Vishay Intertechnology (VSH)

Vishay Intertechnology is up against the odds. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Vishay Intertechnology Will Underperform

Named after the founder's ancestral village in present-day Lithuania, Vishay Intertechnology (NYSE:VSH) manufactures simple chips and electronic components that are building blocks of virtually all types of electronic devices.

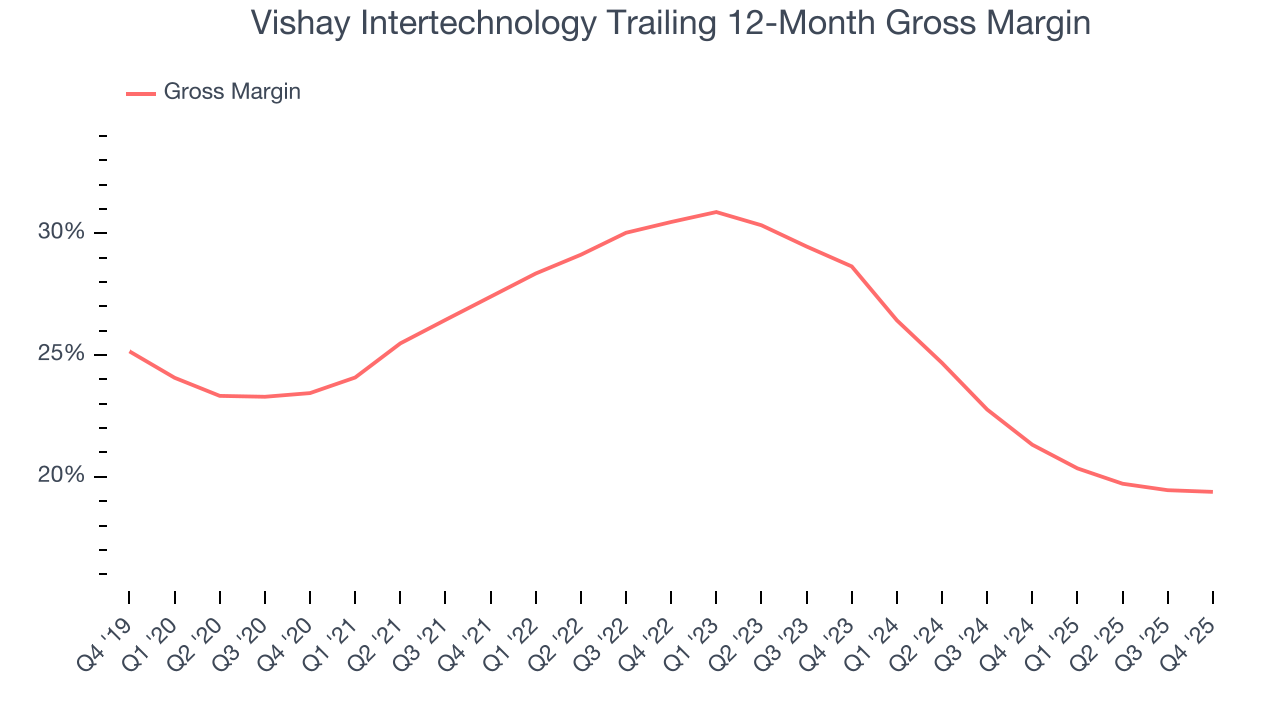

- Gross margin of 20.3% reflects its high production costs

- Increased cash burn over the last five years raises questions about the return timeline for its investments

- Performance over the past five years shows its incremental sales were much less profitable, as its earnings per share fell by 15.5% annually

Vishay Intertechnology doesn’t meet our quality criteria. There are more promising alternatives.

Why There Are Better Opportunities Than Vishay Intertechnology

Vishay Intertechnology is trading at $18.64 per share, or 32.2x forward P/E. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Vishay Intertechnology (VSH) Research Report: Q4 CY2025 Update

