Kroger (KR)

We’re cautious of Kroger. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Kroger Will Underperform

With a sprawling network of over 2,400 locations offering digital pickup services, Kroger (NYSE:KR) operates supermarkets, pharmacies, and fuel centers across 35 states, offering customers groceries, household items, and private-label products.

- Widely-available products (and therefore stiff competition) result in an inferior gross margin of 23.4% that must be offset through higher volumes

- Earnings per share have contracted by 20.2% annually over the last three years, a headwind for returns as stock prices often echo long-term EPS performance

- A bright spot is that its unparalleled revenue scale of $147.6 billion offsets its poor gross margin and gives it advantageous pricing and terms with suppliers

Kroger falls short of our expectations. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than Kroger

At $73.50 per share, Kroger trades at 14x forward P/E. This valuation is fair for the quality you get, but we’re on the sidelines for now.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Kroger (KR) Research Report: Q4 CY2025 Update

Grocery retail giant Kroger (NYSE:KR) missed Wall Street’s revenue expectations in Q4 CY2025 as sales only rose 1.2% year on year to $34.73 billion. Its GAAP profit of $1.35 per share was 5.7% above analysts’ consensus estimates.

Kroger (KR) Q4 CY2025 Highlights:

- Revenue: $34.73 billion vs analyst estimates of $35.02 billion (1.2% year-on-year growth, 0.8% miss)

- EPS (GAAP): $1.35 vs analyst estimates of $1.28 (5.7% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $5.20 at the midpoint, in line with analyst estimates

- Operating Margin: 3.6%, in line with the same quarter last year

- Free Cash Flow Margin: 4.8%, up from 1.5% in the same quarter last year

- Same-Store Sales rose 2.4% year on year, in line with the same quarter last year

- Market Capitalization: $43.03 billion

Company Overview

With a sprawling network of over 2,400 locations offering digital pickup services, Kroger (NYSE:KR) operates supermarkets, pharmacies, and fuel centers across 35 states, offering customers groceries, household items, and private-label products.

Kroger combines physical retail with an expanding digital ecosystem to create a seamless shopping experience. Customers can shop in-store or use the company's Pickup, Delivery, and Ship services to receive their orders. The company's omnichannel strategy allows it to serve customers through multiple touchpoints while maintaining consistent selection and pricing.

At the core of Kroger's merchandising approach is its three-tiered private label strategy. The premium Private Selection brand offers gourmet and specialty items; the midrange Kroger brand provides national-brand-equivalent quality at lower prices; and value brands like Big K and Smart Way deliver affordable options. Simple Truth and Simple Truth Organic round out the portfolio with natural and organic products free from artificial ingredients.

Kroger's data analytics capabilities are particularly robust. With approximately 63 million households served annually and over 95% of transactions linked to loyalty cards, the company leverages customer insights to personalize shopping experiences. This data powers Kroger Precision Marketing, the company's retail media business that provides targeted advertising capabilities for consumer packaged goods partners, creating an additional revenue stream beyond traditional retail sales.

Kroger also operates its own food manufacturing facilities, including dairies, bakeries, and meat processing plants, giving it greater control over its supply chain and enabling it to respond quickly to changing consumer preferences.

4. Grocery Store

Grocery stores are non-discretionary because they sell food, an essential staple for life (maybe not that ice cream?). Selling food, however, is a notoriously tough business as grocers must deal with the costs of procuring and transporting oftentimes perishable products. Plus, the costs of operating stores to sell everything from raw meat to ice cream and fresh fruit are high. Competition is also fierce because grocers and other peers such as wholesale clubs tend to sell very similar brands and products. On the bright side, grocery is one of the least penetrated categories in e-commerce because customers prefer to buy their food in person. Still, the online threat exists and will likely increase over time rather than dwindle.

Kroger competes primarily with Walmart (NYSE:WMT), Target (NYSE:TGT), Albertsons (NYSE:ACI), Ahold Delhaize (OTCMKTS:ADRNY), and regional grocery chains, as well as with Amazon (NASDAQ:AMZN) in the online grocery space.

