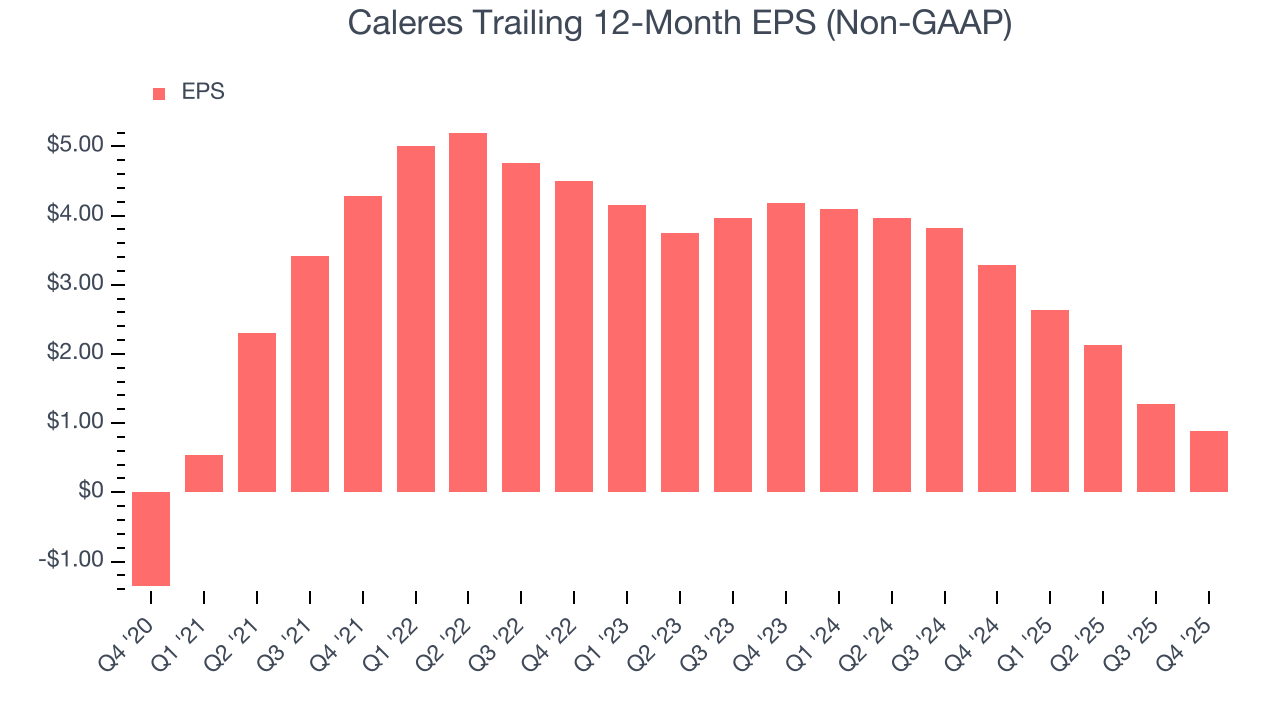

Caleres’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Caleres reported adjusted EPS of negative $0.06, down from $0.33 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Caleres’s full-year EPS of $0.89 to grow 68.5%.