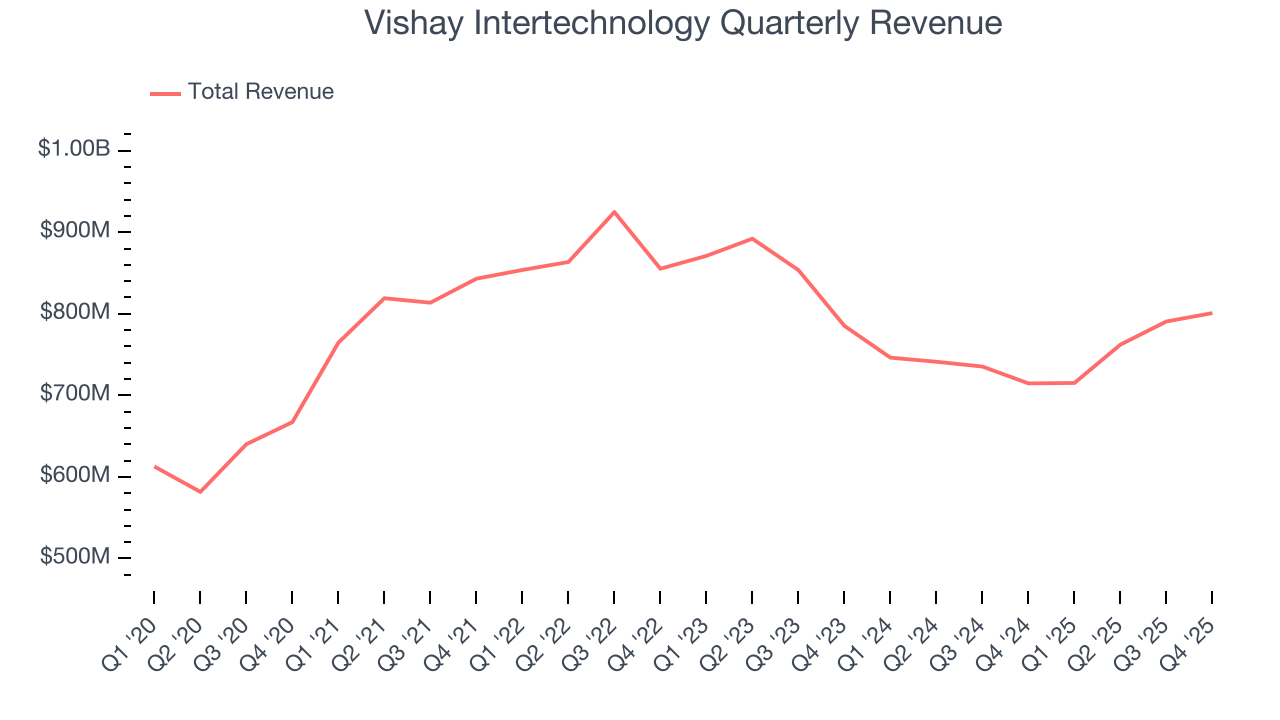

Semiconductor manufacturer Vishay Intertechnology (NYSE:VSH) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 12.1% year on year to $800.9 million. Guidance for next quarter’s revenue was better than expected at $815 million at the midpoint, 1.2% above analysts’ estimates. Its non-GAAP profit of $0.01 per share was in line with analysts’ consensus estimates.

Vishay Intertechnology (VSH) Q4 CY2025 Highlights:

- Revenue: $800.9 million vs analyst estimates of $795.7 million (12.1% year-on-year growth, 0.7% beat)

- Adjusted EPS: $0.01 vs analyst estimates of $0.02 (in line)

- Adjusted EBITDA: $72.49 million vs analyst estimates of $67.71 million (9.1% margin, 7.1% beat)

- Revenue Guidance for Q1 CY2026 is $815 million at the midpoint, above analyst estimates of $805.6 million

- Operating Margin: 1.8%, up from -7.9% in the same quarter last year

- Free Cash Flow was $54.87 million, up from -$75.63 million in the same quarter last year

