Upland Software (UPLD)

We wouldn’t recommend Upland Software. Its shrinking sales suggest demand is waning and its lousy free cash flow generation doesn’t do it any favors.― StockStory Analyst Team

1. News

2. Summary

Why We Think Upland Software Will Underperform

Operating under the mantra "land and expand," Upland Software (NASDAQ:UPLD) provides cloud-based applications that help organizations manage projects, workflows, and digital transformation across various business functions.

- Sales tumbled by 5.8% annually over the last five years, showing industry trends like AI are working against its favor

- Forecasted revenue decline of 7.7% for the upcoming 12 months implies demand will fall even further

- Competitive market means the company must spend more on sales and marketing to stand out even if the return on investment is low

Upland Software doesn’t fulfill our quality requirements. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Upland Software

At $0.56 per share, Upland Software trades at 0.1x forward price-to-sales. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Upland Software (UPLD) Research Report: Q4 CY2025 Update

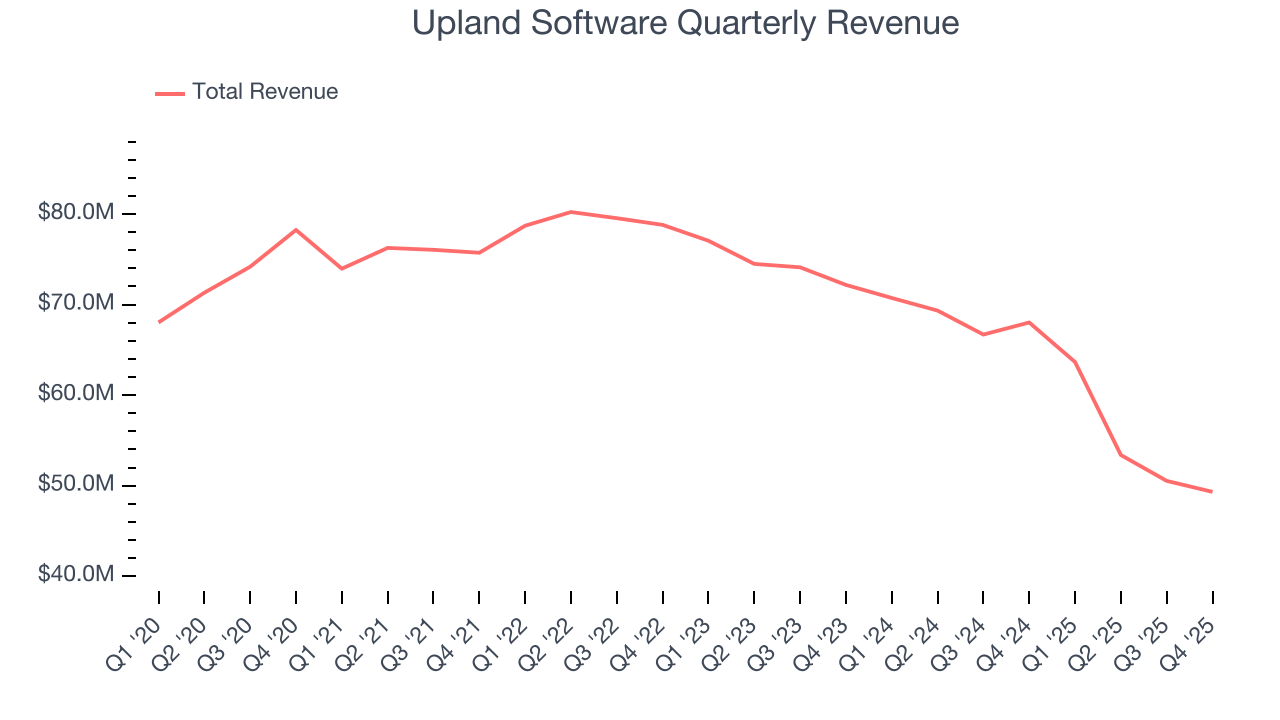

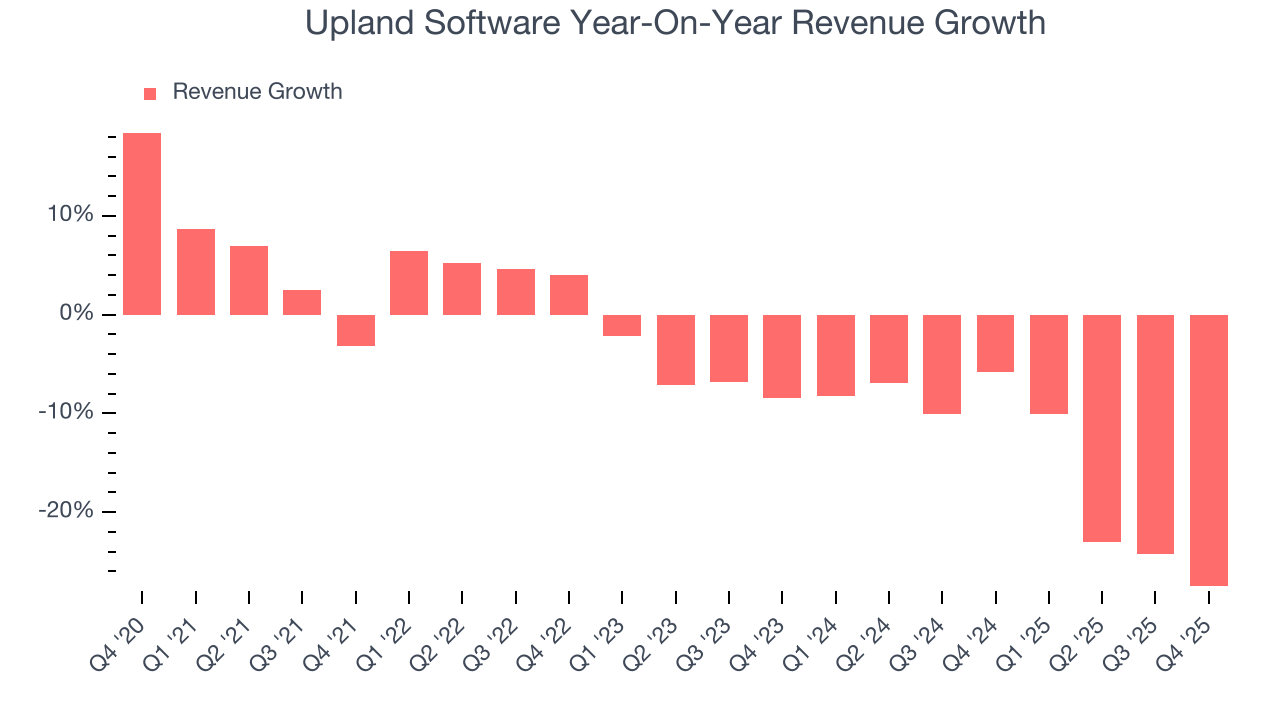

