Hewlett Packard Enterprise (HPE)

Hewlett Packard Enterprise is interesting. Its revenue and EPS are projected to skyrocket next year, an optimistic sign for its share price.― StockStory Analyst Team

1. News

2. Summary

Why Hewlett Packard Enterprise Is Interesting

Born from the 2015 split of the iconic Silicon Valley pioneer Hewlett-Packard, Hewlett Packard Enterprise (NYSE:HPE) provides edge-to-cloud technology solutions that help businesses capture, analyze, and act upon their data across hybrid IT environments.

- Unparalleled revenue scale of $35.74 billion gives it an edge in distribution

- Projected revenue growth of 16.8% for the next 12 months is above its two-year trend, pointing to accelerating demand

- On the flip side, its ROIC of 3.1% reflects management’s challenges in identifying attractive investment opportunities

Hewlett Packard Enterprise has some noteworthy aspects. If you like the story, the valuation seems fair.

Why Is Now The Time To Buy Hewlett Packard Enterprise?

Hewlett Packard Enterprise is trading at $21.73 per share, or 9.2x forward P/E. Price is what you pay, and value is what you get. With this in mind, we think the current price is quite attractive.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Hewlett Packard Enterprise (HPE) Research Report: Q4 CY2025 Update

Enterprise technology company Hewlett Packard Enterprise (NYSE:HPE) fell short of the market’s revenue expectations in Q4 CY2025, but sales rose 18.4% year on year to $9.30 billion. On the other hand, next quarter’s outlook exceeded expectations with revenue guided to $9.8 billion at the midpoint, or 2.8% above analysts’ estimates. Its non-GAAP profit of $0.65 per share was 10.8% above analysts’ consensus estimates.

Hewlett Packard Enterprise (HPE) Q4 CY2025 Highlights:

- Revenue: $9.30 billion vs analyst estimates of $9.35 billion (18.4% year-on-year growth, 0.5% miss)

- Adjusted EPS: $0.65 vs analyst estimates of $0.59 (10.8% beat)

- Adjusted EBITDA: $1.56 billion vs analyst estimates of $1.67 billion (16.8% margin, 6.4% miss)

- Revenue Guidance for Q1 CY2026 is $9.8 billion at the midpoint, above analyst estimates of $9.53 billion

- Management raised its full-year Adjusted EPS guidance to $2.40 at the midpoint, a 2.1% increase

- Operating Margin: 5.1%, in line with the same quarter last year

- Free Cash Flow was $708 million, up from -$834 million in the same quarter last year

- Market Capitalization: $28.08 billion

Company Overview

Born from the 2015 split of the iconic Silicon Valley pioneer Hewlett-Packard, Hewlett Packard Enterprise (NYSE:HPE) provides edge-to-cloud technology solutions that help businesses capture, analyze, and act upon their data across hybrid IT environments.

HPE's business spans several key technology domains. Its server segment offers a range of computing solutions from general-purpose ProLiant servers to specialized high-performance systems designed for artificial intelligence and data analytics workloads. For example, a research institution might use HPE's Cray supercomputers to process complex climate models requiring massive computational power.

The company's hybrid cloud segment provides storage, private cloud infrastructure, and software-as-a-service offerings that enable organizations to manage data across on-premises systems and public clouds. A healthcare provider might use HPE's Alletra storage systems to securely store patient records while leveraging HPE GreenLake to access those records through a cloud-like experience.

HPE's intelligent edge portfolio includes networking hardware and software that connect devices and users across campus, branch, and remote locations. A retail chain might deploy HPE Aruba wireless access points and switches to provide connectivity for point-of-sale systems, inventory management devices, and customer Wi-Fi.

The company generates revenue through hardware sales, software licenses, subscription services, and financing options. Its HPE GreenLake platform represents a strategic shift toward consumption-based models, allowing customers to pay for technology as they use it rather than making large upfront investments.

HPE Financial Services provides leasing and financing solutions that help customers acquire technology while managing cash flow. This division enables flexible consumption models, including the ability to return and upgrade equipment as needs change.

With operations spanning the globe, HPE serves organizations ranging from small businesses to large enterprises and government entities through both direct sales and channel partners.

