Stanley Black & Decker (SWK)

Stanley Black & Decker is in for a bumpy ride. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Stanley Black & Decker Will Underperform

With an iconic “STANLEY” logo which has remained virtually unchanged for over a century, Stanley Black & Decker (NYSE:SWK) is a manufacturer primarily catering to the tool and outdoor equipment industry.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 2.1% annually over the last two years

- Earnings per share have contracted by 12.3% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

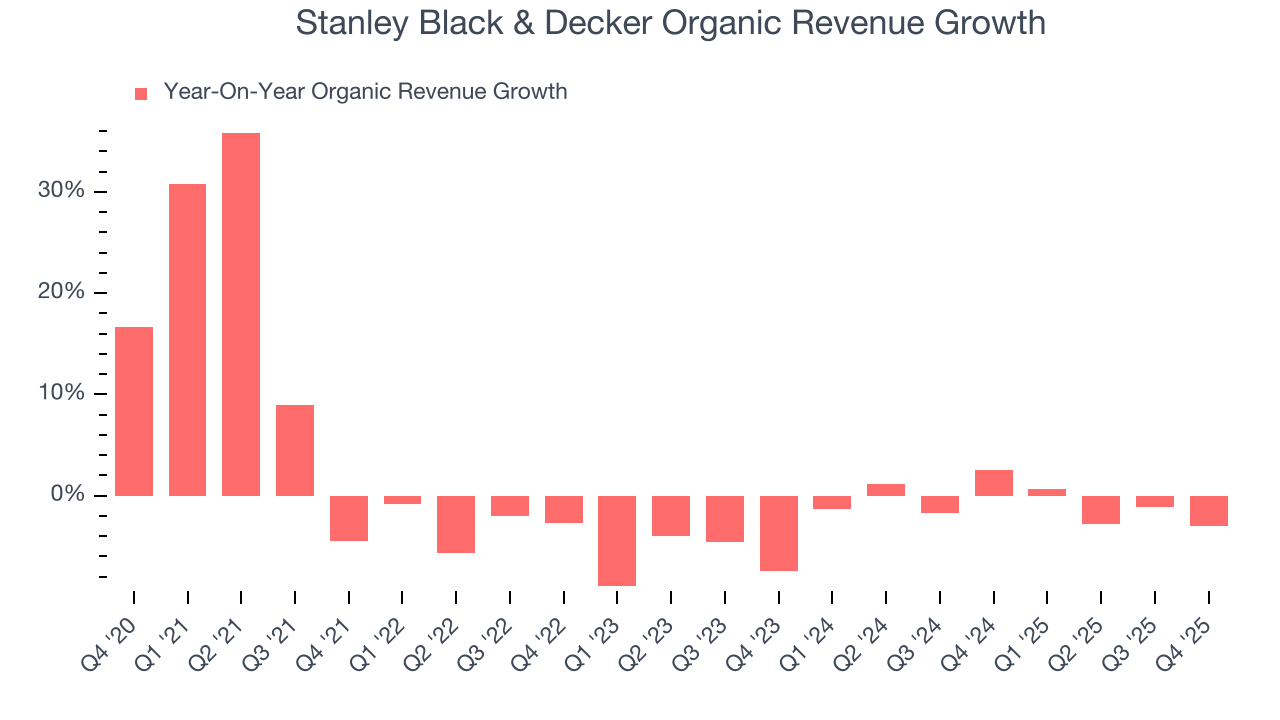

- Organic sales performance over the past two years indicates the company may need to make strategic adjustments or rely on M&A to catalyze faster growth

Stanley Black & Decker’s quality doesn’t meet our hurdle. You should search for better opportunities.

Why There Are Better Opportunities Than Stanley Black & Decker

Stanley Black & Decker’s stock price of $71.67 implies a valuation ratio of 13.4x forward P/E. This multiple is lower than most industrials companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Stanley Black & Decker (SWK) Research Report: Q4 CY2025 Update

Manufacturing company Stanley Black & Decker (NYSE:SWK) missed Wall Street’s revenue expectations in Q4 CY2025, with sales flat year on year at $3.68 billion. Its non-GAAP profit of $1.41 per share was 9.9% above analysts’ consensus estimates.

