Montrose (MEG)

We’d invest in Montrose. It’s not only rapidly winning market share but also boasts impressive unit economics, a winning formula.― StockStory Analyst Team

1. News

2. Summary

Why We Like Montrose

Founded to protect a tree-lined two-lane road, Montrose (NYSE:MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

- Annual revenue growth of 20.4% over the past five years was outstanding, reflecting market share gains this cycle

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 106% outpaced its revenue gains

- Offerings are difficult to replicate at scale and lead to a top-tier gross margin of 37.7%

Montrose is a market leader. The price seems reasonable when considering its quality, so this might be a prudent time to invest in some shares.

Why Is Now The Time To Buy Montrose?

Montrose is trading at $21.11 per share, or 16.1x forward P/E. Most industrials companies are more expensive, so we think Montrose is a good deal when considering its quality characteristics.

Where you buy a stock impacts returns. Our analysis shows that business quality is a much bigger determinant of market outperformance over the long term compared to entry price, but getting a good deal on a stock certainly isn’t a bad thing.

3. Montrose (MEG) Research Report: Q4 CY2025 Update

Environmental services provider Montrose (NYSE:MEG) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 2.2% year on year to $193.3 million. The company’s full-year revenue guidance of $870 million at the midpoint came in 2.6% above analysts’ estimates. Its non-GAAP profit of $0.35 per share was 84.4% above analysts’ consensus estimates.

Montrose (MEG) Q4 CY2025 Highlights:

- Revenue: $193.3 million vs analyst estimates of $188.6 million (2.2% year-on-year growth, 2.5% beat)

- Adjusted EPS: $0.35 vs analyst estimates of $0.19 (84.4% beat)

- Adjusted EBITDA: $23.89 million vs analyst estimates of $23.23 million (12.4% margin, 2.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $127.5 million at the midpoint, above analyst estimates of $125.7 million

- Operating Margin: -1.3%, up from -12.1% in the same quarter last year

- Free Cash Flow Margin: 23.7%, up from 15.7% in the same quarter last year

- Market Capitalization: $799.3 million

Company Overview

Founded to protect a tree-lined two-lane road, Montrose (NYSE:MEG) provides air quality monitoring, environmental laboratory testing, compliance, and environmental consulting services.

Montrose traces its roots back to a community effort to protect local landscapes from a proposed highway. The company has since expanded its service offerings by acquiring environmental consulting and testing firms. Specifically, its acquisition of Enthalpy Analytical, a provider of laboratory testing services for air, water, and soil samples, was crucial for strengthening its environmental lab capabilities. Today, the company’s services help clients manage environmental risks, ensure compliance with regulations, and achieve sustainability goals.

Its expertise includes precise air quality monitoring to measure pollutants and ensure compliance with environmental standards. Through environmental laboratory testing, it analyzes soil, water, and air samples to identify and manage contaminants. Additionally, Montrose guides clients through environmental laws and regulations. Specifically, it helps obtain necessary permits, fulfill reporting requirements, and maintain alignment with federal, state, and local environmental guidelines.

Montrose serves industries such as oil and gas, helping manage emissions and wastewater. It primarily enters into long-term contracts that involve recurring services over several years such as frequent monitoring and testing. Additionally, Montrose provides project-based services for specific environmental challenges or regulatory requirements.

4. Waste Management

Waste management companies can possess licenses permitting them to handle hazardous materials. Furthermore, many services are performed through contracts and statutorily mandated, non-discretionary, or recurring, leading to more predictable revenue streams. However, regulation can be a headwind, rendering existing services obsolete or forcing companies to invest precious capital to comply with new, more environmentally-friendly rules. Lastly, waste management companies are at the whim of economic cycles. Interest rates, for example, can greatly impact industrial production or commercial projects that create waste and byproducts.

Montrose Environmental Group competes with environmental divisions of larger engineering and consulting firms such as ERM, Ramboll, WSP, AECOM, and Tetra Tech, as well as specialized environmental testing companies like Eurofins and Pace Analytical.