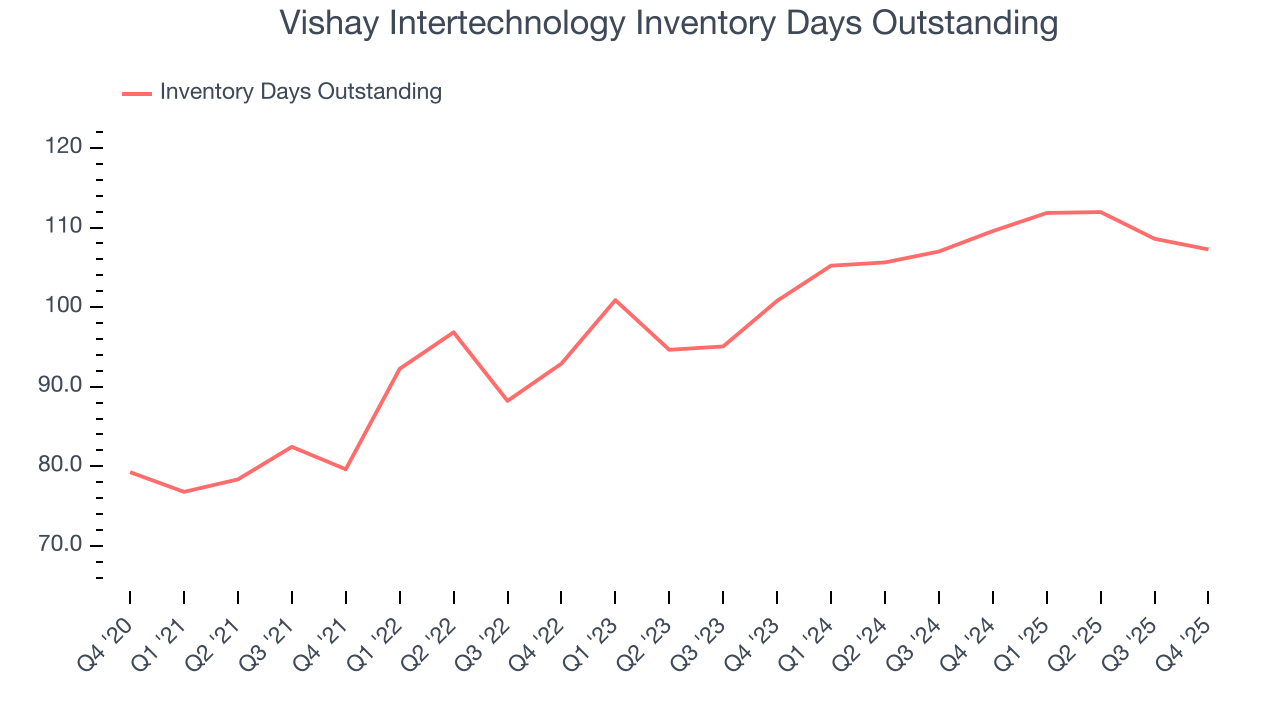

- Inventory Days Outstanding: 107, down from 109 in the previous quarter

- Market Capitalization: $2.54 billion

Company Overview

Named after the founder's ancestral village in present-day Lithuania, Vishay Intertechnology (NYSE:VSH) manufactures simple chips and electronic components that are building blocks of virtually all types of electronic devices.

Vishay Intertechnology mainly manufactures discrete semiconductors and passive electronic components that can be found in almost any electronic device. Discrete semiconductors are chips that have a small number of transistors and are used for basic functions. Discrete semiconductors essentially exist in an on or off state and function alongside more complex chips in virtually every electronic device. The company also manufactures passive electronic devices such as resistors, inductors, and capacitors. These components are essential for the operation of electronic devices and work in tandem with more complex parts from other manufacturers. Through the manufacturing of discrete semiconductors and passive electronic components, it is essentially supplying the most basic elements of any electronic device.Vishay Intertechnology’s peers and competitors include Analog Devices (NASDAQ: ADI) Texas Instruments (NASDAQ: TXN), Skyworks (NASDAQ:SWKS), Infineon (XTRA:IFX), NXP Semiconductors NV (NASDAQ:NXPI), ON Semi (NASDAQ:ON), Marvell Technology (NASDAQ:MRVL), and Microchip (NASDAQ:MCHP).