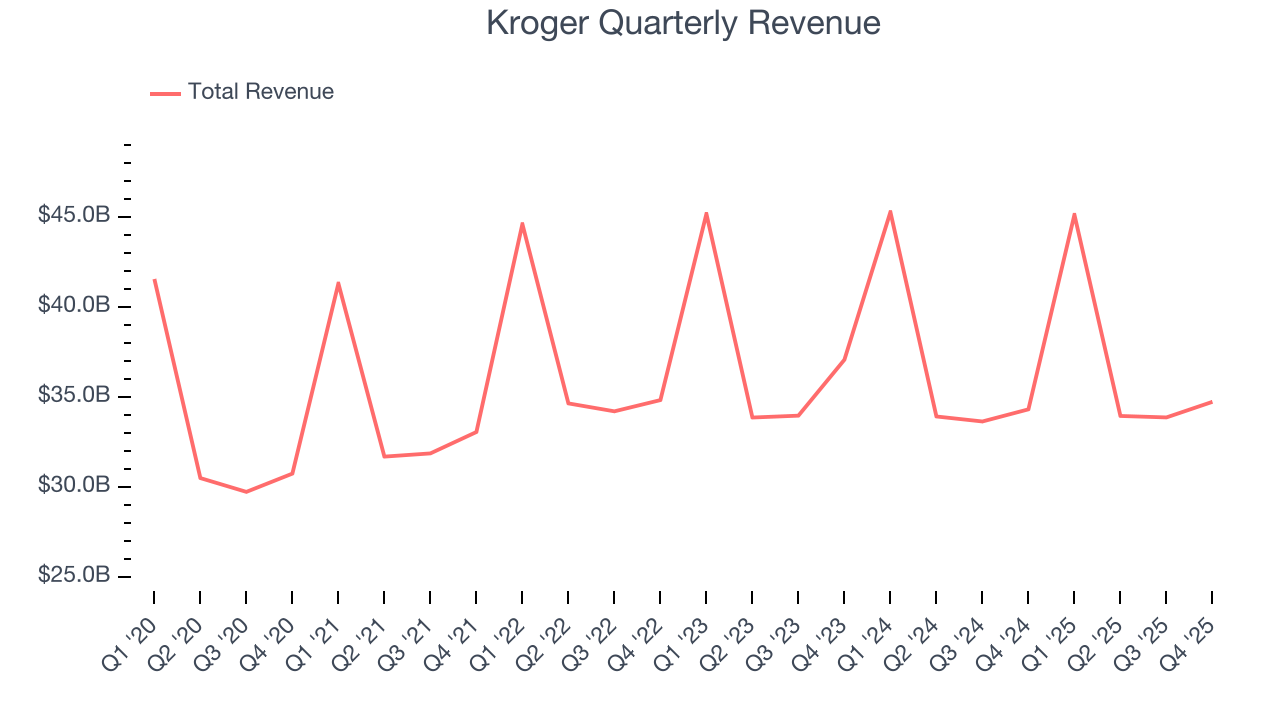

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $147.6 billion in revenue over the past 12 months, Kroger is a behemoth in the consumer retail sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because there is only so much real estate to build new stores, placing a ceiling on its growth. To accelerate sales, Kroger likely needs to optimize its pricing or lean into international expansion.

As you can see below, Kroger struggled to increase demand as its $147.6 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it didn’t open many new stores.

This quarter, Kroger’s revenue grew by 1.2% year on year to $34.73 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.8% over the next 12 months. Although this projection suggests its newer products will spur better top-line performance, it is still below average for the sector.

