Sprout Social (SPT)

We’re wary of Sprout Social. Its growth has decelerated and its failure to generate meaningful free cash flow makes us question its prospects.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sprout Social Will Underperform

Born from the recognition that businesses needed a centralized way to handle their growing social media presence, Sprout Social (NASDAQ:SPT) provides a comprehensive software platform that helps businesses manage, analyze, and optimize their presence across various social media networks.

- Estimated sales growth of 7.8% for the next 12 months implies demand will slow from its two-year trend

- Rapid expansion strategy came at the expense of operating margin profitability

- One positive is that its annual revenue growth of 28% over the past five years was outstanding, reflecting market share gains

Sprout Social doesn’t fulfill our quality requirements. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Sprout Social

At $5.86 per share, Sprout Social trades at 0.7x forward price-to-sales. This sure is a cheap multiple, but you get what you pay for.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Sprout Social (SPT) Research Report: Q4 CY2025 Update

Social media management platform Sprout Social (NASDAQ:SPT) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 12.9% year on year to $120.9 million. On the other hand, next quarter’s revenue guidance of $120.3 million was less impressive, coming in 0.8% below analysts’ estimates. Its non-GAAP profit of $0.20 per share was 26.3% above analysts’ consensus estimates.

Sprout Social (SPT) Q4 CY2025 Highlights:

- Revenue: $120.9 million vs analyst estimates of $118.8 million (12.9% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.20 vs analyst estimates of $0.16 (26.3% beat)

- Adjusted Operating Income: $11.51 million vs analyst estimates of $10.24 million (9.5% margin, 12.5% beat)

- Revenue Guidance for Q1 CY2026 is $120.3 million at the midpoint, below analyst estimates of $121.3 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $0.93 at the midpoint, beating analyst estimates by 3%

- Operating Margin: -9%, up from -12.8% in the same quarter last year

- Free Cash Flow Margin: 9%, up from 7.4% in the previous quarter

- Billings: $153.9 million at quarter end, up 12.7% year on year

- Market Capitalization: $400.1 million

Company Overview

Born from the recognition that businesses needed a centralized way to handle their growing social media presence, Sprout Social (NASDAQ:SPT) provides a comprehensive software platform that helps businesses manage, analyze, and optimize their presence across various social media networks.

Sprout Social's platform integrates with major social networks including X (formerly Twitter), Facebook, Instagram, TikTok, LinkedIn, and YouTube, creating a unified system for social media management. The cloud-based software consolidates multiple functions such as social engagement, publishing, analytics, listening, reputation management, and commerce into a single interface.

A marketing team might use Sprout Social to schedule posts across multiple platforms, monitor brand mentions, respond to customer inquiries, and analyze which content performs best—all from one dashboard. The platform also offers specialized tools for customer service teams to handle support requests coming through social channels.

The company serves over 31,000 customers across more than 100 countries, ranging from small businesses to large enterprises. While many users can self-onboard through free trials, Sprout Social also maintains sales teams for larger clients with more complex needs. The company generates revenue primarily through subscription-based pricing tiers, with additional revenue coming from professional services such as consulting and training.

Sprout Social's platform is designed to be accessible yet powerful, allowing organizations to coordinate social media efforts across departments, measure performance, gain market insights, and ultimately build stronger relationships with their audiences.

4. Marketing Software

Whether or not companies market their products through social media, all businesses need to meet customers where they are; and increasingly, that is social media. As more and more people use a greater number of social media platforms, social media management software become more valuable to their customers.

Sprout Social competes primarily with other social media management platforms including Hootsuite, Khoros, and Sprinklr, along with various point solutions that address specific aspects of social media management.