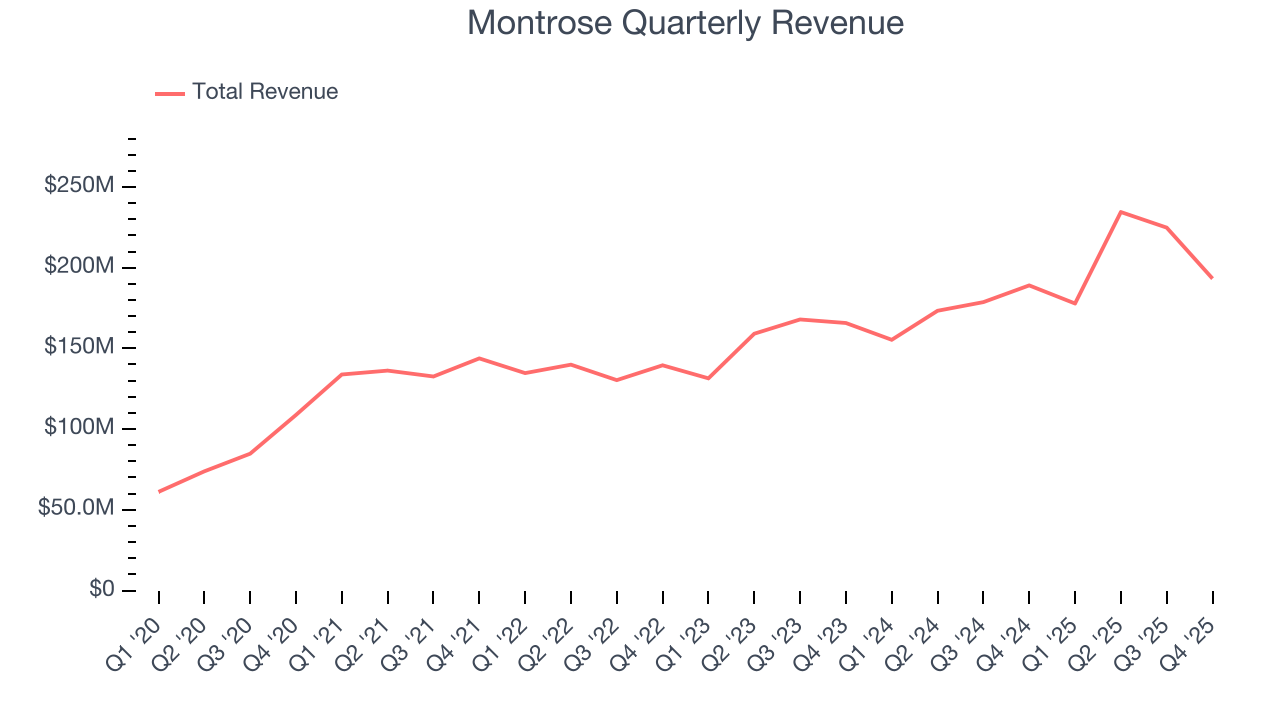

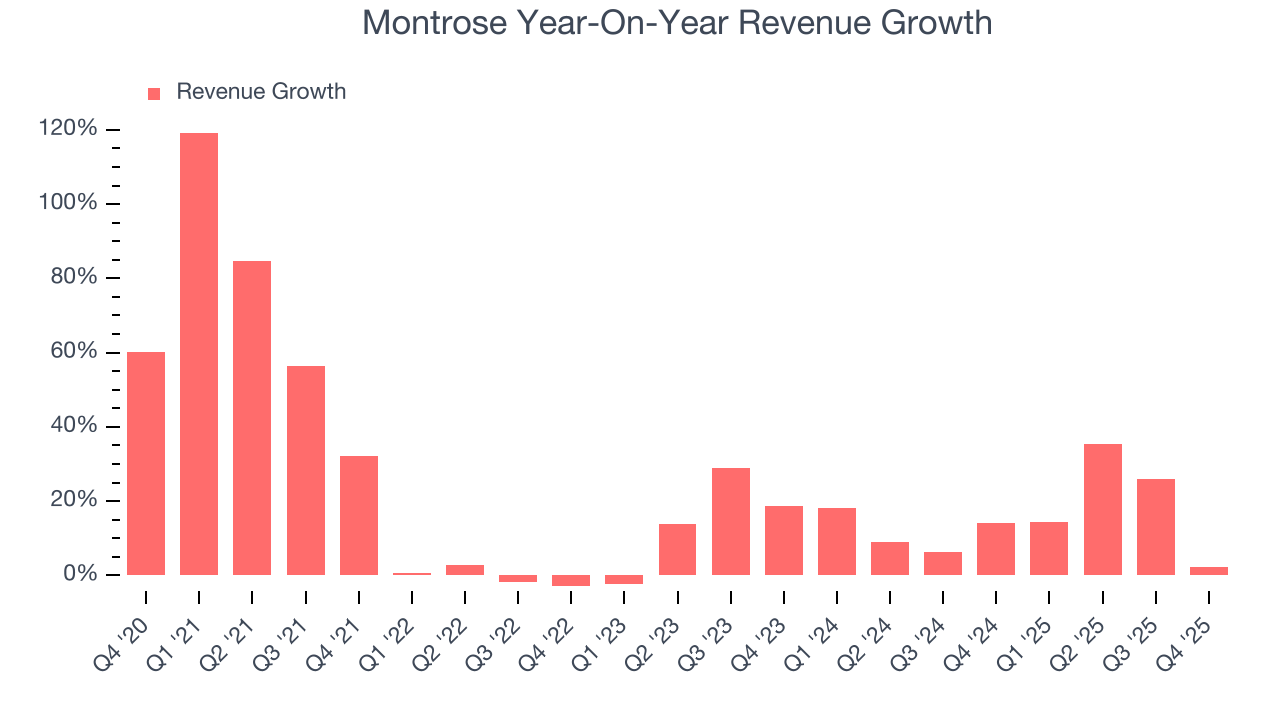

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Montrose grew its sales at an incredible 20.4% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Montrose’s annualized revenue growth of 15.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Montrose reported modest year-on-year revenue