Snowflake (SNOW)

We’re firm believers in Snowflake. Its high growth and retention show customers can’t stop spending money on its mission-critical products.― StockStory Analyst Team

1. News

2. Summary

Why We Like Snowflake

Named after the unique architecture of its data warehouse which resembles a snowflake pattern, Snowflake (NYSE:SNOW) provides a cloud-based data platform that enables organizations to consolidate, analyze, and share data across multiple cloud providers.

- Winning new contracts that can potentially increase in value as its billings growth has averaged 36% over the last year

- Revenue outlook for the upcoming 12 months is outstanding and shows it’s on track to gain market share

- Customers use its software daily and increase their spending every year, as seen in its 125% net revenue retention rate

Snowflake is a top-tier company. The valuation looks fair when considering its quality, so this might be an opportune time to invest in some shares.

Why Is Now The Time To Buy Snowflake?

At $168.82 per share, Snowflake trades at 10.1x forward price-to-sales. While this multiple is higher than most software companies, we think the valuation is fair given its quality characteristics.

By definition, where you buy a stock impacts returns. But according to our work on the topic, business quality is a much bigger determinant of market outperformance over the long term compared to entry price.

3. Snowflake (SNOW) Research Report: Q4 CY2025 Update

Cloud data platform provider Snowflake (NYSE:SNOW) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 30.1% year on year to $1.28 billion. Its non-GAAP profit of $0.32 per share was 17.8% above analysts’ consensus estimates.

Snowflake (SNOW) Q4 CY2025 Highlights:

- Revenue: $1.28 billion vs analyst estimates of $1.26 billion (30.1% year-on-year growth, 2.1% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.27 (17.8% beat)

- Adjusted Operating Income: $139.2 million vs analyst estimates of $90.49 million (10.8% margin, 53.8% beat)