4. Hardware & Infrastructure

The Hardware & Infrastructure sector will be buoyed by demand related to AI adoption, cloud computing expansion, and the need for more efficient data storage and processing solutions. Companies with tech offerings such as servers, switches, and storage solutions are well-positioned in our new hybrid working and IT world. On the other hand, headwinds include ongoing supply chain disruptions, rising component costs, and intensifying competition from cloud-native and hyperscale providers reducing reliance on traditional hardware. Additionally, regulatory scrutiny over data sovereignty, cybersecurity standards, and environmental sustainability in hardware manufacturing could increase compliance costs.

HPE competes with Dell Technologies (NYSE:DELL) and Cisco Systems (NASDAQ:CSCO) across most of its business segments. In cloud services, it faces competition from public cloud providers like Amazon Web Services (NASDAQ:AMZN), Microsoft Azure (NASDAQ:MSFT), and Google Cloud (NASDAQ:GOOGL). In networking, it competes with Juniper Networks (NYSE:JNPR), which HPE is in the process of acquiring.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

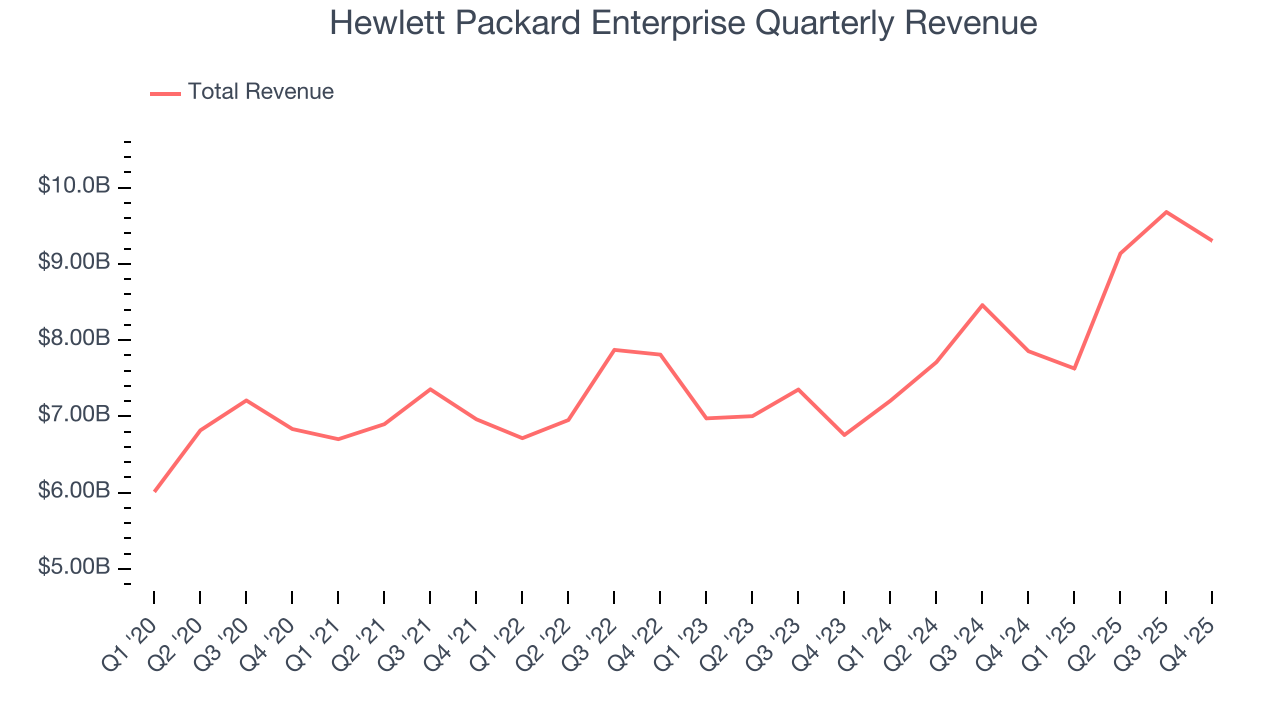

With $35.74 billion in revenue over the past 12 months, Hewlett Packard Enterprise is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices.