4. Revenue Growth

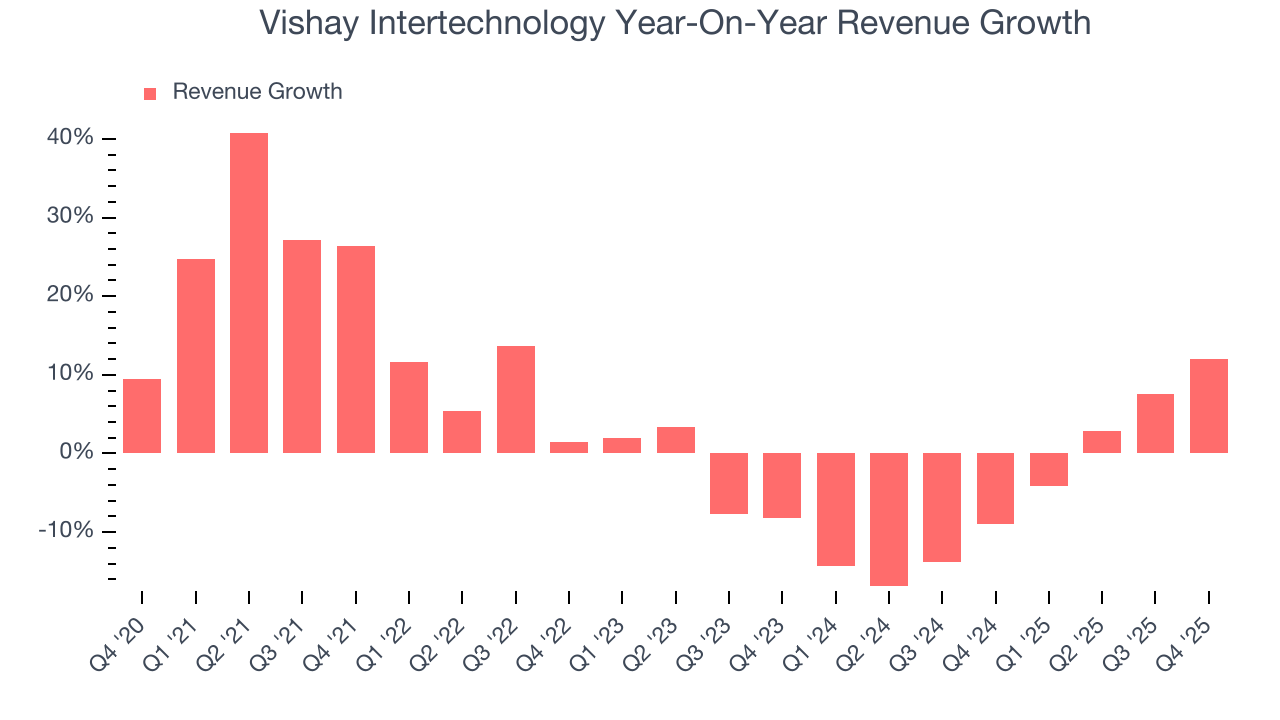

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Vishay Intertechnology’s sales grew at a mediocre 4.2% compounded annual growth rate over the last five years. This was below our standard for the semiconductor sector and is a tough starting point for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Vishay Intertechnology’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5% annually.

This quarter, Vishay Intertechnology reported year-on-year revenue growth of 12.1%, and its $800.9 million of revenue exceeded Wall Street’s estimates by 0.7%. Beyond the beat, we believe the company is still in the early days of an upcycle as this was the third consecutive quarter of growth - a typical upcycle tends to last 8-10 quarters. Company management is currently guiding for a 13.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.2% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

5. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Vishay Intertechnology’s DIO came in at 107, which is 10 days above its five-year average. These numbers suggest that despite the recent decrease, the company’s inventory levels are higher than what we’ve seen in the past.

6. Gross Margin & Pricing Power

In the semiconductor industry, a company’s gross profit margin is a critical metric to track because it sheds light on its pricing power, complexity of products, and ability to procure raw materials, equipment, and labor.

Vishay Intertechnology’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 20.3% gross margin over the last two years. That means Vishay Intertechnology paid its suppliers a lot of money ($79.67 for every $100 in revenue) to run its business.

Vishay Intertechnology’s gross profit margin came in at 19.6% this quarter, in line with the same quarter last year. Zooming out, Vishay Intertechnology’s full-year margin has been trending down over the past 12 months, decreasing by 1.9 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

