3D Systems (DDD)

3D Systems is up against the odds. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think 3D Systems Will Underperform

Founded by the inventor of stereolithography, 3D Systems (NYSE:DDD) engineers, manufactures, and sells 3D printers and other related products to the aerospace, automotive, healthcare, and consumer goods industries.

- Annual sales declines of 7% for the past five years show its products and services struggled to connect with the market during this cycle

- Earnings per share decreased by more than its revenue over the last five years, showing each sale was less profitable

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

3D Systems’s quality isn’t great. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than 3D Systems

At $2.14 per share, 3D Systems trades at 0.7x forward price-to-sales. The market typically values companies like 3D Systems based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

It’s better to invest in high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. 3D Systems (DDD) Research Report: Q4 CY2025 Update

3D printing company 3D Systems (NYSE:DDD) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 4.3% year on year to $106.3 million. On top of that, next quarter’s revenue guidance ($92.5 million at the midpoint) was surprisingly good and 3.5% above what analysts were expecting. Its non-GAAP loss of $0.13 per share was 40.5% below analysts’ consensus estimates.

3D Systems (DDD) Q4 CY2025 Highlights:

- Revenue: $106.3 million vs analyst estimates of $97.92 million (4.3% year-on-year decline, 8.5% beat)

- Adjusted EPS: -$0.13 vs analyst expectations of -$0.09 (40.5% miss)

- Adjusted EBITDA: -$5.3 million (-5% margin, 70.8% year-on-year growth)

- Revenue Guidance for Q1 CY2026 is $92.5 million at the midpoint, above analyst estimates of $89.41 million

- EBITDA guidance for Q1 CY2026 is -$4 million at the midpoint, above analyst estimates of -$7.13 million

- Adjusted EBITDA Margin: -5%, up from -16.4% in the same quarter last year

- Free Cash Flow was -$16.65 million compared to -$13.1 million in the same quarter last year

- Market Capitalization: $286.3 million

Company Overview

Founded by the inventor of stereolithography, 3D Systems (NYSE:DDD) engineers, manufactures, and sells 3D printers and other related products to the aerospace, automotive, healthcare, and consumer goods industries.

3D Systems was established in 1986 by Chuck Hull, who is credited with inventing stereolithography, a process that enabled the creation of a three-dimensional object from a digital model. This breakthrough led to the development of the first commercial 3D printer.

The company quickly became a leader in the 3D printing industry, contributing significantly to the evolution of rapid prototyping and additive manufacturing technologies. Over the years, 3D Systems has expanded its technology portfolio to include various 3D printing methods, materials, software, and healthcare solutions.

Today, the company's suite of 3D printers is critical in manufacturing sectors including aerospace, automotive, and industrial goods, enabling rapid prototyping, tooling, and direct production of complex parts. These capabilities significantly reduce lead times and costs while improving product performance and customization.

In the healthcare sector, 3D Systems leverages its technology to revolutionize medical practices by producing patient-specific implants, prosthetics, and surgical planning tools. The precision and adaptability of 3D printing meet the needs of medical professionals, improving patient outcomes and surgical efficiencies.

Additionally, the company supports the manufacturing industry and the medical community with software for design and simulation. The company’s software services provide a source of recurring revenue through ongoing updates and licenses. By partnering with companies and institutions, 3D Systems leverages its expertise to co-create solutions.

The company engages in contracts with customers ranging from small businesses to large enterprises, often involving pricing agreements, volume commitments, and ongoing support contracts, which enhance financial stability and predictability.

4. Custom Parts Manufacturing

Onshoring and inventory management–themes that grew in focus after COVID wreaked havoc on global supply chains–are tailwinds for companies that combine economies of scale with reliable service. Many in the space have adopted 3D printing to efficiently address the need for bespoke parts and components, but all companies are still at the whim of economic cycles. For example, consumer spending and interest rates can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Stratasys (NASDAQ:SSYS), EOS (private), HP (NYSE:HPQ), and Desktop Metal (NYSE:DM).