6. Store Performance

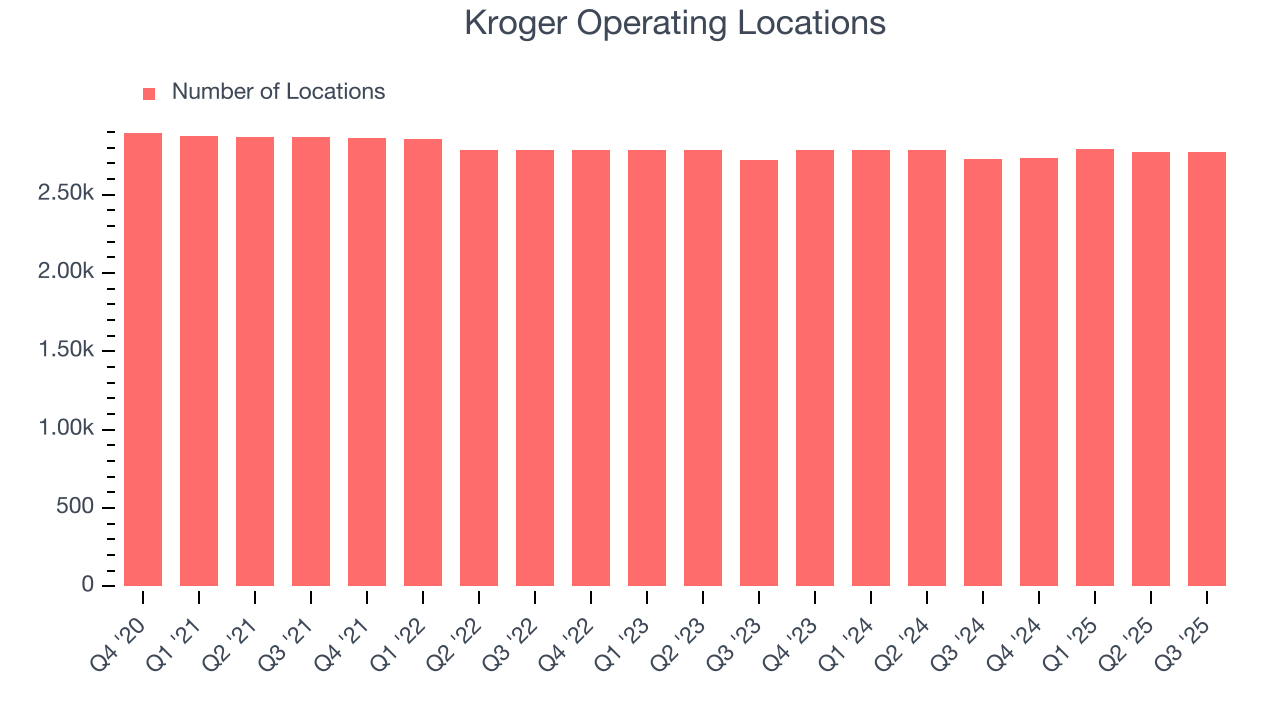

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Kroger has kept its store count flat over the last two years while other consumer retail businesses have opted for growth.

When a retailer keeps its store footprint steady, it usually means demand is stable and it’s focusing on operational efficiency to increase profitability.

Note that Kroger reports its store count intermittently, so some data points are missing in the chart below.