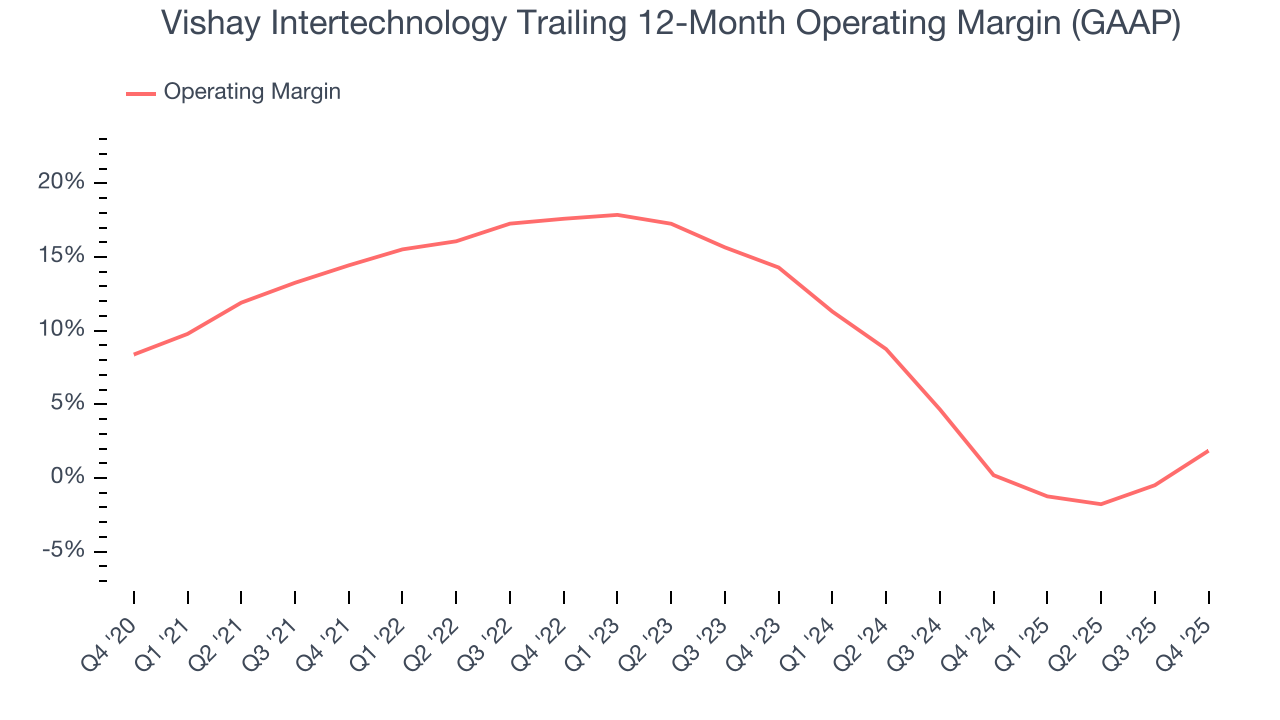

7. Operating Margin

Vishay Intertechnology was profitable over the last two years but held back by its large cost base. Its average operating margin of 1% was weak for a semiconductor business. This result isn’t too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Vishay Intertechnology’s operating margin decreased by 12.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Vishay Intertechnology’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Vishay Intertechnology generated an operating margin profit margin of 1.8%, up 9.8 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