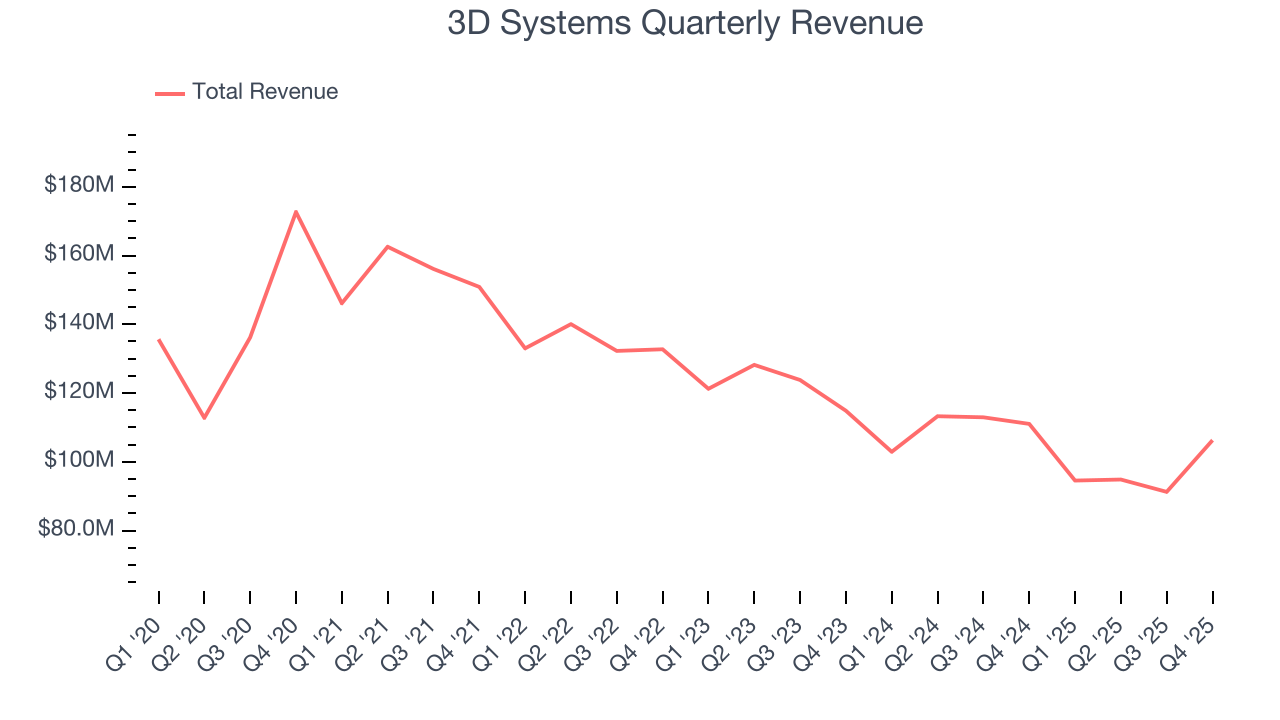

5. Revenue Growth

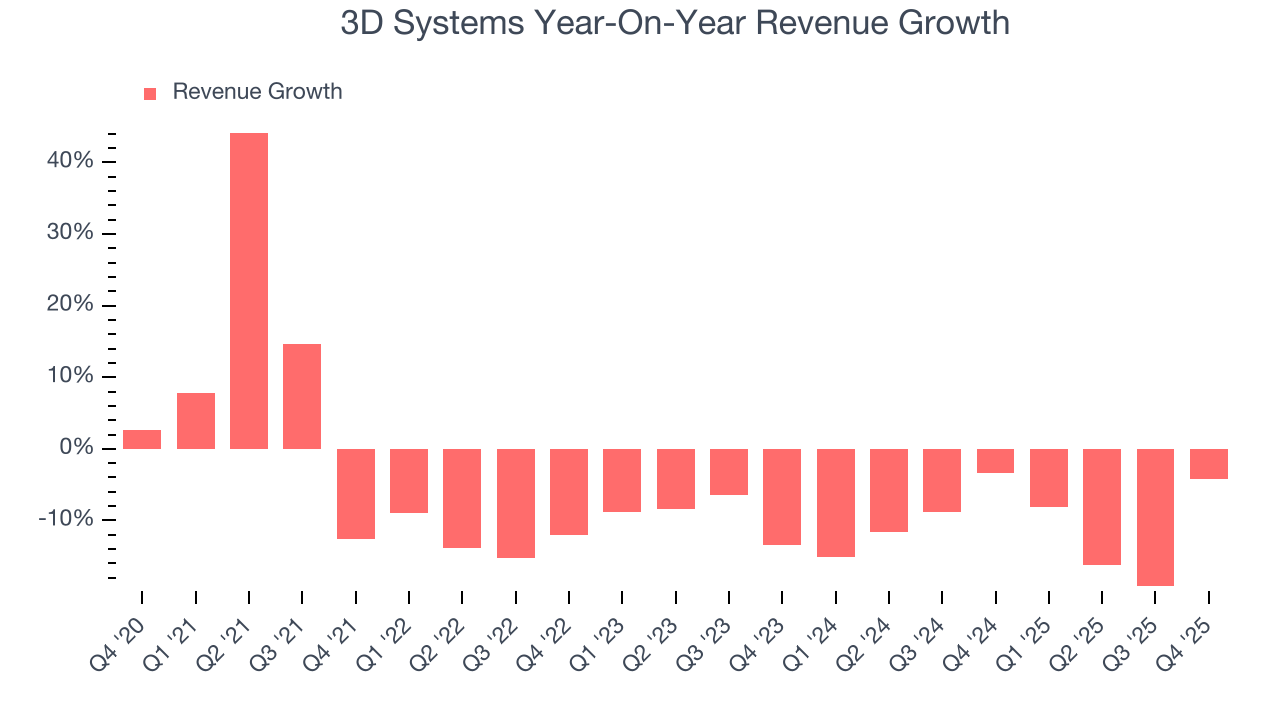

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last five years, 3D Systems’s demand was weak and its revenue declined by 7% per year. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. 3D Systems’s recent performance shows its demand remained suppressed as its revenue has declined by 11% annually over the last two years.