Stanley Black & Decker (SWK) Q4 CY2025 Highlights:

- Revenue: $3.68 billion vs analyst estimates of $3.77 billion (flat year on year, 2.2% miss)

- Adjusted EPS: $1.41 vs analyst estimates of $1.28 (9.9% beat)

- Adjusted EBITDA: $497.3 million vs analyst estimates of $487.8 million (13.5% margin, 1.9% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.30 at the midpoint, missing analyst estimates by 5.7%

- Operating Margin: 8.4%, in line with the same quarter last year

- Free Cash Flow Margin: 24%, up from 15.2% in the same quarter last year

- Organic Revenue fell 3% year on year (miss)

- Market Capitalization: $12.54 billion

Company Overview

With an iconic “STANLEY” logo which has remained virtually unchanged for over a century, Stanley Black & Decker (NYSE:SWK) is a manufacturer primarily catering to the tool and outdoor equipment industry.

Stanley Black & Decker's story starts with the establishment of Stanley's Bolt Manufactory by Frederick Stanley in 1843 and the Stanley Rule and Level Company by his cousin Henry Stanley in 1857. The two companies merged in 1920, forming The Stanley Works. In 2010, The Stanley Works merged with Black & Decker, creating Stanley Black & Decker.

In recent years, Stanley Black & Decker has actively reshaped its portfolio through strategic acquisitions and divestitures, concentrating on its core strengths in tools, outdoor products, and fastening systems. Notably, in December 2021, the company acquired the remaining 80% stake in MTD Holdings for $1.5 billion, expanding its presence in the outdoor market. Additionally, the acquisition of Excel Industries for $374 million strengthened the company's foothold in the independent dealer network. Stanley sold its CSS and MAS businesses, as well as the Oil & Gas and Infrastructure businesses to shed non-core operations to focus on areas where the company holds strong market positions.

Stanley Black & Decker’s product offerings can be logically divided into two categories: tools and outdoor and industrial products, which it sells through a variety of brands. In the tools and outdoor category, the company provides a lineup of power tools, hand tools, accessories, and outdoor power equipment. For instance, the DEWALT® Cordless Drill is a key product used for drilling holes and driving screws. In the industrial category Stanley Black & Decker specializes in engineered components such as fasteners, fittings, and various engineered products. The business serves automotive, manufacturing, electronics, construction, and aerospace sectors. Additionally, the company designs and manufactures attachments for excavators and handheld hydraulic tools used in infrastructure and construction. While its tools and outdoors products are primarily sold through mass retailers and third party distributors, its industrial products are primarily distributed through a direct sales force, for a more targeted and effective market reach given the large orders customers place. Stanley Black & Decker generates revenue from the sale of its goods, with the majority of its revenue from its tools and outdoor products. The company also benefits from recurring revenue through its aftermarket services, the sale of consumables and replacement parts.

4. Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Snap-On (NYSE:SNA), Illinois Tool Works (NYSE:ITW), and Newell Brands (NYSE:NWL).