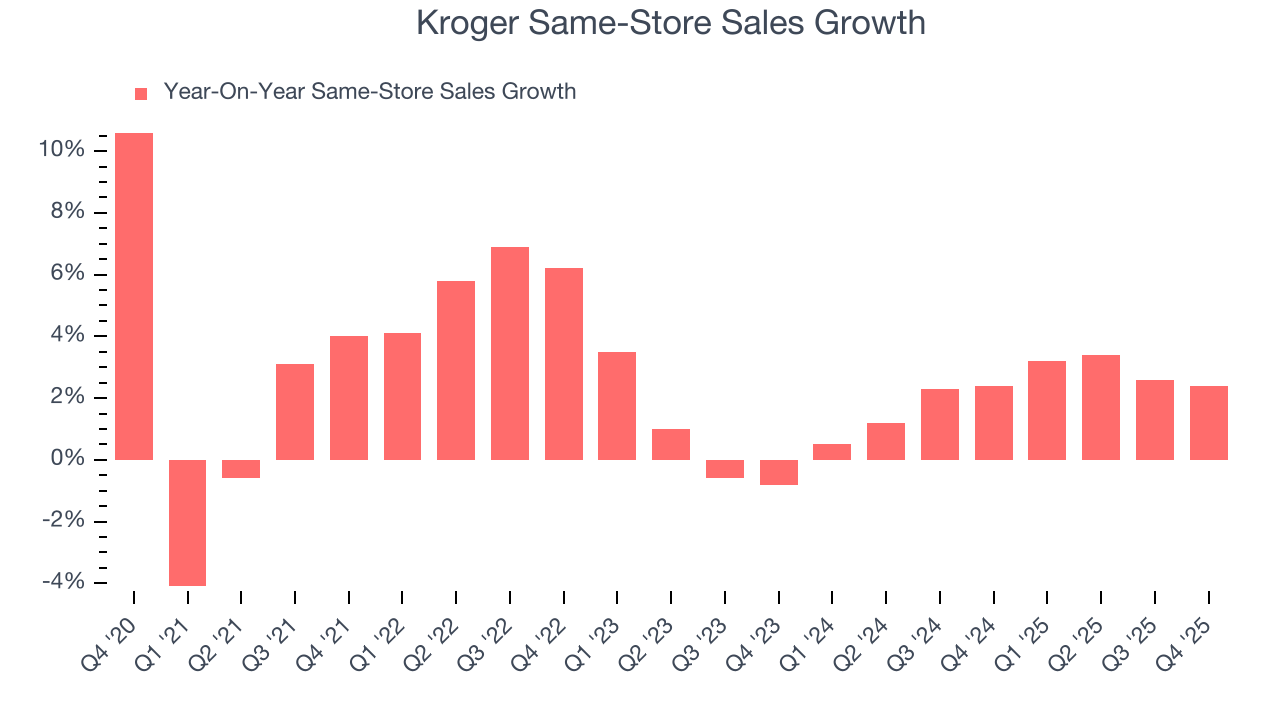

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Kroger’s demand rose over the last two years and slightly outpaced the industry. On average, the company’s same-store sales have grown by 2.3% per year. Given its flat store base over the same period, this performance stems from not only increased foot traffic at existing locations but also higher e-commerce sales as demand shifts from in-store to online.

In the latest quarter, Kroger’s same-store sales rose 2.4% year on year. This performance was more or less in line with its historical levels.