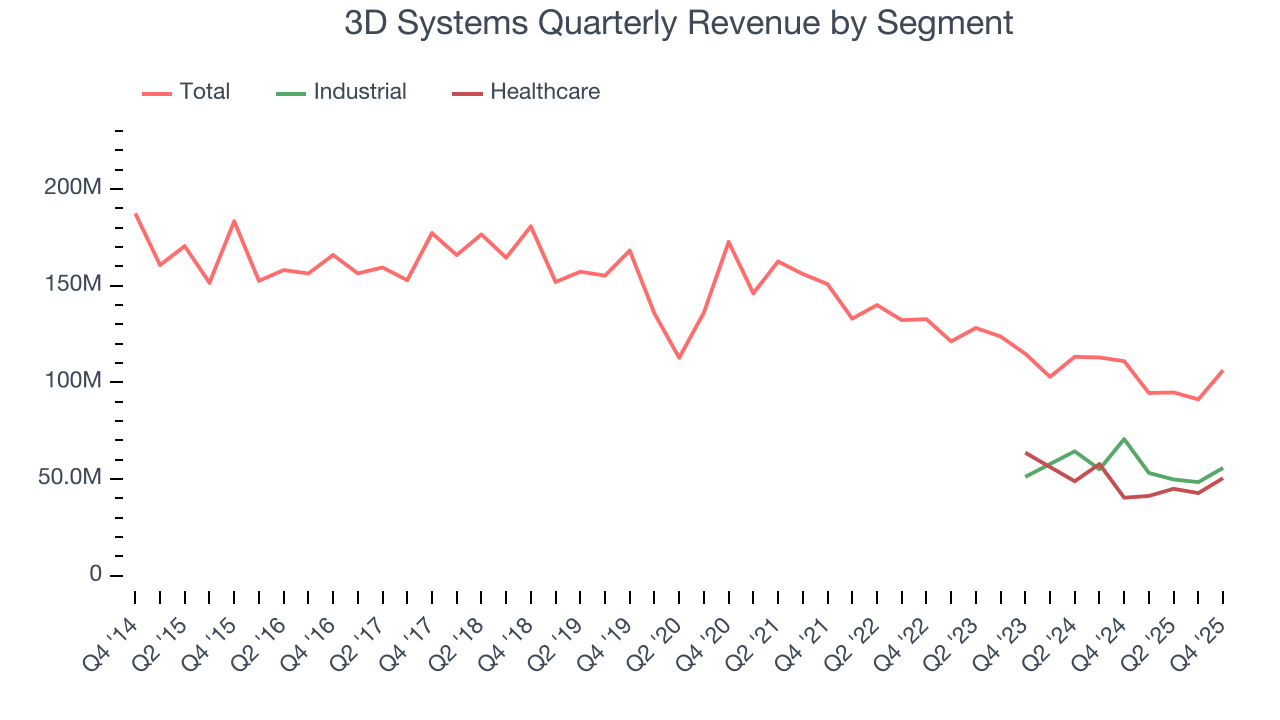

We can better understand the company’s revenue dynamics by analyzing its most important segments, Industrial and Healthcare, which are 52.5% and 47.5% of revenue. Over the last two years, 3D Systems’s Industrial revenue (aerospace, defense, and transportation manufacturing) averaged 4.4% year-on-year declines while its Healthcare revenue (dental and medical devices) averaged 11.4% declines.