- Product Revenue Guidance for Q1 CY2026 is $1.26 billion at the midpoint

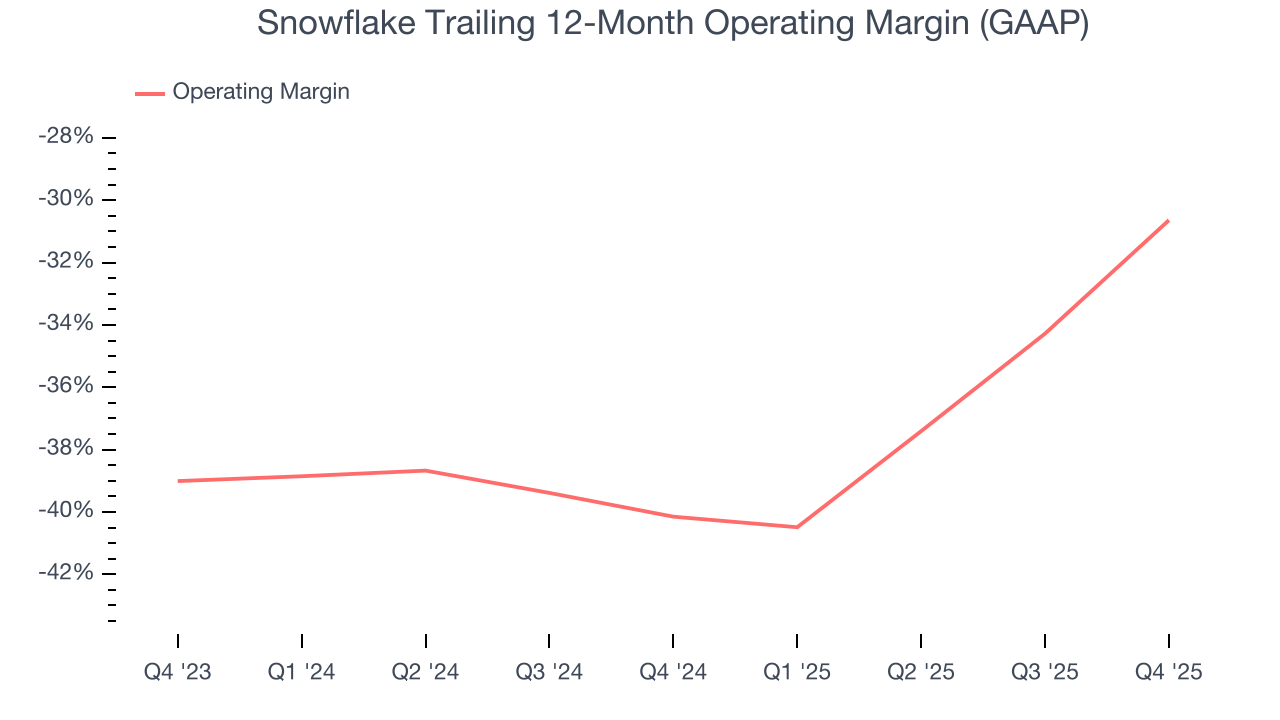

- Operating Margin: -24.8%, up from -39.2% in the same quarter last year

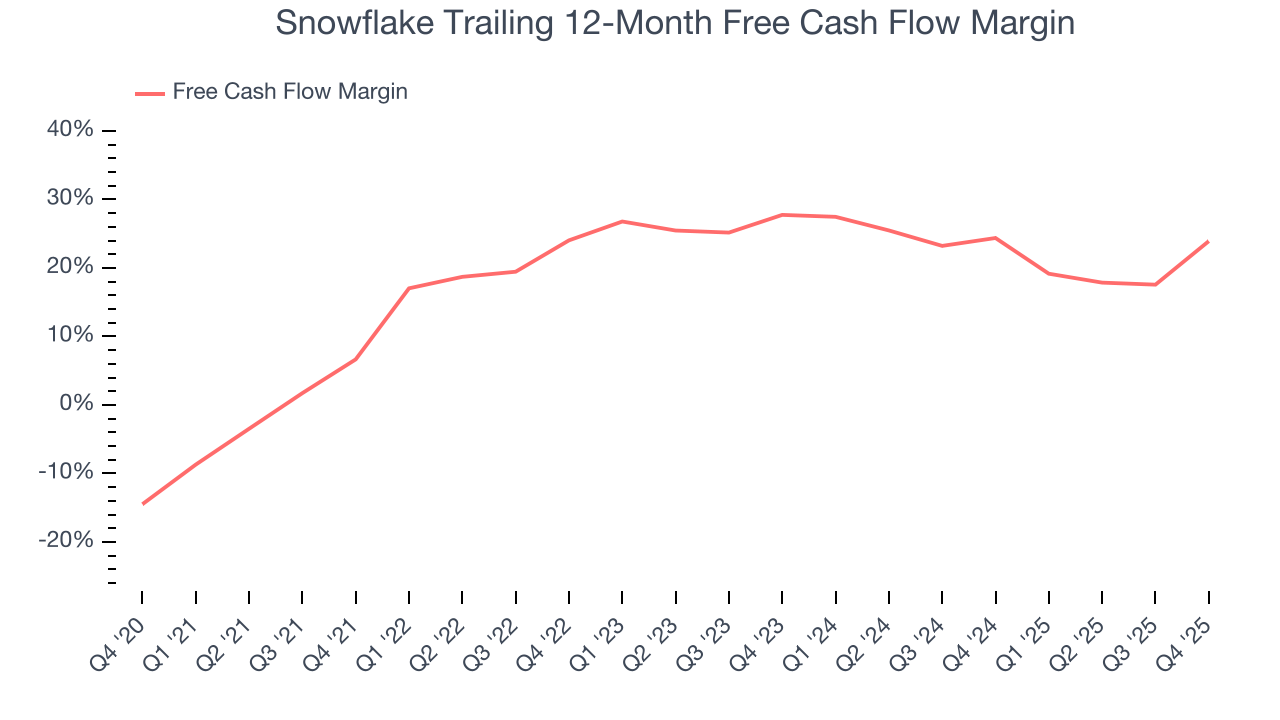

- Free Cash Flow Margin: 59.6%, up from 9.4% in the previous quarter

- Customers: 733 customers paying more than $1 million annually

- Net Revenue Retention Rate: 125%, in line with the previous quarter

- Billings: $2.21 billion at quarter end, up 38.6% year on year

- Market Capitalization: $55.11 billion

Company Overview

Named after the unique architecture of its data warehouse which resembles a snowflake pattern, Snowflake (NYSE:SNOW) provides a cloud-based data platform that enables organizations to consolidate, analyze, and share data across multiple cloud providers.

Snowflake's platform solves the persistent challenge of data silos by unifying diverse data types—structured, semi-structured, and unstructured—into a single source of truth. This architecture consists of three independent but integrated layers: storage for maintaining data, compute for processing queries, and cloud services for orchestrating operations. The platform operates across AWS, Microsoft Azure, and Google Cloud with 40 regional deployments worldwide, giving customers flexibility and global reach.

Unlike traditional data solutions, Snowflake uses a consumption-based pricing model where customers pay only for the computing resources they use. This approach eliminates upfront infrastructure costs and ongoing maintenance headaches. The platform supports multiple concurrent workloads—from data warehousing and data lakes to AI/machine learning and application development—all while maintaining consistent security and governance.

A manufacturing company might use Snowflake to integrate production data, supply chain information, and customer feedback to optimize operations. The platform's sharing capabilities also allow organizations to securely exchange data with partners or monetize data products through the Snowflake Marketplace without moving or copying the underlying information. This creates network effects as more customers join the ecosystem, increasing the platform's overall value proposition for all participants.

4. Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

Snowflake competes primarily with cloud data warehouse offerings from major cloud providers including Amazon Web Services (Amazon Redshift), Microsoft Azure (Azure Synapse Analytics), and Google Cloud Platform (BigQuery). Other competitors include traditional data warehouse vendors like Oracle, IBM, and Teradata, as well as newer cloud-native analytics platforms like Databricks.

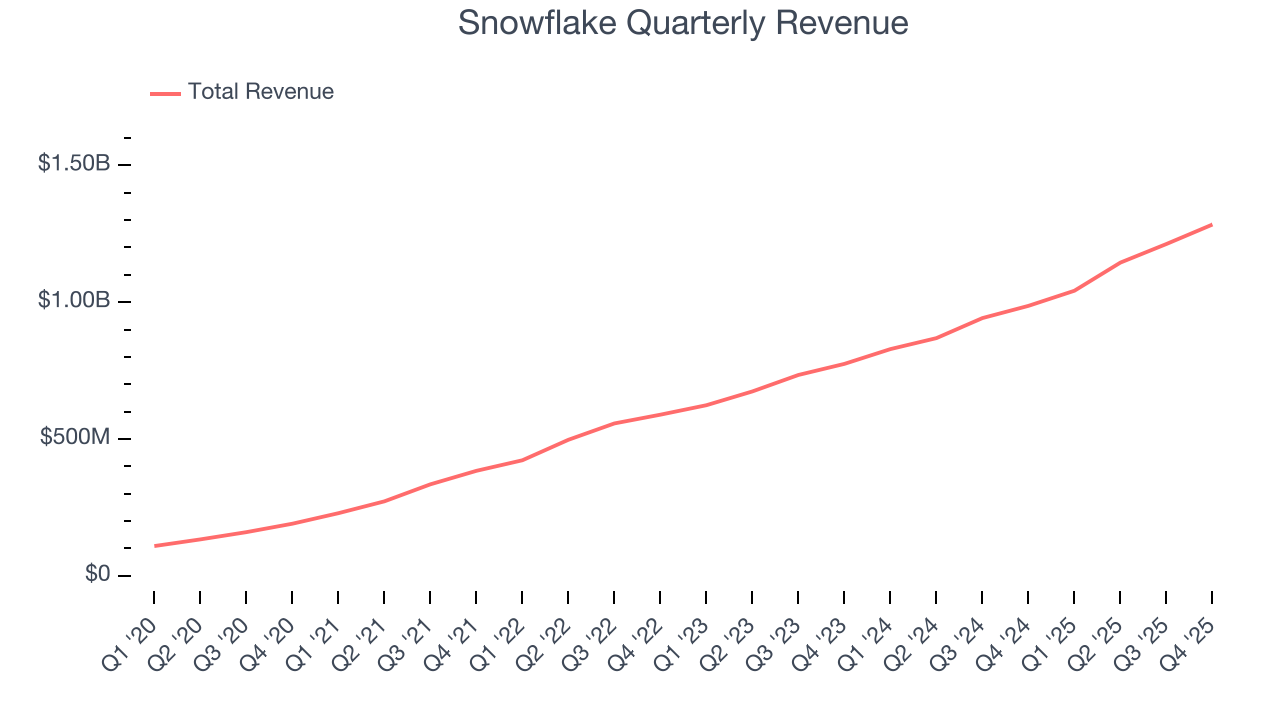

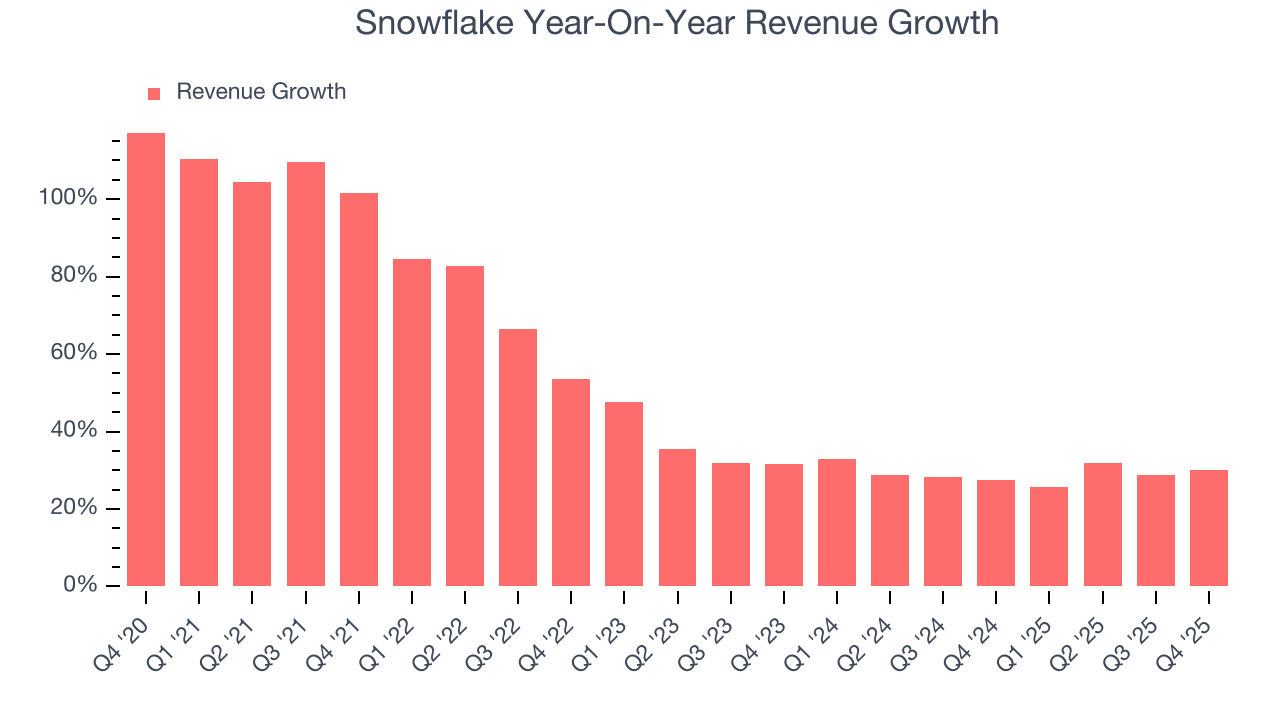

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, Snowflake grew its sales at an incredible 51.2% compounded annual growth rate. Its growth surpassed the average software company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Snowflake’s annualized revenue growth of 29.