Cloud software provider Upland Software (NASDAQ:UPLD) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 27.5% year on year to $49.31 million. Next quarter’s revenue guidance of $48.5 million underwhelmed, coming in 4.4% below analysts’ estimates. Its non-GAAP profit of $0.24 per share was 24.1% above analysts’ consensus estimates.

Upland Software (UPLD) Q4 CY2025 Highlights:

- Revenue: $49.31 million vs analyst estimates of $49.99 million (27.5% year-on-year decline, 1.4% miss)

- Adjusted EPS: $0.24 vs analyst estimates of $0.19 (24.1% beat)

- Adjusted EBITDA: $15.31 million vs analyst estimates of $16.09 million (31.1% margin, 4.8% miss)

- Revenue Guidance for Q1 CY2026 is $48.5 million at the midpoint, below analyst estimates of $50.73 million

- EBITDA guidance for the upcoming financial year 2026 is $55.6 million at the midpoint, below analyst estimates of $61.17 million

- Operating Margin: 14.5%, up from -2.9% in the same quarter last year

- Free Cash Flow Margin: 14.7%, up from 13.2% in the previous quarter

- Market Capitalization: $25.43 million

Company Overview

Operating under the mantra "land and expand," Upland Software (NASDAQ:UPLD) provides cloud-based applications that help organizations manage projects, workflows, and digital transformation across various business functions.