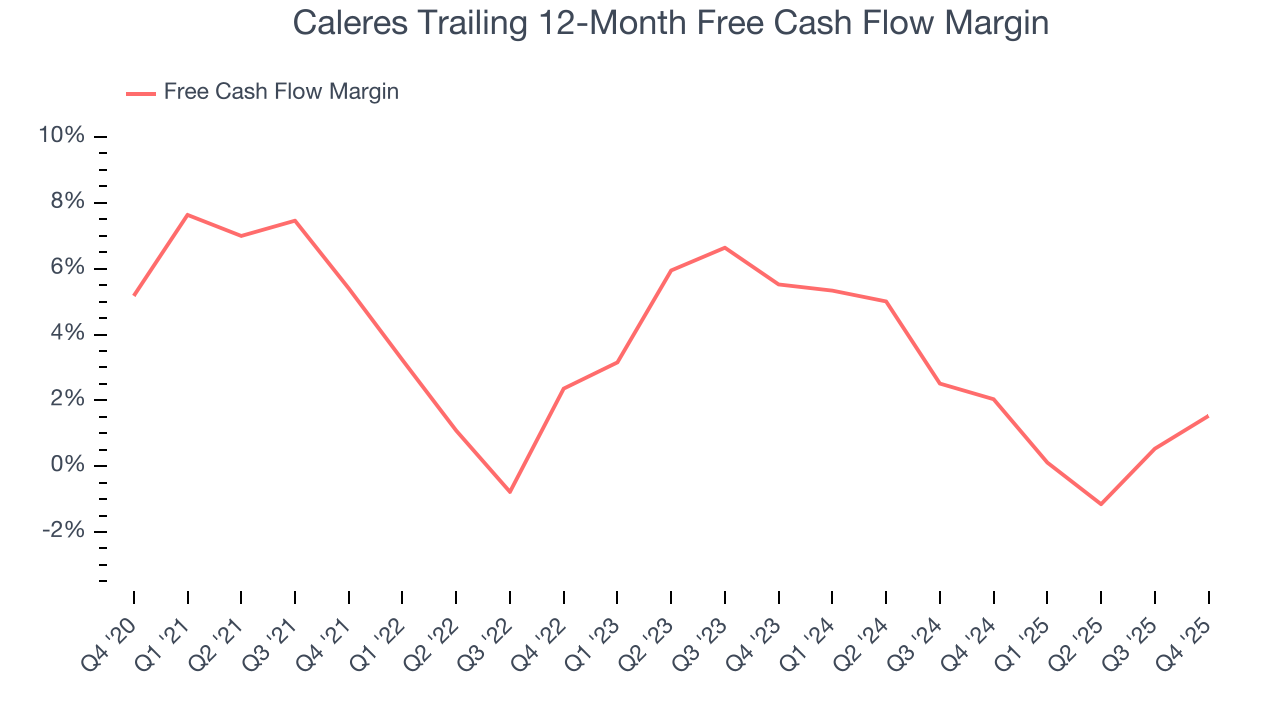

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Caleres has shown poor cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.8%, below what we’d expect for a consumer discretionary business.

Caleres’s free cash flow clocked in at $45.79 million in Q4, equivalent to a 6.6% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

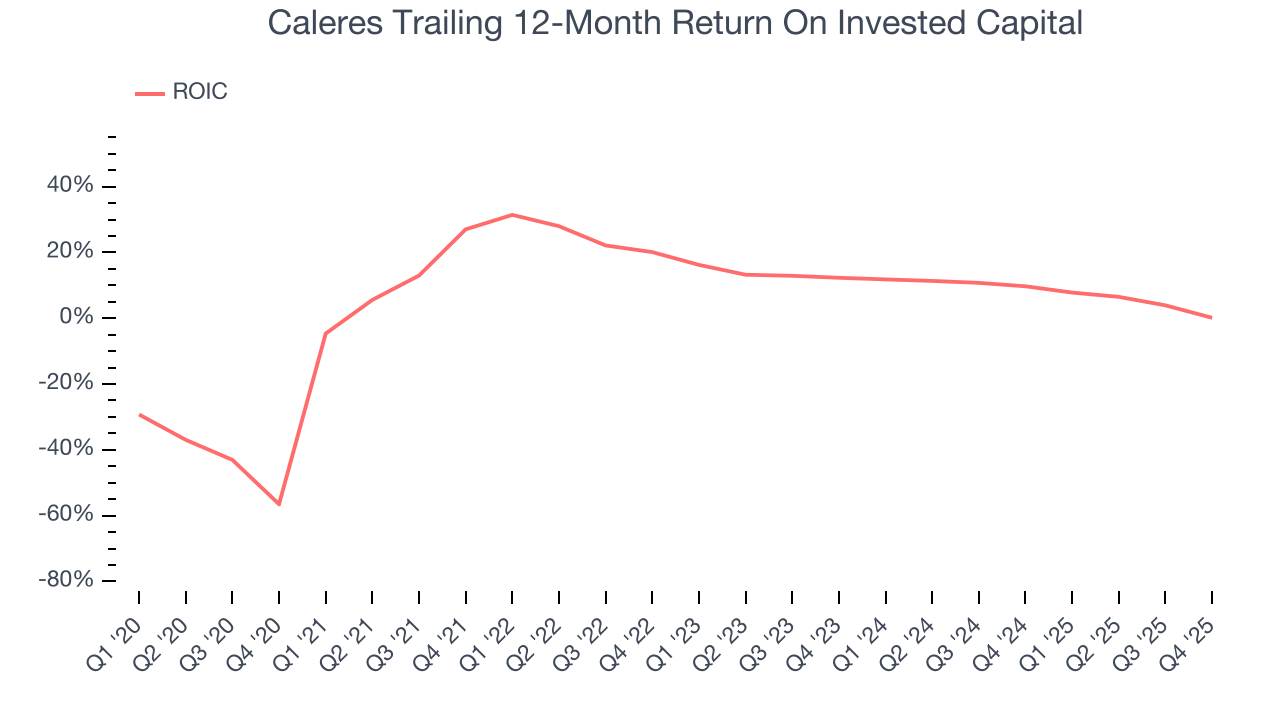

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Caleres historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 13.9%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Caleres’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