This quarter, 3D Systems’s revenue fell by 4.3% year on year to $106.3 million but beat Wall Street’s estimates by 8.5%. Company management is currently guiding for a 2.2% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 1.4% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

6. Gross Margin & Pricing Power

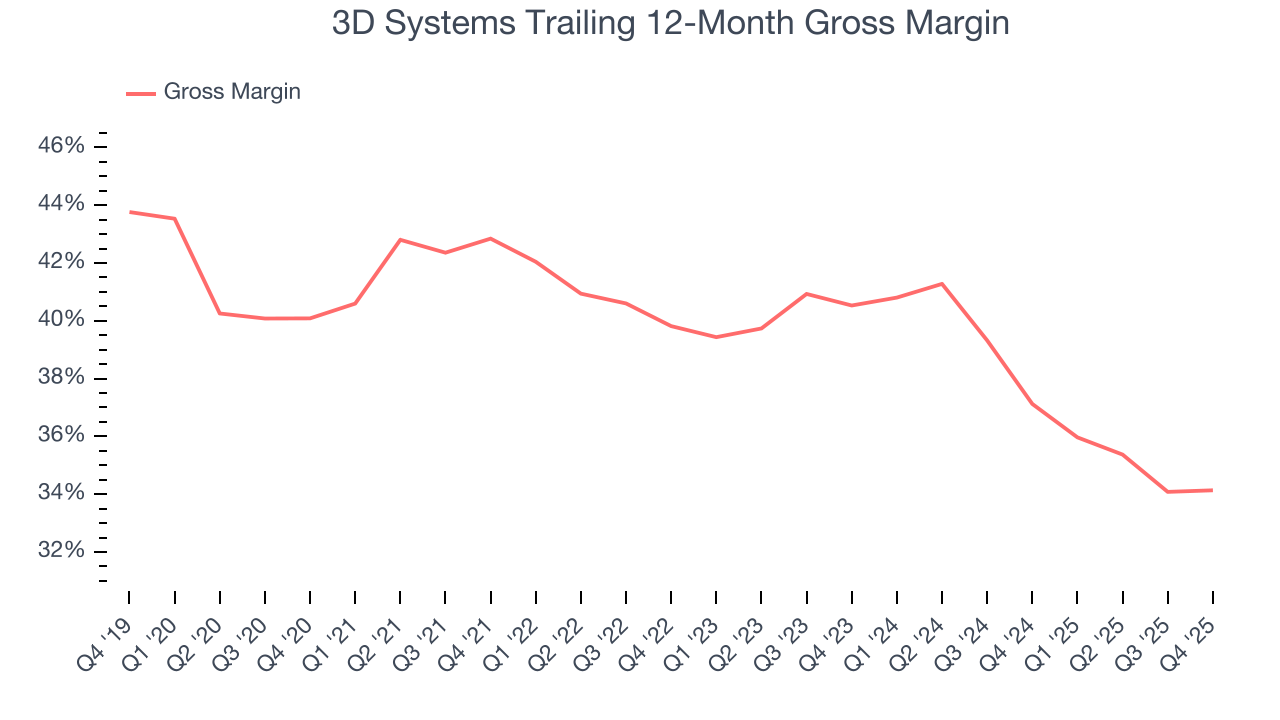

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

3D Systems’s unit economics are great compared to the broader industrials sector and signal that it enjoys product differentiation through quality or brand. As you can see below, it averaged an excellent 39.3% gross margin over the last five years. That means 3D Systems only paid its suppliers $60.66 for every $100 in revenue.