Upland's software suite spans eight key functional areas: marketing, sales, contact center, knowledge management, project management, IT, business operations, and human resources/legal. This diverse portfolio allows the company to address numerous business needs, from strategic planning to everyday task execution. Each solution aims to improve productivity, streamline processes, and enhance collaboration within organizations.

The company generates revenue primarily through subscription-based pricing models, with contracts typically ranging from one to three years. Subscriptions are sold either on a per-seat basis or with minimum contracted volumes plus overage fees. Upland has built its product portfolio through numerous acquisitions—31 in total over a 12-year period ending in 2023—which it integrates through its "UplandOne" operating platform.

For example, a marketing department might use Upland's applications to run email campaigns and analyze customer feedback, while a project management office could employ different Upland tools to optimize resource allocation and track deliverables. The company serves over 10,000 customers across industries including financial services, technology, healthcare, government, and retail, with a particular focus on mid-sized to large enterprises designated as "major accounts."

4. Marketing Software

Whether or not companies market their products through social media, all businesses need to meet customers where they are; and increasingly, that is social media. As more and more people use a greater number of social media platforms, social media management software become more valuable to their customers.

Upland Software competes with larger enterprise software providers like Microsoft (NASDAQ:MSFT), Salesforce (NYSE:CRM), and Adobe (NASDAQ:ADBE), as well as specialized cloud software vendors such as Monday.com (NASDAQ:MNDY), Atlassian (NASDAQ:TEAM), and HubSpot (NYSE:HUBS).

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Upland Software’s demand was weak over the last five years as its sales fell at a 5.8% annual rate. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within software, a half-decade historical view may miss new innovations or demand cycles. Upland Software’s recent performance shows its demand remained suppressed as its revenue has declined by 14.7% annually over the last two years.

This quarter, Upland Software missed Wall Street’s estimates and reported a rather uninspiring 27.5% year-on-year revenue decline, generating $49.31 million of revenue. Company management is currently guiding for a 23.8% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 5.8% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

6. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Upland Software’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between Upland Software’s products and its peers.