5. Revenue Growth

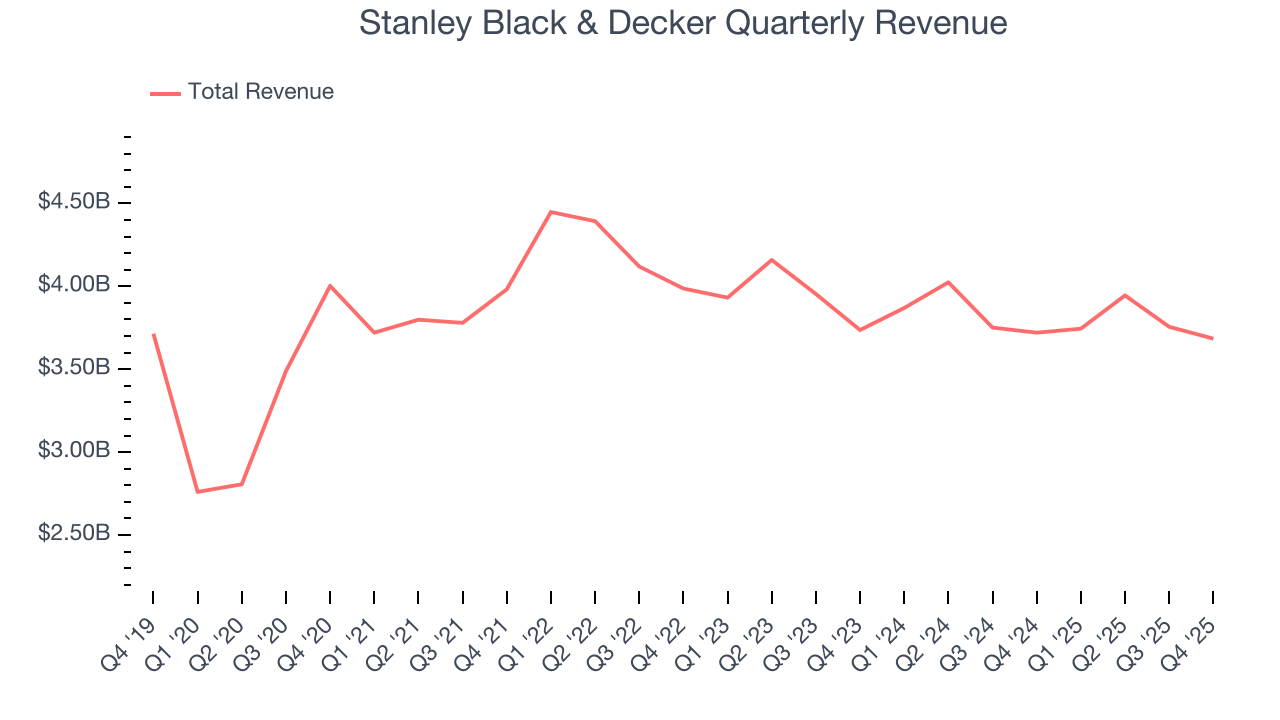

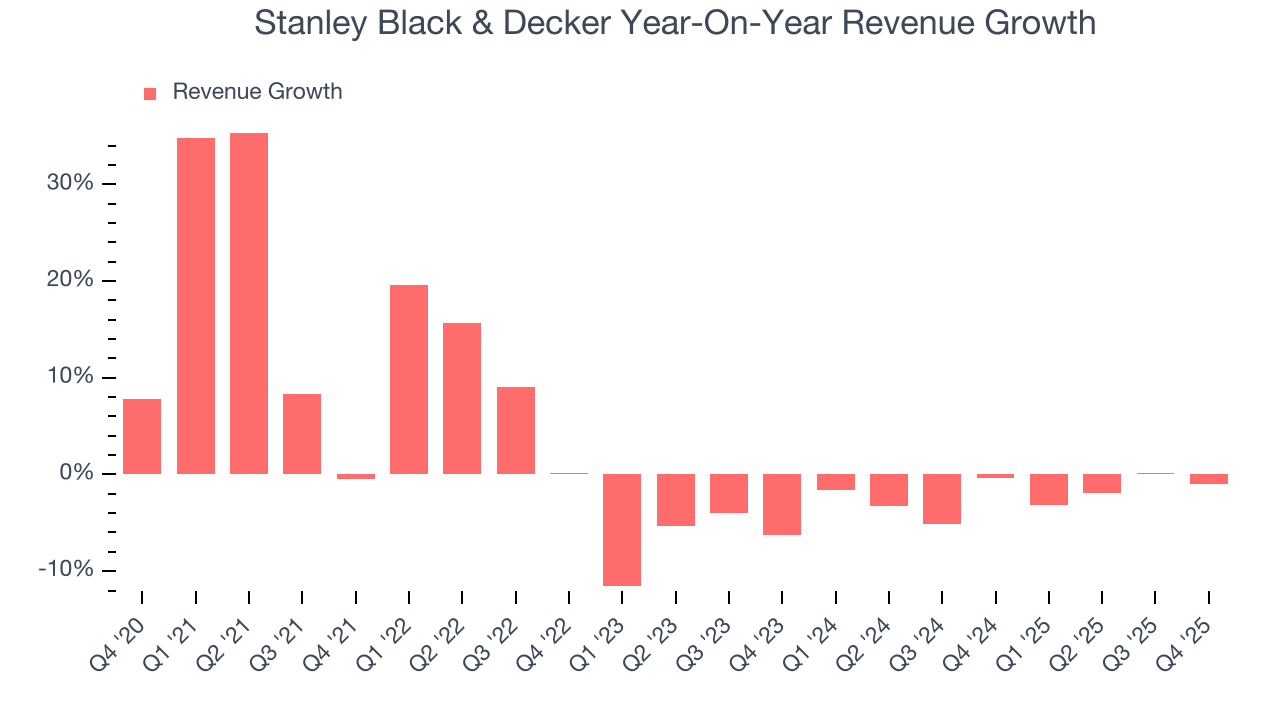

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Stanley Black & Decker grew its sales at a sluggish 3% compounded annual growth rate. This fell short of our benchmarks and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Stanley Black & Decker’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.1% annually.

