Getty Images (GETY)

Getty Images doesn’t excite us. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Getty Images Will Underperform

With a vast library of over 562 million visual assets documenting everything from breaking news to iconic historical moments, Getty Images (NYSE:GETY) is a global visual content marketplace that licenses photos, videos, illustrations, and music to businesses, media outlets, and creative professionals.

- Estimated sales growth of 2.4% for the next 12 months is soft and implies weaker demand

- 2.7% annual revenue growth over the last five years was slower than its business services peers

- On the plus side, its stellar returns on capital showcase management’s ability to surface highly profitable business ventures

Getty Images’s quality is inadequate. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than Getty Images

Getty Images’s stock price of $0.75 implies a valuation ratio of 11.9x forward P/E. Yes, this valuation multiple is lower than that of other business services peers, but we’ll remind you that you often get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Getty Images (GETY) Research Report: Q4 CY2025 Update

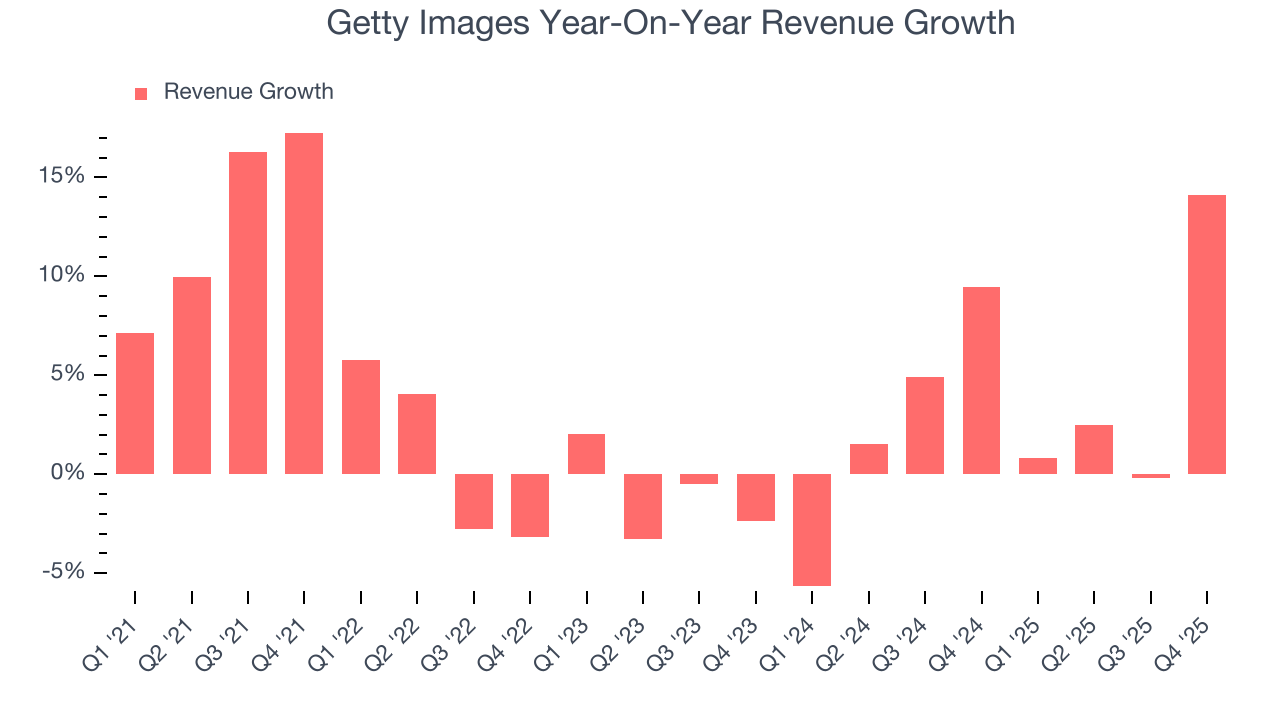

Visual content marketplace Getty Images (NYSE:GETY) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 14.1% year on year to $282.3 million. On the other hand, the company’s full-year revenue guidance of $968 million at the midpoint came in 0.5% below analysts’ estimates. Its non-GAAP loss of $0.01 per share was $0.03 below analysts’ consensus estimates.