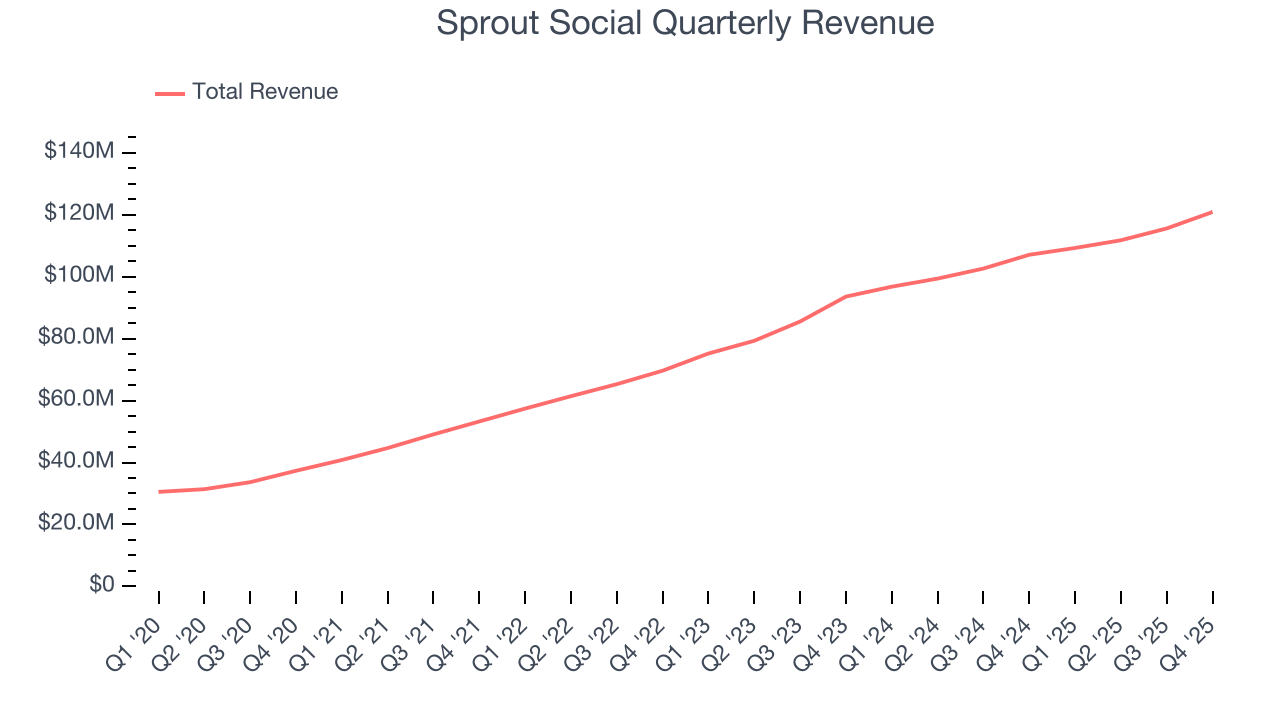

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Sprout Social’s 28% annualized revenue growth over the last five years was impressive. Its growth beat the average software company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Sprout Social’s annualized revenue growth of 17.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Sprout Social reported year-on-year revenue growth of 12.9%, and its $120.9 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds.