Stanley Black & Decker also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Stanley Black & Decker’s organic revenue was flat. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Stanley Black & Decker missed Wall Street’s estimates and reported a rather uninspiring 1% year-on-year revenue decline, generating $3.68 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 3% over the next 12 months. Although this projection implies its newer products and services will spur better top-line performance, it is still below average for the sector.

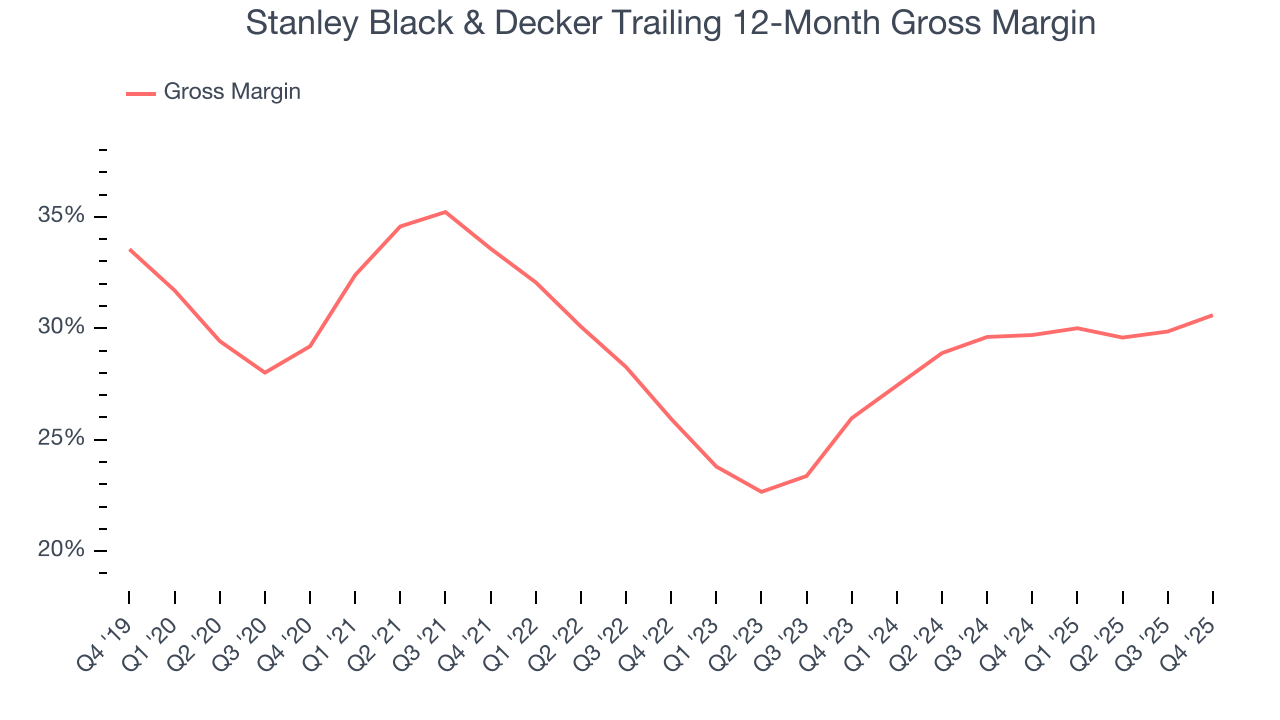

6. Gross Margin & Pricing Power

Stanley Black & Decker’s gross margin is slightly below the average industrials company, giving it less room to invest in areas such as research and development. As you can see below, it averaged a 29.1% gross margin over the last five years. Said differently, Stanley Black & Decker had to pay a chunky $70.94 to its suppliers for every $100 in revenue.