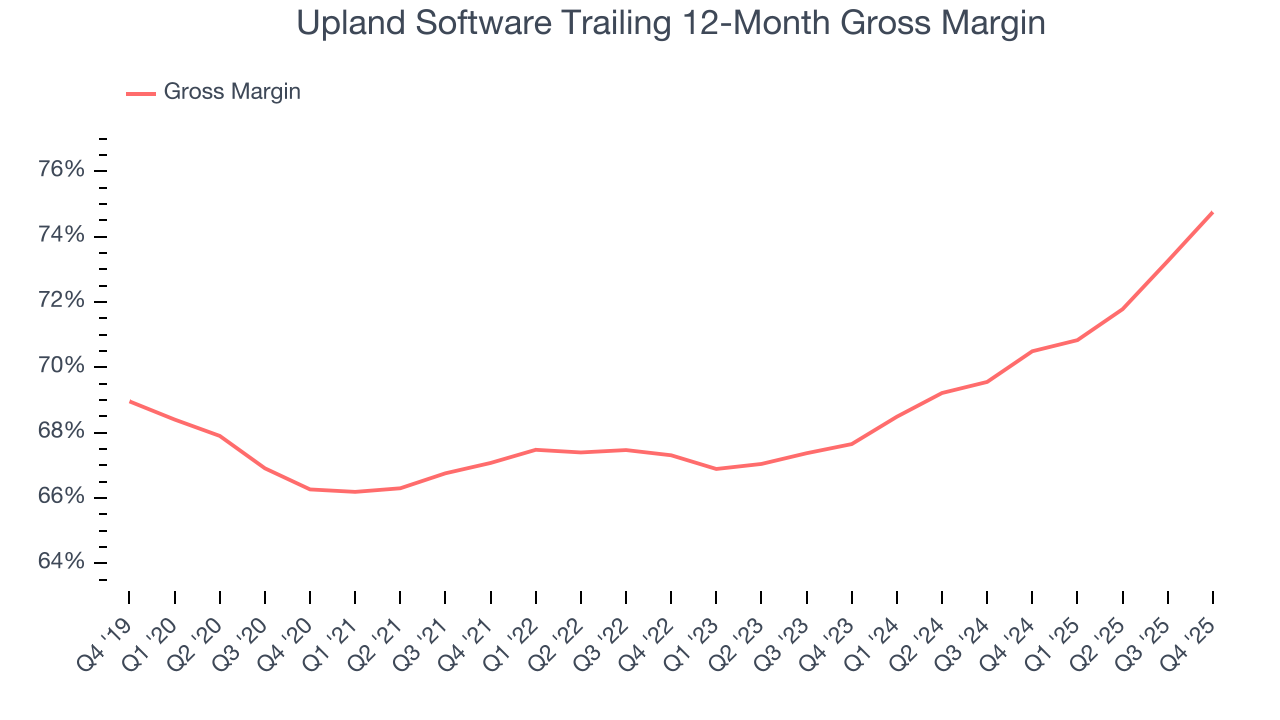

7. Gross Margin & Pricing Power

For software companies like Upland Software, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Upland Software’s gross margin is better than the broader software industry and signals it has solid unit economics and competitive products. As you can see below, it averaged a decent 74.8% gross margin over the last year. Said differently, Upland Software paid its providers $25.25 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Upland Software has seen gross margins improve by 7.1 percentage points over the last 2 year, which is elite in the software space.

In Q4, Upland Software produced a 76.5% gross profit margin, up 5.7 percentage points year on year. Upland Software’s full-year margin has also been trending up over the past 12 months, increasing by 4.3 percentage points. If this move continues, it could suggest better unit economics due to some combination of stable to improving pricing power and input costs.

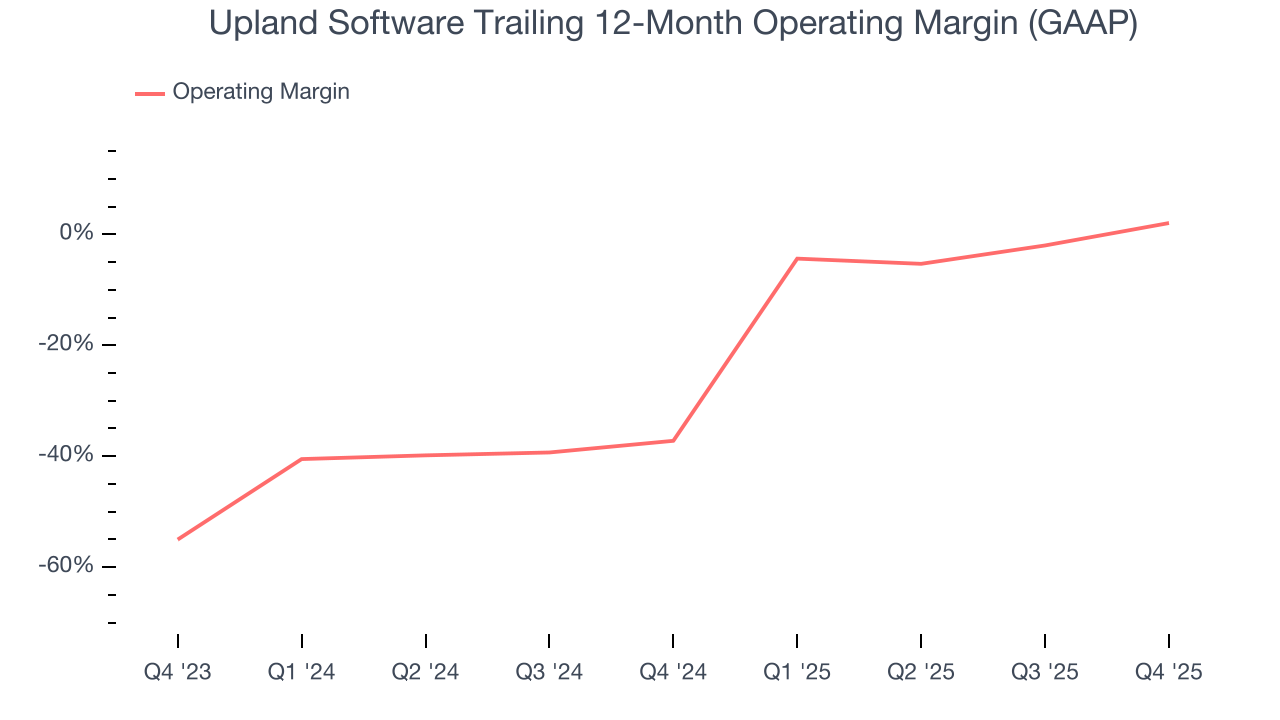

8. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This is one of the best measures of profitability because it shows how much money a company takes home after developing, marketing, and selling its products.

