Organon (OGN)

We’re wary of Organon. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think Organon Will Underperform

Spun off from Merck in 2021 to create a company dedicated to addressing unmet needs in women's health, Organon (NYSE:OGN) is a global healthcare company focused on improving women's health through prescription therapies, medical devices, biosimilars, and established medicines.

- Falling earnings per share over the last four years has some investors worried as stock prices ultimately follow EPS over the long term

- Sales were flat over the last five years, indicating it’s failed to expand this cycle

- The good news is that its disciplined cost controls and effective management have materialized in a strong adjusted operating margin

Organon doesn’t meet our quality criteria. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Organon

At $6.37 per share, Organon trades at 1.8x forward P/E. Organon’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Organon (OGN) Research Report: Q4 CY2025 Update

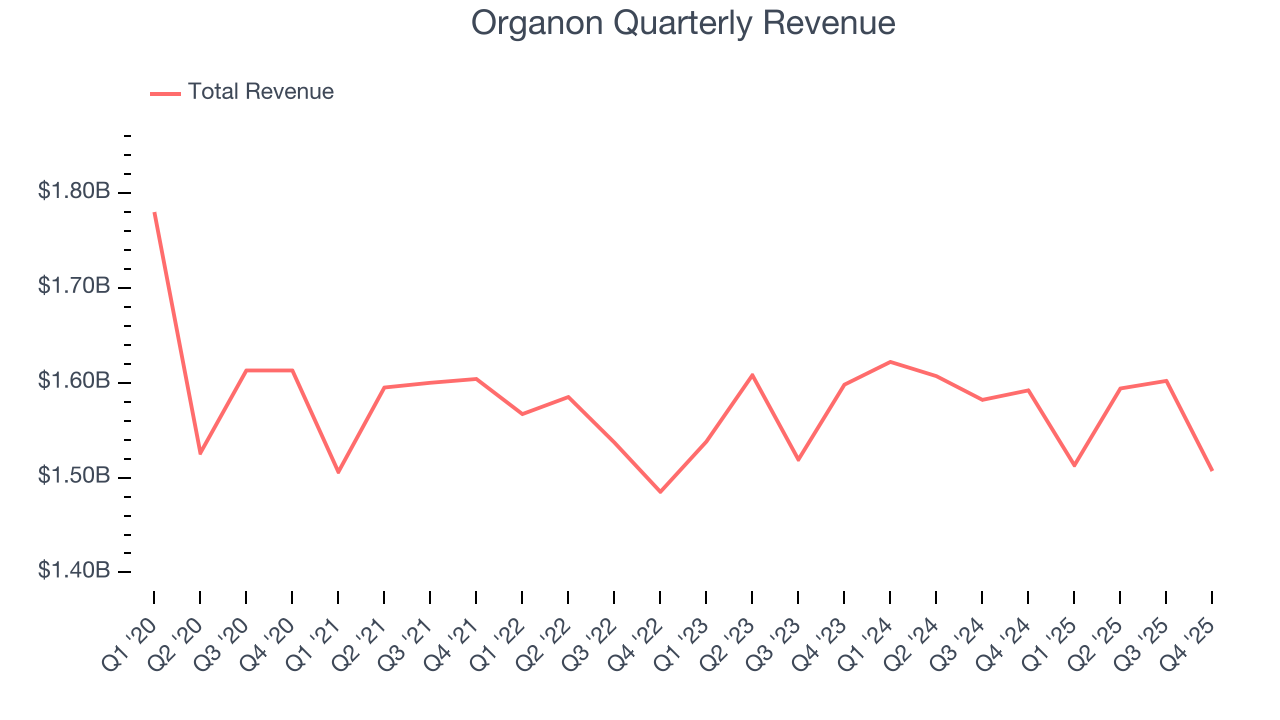

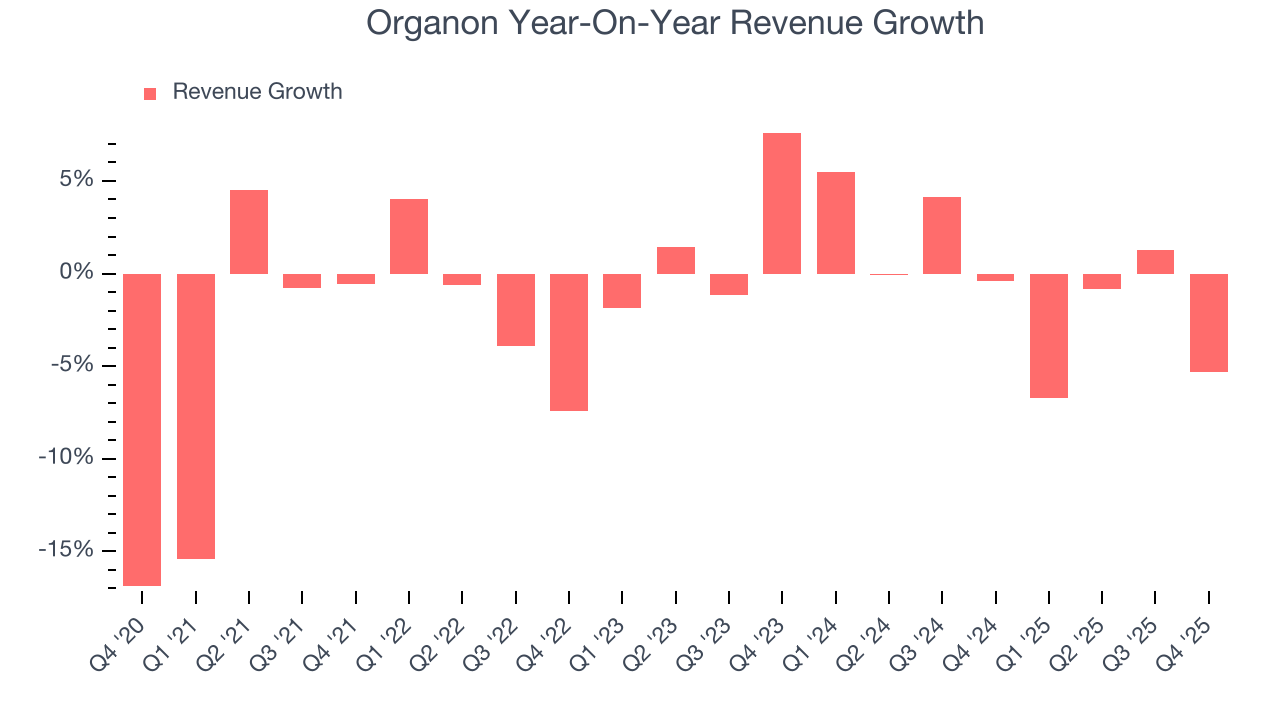

Pharmaceutical company Organon (NYSE:OGN) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 5.3% year on year to $1.51 billion. The company’s full-year revenue guidance of $6.2 billion at the midpoint came in 1.5% above analysts’ estimates. Its non-GAAP profit of $0.63 per share was 13.3% below analysts’ consensus estimates.

Organon (OGN) Q4 CY2025 Highlights:

- Revenue: $1.51 billion vs analyst estimates of $1.51 billion (5.3% year-on-year decline, in line)

- Adjusted EPS: $0.63 vs analyst expectations of $0.73 (13.3% miss)

- Adjusted EBITDA: $383 million vs analyst estimates of $390.2 million (25.4% margin, 1.8% miss)

- EBITDA guidance for the upcoming financial year 2026 is $1.9 billion at the midpoint, in line with analyst expectations

- Operating Margin: -9.8%, down from 18.1% in the same quarter last year

- Market Capitalization: $2.00 billion

Company Overview

Spun off from Merck in 2021 to create a company dedicated to addressing unmet needs in women's health, Organon (NYSE:OGN) is a global healthcare company focused on improving women's health through prescription therapies, medical devices, biosimilars, and established medicines.