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Snowflake reported wonderful year-on-year revenue growth of 30.1%, and its $1.28 billion of revenue exceeded Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to grow 23.5% over the next 12 months, a deceleration versus the last two years. Still, this projection is noteworthy and indicates the market sees success for its products and services.

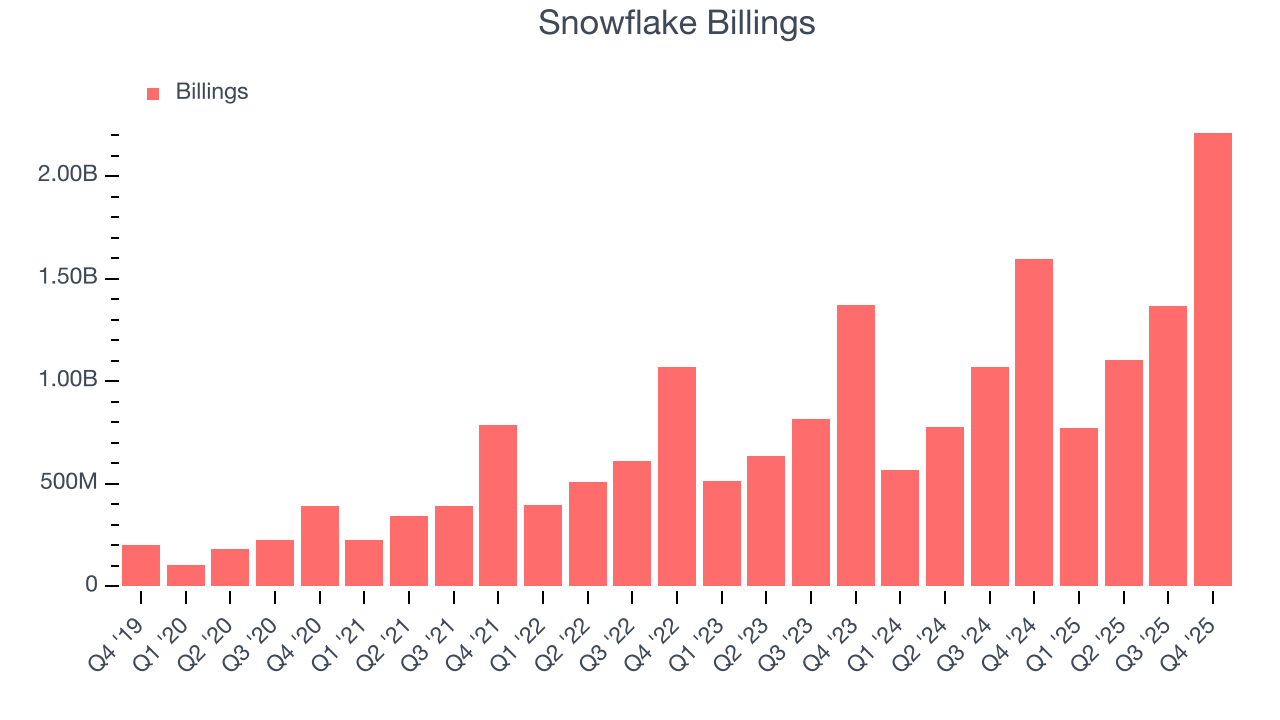

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Snowflake’s billings punched in at $2.21 billion in Q4, and over the last four quarters, its growth was fantastic as it averaged 36% year-on-year increases. This alternate topline metric grew faster than total sales, meaning the company collects cash upfront and then recognizes the revenue over the length of its contracts - a boost for its liquidity and future revenue prospects.