growth of 2.2% but beat Wall Street’s estimates by 2.5%.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

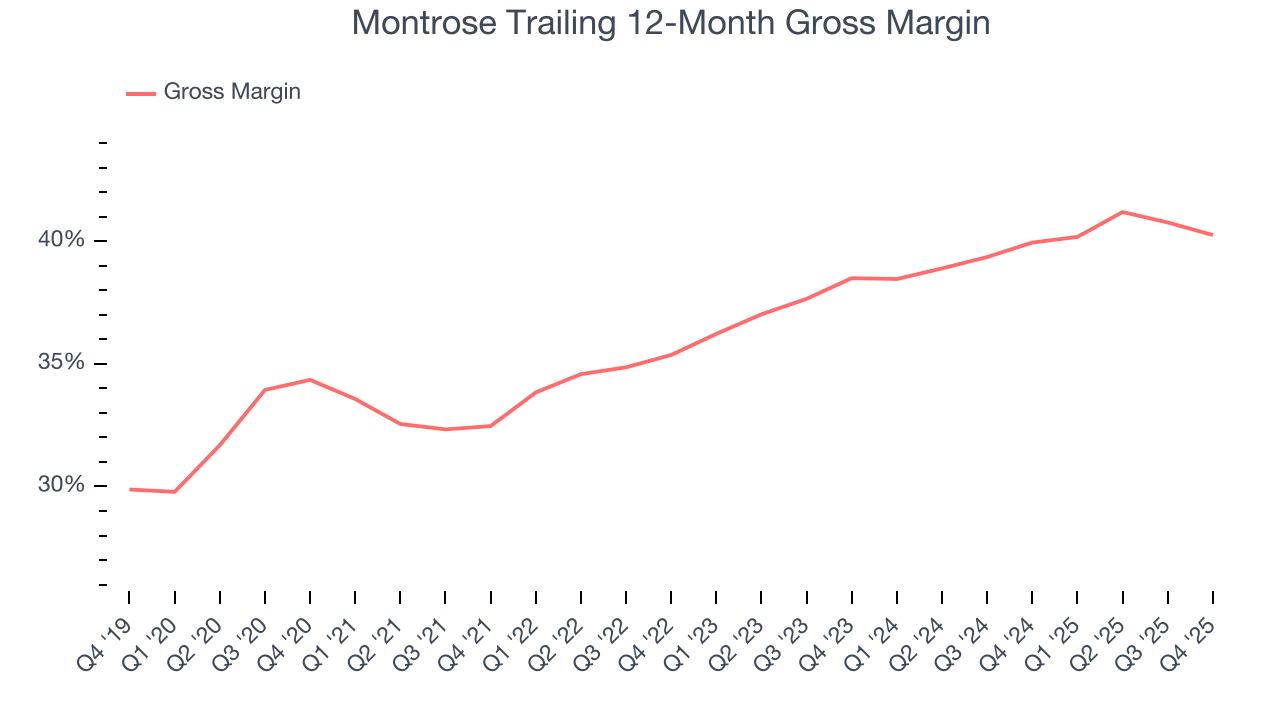

6. Gross Margin & Pricing Power

Montrose’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 37.7% gross margin over the last five years. That means Montrose only paid its suppliers $62.28 for every $100 in revenue.