Organon's business is structured around three key portfolios. Its women's health division, which generates about 27% of total revenue, includes contraceptive products like Nexplanon (a long-acting reversible contraceptive implant) and NuvaRing (a vaginal contraceptive ring), as well as fertility treatments such as Follistim AQ. The company also markets the Jada System for treating postpartum hemorrhage and Xaciato for bacterial vaginosis.

The biosimilars portfolio includes lower-cost alternatives to popular biologic medications across immunology and oncology. These include Hadlima (biosimilar to Humira), Brenzys (biosimilar to Enbrel), Renflexis (biosimilar to Remicade), and oncology treatments Ontruzant (biosimilar to Herceptin) and Aybintio (biosimilar to Avastin). Organon has commercialization rights to these products in various global markets through partnerships with companies like Samsung Bioepis and Henlius.

The established brands segment comprises mature medications across therapeutic areas including cardiovascular (Zetia, Vytorin), respiratory (Singulair, Nasonex), dermatology (Diprosone, Elocon), bone health (Fosamax), and non-opioid pain management (Arcoxia, Diprospan). While many of these products have lost patent protection, they continue to generate significant cash flow, particularly in international markets where approximately 76% of the company's total revenue originates.

Organon distributes its products through various channels including drug wholesalers, retailers, hospitals, clinics, and managed healthcare providers across more than 140 countries and territories. The company reinvests cash flows from established brands to fund research and development in women's health, including partnerships to develop new treatments for conditions like endometriosis and polycystic ovarian syndrome.

4. Branded Pharmaceuticals

Looking ahead, the branded pharmaceutical industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Organon's competitors vary by business segment. In women's health, it competes with companies like Bayer, AbbVie, and CooperSurgical. In biosimilars, competitors include Amgen, Pfizer, and Novartis. For established brands, Organon faces competition from generic manufacturers and companies with similar portfolios like Viatris.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $6.22 billion in revenue over the past 12 months, Organon has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Organon struggled to consistently increase demand as its $6.22 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Just like its five-year trend, Organon’s revenue over the last two years was flat, suggesting it is in a slump.

This quarter, Organon reported a rather uninspiring 5.3% year-on-year revenue decline to $1.51 billion of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 3.5% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will face some demand challenges.