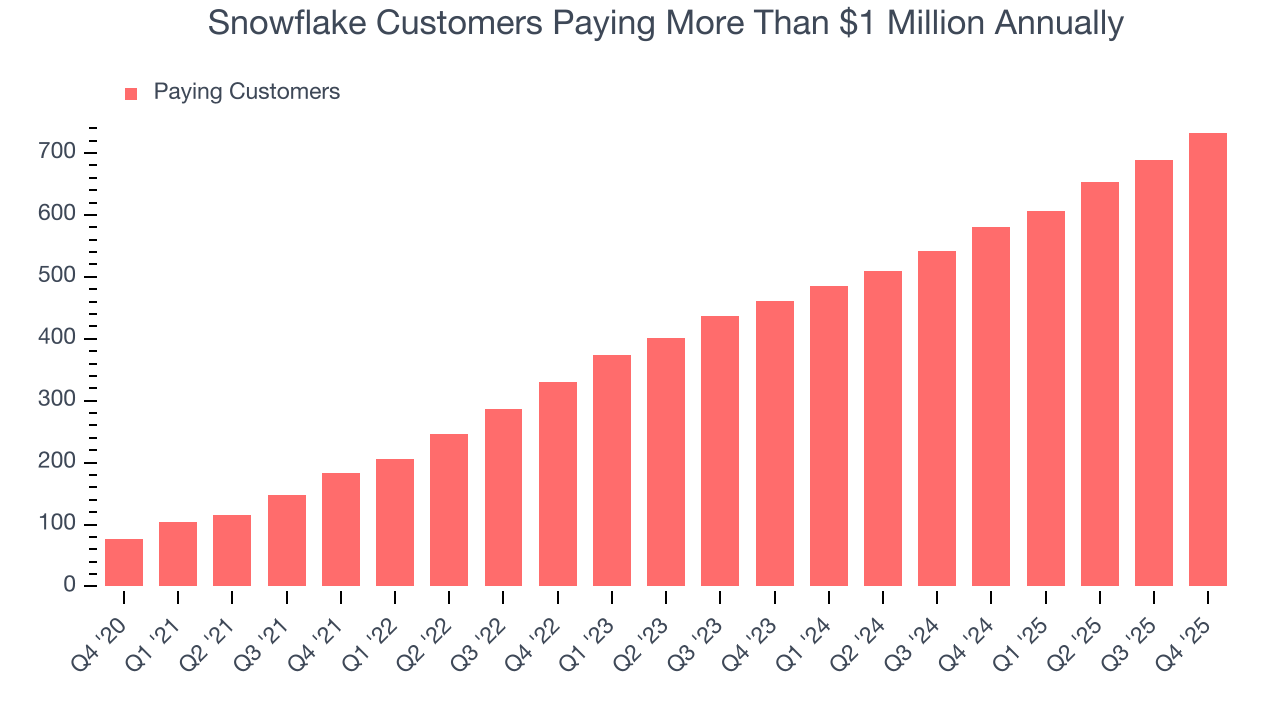

7. Enterprise Customer Base

This quarter, Snowflake reported 733 enterprise customers paying more than $1 million annually, an increase of 45 from the previous quarter. That’s quite a bit more contract wins than last quarter and quite a bit above what we’ve observed over the previous year. Shareholders should take this as an indication that Snowflake’s go-to-market strategy is working well.