Getty Images (GETY) Q4 CY2025 Highlights:

- Revenue: $282.3 million vs analyst estimates of $245.6 million (14.1% year-on-year growth, 15% beat)

- Adjusted EPS: -$0.01 vs analyst estimates of $0.02 ($0.03 miss)

- Adjusted EBITDA: $104.1 million vs analyst estimates of $74.7 million (36.9% margin, 39.3% beat)

- EBITDA guidance for the upcoming financial year 2026 is $287 million at the midpoint, below analyst estimates of $304.5 million

- Operating Margin: -8.5%, down from 14.5% in the same quarter last year

- Free Cash Flow Margin: 2.7%, down from 9.9% in the same quarter last year

- Market Capitalization: $303.2 million

Company Overview

With a vast library of over 562 million visual assets documenting everything from breaking news to iconic historical moments, Getty Images (NYSE:GETY) is a global visual content marketplace that licenses photos, videos, illustrations, and music to businesses, media outlets, and creative professionals.

The company operates through three main brands: Getty Images for premium content, iStock for value-oriented offerings, and Unsplash for both free and subscription-based content. This multi-tiered approach allows Getty Images to serve customers ranging from major corporations and news organizations to small businesses and individual creators.

Getty Images sources its content from a network of over 557,000 contributors worldwide, including more than 110 staff photographers and videographers who cover news, sports, and entertainment events. The company maintains exclusive relationships with over 80,000 contributors and 70 editorial content partners, including major organizations like Disney, Bloomberg, and sports leagues such as Formula One, NBA, and FIFA.

A corporate marketing team might use Getty Images to license professional photography for an advertising campaign, paying either through a single purchase or via a Premium Access subscription that provides broad access to the company's entire library. Meanwhile, a small business owner could turn to iStock for more affordable visual assets, while a blogger might utilize Unsplash's free content collection.

The company has increasingly shifted toward subscription-based revenue models, with annual subscriptions now representing more than half of total revenue. These subscription offerings provide customers with ongoing access to content while giving Getty Images more predictable revenue streams. Beyond simple licensing, the company also offers services like custom content creation, digital asset management, and recently launched AI-generated imagery in partnership with NVIDIA.

Getty Images maintains one of the world's largest private photographic archives, with over 135 million historical images spanning various time periods, geographies, and subject matters. This includes exclusive representation of historically significant collections like Hulton, Bettman, Sygma, and Gamma archives.

4. Digital Media & Content Platforms

AI-driven content creation, personalized media experiences, and digital advertising are evolving, which could benefit companies investing in these themes. For example, companies with a portfolio of licensed visual content or platforms facilitating direct monetization models could see increased demand for years. On the other hand, headwinds include growing regulatory scrutiny on AI-generated content, with many publishers balking at anything that gets no human oversight. Additional areas to navigate include the phasing out of third-party cookies, which could make traditional ways of tracking the online behavior of consumers (a secret sauce in digital marketing) much less effective.

Getty Images competes with visual content marketplaces like Shutterstock (NYSE:SSTK), Adobe Stock (part of Adobe Inc., NASDAQ:ADBE), and privately-held companies such as Alamy and VCG. The company also faces competition from user-generated content platforms and AI image generation services.