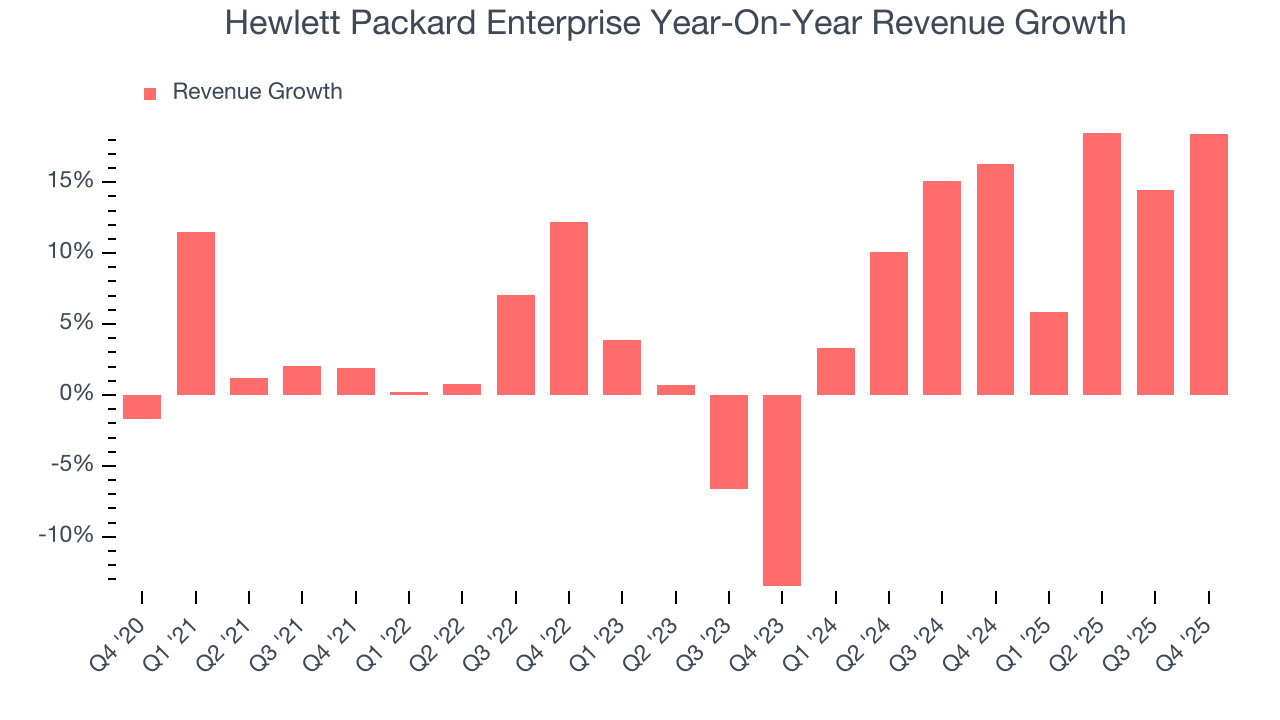

As you can see below, Hewlett Packard Enterprise’s 5.9% annualized revenue growth over the last five years was decent. This shows its offerings generated slightly more demand than the average business services company, a useful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Hewlett Packard Enterprise’s annualized revenue growth of 12.8% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Hewlett Packard Enterprise’s revenue grew by 18.4% year on year to $9.30 billion but fell short of Wall Street’s estimates. Company management is currently guiding for a 28.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16.1% over the next 12 months, an improvement versus the last two years. This projection is eye-popping for a company of its scale and indicates its newer products and services will fuel better top-line performance.