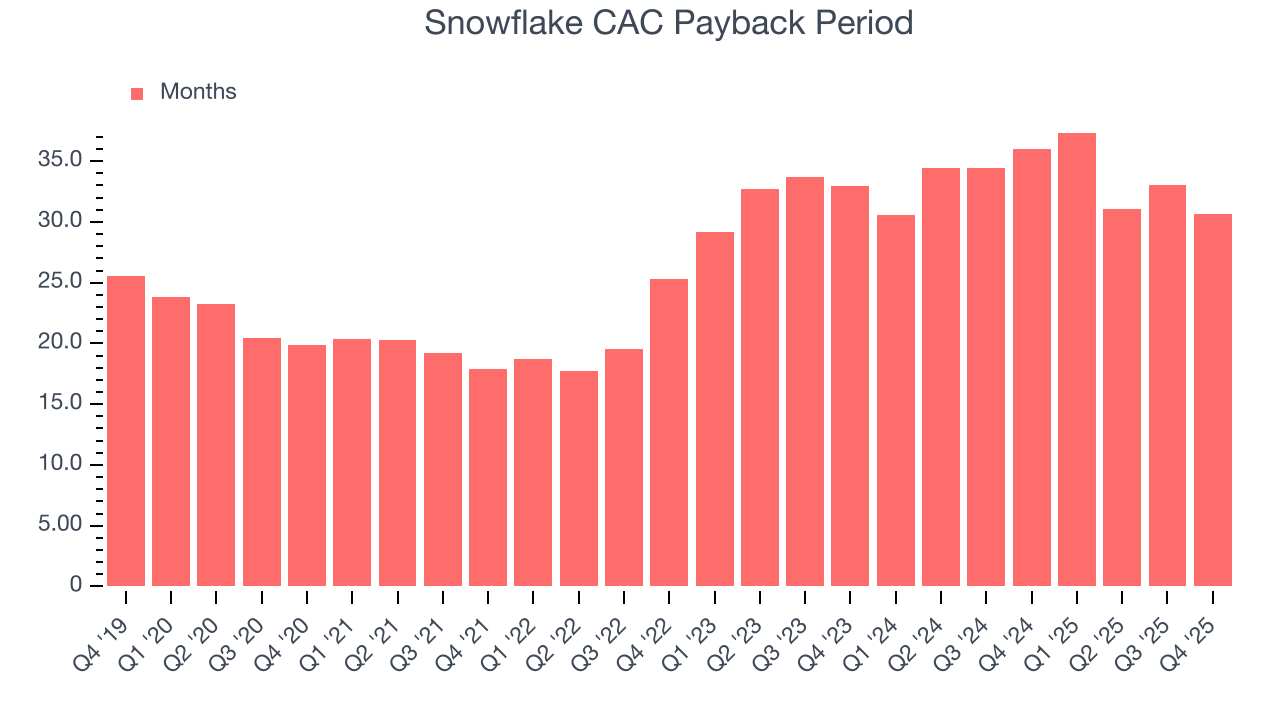

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Snowflake is quite efficient at acquiring new customers, and its CAC payback period checked in at 30.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a strong brand reputation, giving it more resources pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

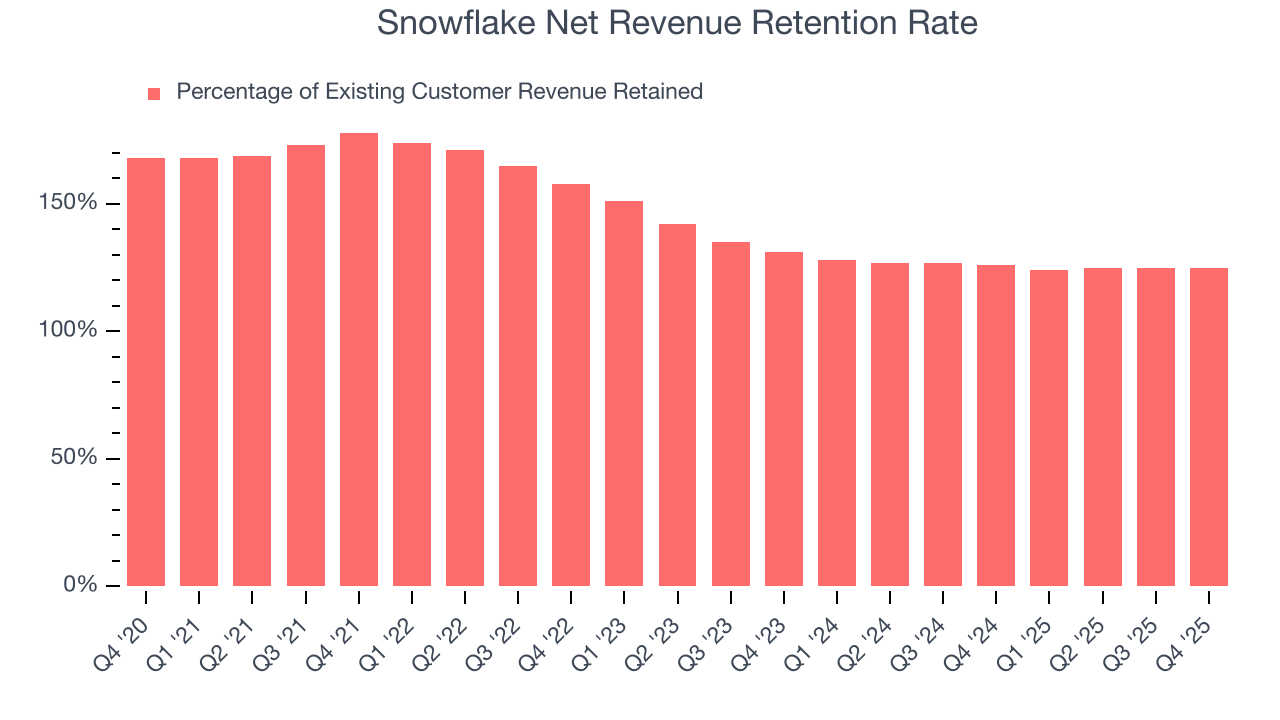

9. Customer Retention

One of the best parts about the software-as-a-service business model (and a reason why they trade at high valuation multiples) is that customers typically spend more on a company’s products and services over time.