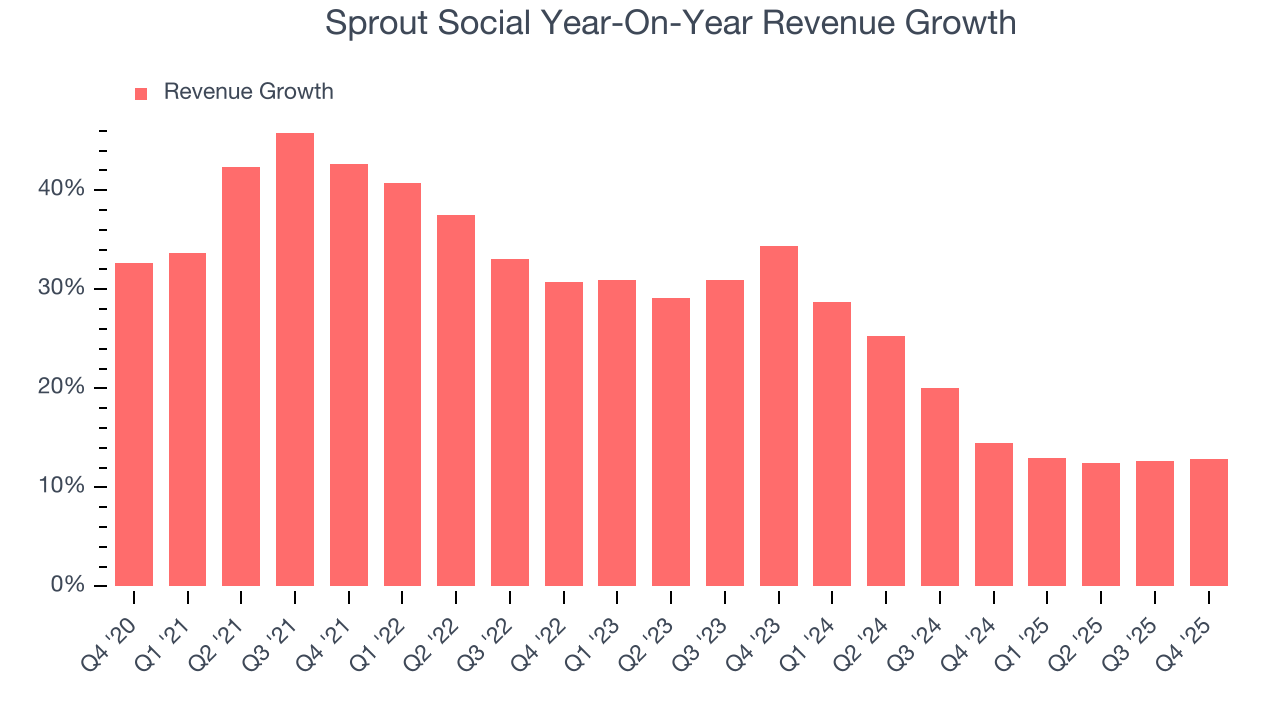

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Sprout Social’s billings came in at $153.9 million in Q4, and over the last four quarters, its growth was underwhelming as it averaged 8.7% year-on-year increases. This alternate topline metric grew slower than total sales, meaning the company recognizes revenue faster than it collects cash - a headwind for its liquidity that could also signal a slowdown in future revenue growth.