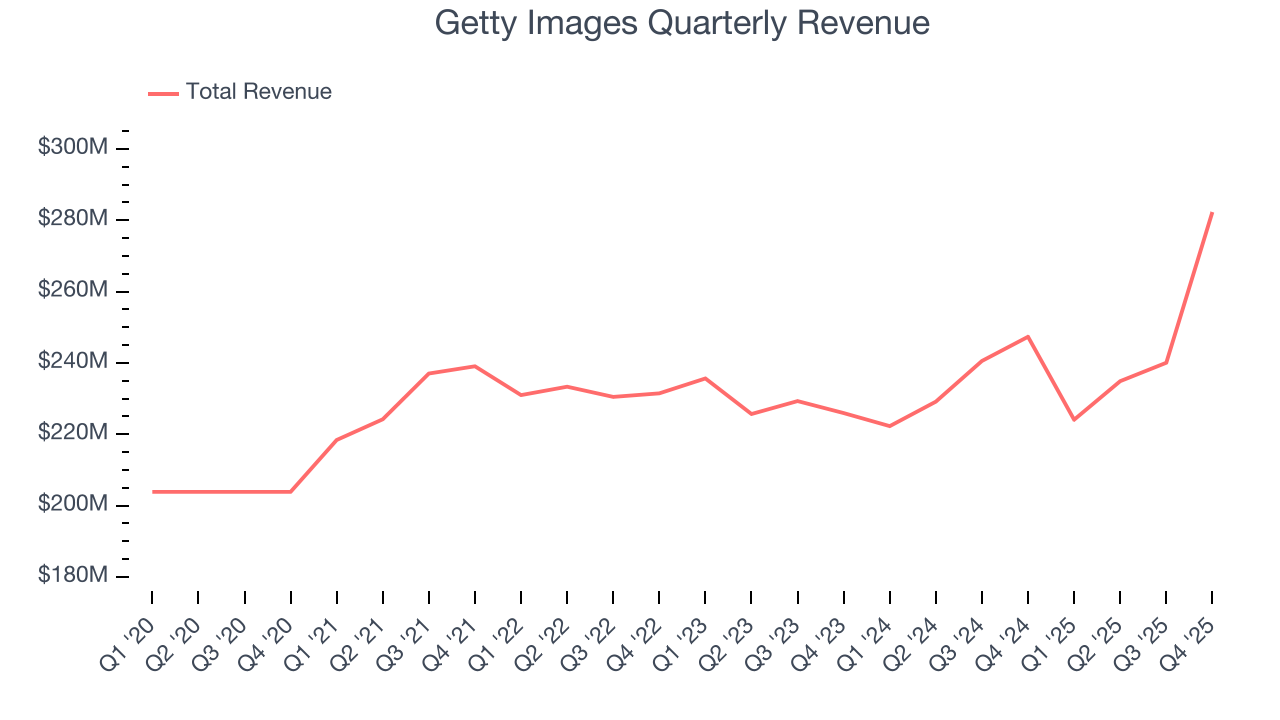

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $981.3 million in revenue over the past 12 months, Getty Images is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels.

As you can see below, Getty Images’s sales grew at a tepid 3.8% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Getty Images’s annualized revenue growth of 3.5% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

This quarter, Getty Images reported year-on-year revenue growth of 14.1%, and its $282.3 million of revenue exceeded Wall Street’s estimates by 15%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will see some demand headwinds.