In Q4, 3D Systems produced a 30.8% gross profit margin, in line with the same quarter last year. Zooming out, 3D Systems’s full-year margin has been trending down over the past 12 months, decreasing by 3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

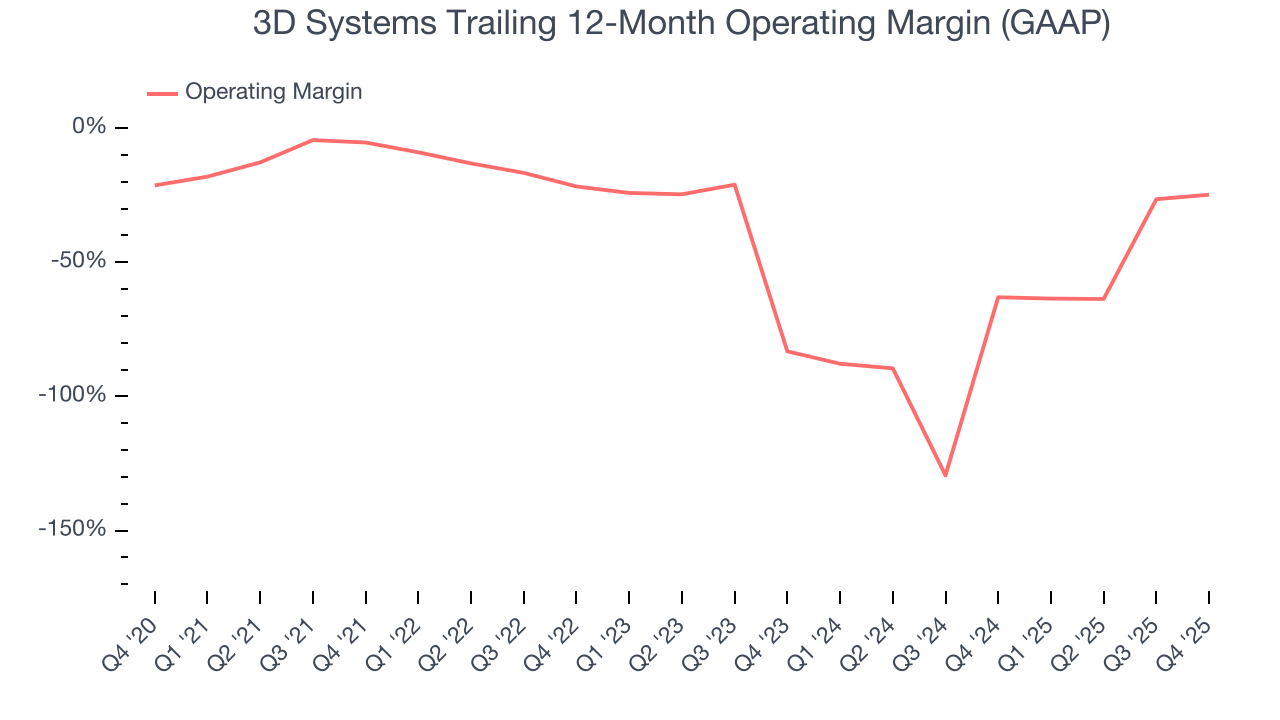

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

3D Systems’s high expenses have contributed to an average operating margin of negative 37.7% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Looking at the trend in its profitability, 3D Systems’s operating margin decreased by 19.5 percentage points over the last five years. 3D Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

3D Systems’s operating margin was negative 21.3% this quarter. The company's consistent lack of profits raise a flag.