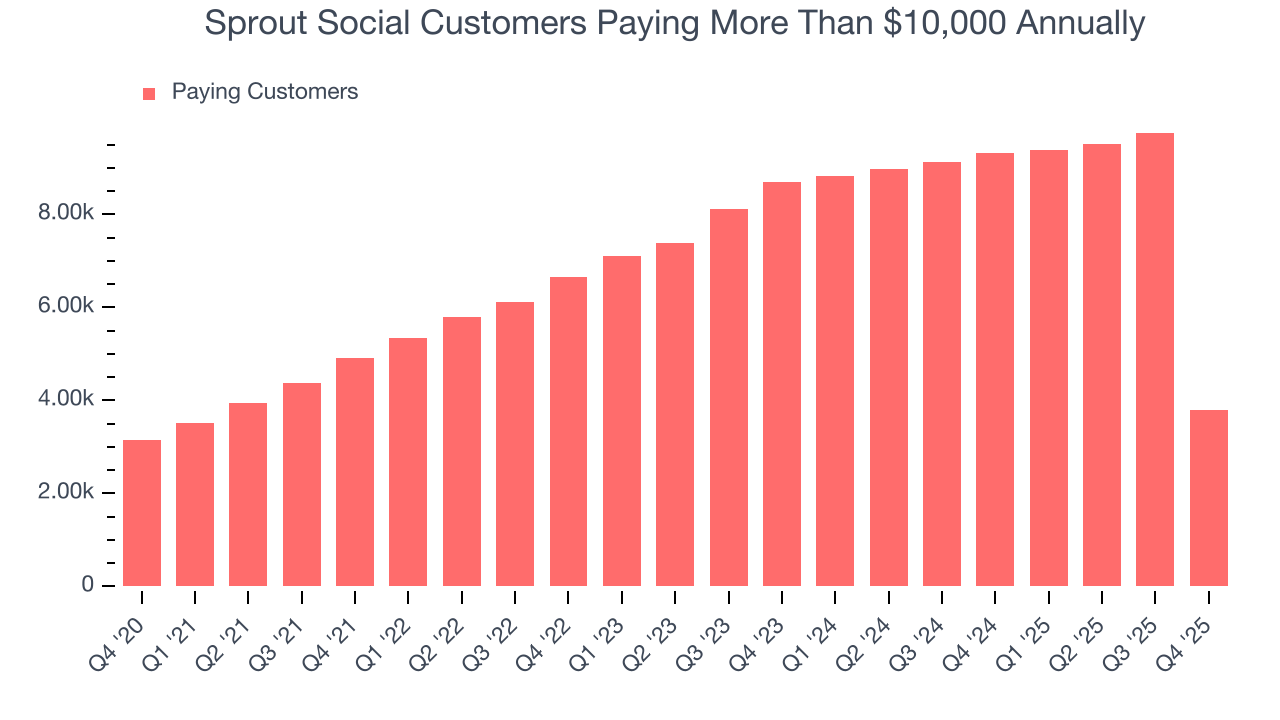

7. Enterprise Customer Base

This quarter, Sprout Social reported 3,803 enterprise customers paying more than $10,000 annually, a decrease of 5,953 from the previous quarter. We’ve no doubt shareholders would like to see the company accelerate its sales momentum.