This quarter, Stanley Black & Decker’s gross profit margin was 33.2%, marking a 3 percentage point increase from 30.1% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

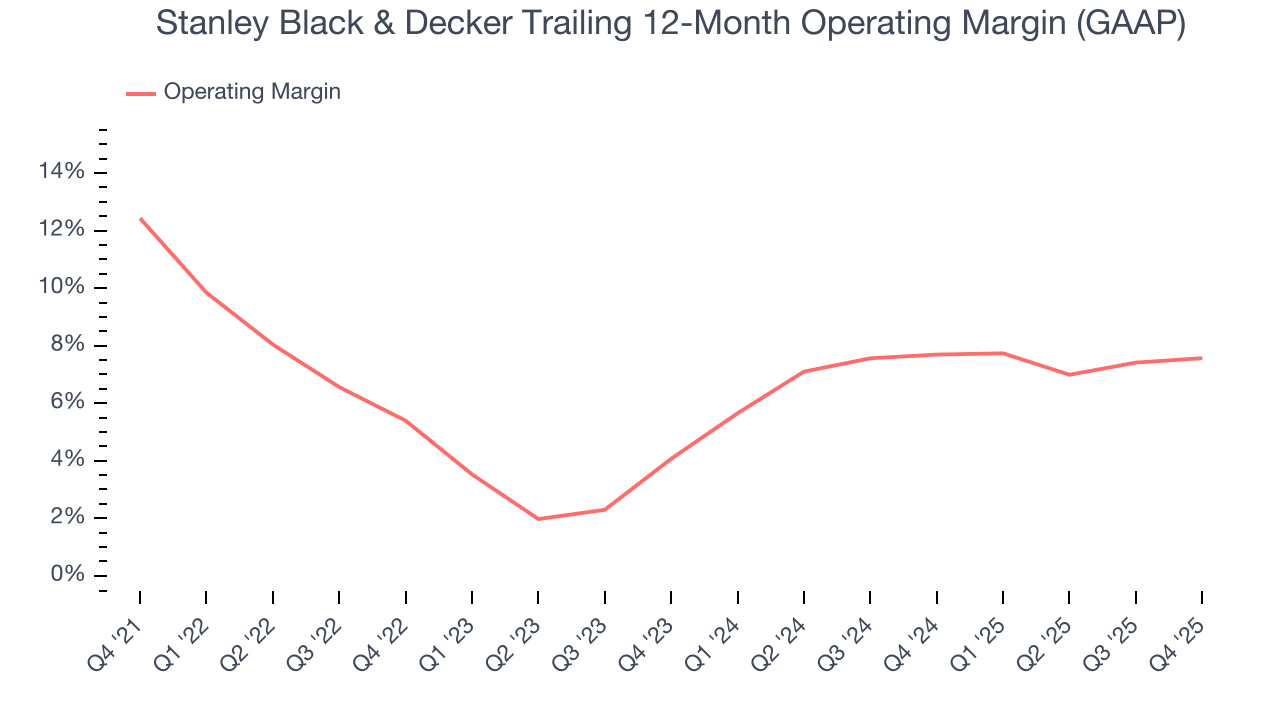

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Stanley Black & Decker was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Stanley Black & Decker’s operating margin decreased by 4.9 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Stanley Black & Decker’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Stanley Black & Decker generated an operating margin profit margin of 8.4%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