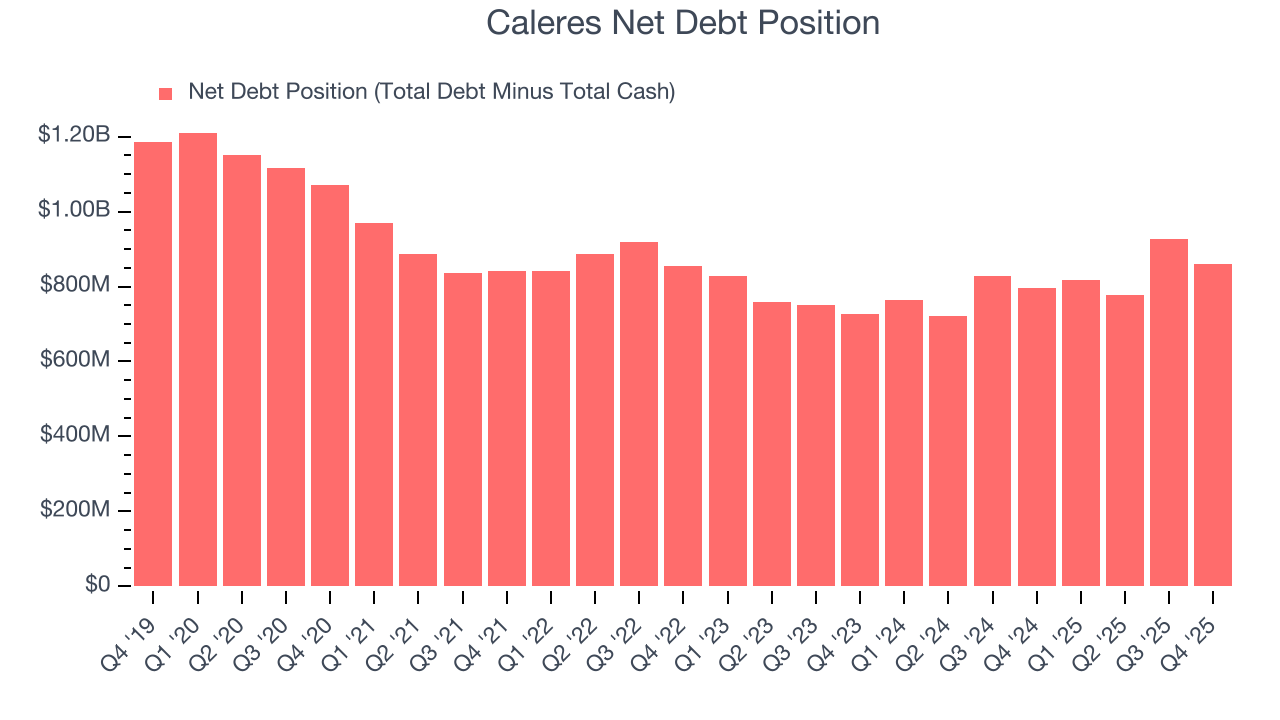

10. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Caleres’s $891.1 million of debt exceeds the $29.77 million of cash on its balance sheet. Furthermore, its 9× net-debt-to-EBITDA ratio (based on its EBITDA of $92.61 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Caleres could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Caleres can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Caleres’s Q4 Results

It was good to see Caleres beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed. Overall, this print had some key positives. The stock traded up 9.5% to $9.66 immediately after reporting.

12. Is Now The Time To Buy Caleres?

Updated: March 24, 2026 at 10:52 PM EDT

Are you wondering whether to buy Caleres or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

We cheer for all companies serving everyday consumers, but in the case of Caleres, we’ll be cheering from the sidelines. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its Forecasted free cash flow margin suggests the company will have more capital to invest or return to shareholders next year. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Caleres’s P/E ratio based on the next 12 months is 7.5x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $15 on the company (compared to the current share price of $11.47).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.