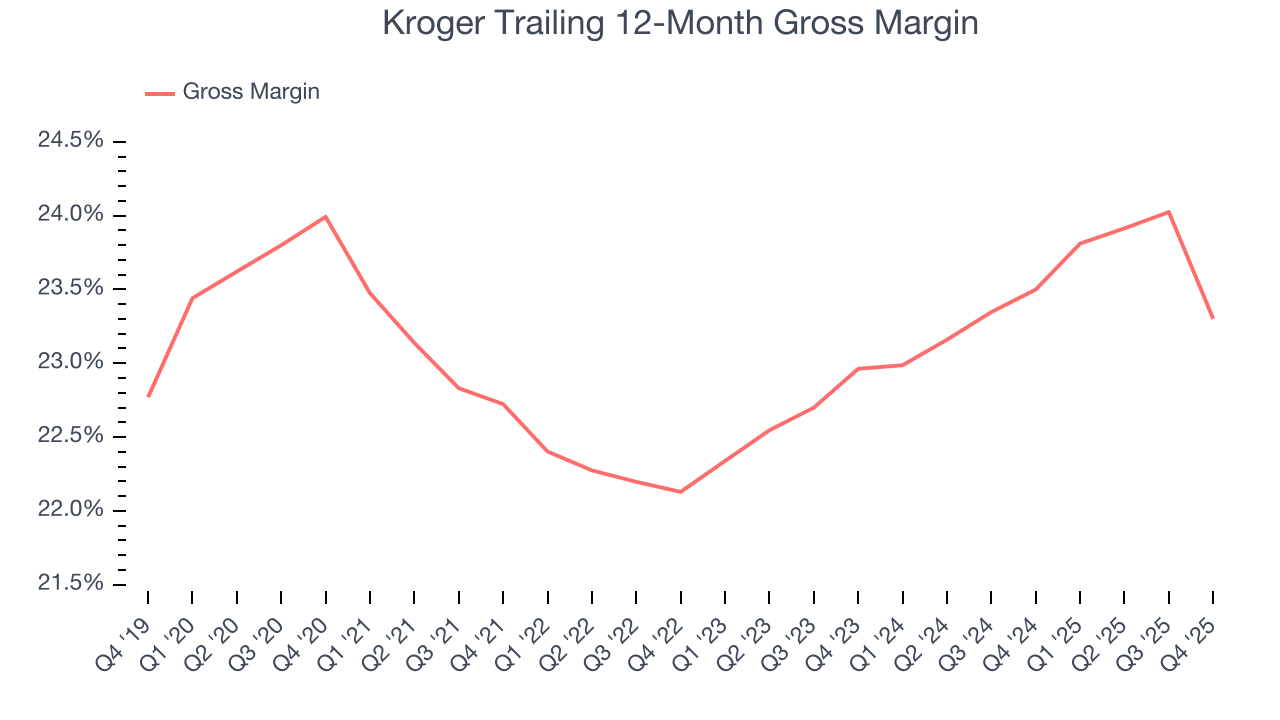

7. Gross Margin & Pricing Power

Kroger has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 23.4% gross margin over the last two years.

Non-discretionary retailers, however, must be viewed through a different lens because they compete on the lowest price, sell products easily found elsewhere, and have high transportation costs to move goods. These dynamics lead to structurally lower gross margins, so the best metrics to assess them are free cash flow margin, operating leverage, and profit volatility, which account for their scale advantages and non-cyclical demand.

This quarter, Kroger’s gross profit margin was 23.4%, down 3.1 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