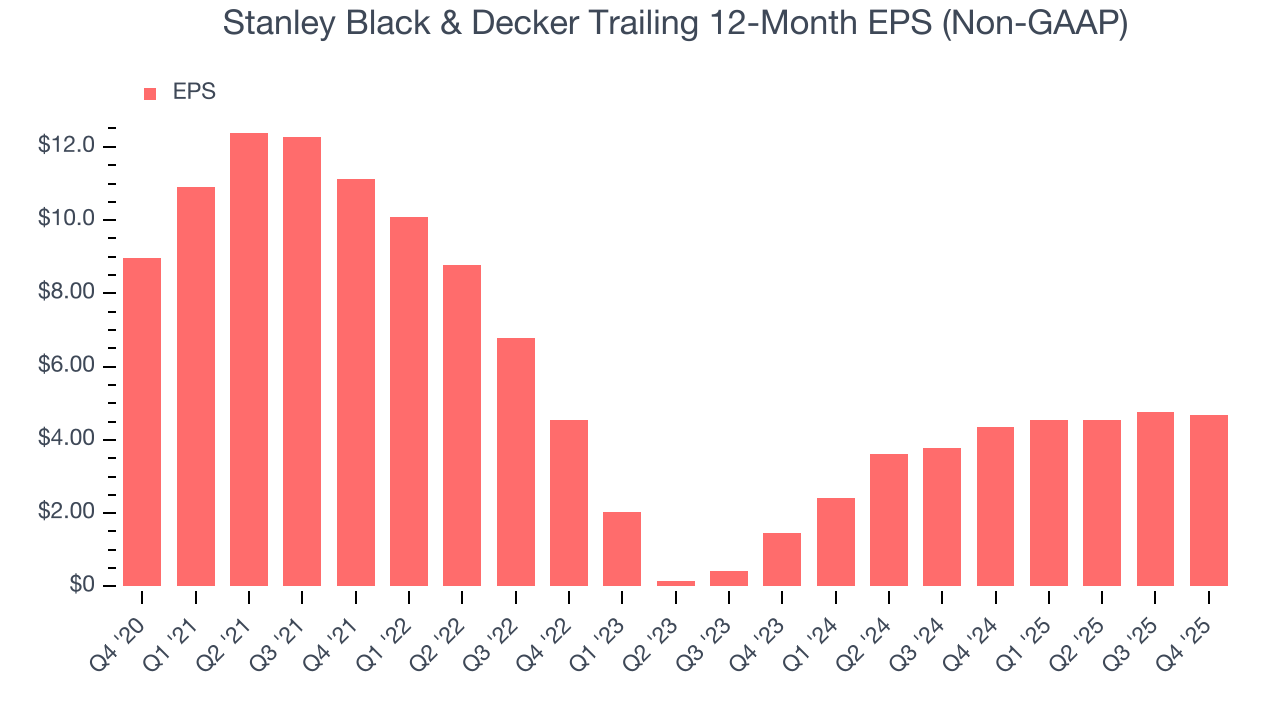

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Stanley Black & Decker, its EPS declined by 12.3% annually over the last five years while its revenue grew by 3%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Stanley Black & Decker’s earnings can give us a better understanding of its performance. As we mentioned earlier, Stanley Black & Decker’s operating margin was flat this quarter but declined by 4.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Stanley Black & Decker, its two-year annual EPS growth of 79.5% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, Stanley Black & Decker reported adjusted EPS of $1.41, down from $1.49 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 9.9%. Over the next 12 months, Wall Street expects Stanley Black & Decker’s full-year EPS of $4.67 to grow 19%.