6. Operating Margin

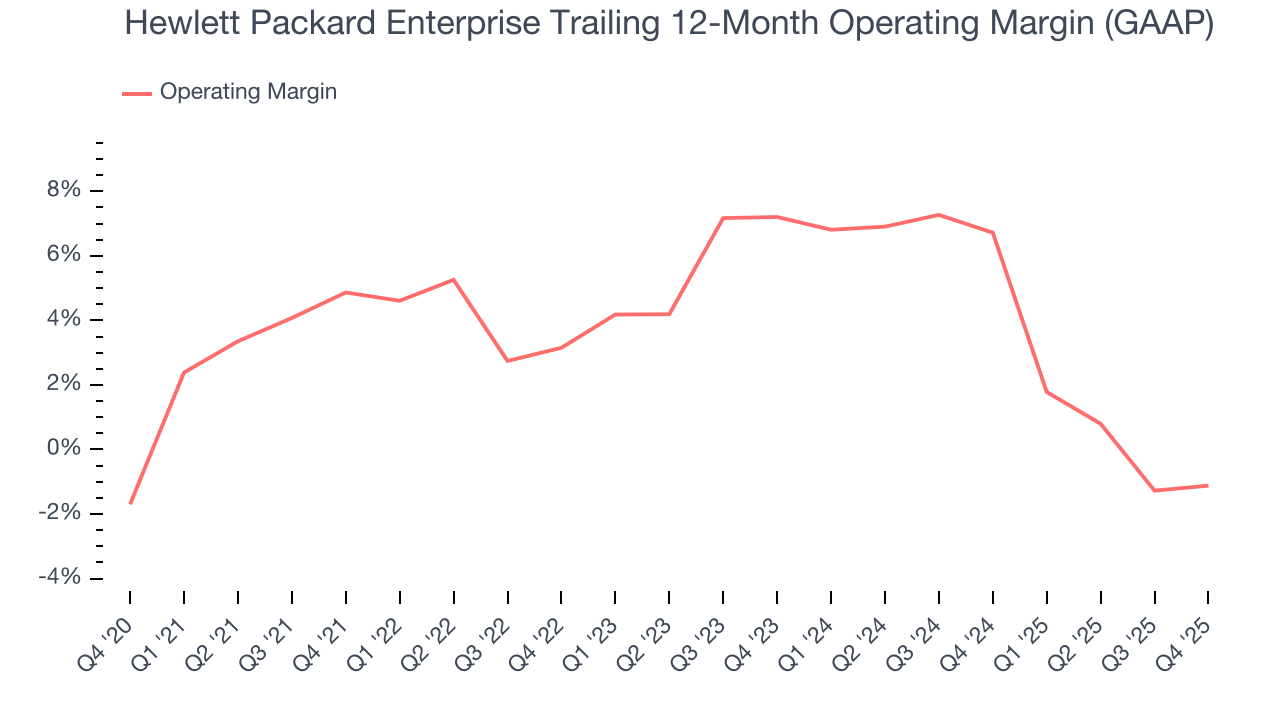

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Hewlett Packard Enterprise was profitable over the last five years but held back by its large cost base. Its average operating margin of 3.9% was weak for a business services business.

Looking at the trend in its profitability, Hewlett Packard Enterprise’s operating margin decreased by 6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Hewlett Packard Enterprise’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Hewlett Packard Enterprise generated an operating margin profit margin of 5.1%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