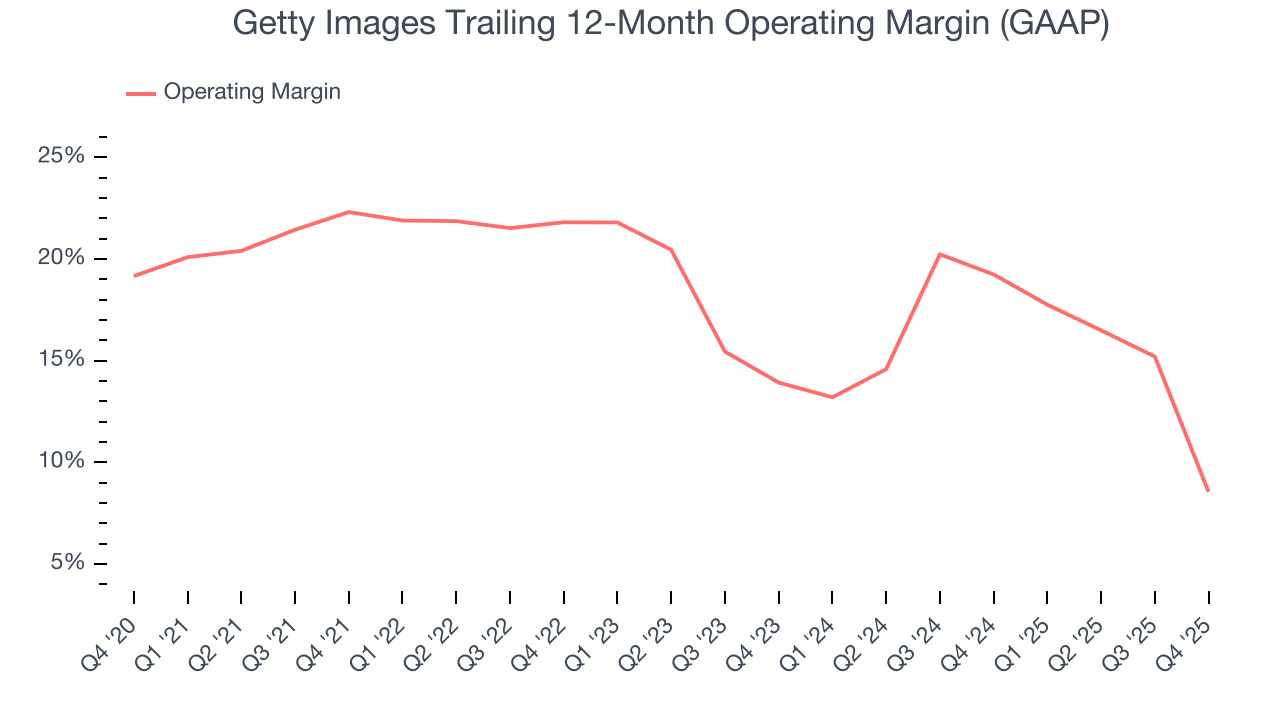

6. Operating Margin

Getty Images has been an efficient company over the last five years. It was one of the more profitable businesses in the business services sector, boasting an average operating margin of 17.1%.

Analyzing the trend in its profitability, Getty Images’s operating margin decreased by 13.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Getty Images generated an operating margin profit margin of negative 8.5%, down 23 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

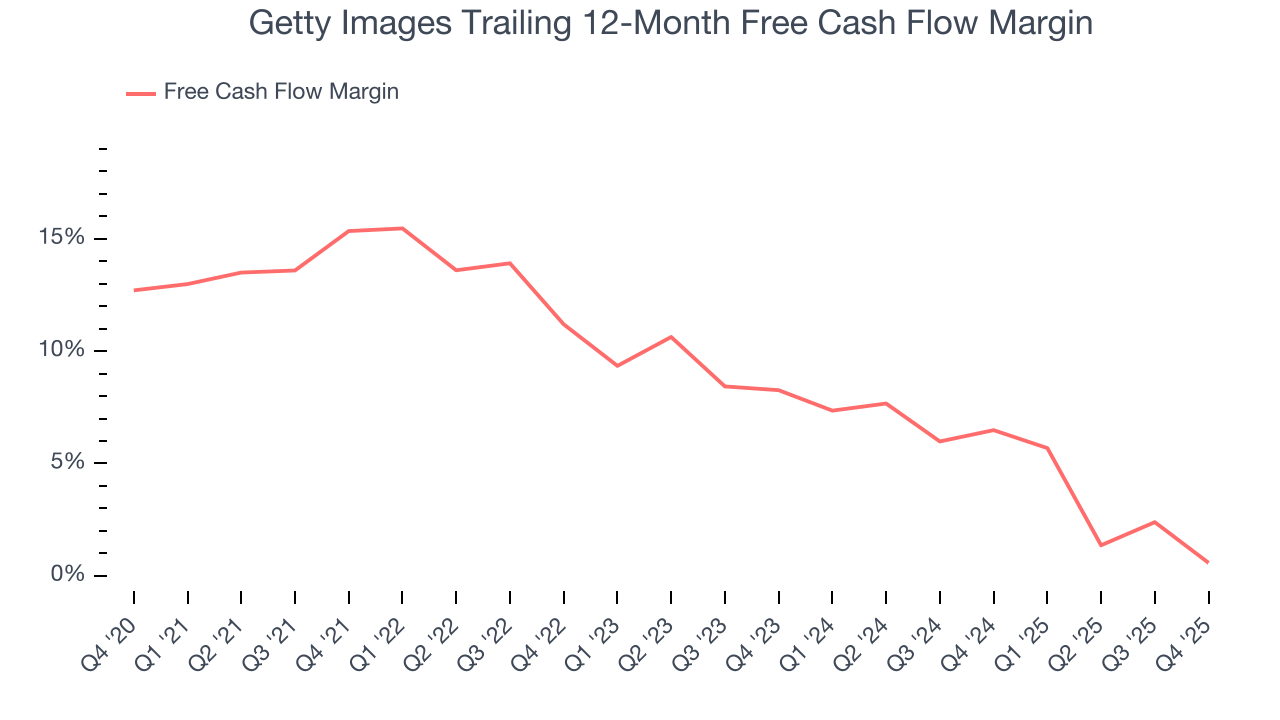

7. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Getty Images has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.3% over the last five years, better than the broader business services sector.