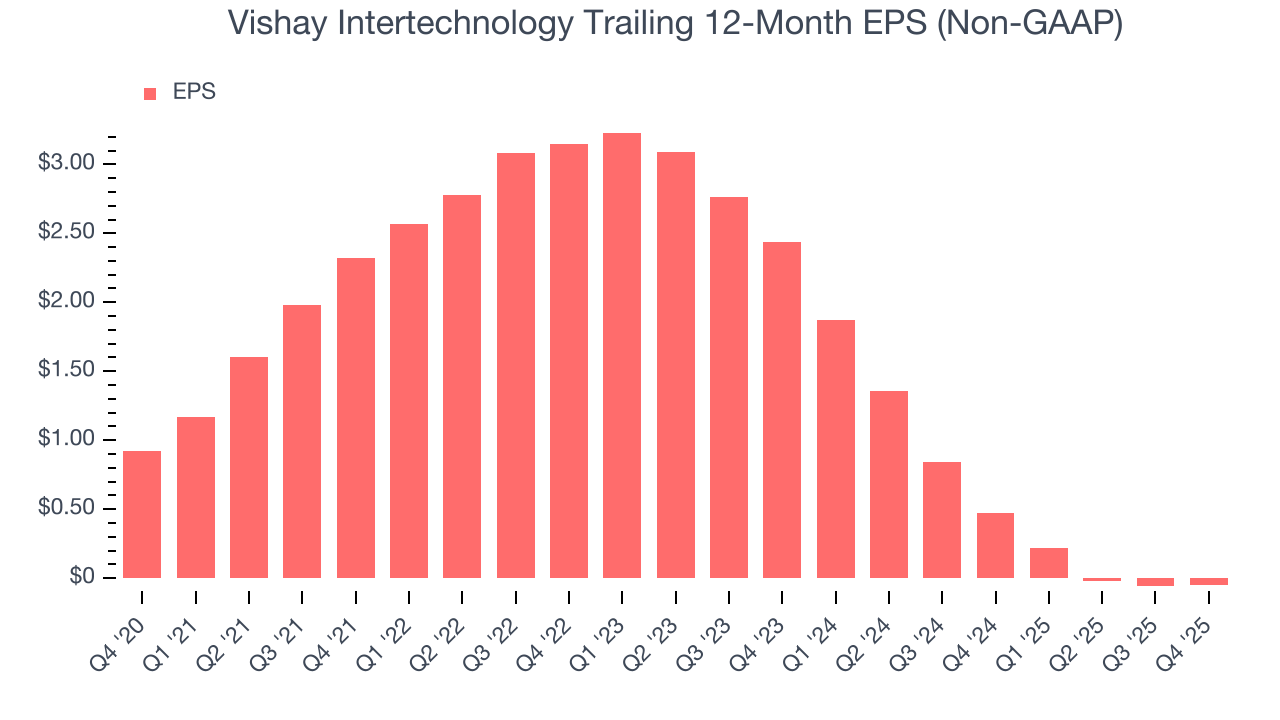

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Vishay Intertechnology, its EPS declined by 15.5% annually over the last five years while its revenue grew by 4.2%. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

Diving into the nuances of Vishay Intertechnology’s earnings can give us a better understanding of its performance. As we mentioned earlier, Vishay Intertechnology’s operating margin expanded this quarter but declined by 12.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Vishay Intertechnology reported adjusted EPS of $0.01, up from $0 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Vishay Intertechnology’s full-year EPS of negative $0.05 will flip to positive $0.59.