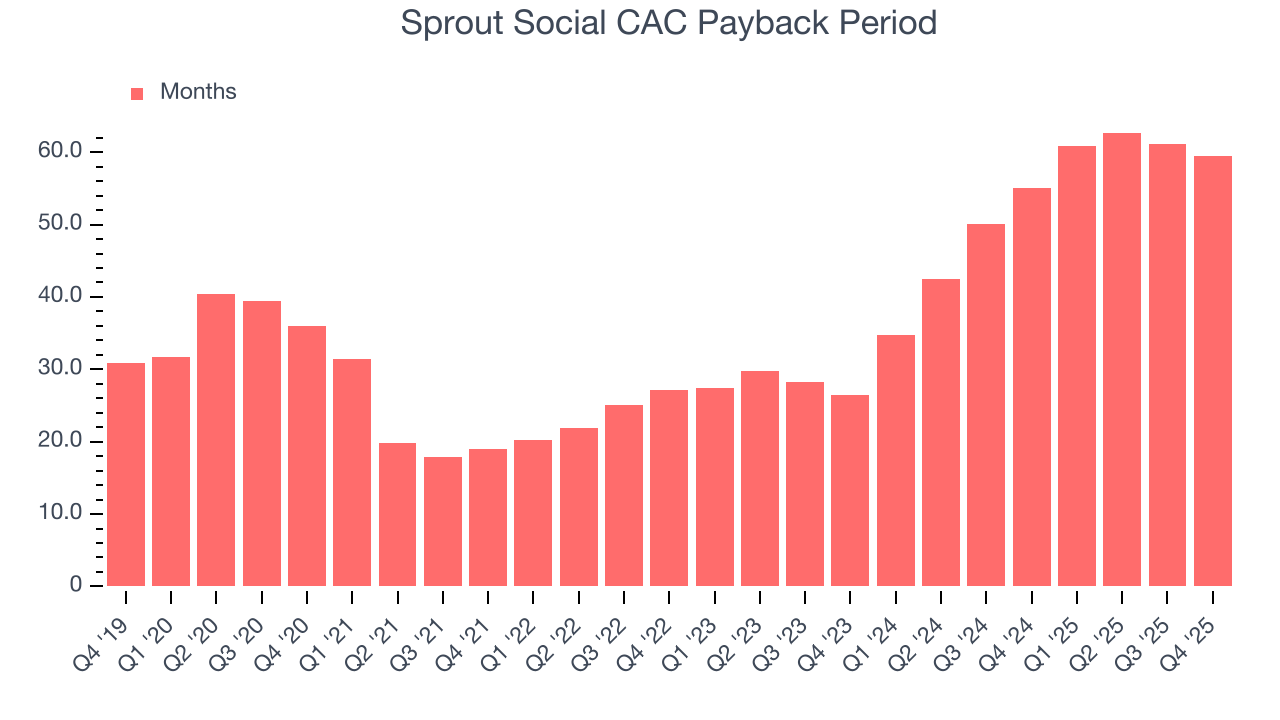

8. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Sprout Social to acquire new customers as its CAC payback period checked in at 59.4 months this quarter. The company’s drawn-out sales cycles partly stem from its focus on enterprise clients who require some degree of customization, resulting in long onboarding periods that delay delay returns and limit customer growth.