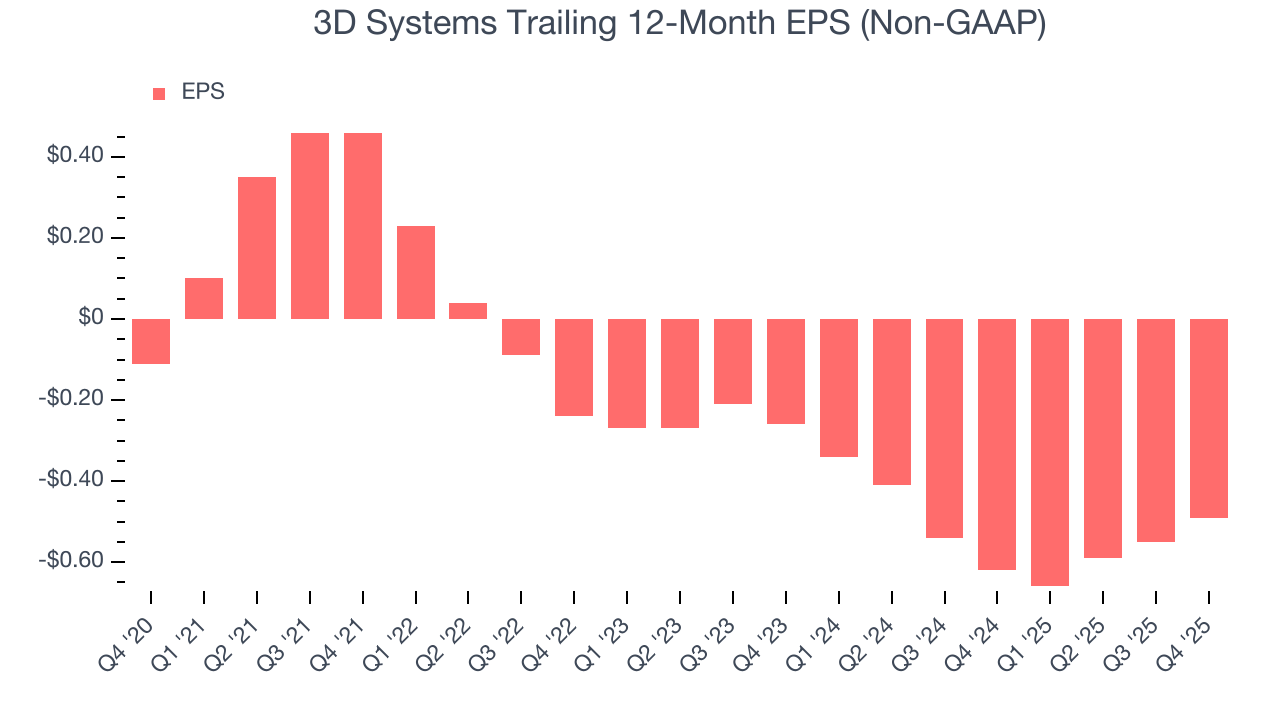

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

3D Systems’s earnings losses deepened over the last five years as its EPS dropped 34.8% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, 3D Systems’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For 3D Systems, its two-year annual EPS declines of 37.3% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, 3D Systems reported adjusted EPS of negative $0.13, up from negative $0.19 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects 3D Systems to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.49 will advance to negative $0.29.