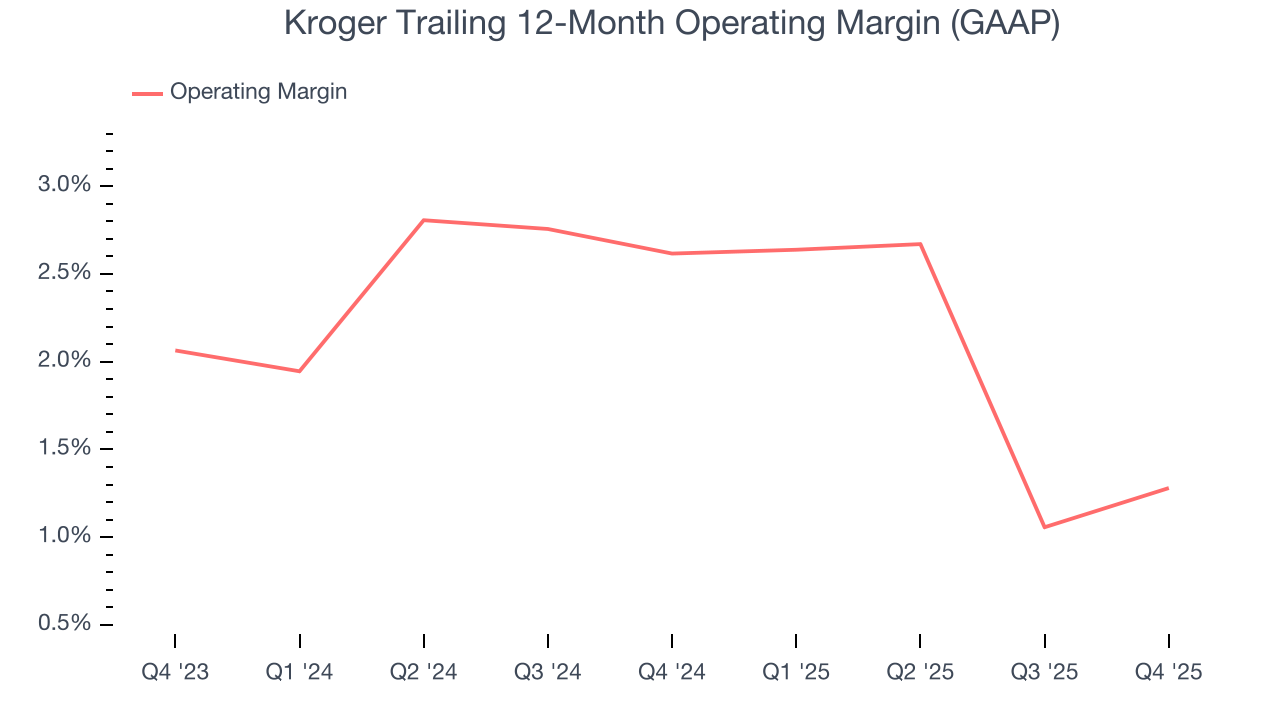

8. Operating Margin

Kroger was profitable over the last two years but held back by its large cost base. Its average operating margin of 1.9% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Kroger’s operating margin decreased by 1.3 percentage points over the last year. Kroger’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Kroger generated an operating margin profit margin of 3.6%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

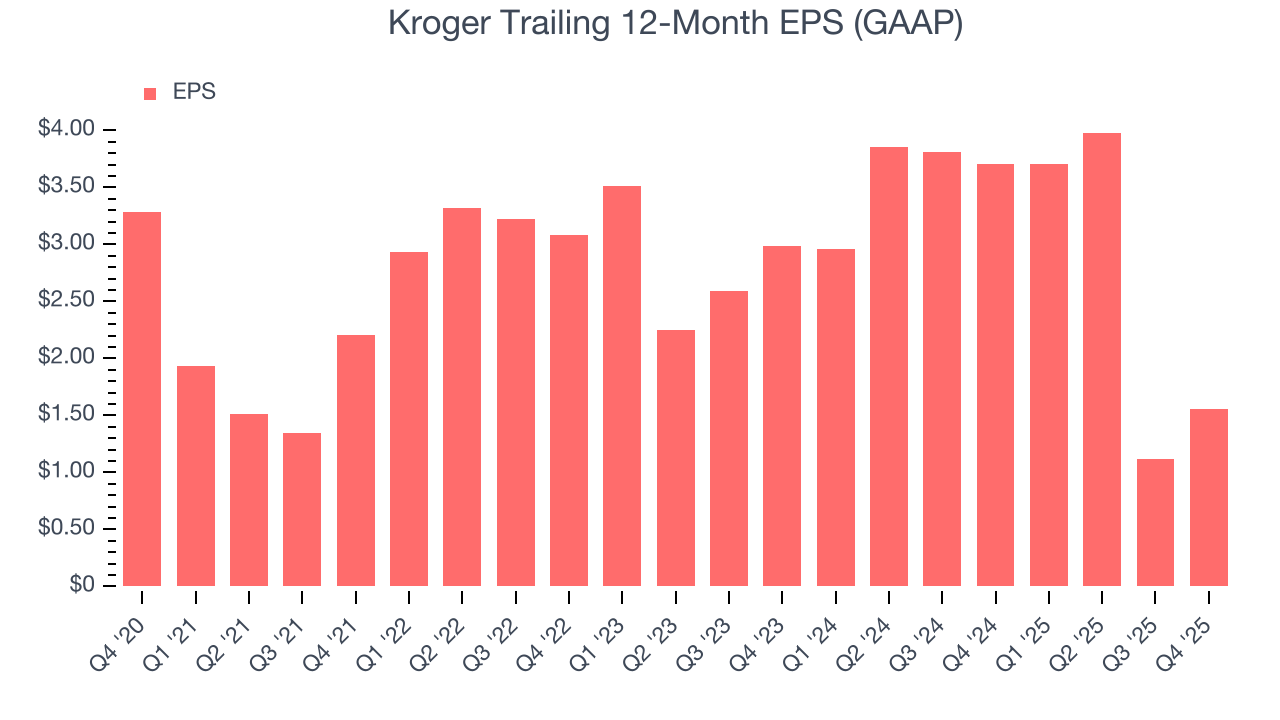

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Kroger, its EPS declined by 20.4% annually over the last three years while its revenue was flat. We can see the difference stemmed from higher interest expenses or taxes as the company actually improved its operating margin and repurchased its shares during this time.