Montrose produced a 38.6% gross profit margin in Q4 , marking a 2.2 percentage point decrease from 40.8% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

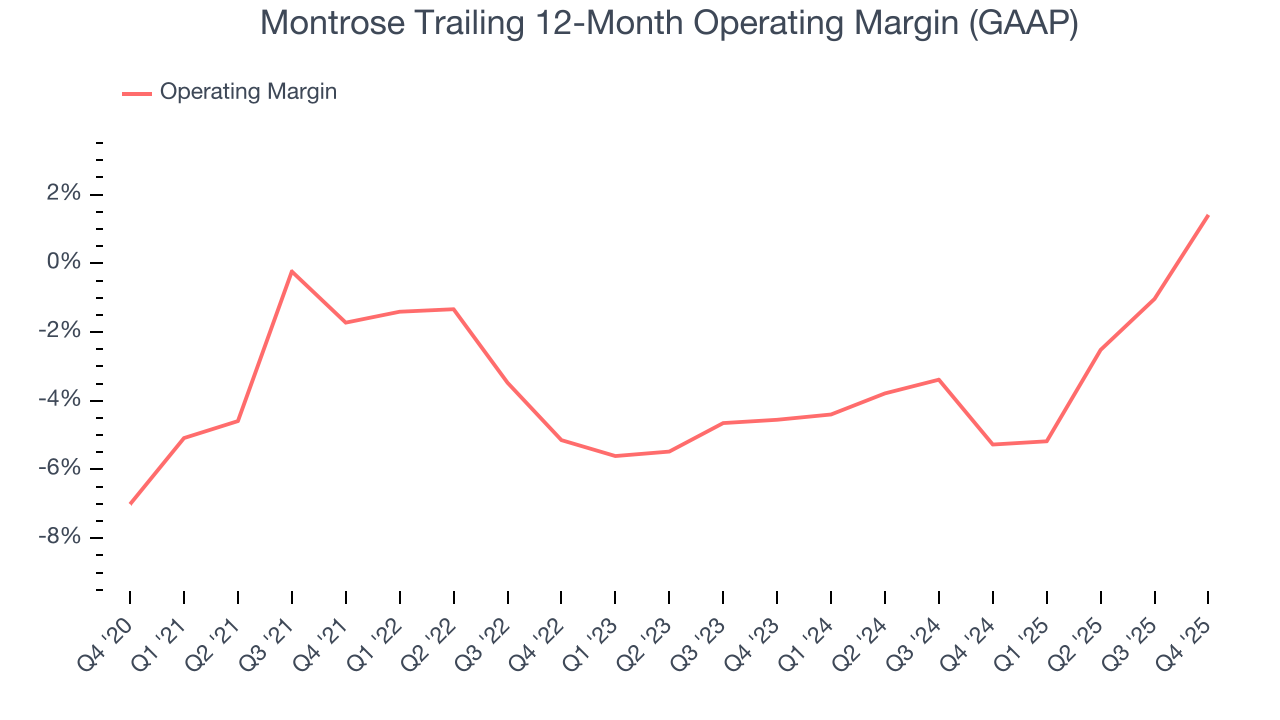

7. Operating Margin

Montrose’s high expenses have contributed to an average operating margin of negative 2.8% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Montrose’s operating margin rose by 3.1 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Montrose generated a negative 1.3% operating margin.