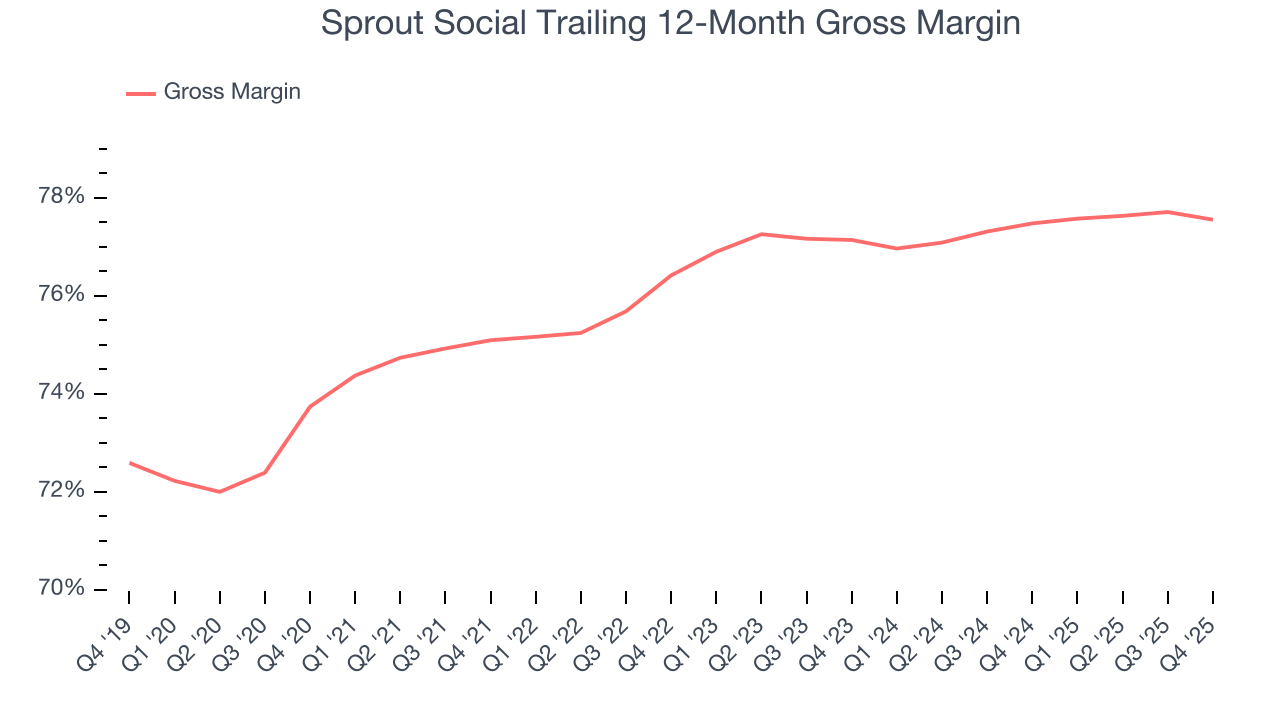

9. Gross Margin & Pricing Power

For software companies like Sprout Social, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Sprout Social’s robust unit economics are better than the broader software industry, an output of its asset-lite business model and pricing power. They also enable the company to fund large investments in new products and sales during periods of rapid growth to achieve outsized profits at scale. As you can see below, it averaged an excellent 77.6% gross margin over the last year. That means Sprout Social only paid its providers $22.44 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Sprout Social has seen gross margins improve by 0.4 percentage points over the last 2 year, which is slightly better than average for software.

This quarter, Sprout Social’s gross profit margin was 77.6%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

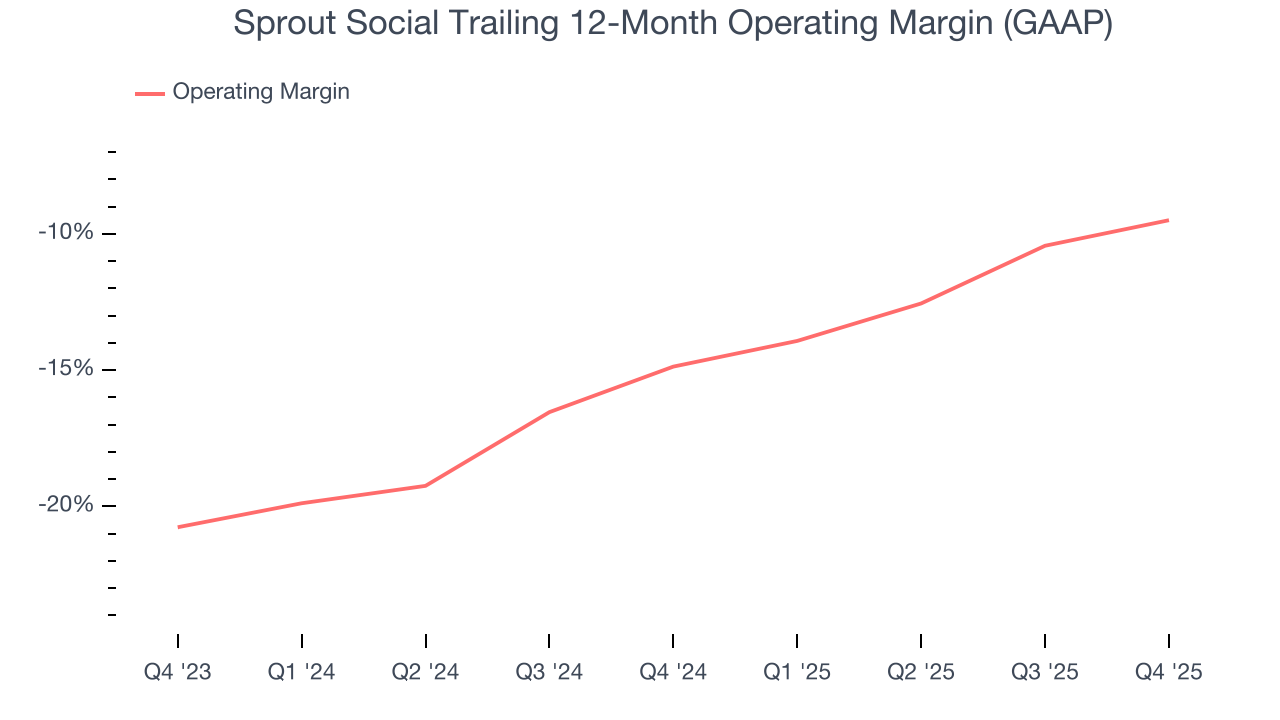

10. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Sprout Social’s expensive cost structure has contributed to an average operating margin of negative 9.5% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Sprout Social reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

Over the last two years, Sprout Social’s expanding sales gave it operating leverage as its margin rose by 5.4 percentage points. Still, it will take much more for the company to reach long-term profitability.