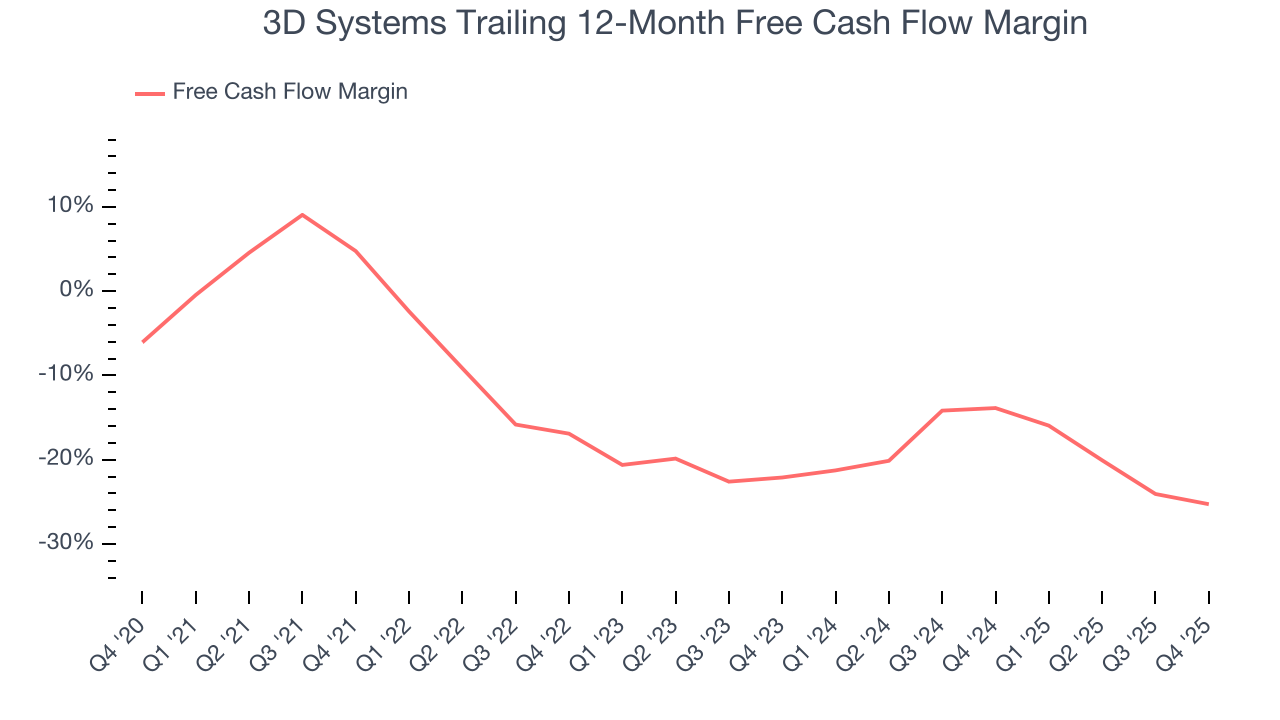

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

3D Systems’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 13.3%, meaning it lit $13.30 of cash on fire for every $100 in revenue.

Taking a step back, we can see that 3D Systems’s margin dropped by 30 percentage points during that time. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

3D Systems burned through $16.65 million of cash in Q4, equivalent to a negative 15.7% margin. The company’s cash burn was similar to its $13.1 million of lost cash in the same quarter last year.

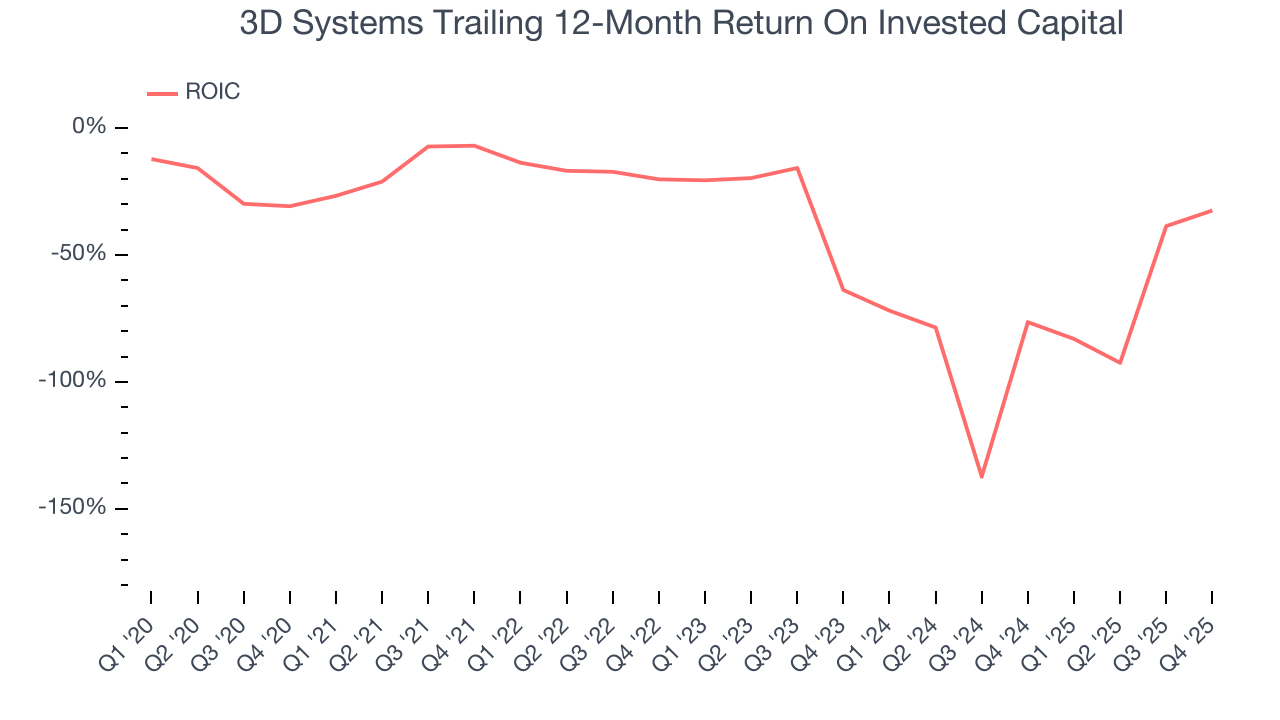

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

3D Systems’s five-year average ROIC was negative 40%, meaning management lost money while trying to expand the business. Its returns were among the worst in the industrials sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, 3D Systems’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