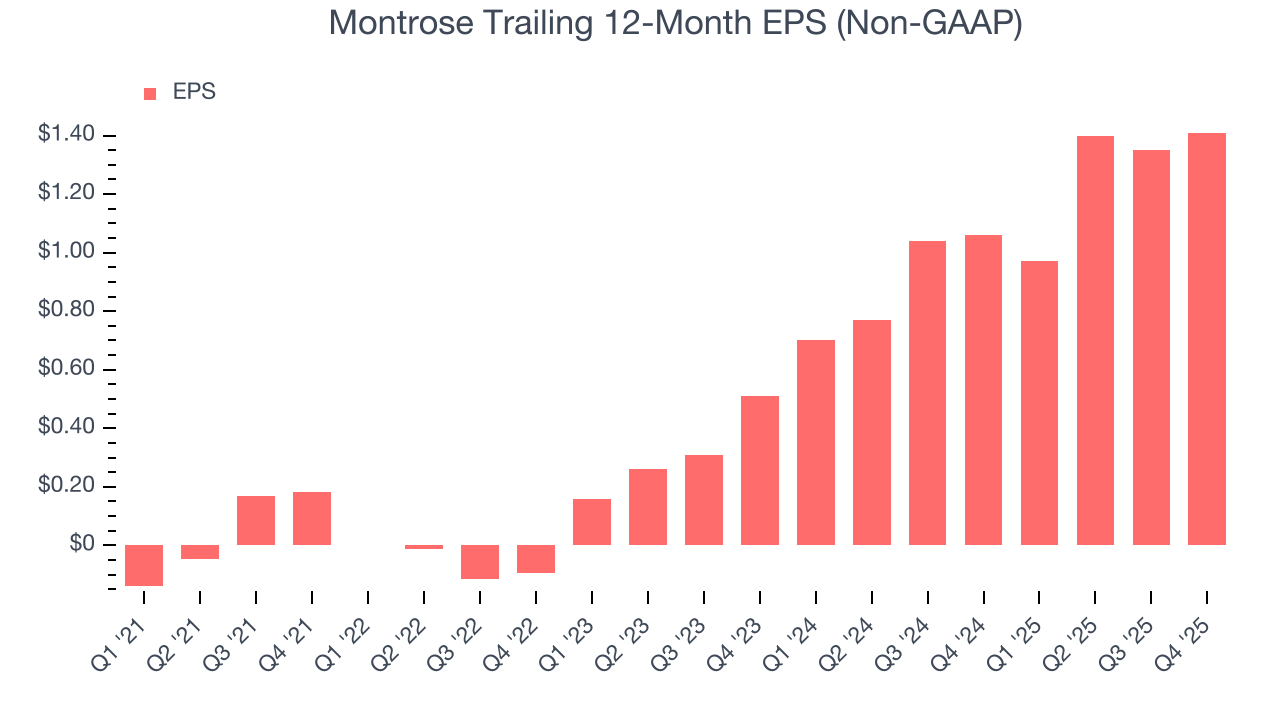

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Montrose’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Montrose’s EPS grew at an astounding 66.3% compounded annual growth rate over the last two years, higher than its 15.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Montrose’s earnings can give us a better understanding of its performance. Montrose’s operating margin has expanded over the last two years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Montrose reported adjusted EPS of $0.35, up from $0.29 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Montrose’s full-year EPS of $1.41 to grow 2%.