In Q4, Sprout Social generated a negative 9% operating margin.

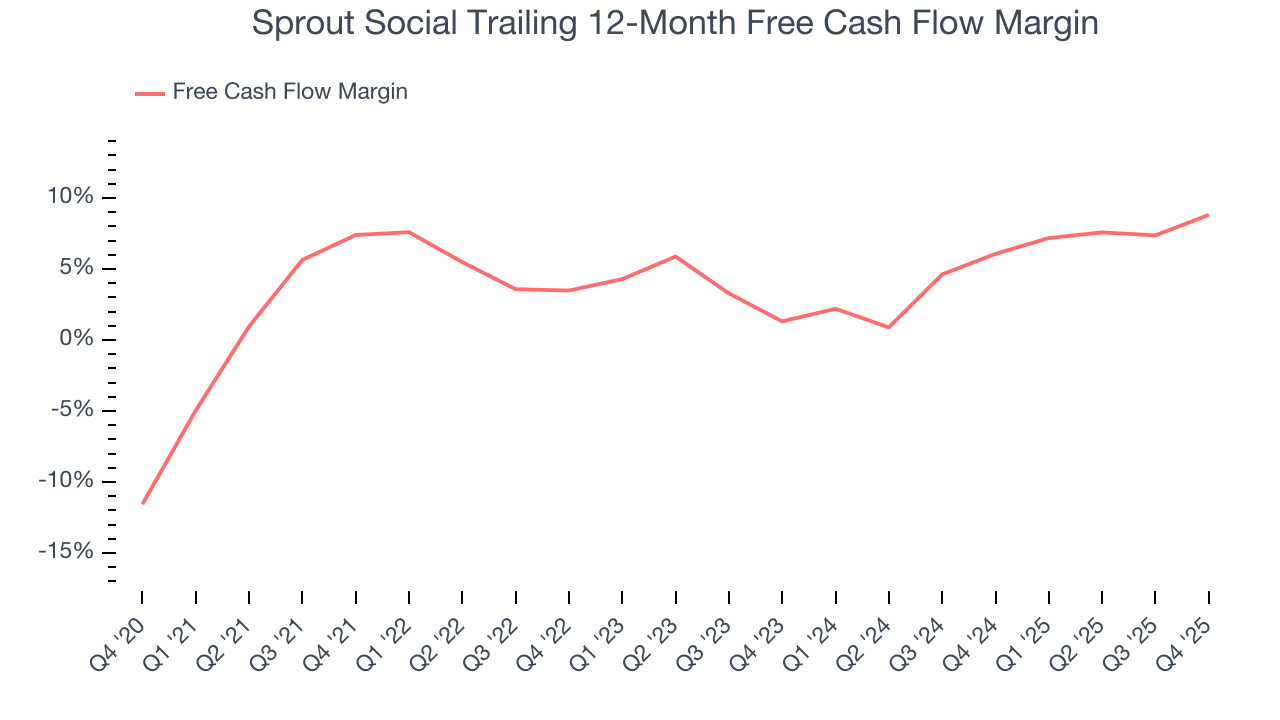

11. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Sprout Social has shown weak cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 8.8%, subpar for a software business.

Sprout Social’s free cash flow clocked in at $10.88 million in Q4, equivalent to a 9% margin. This result was good as its margin was 6 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

Over the next year, analysts predict Sprout Social’s cash conversion will slightly improve. Their consensus estimates imply its free cash flow margin of 8.8% for the last 12 months will increase to 10.3%, it options for capital deployment (investments, share buybacks, etc.).