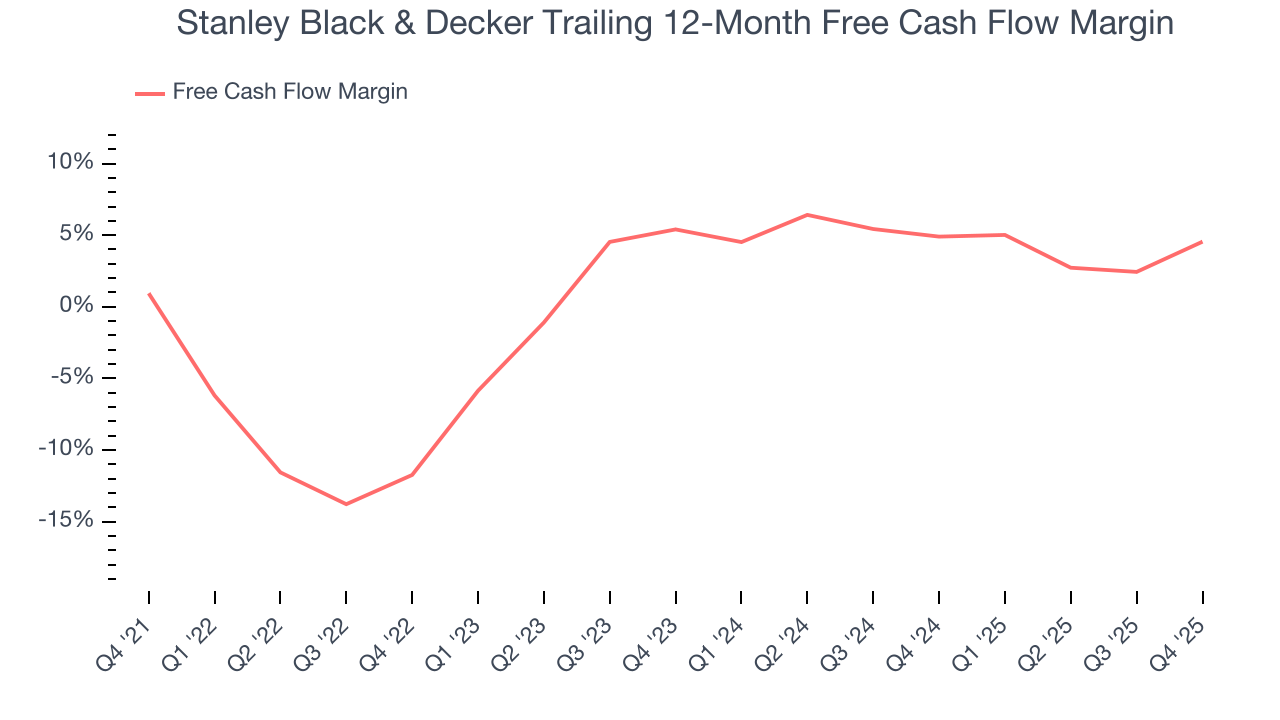

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Stanley Black & Decker broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that Stanley Black & Decker’s margin expanded by 3.6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Stanley Black & Decker’s free cash flow clocked in at $882.9 million in Q4, equivalent to a 24% margin. This result was good as its margin was 8.8 percentage points higher than in the same quarter last year, building on its favorable historical trend.

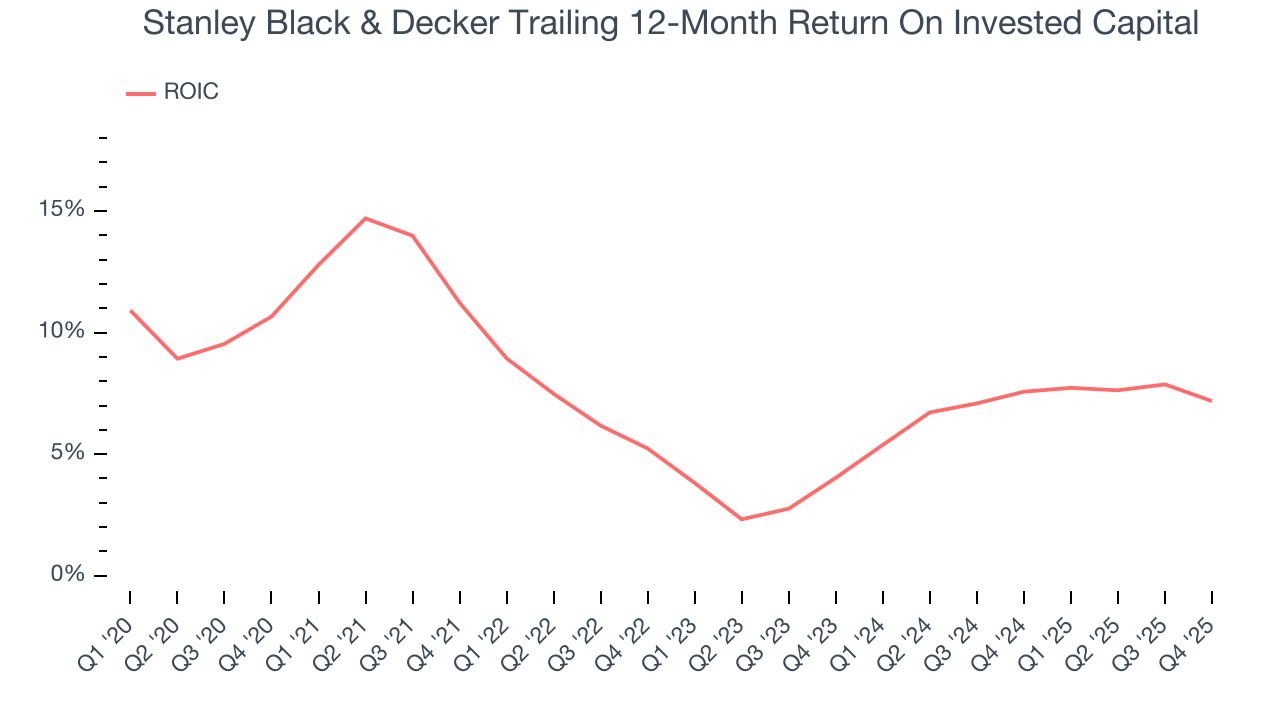

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Stanley Black & Decker historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 7%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Stanley Black & Decker’s ROIC has stayed the same over the last few years. If the company wants to become an investable business, it must improve its returns by generating more profitable growth.