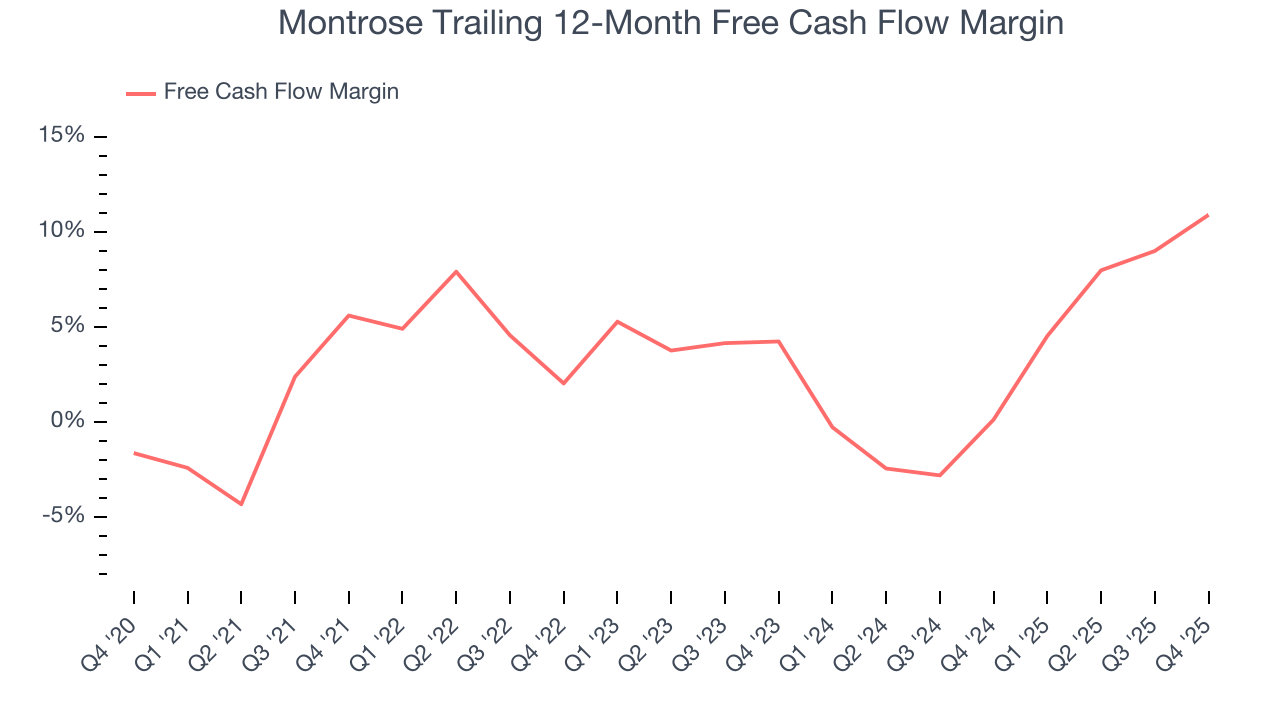

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Montrose has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.9%, subpar for an industrials business.

Taking a step back, an encouraging sign is that Montrose’s margin expanded by 5.3 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Montrose’s free cash flow clocked in at $45.85 million in Q4, equivalent to a 23.7% margin. This result was good as its margin was 8 percentage points higher than in the same quarter last year, building on its favorable historical trend.

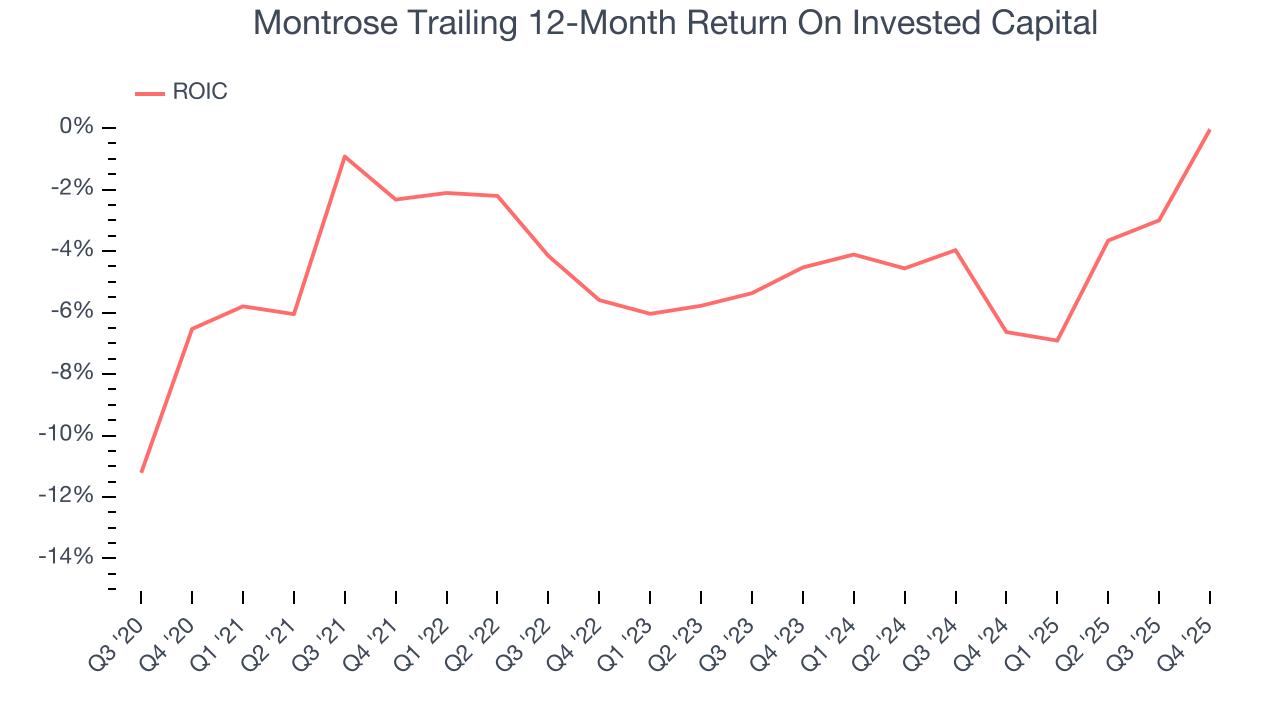

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Montrose has shown solid business quality lately, it struggled to grow profitably in the past. Its five-year average ROIC was negative 3.8%, meaning management lost money while trying to expand the business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Montrose’s ROIC has stayed the same over the last few years. We still think it’s a good business, but if the company wants to reach the next level, it must improve its returns.