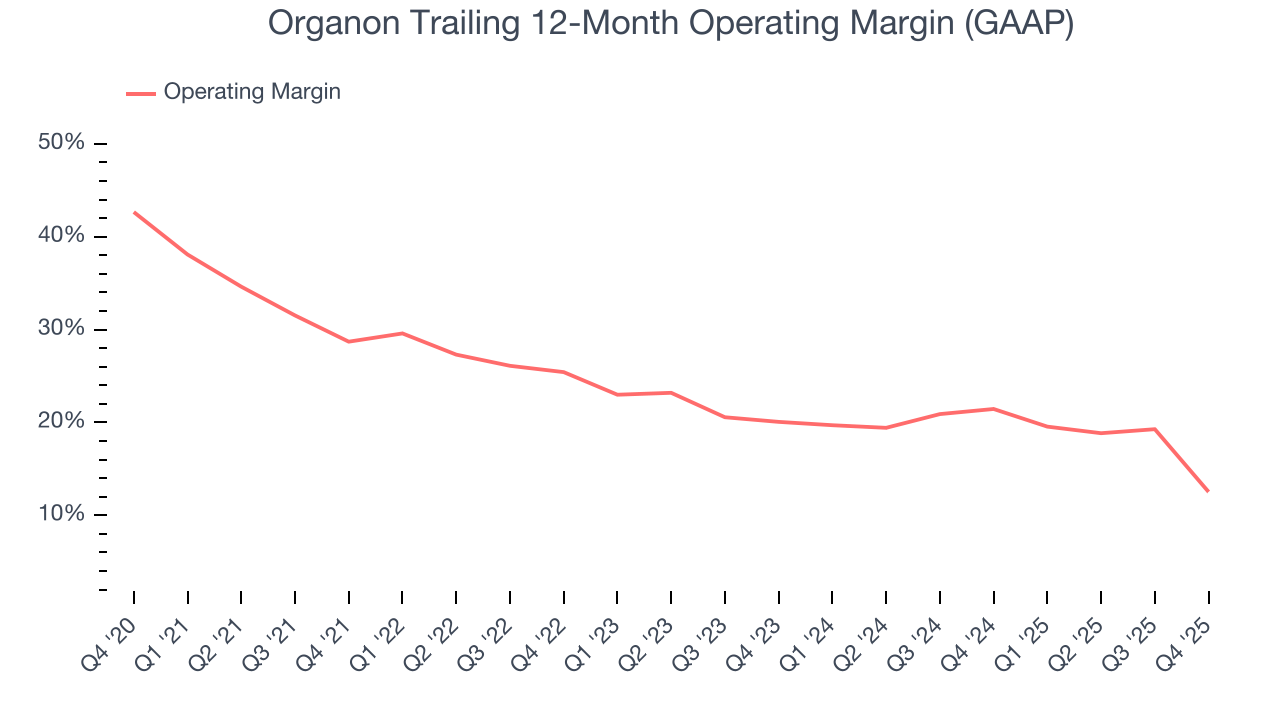

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Organon has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 21.7%.

Looking at the trend in its profitability, Organon’s operating margin decreased by 16.2 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 7.5 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Organon generated an operating margin profit margin of negative 9.8%, down 27.9 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