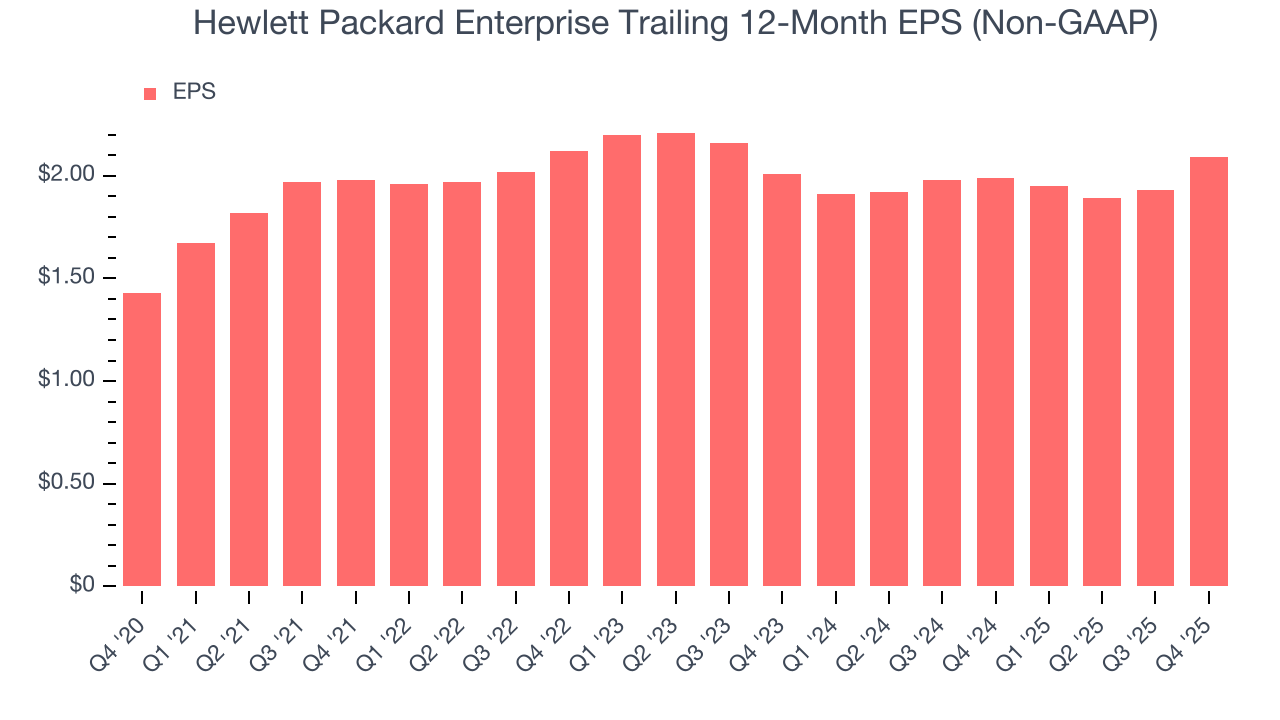

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Hewlett Packard Enterprise’s EPS grew at 7.9% compounded annual growth rate over the last five years, higher than its 5.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Hewlett Packard Enterprise, its two-year annual EPS growth of 2% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q4, Hewlett Packard Enterprise reported adjusted EPS of $0.65, up from $0.49 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Hewlett Packard Enterprise’s full-year EPS of $2.09 to grow 15.2%.