Upland Software has done a decent job managing its cost base over the last year. The company has produced an average operating margin of 2%, higher than the broader software sector.

Looking at the trend in its profitability, Upland Software’s operating margin rose by 39.3 percentage points over the last two years, showing its efficiency has meaningfully improved.

This quarter, Upland Software generated an operating margin profit margin of 14.5%, up 17.4 percentage points year on year. The increase was solid, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

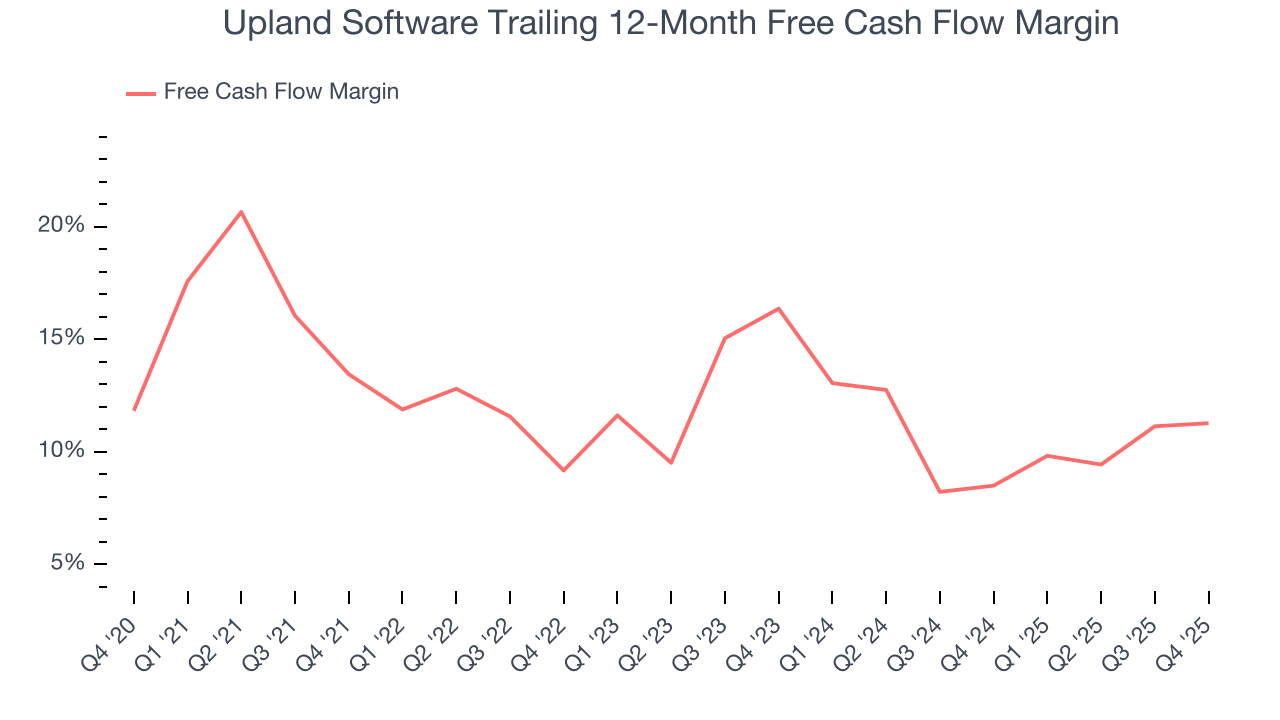

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Upland Software has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 11.3%, subpar for a software business.