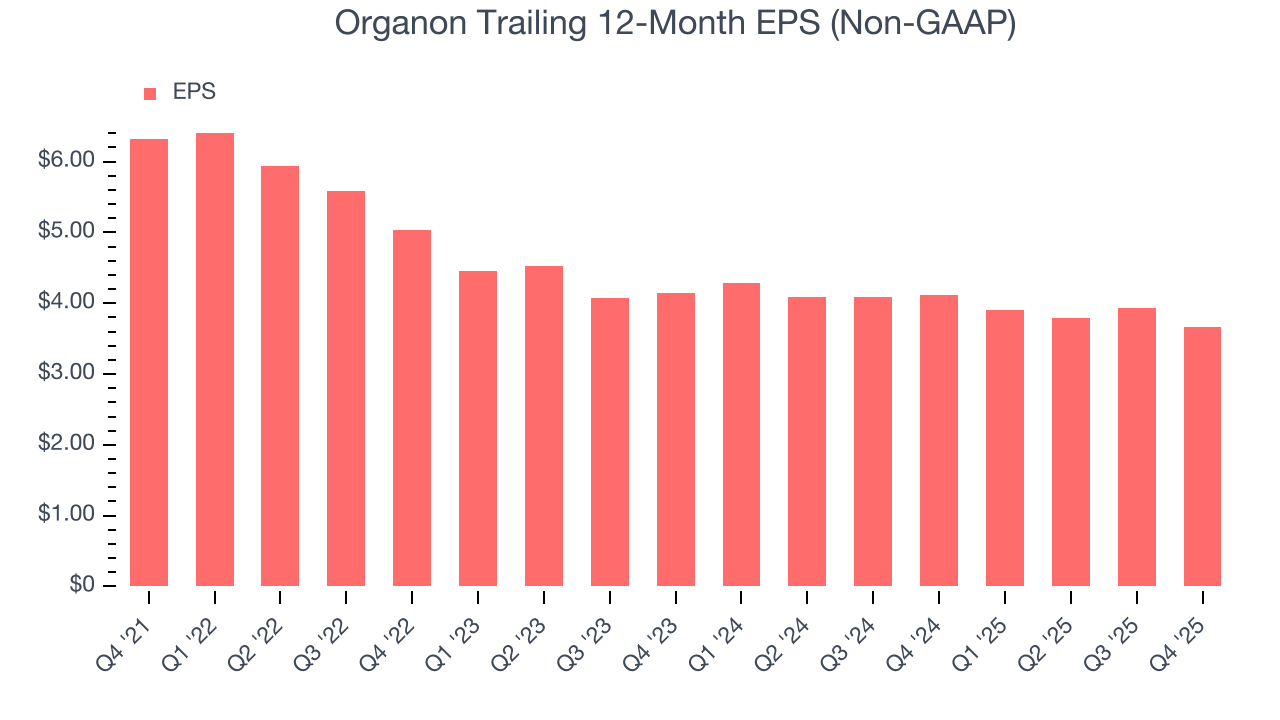

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Organon’s full-year EPS dropped 61.7%, or 12.8% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Organon’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Organon reported adjusted EPS of $0.63, down from $0.90 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Organon’s full-year EPS of $3.66 to grow 3%.

9. Cash Is King

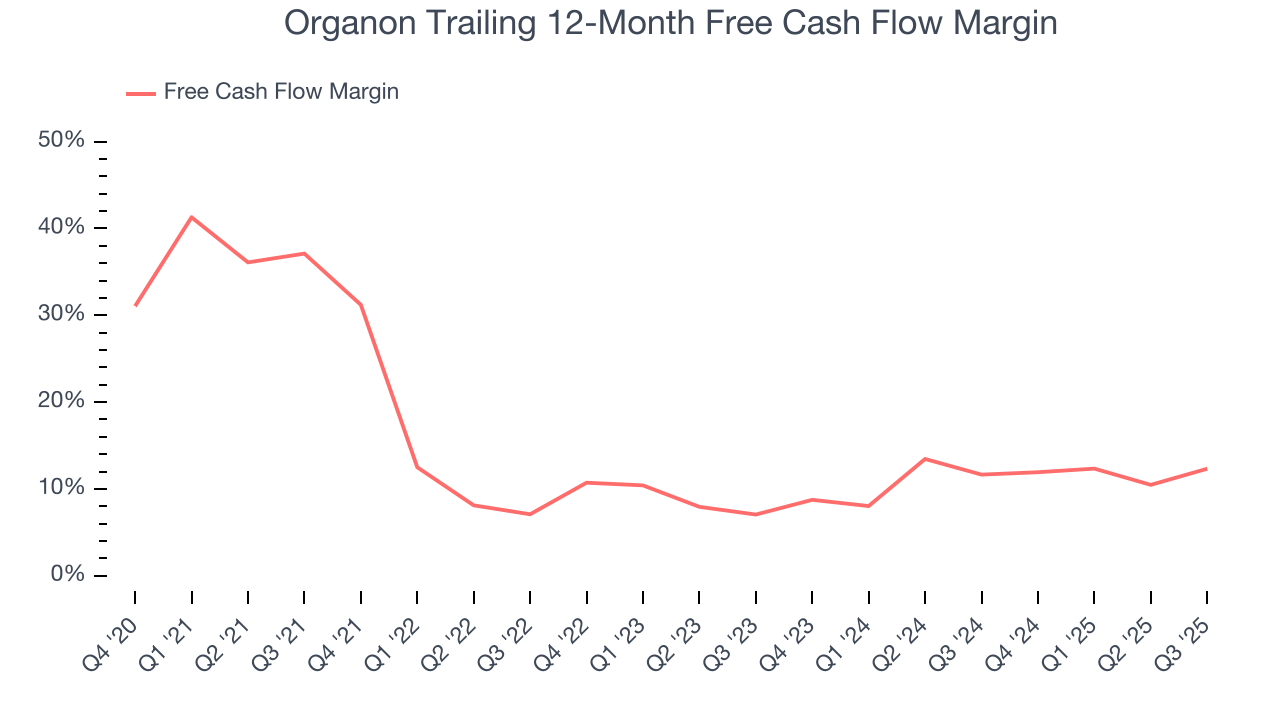

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Organon has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 14.7% over the last five years, better than the broader healthcare sector.