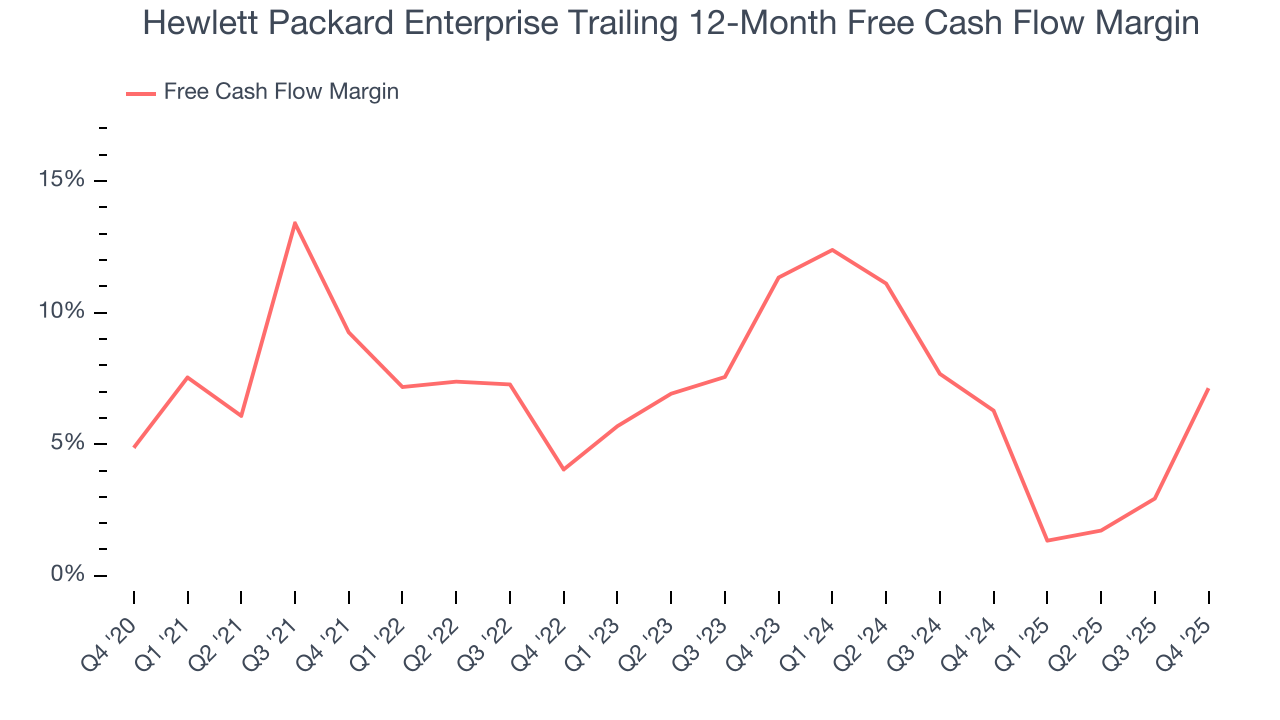

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Hewlett Packard Enterprise has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.5% over the last five years, better than the broader business services sector. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Taking a step back, we can see that Hewlett Packard Enterprise’s margin dropped by 2.1 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Hewlett Packard Enterprise’s free cash flow clocked in at $708 million in Q4, equivalent to a 7.6% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

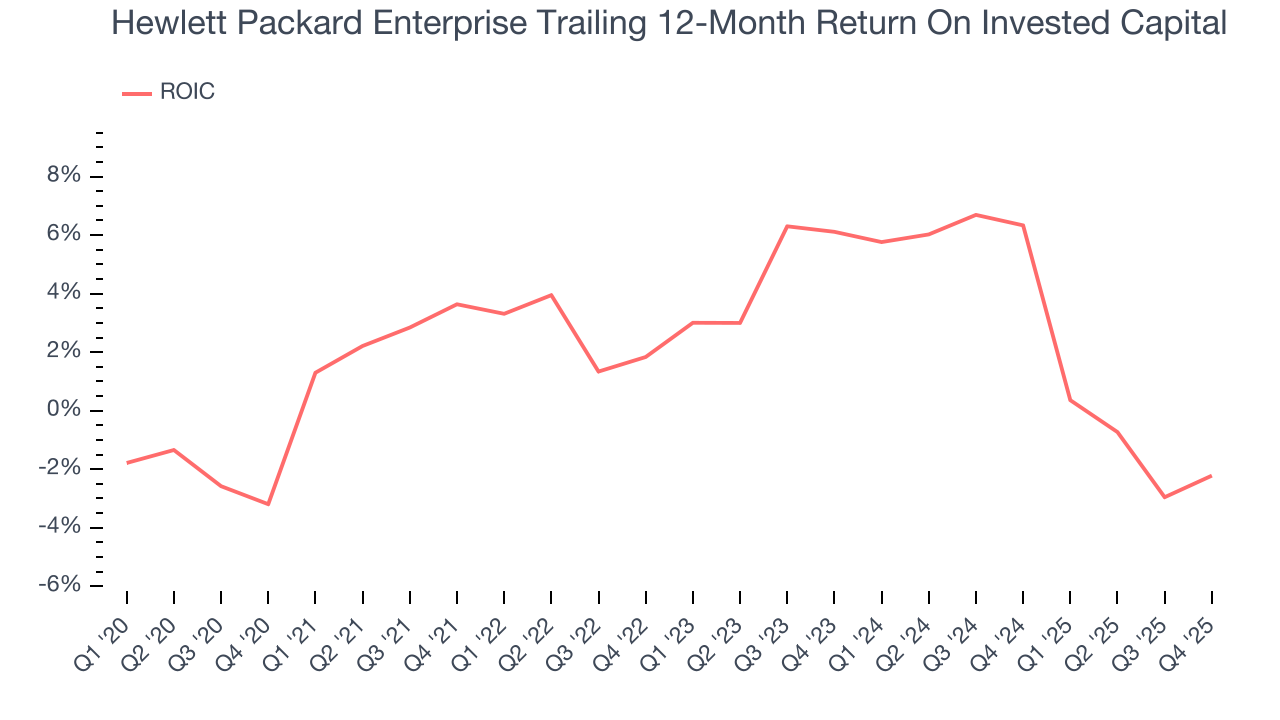

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Hewlett Packard Enterprise historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.1%, lower than the typical cost of capital (how much it costs to raise money) for business services companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Hewlett Packard Enterprise’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