11. Balance Sheet Assessment

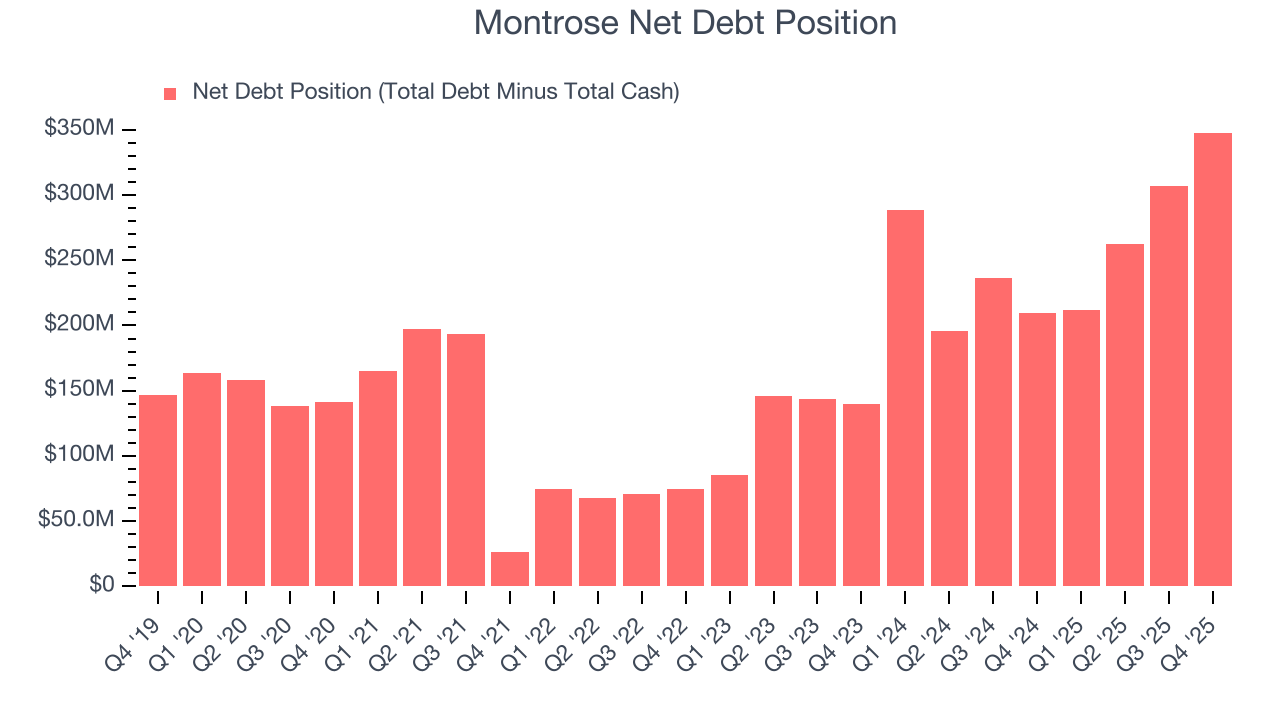

Montrose reported $11.22 million of cash and $359 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $116.2 million of EBITDA over the last 12 months, we view Montrose’s 3.0× net-debt-to-EBITDA ratio as safe. We also see its $21.38 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Montrose’s Q4 Results

It was good to see Montrose beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 7.5% to $25.10 immediately following the results.

13. Is Now The Time To Buy Montrose?

Updated: March 27, 2026 at 10:10 PM EDT

Before making an investment decision, investors should account for Montrose’s business fundamentals and valuation in addition to what happened in the latest quarter.

Montrose is a high-quality business worth owning. First of all, the company’s revenue growth was exceptional over the last five years. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its rising cash profitability gives it more optionality. On top of that, Montrose’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Montrose’s P/E ratio based on the next 12 months is 16.1x. Analyzing the industrials landscape today, Montrose’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $35.67 on the company (compared to the current share price of $21.11), implying they see 69% upside in buying Montrose in the short term.