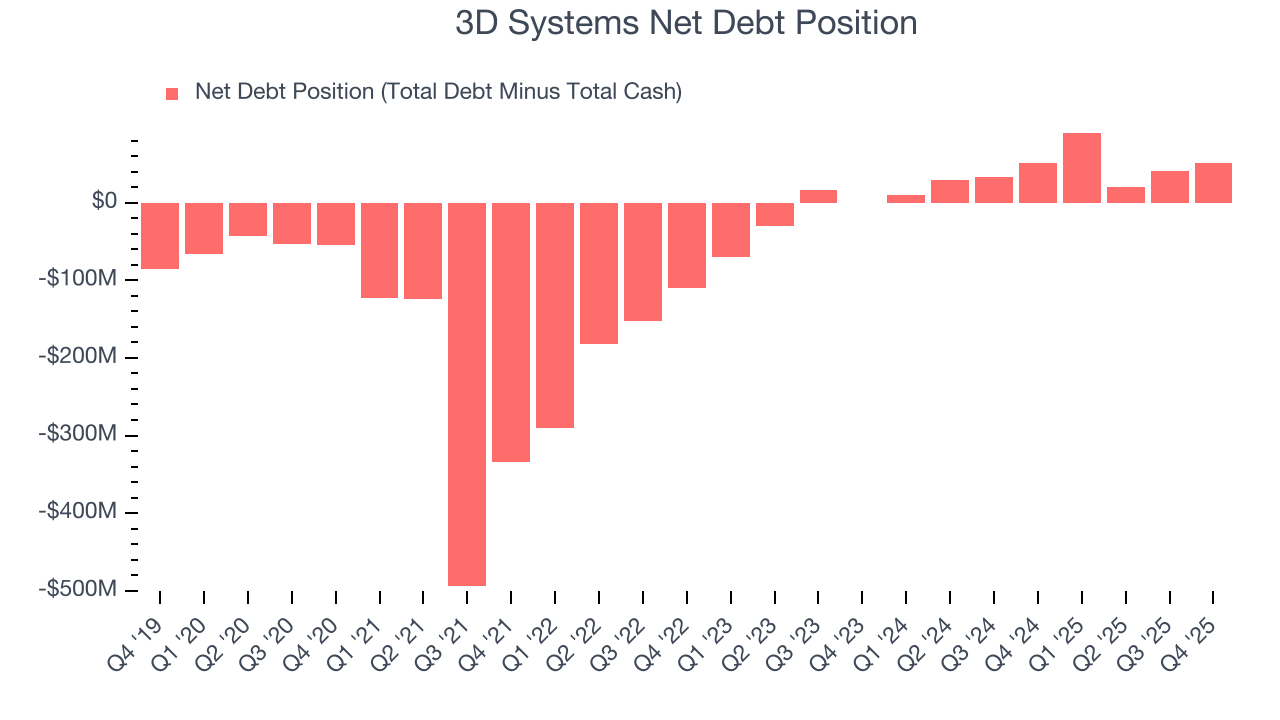

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

3D Systems burned through $97.77 million of cash over the last year, and its $147.3 million of debt exceeds the $95.64 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the 3D Systems’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of 3D Systems until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

12. Key Takeaways from 3D Systems’s Q4 Results

We were impressed by 3D Systems’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue and EBITDA outperformed Wall Street’s estimates by wide margins. Overall, we think this was a very solid quarter with some key areas of upside. The stock traded up 9.5% to $2.12 immediately following the results.

13. Is Now The Time To Buy 3D Systems?

Updated: March 18, 2026 at 11:47 PM EDT

Before making an investment decision, investors should account for 3D Systems’s business fundamentals and valuation in addition to what happened in the latest quarter.

3D Systems falls short of our quality standards. To begin with, its revenue has declined over the last five years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

3D Systems’s forward price-to-sales ratio is 0.7x. The market typically values companies like 3D Systems based on their anticipated profits for the next 12 months, but it expects the business to lose money. We also think the upside isn’t great compared to the potential downside here - there are more exciting stocks to buy.

Wall Street analysts have a consensus one-year price target of $3.75 on the company (compared to the current share price of $2.14).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.