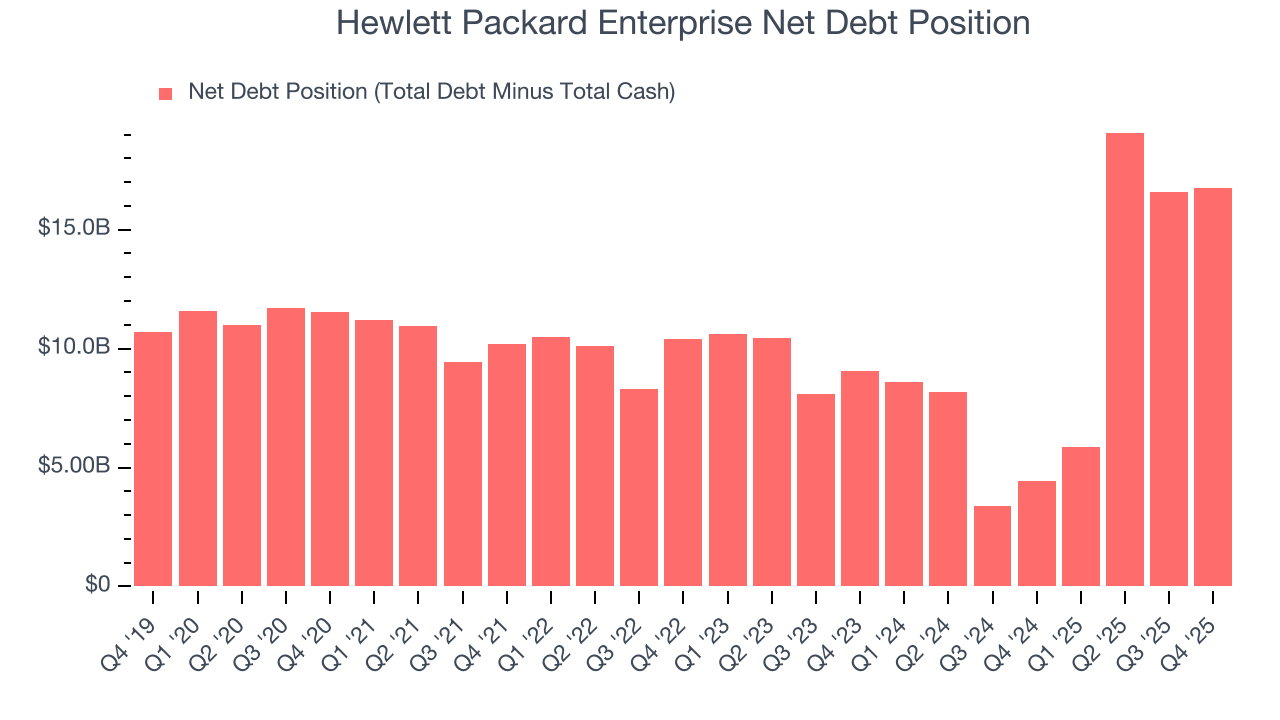

10. Balance Sheet Assessment

Hewlett Packard Enterprise reported $4.84 billion of cash and $21.61 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $6.27 billion of EBITDA over the last 12 months, we view Hewlett Packard Enterprise’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $25 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Hewlett Packard Enterprise’s Q4 Results

We were impressed by Hewlett Packard Enterprise’s optimistic revenue guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 2.6% to $22.46 immediately after reporting.

12. Is Now The Time To Buy Hewlett Packard Enterprise?

Updated: March 23, 2026 at 12:08 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Hewlett Packard Enterprise.

There are some positives when it comes to Hewlett Packard Enterprise’s fundamentals. First off, its revenue growth was decent over the last five years and is expected to accelerate over the next 12 months. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its scale makes it a trusted partner with negotiating leverage. On top of that, its ARR growth has been marvelous.

Hewlett Packard Enterprise’s P/E ratio based on the next 12 months is 9.2x. When scanning the business services space, Hewlett Packard Enterprise trades at a fair valuation. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $25.90 on the company (compared to the current share price of $21.73), implying they see 19.2% upside in buying Hewlett Packard Enterprise in the short term.