In Q4, Kroger reported EPS of $1.35, up from $0.91 in the same quarter last year. This print beat analysts’ estimates by 5.7%. Over the next 12 months, Wall Street expects Kroger’s full-year EPS of $1.55 to grow 240%.

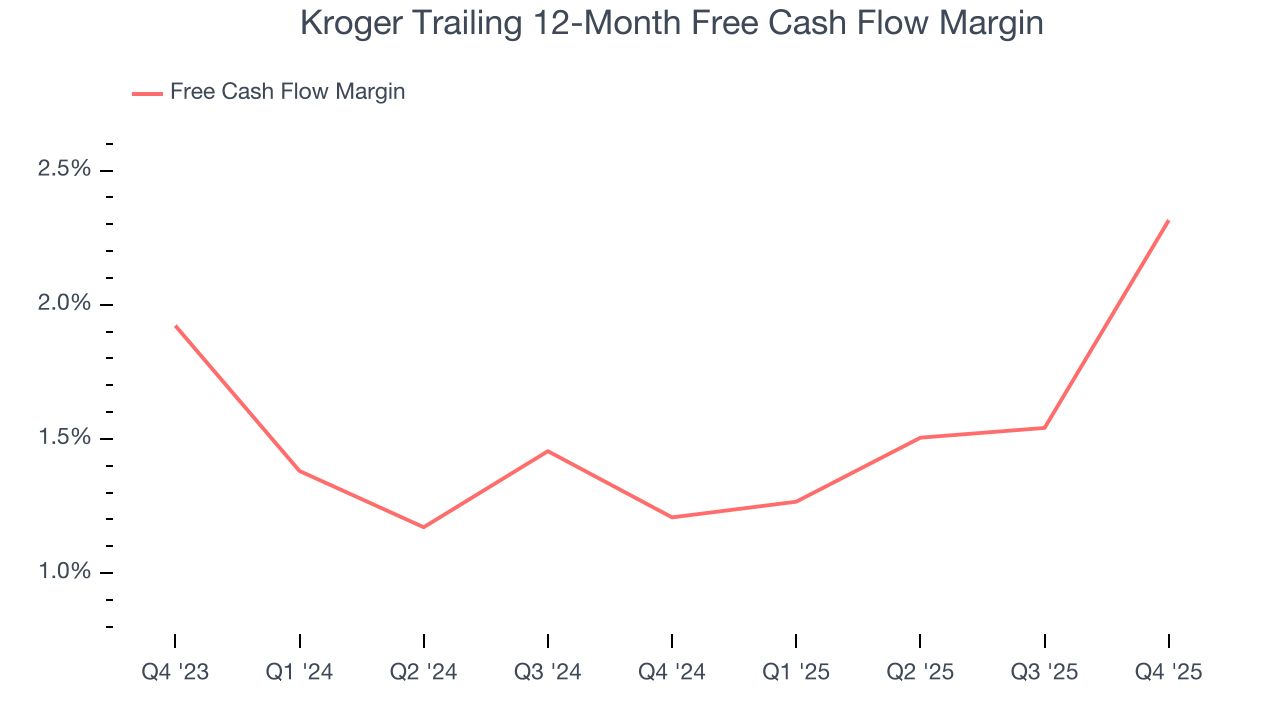

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Kroger has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 1.8%, below what we’d expect for a consumer retail business.