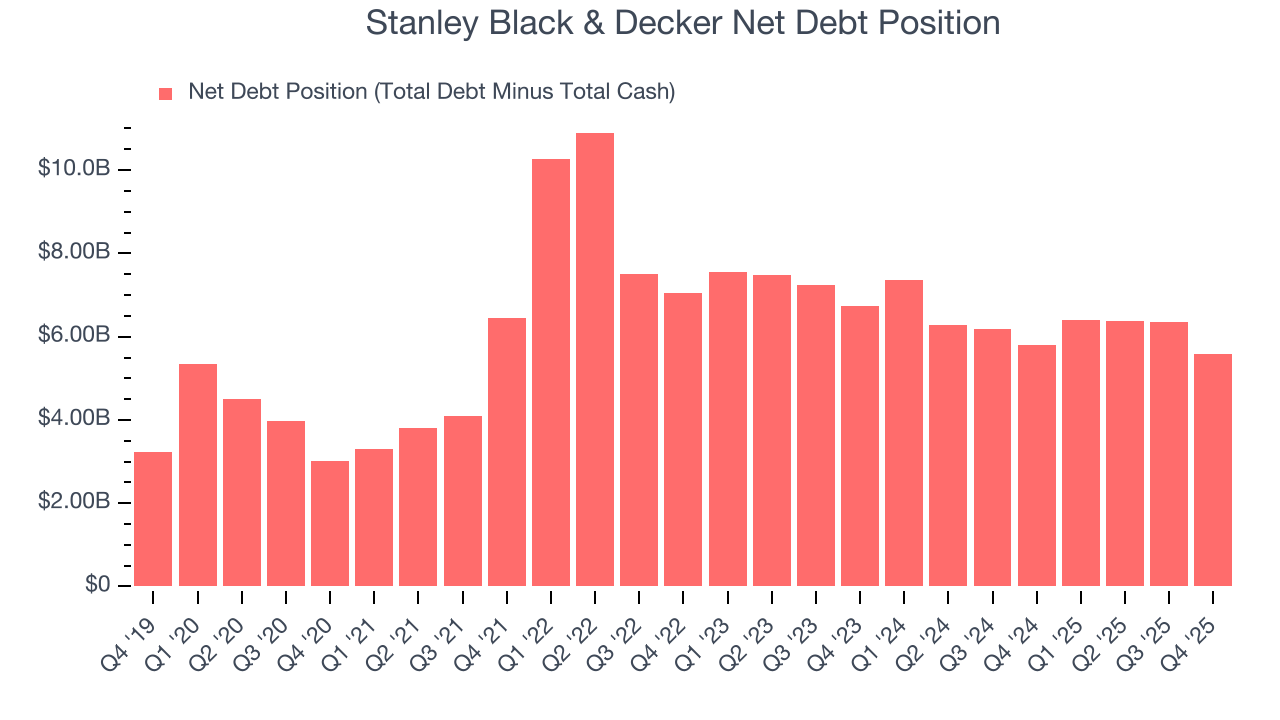

11. Balance Sheet Assessment

Stanley Black & Decker reported $280.1 million of cash and $5.86 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.64 billion of EBITDA over the last 12 months, we view Stanley Black & Decker’s 3.4× net-debt-to-EBITDA ratio as safe. We also see its $155.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Stanley Black & Decker’s Q4 Results

It was good to see Stanley Black & Decker beat analysts’ EPS expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 1.3% to $79.90 immediately after reporting.

13. Is Now The Time To Buy Stanley Black & Decker?

Updated: March 26, 2026 at 11:30 PM EDT

Before making an investment decision, investors should account for Stanley Black & Decker’s business fundamentals and valuation in addition to what happened in the latest quarter.

Stanley Black & Decker falls short of our quality standards. To kick things off, its revenue growth was weak over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its flat organic revenue disappointed.

Stanley Black & Decker’s P/E ratio based on the next 12 months is 13.4x. While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $91.87 on the company (compared to the current share price of $71.67).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.