Upland Software’s free cash flow clocked in at $7.23 million in Q4, equivalent to a 14.7% margin. This result was good as its margin was 1.4 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting Upland Software’s free cash flow margin of 11.3% for the last 12 months to remain the same.

10. Balance Sheet Assessment

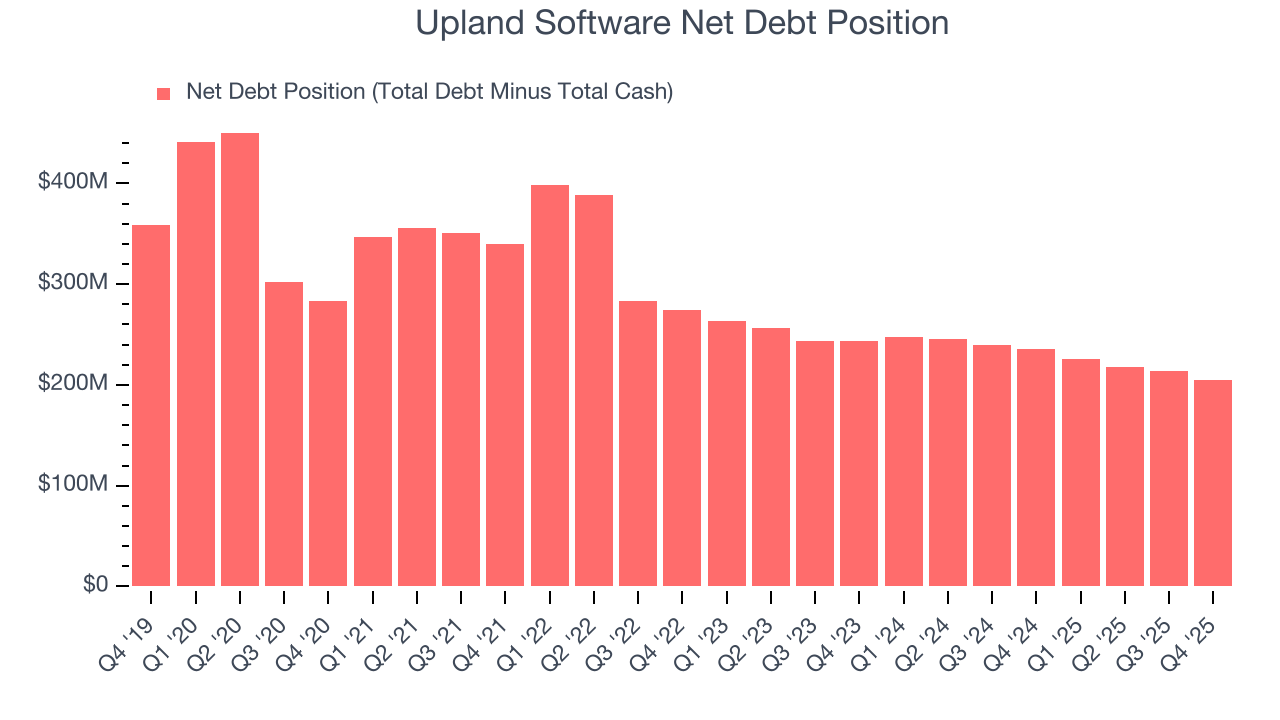

Upland Software reported $30.02 million of cash and $235.2 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $58.01 million of EBITDA over the last 12 months, we view Upland Software’s 3.5× net-debt-to-EBITDA ratio as safe. We also see its $15.79 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Upland Software’s Q4 Results

It was great to see Upland Software expecting revenue growth to accelerate next year. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 14.3% to $0.76 immediately following the results.

12. Is Now The Time To Buy Upland Software?

Updated: March 13, 2026 at 10:23 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Upland Software, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies solving complex business issues, but in the case of Upland Software, we’ll be cheering from the sidelines. For starters, its revenue has declined over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its expanding operating margin shows it took many unnecessary costs out of the business, the downside is its customer acquisition is less efficient than many comparable companies. On top of that, its low free cash flow margins give it little breathing room.

Upland Software’s price-to-sales ratio based on the next 12 months is 0.1x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $3.75 on the company (compared to the current share price of $0.56).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.