Snowflake’s net revenue retention rate, a key performance metric measuring how much money existing customers from a year ago are spending today, was 125% in Q4. This means Snowflake would’ve grown its revenue by 24.8% even if it didn’t win any new customers over the last 12 months.

Snowflake has a good net retention rate, proving that customers are satisfied with its software and getting more value from it over time, which is always great to see.

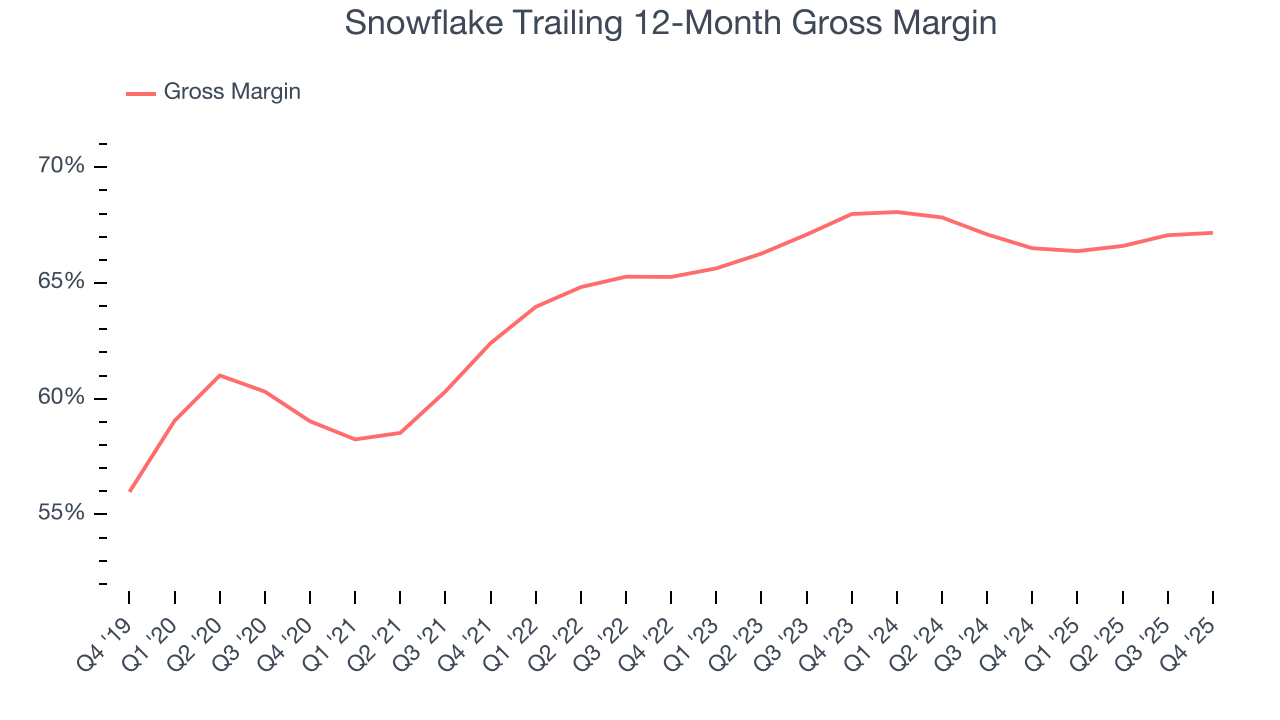

10. Gross Margin & Pricing Power

For software companies like Snowflake, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Snowflake’s gross margin is worse than the software industry average, giving it less room than its competitors to hire new talent that can expand its products and services. As you can see below, it averaged a 67.2% gross margin over the last year. Said differently, Snowflake had to pay a chunky $32.83 to its service providers for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Snowflake has seen gross margins decline by 0.8 percentage points over the last 2 year, which is poor compared to software peers.

Snowflake produced a 66.8% gross profit margin in Q4, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

11. Operating Margin

While many software businesses point investors to their adjusted profits, which exclude stock-based compensation (SBC), we prefer GAAP operating margin because SBC is a legitimate expense used to attract and retain talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Snowflake’s expensive cost structure has contributed to an average operating margin of negative 30.6% over the last year. This happened because the company spent loads of money to capture market share. As seen in its fast revenue growth, the aggressive strategy has paid off so far, and Wall Street’s estimates suggest the party will continue. We tend to agree and believe the business has a good chance of reaching profitability upon scale.

Over the last two years, Snowflake’s expanding sales gave it operating leverage as its margin rose by 9.5 percentage points. Still, it will take much more for the company to reach long-term profitability.