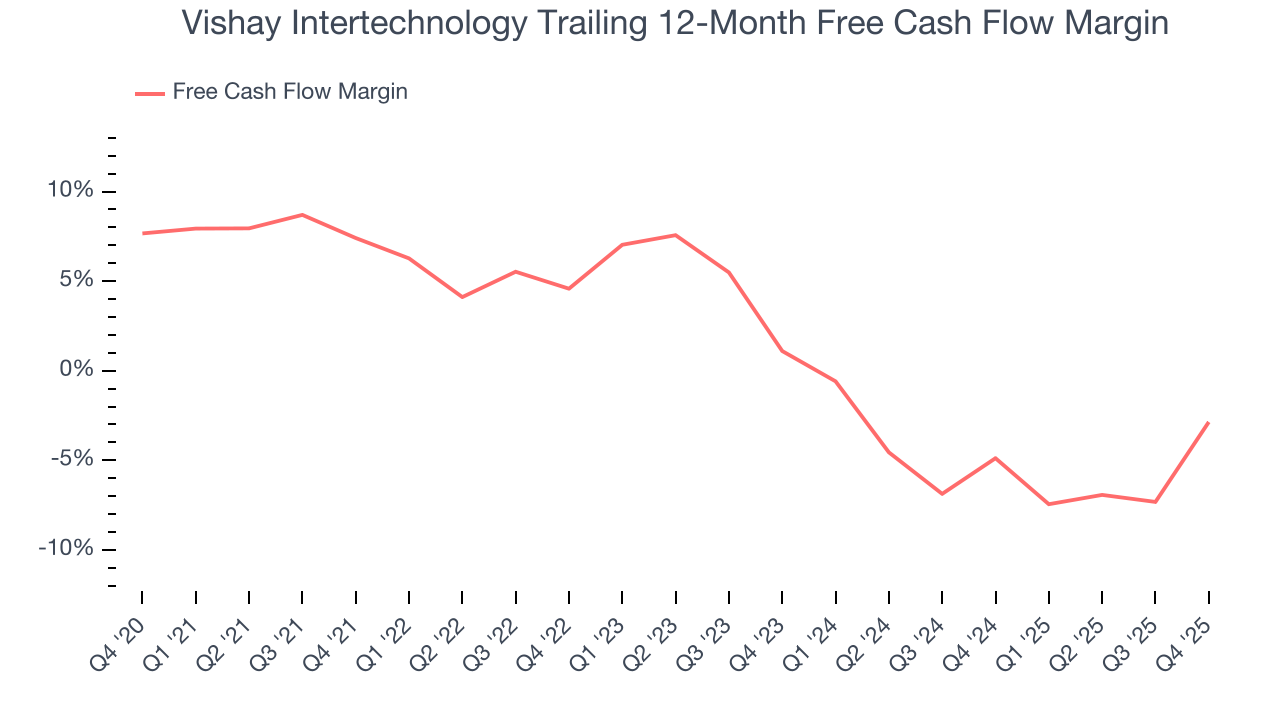

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

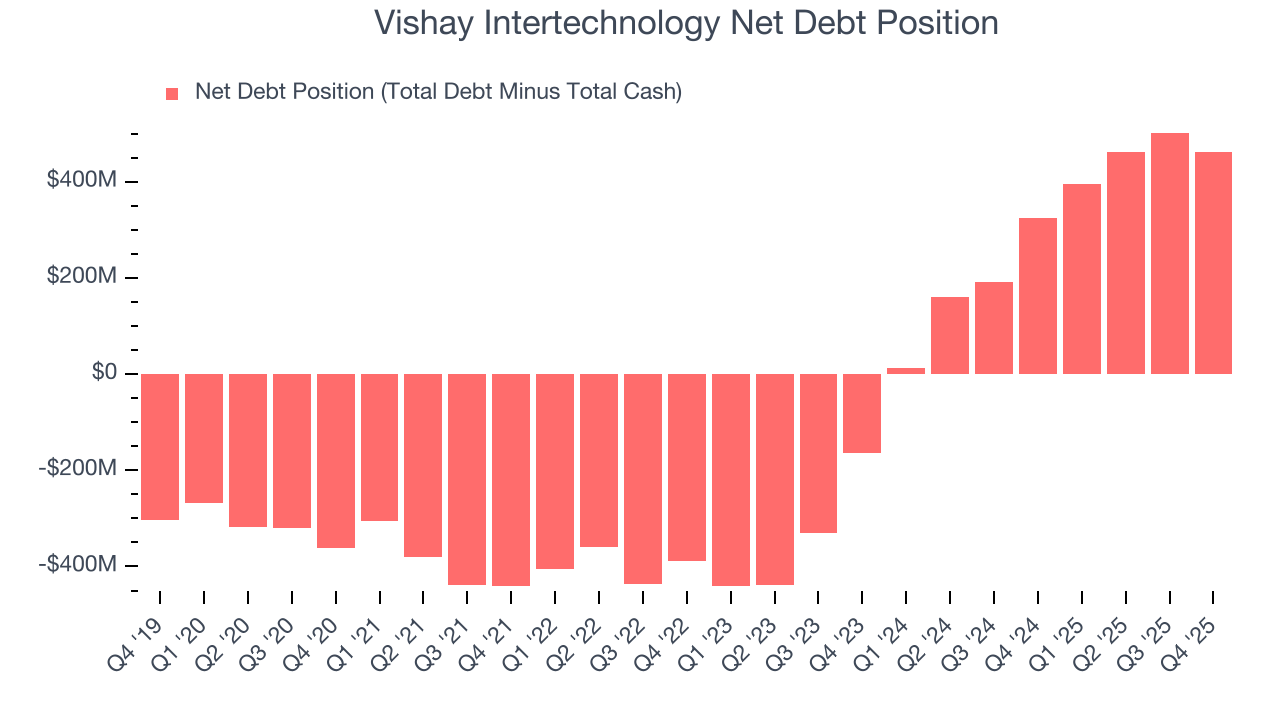

While Vishay Intertechnology posted positive free cash flow this quarter, the broader story hasn’t been so clean. Vishay Intertechnology’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 3.8%, meaning it lit $3.85 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Vishay Intertechnology’s margin dropped by 10.3 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because it’s already burning cash. If the longer-term trend returns, it could signal it’s in the middle of a big investment cycle.