Taking a step back, an encouraging sign is that Kroger’s margin expanded by 1.1 percentage points over the last year. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Kroger’s free cash flow clocked in at $1.67 billion in Q4, equivalent to a 4.8% margin. This result was good as its margin was 3.3 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Kroger historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 12.4%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

12. Balance Sheet Assessment

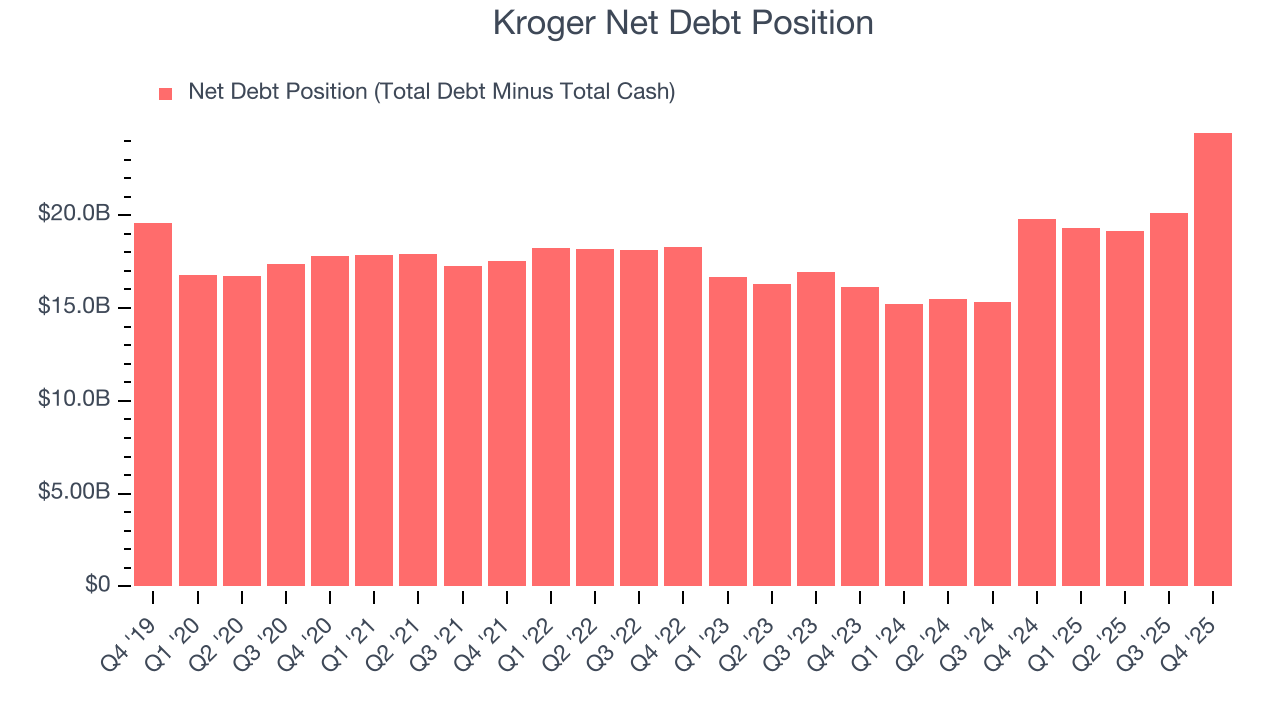

Kroger reported $228 million of cash and $24.68 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $7.51 billion of EBITDA over the last 12 months, we view Kroger’s 3.3× net-debt-to-EBITDA ratio as safe. We also see its $639 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Kroger’s Q4 Results

It was good to see Kroger narrowly top analysts’ gross margin expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter was mixed. The stock remained flat at $67.47 immediately following the results.

14. Is Now The Time To Buy Kroger?

Updated: March 10, 2026 at 1:38 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Kroger.

Kroger’s business quality ultimately falls short of our standards. To kick things off, its revenue has declined over the last three years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its gross margins make it more challenging to reach positive operating profits compared to other consumer retail businesses. On top of that, its declining EPS over the last three years makes it a less attractive asset to the public markets.

Kroger’s P/E ratio based on the next 12 months is 14.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $74.38 on the company (compared to the current share price of $73.63).