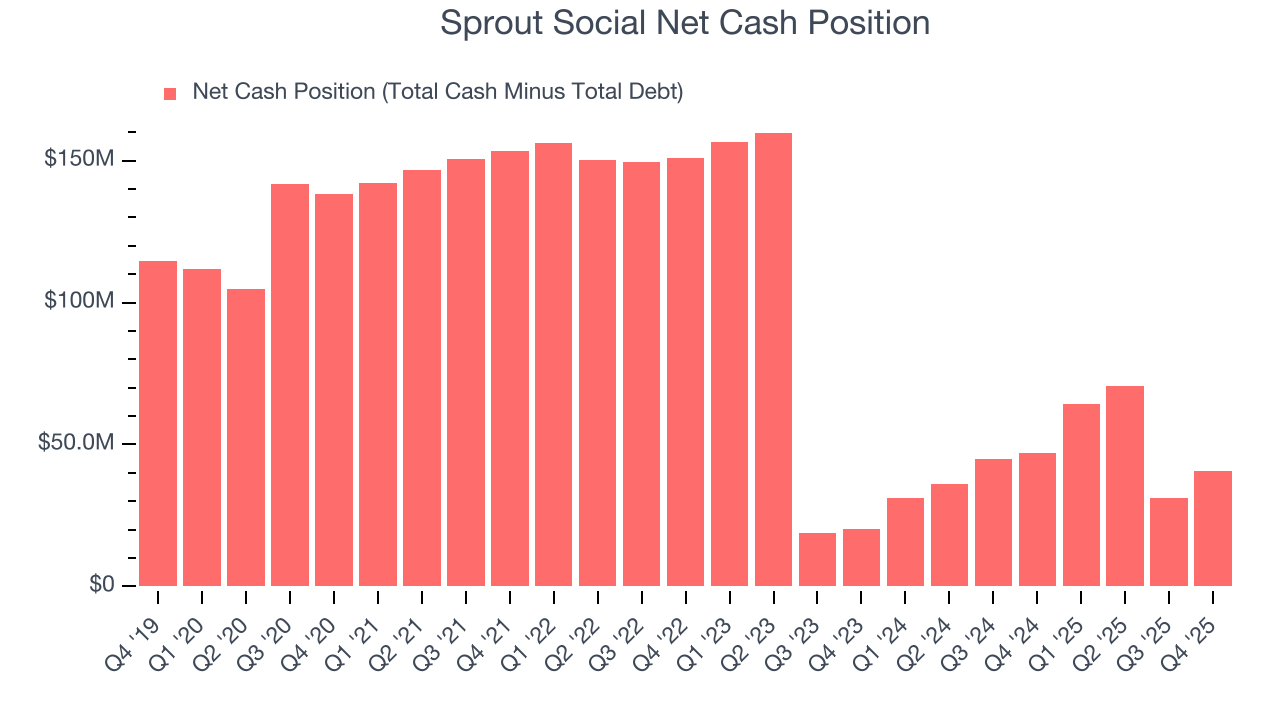

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Sprout Social is a well-capitalized company with $95.27 million of cash and $54.72 million of debt on its balance sheet. This $40.55 million net cash position is 10.6% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Sprout Social’s Q4 Results

It was great to see Sprout Social’s full-year EPS guidance top analysts’ expectations. We were also glad its billings outperformed Wall Street’s estimates. On the other hand, its EPS guidance for next quarter missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock remained flat at $7.13 immediately after reporting.

14. Is Now The Time To Buy Sprout Social?

Updated: March 14, 2026 at 10:20 PM EDT

Before deciding whether to buy Sprout Social or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Sprout Social isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was strong over the last five years, it’s expected to deteriorate over the next 12 months and its operating margins reveal poor profitability compared to other software companies. And while the company’s gross margin suggests it can generate sustainable profits, the downside is its expanding operating margin shows it’s becoming more efficient at building and selling its software.

Sprout Social’s price-to-sales ratio based on the next 12 months is 0.7x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $9.60 on the company (compared to the current share price of $5.86).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.