Snowflake’s operating margin was negative 24.8% this quarter.

12. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Snowflake has shown robust cash profitability, driven by its cost-effective customer acquisition strategy that enables it to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 23.9% over the last year, quite impressive for a software business. The divergence from its underwhelming operating margin stems from the add-back of non-cash charges like depreciation and stock-based compensation. GAAP operating profit expenses these line items, but free cash flow does not.

Snowflake’s free cash flow clocked in at $765.1 million in Q4, equivalent to a 59.6% margin. This result was good as its margin was 17.5 percentage points higher than in the same quarter last year. Its cash profitability was also above its one-year level, and we hope the company can build on this trend.

Over the next year, analysts’ consensus estimates show they’re expecting Snowflake’s free cash flow margin of 23.9% for the last 12 months to remain the same.

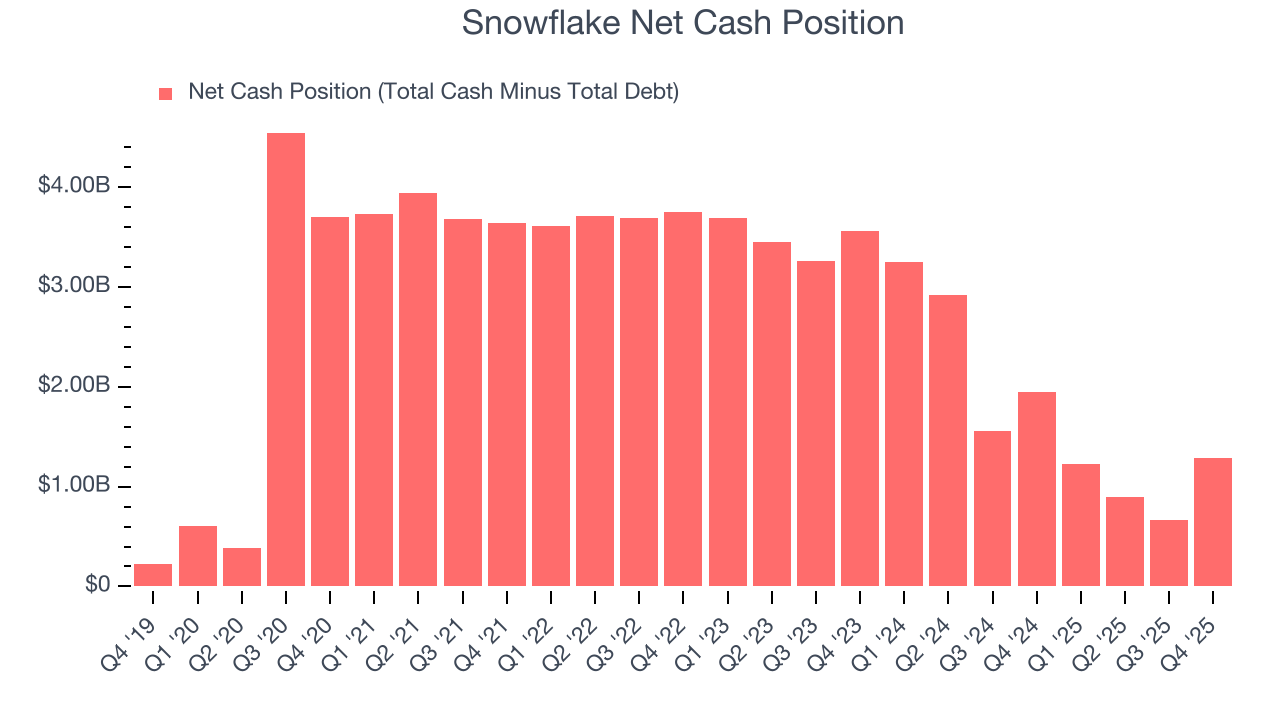

13. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Snowflake is a well-capitalized company with $4.03 billion of cash and $2.74 billion of debt on its balance sheet. This $1.29 billion net cash position is 2.2% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

14. Key Takeaways from Snowflake’s Q4 Results

We were impressed by how significantly Snowflake blew past analysts’ billings expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 3.7% to $163.63 immediately after reporting.

15. Is Now The Time To Buy Snowflake?

Updated: March 22, 2026 at 10:17 PM EDT

When considering an investment in Snowflake, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There are multiple reasons why we think Snowflake is an amazing business. For starters, its revenue growth was exceptional over the last five years. And while its operating margins reveal poor profitability compared to other software companies, its customers use its software frequently and increase their spending every year. Additionally, Snowflake’s efficient sales strategy allows it to target and onboard new users at scale.

Snowflake’s price-to-sales ratio based on the next 12 months is 10.1x. Analyzing the software landscape today, Snowflake’s positive attributes shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $239.84 on the company (compared to the current share price of $168.82), implying they see 42.1% upside in buying Snowflake in the short term.