Taking a step back, we can see that Getty Images’s margin dropped by 14.8 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

Getty Images’s free cash flow clocked in at $7.67 million in Q4, equivalent to a 2.7% margin. The company’s cash profitability regressed as it was 7.2 percentage points lower than in the same quarter last year, suggesting its historical struggles have dragged on.

8. Balance Sheet Assessment

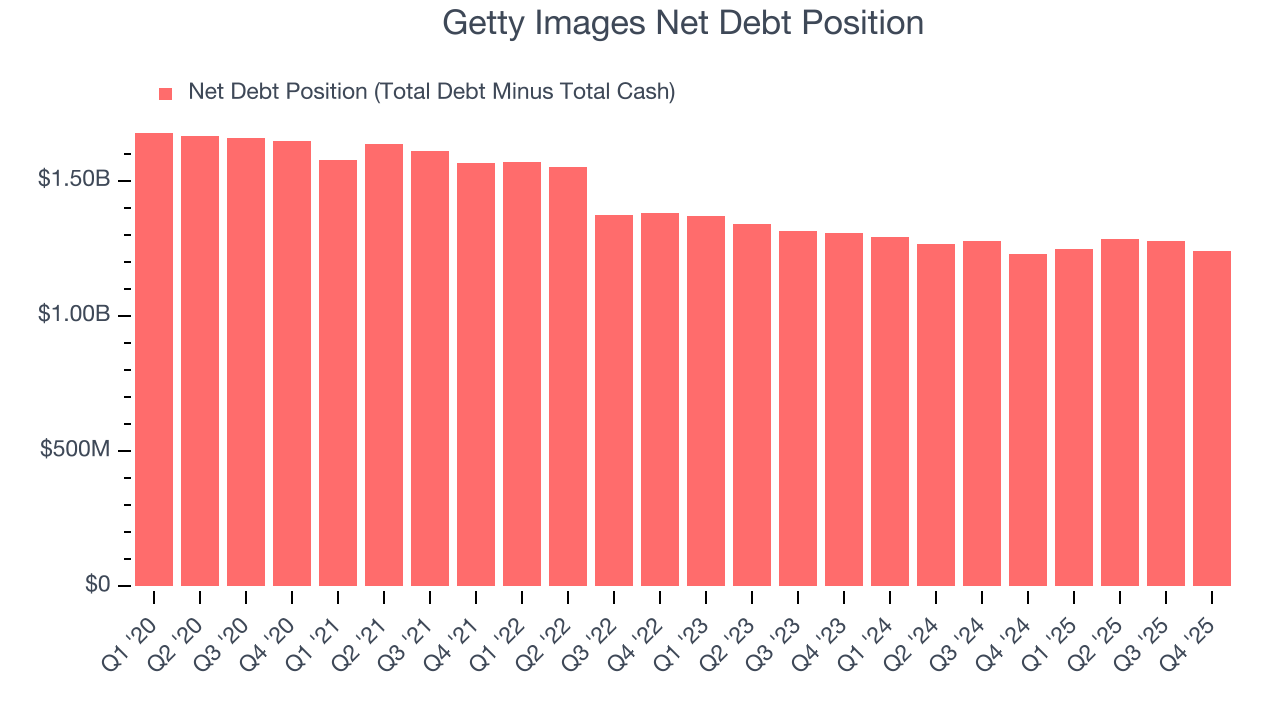

Getty Images reported $725.3 million of cash and $1.97 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $320.9 million of EBITDA over the last 12 months, we view Getty Images’s 3.9× net-debt-to-EBITDA ratio as safe. We also see its $53.78 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

9. Key Takeaways from Getty Images’s Q4 Results

We were impressed by how significantly Getty Images blew past analysts’ revenue expectations this quarter. On the other hand, its EPS was in line and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $0.77 immediately following the results.

10. Is Now The Time To Buy Getty Images?

Updated: March 16, 2026 at 4:25 PM EDT

When considering an investment in Getty Images, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Getty Images doesn’t pass our quality test. To begin with, its revenue growth was uninspiring over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its projected EPS for the next year implies the company will start generating shareholder value, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last two years makes it a less attractive asset to the public markets.

Getty Images’s EV-to-EBITDA ratio based on the next 12 months is 5.2x. This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $3.93 on the company (compared to the current share price of $0.77).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.