Vishay Intertechnology’s free cash flow clocked in at $54.87 million in Q4, equivalent to a 6.9% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

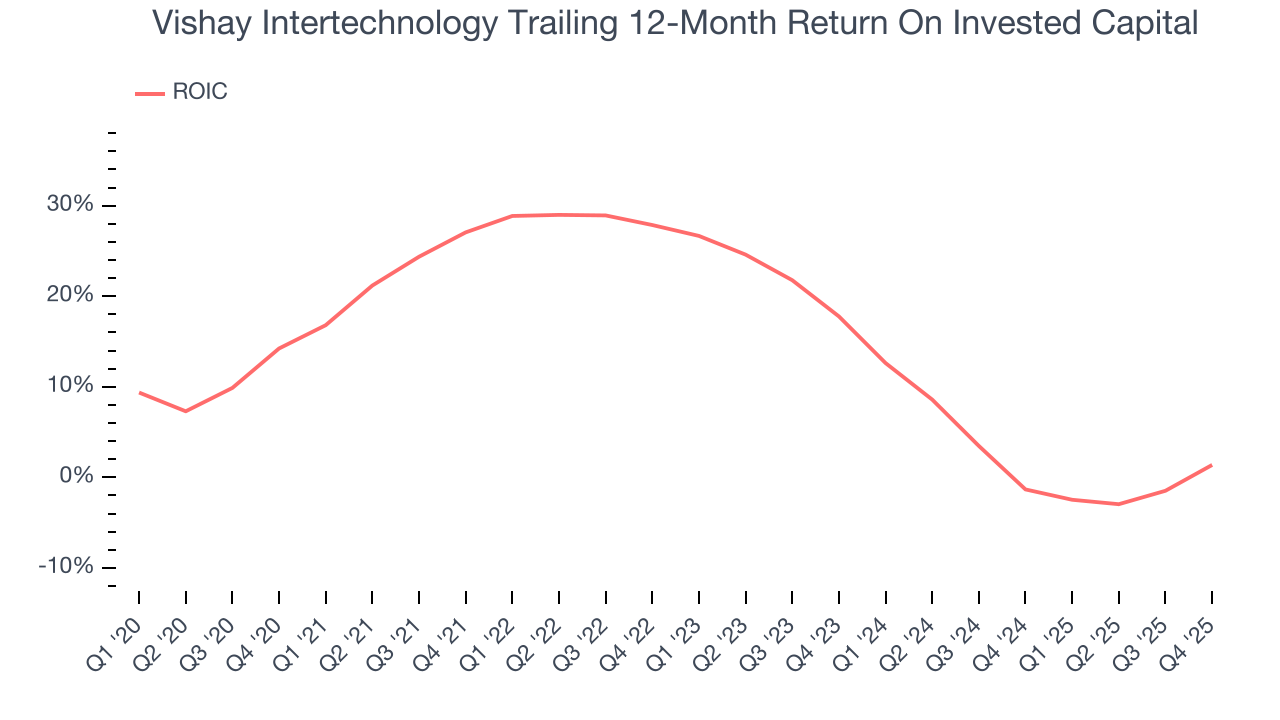

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Vishay Intertechnology historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 14.5%, somewhat low compared to the best semiconductor companies that consistently pump out 35%+.

11. Balance Sheet Assessment

Vishay Intertechnology reported $515.2 million of cash and $977.4 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $270.3 million of EBITDA over the last 12 months, we view Vishay Intertechnology’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $28.04 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Vishay Intertechnology’s Q4 Results

It was good to see Vishay Intertechnology provide revenue guidance for next quarter that slightly beat analysts’ expectations. On the other hand, its adjusted operating income missed and its EPS was in line with Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded up 1% to $18.88 immediately following the results.

13. Is Now The Time To Buy Vishay Intertechnology?

Updated: February 17, 2026 at 9:28 PM EST

Before investing in or passing on Vishay Intertechnology, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

We see the value of companies furthering technological innovation, but in the case of Vishay Intertechnology, we’re out. To begin with, its revenue growth was mediocre over the last five years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its cash burn raises the question of whether it can sustainably maintain growth. On top of that, its low gross margins indicate some combination of pricing pressures or rising production costs.

Vishay Intertechnology’s P/E ratio based on the next 12 months is 32.2x. At this valuation, there’s a lot of good news priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $17.50 on the company (compared to the current share price of $18.88), implying they don’t see much short-term potential in Vishay Intertechnology.