Taking a step back, we can see that Organon’s margin dropped by 32.7 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Organon hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it historically found a few growth initiatives that worked out well. Its five-year average ROIC was 17.1%, impressive for a healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Organon’s ROIC has unfortunately decreased. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

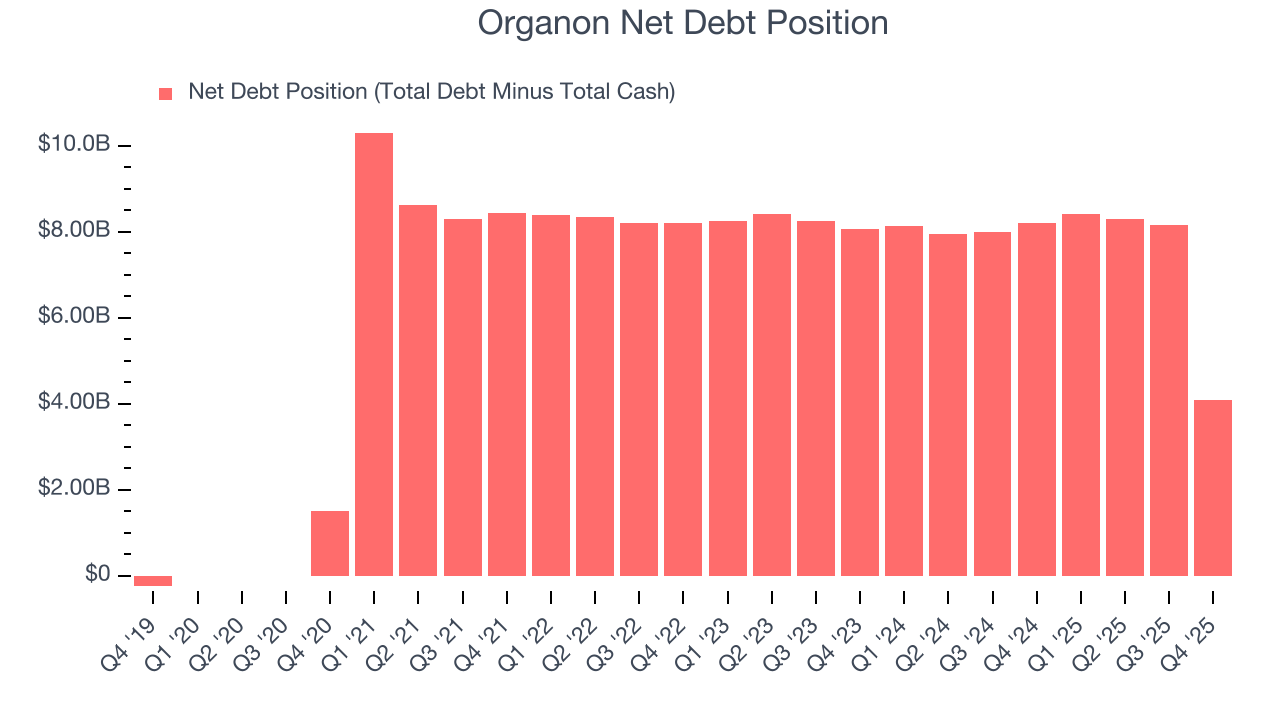

Organon reported $1.96 billion of cash and $6.04 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.91 billion of EBITDA over the last 12 months, we view Organon’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $504 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Organon’s Q4 Results

It was good to see Organon provide full-year revenue guidance that slightly beat analysts’ expectations. On the other hand, its EPS missed. Overall, this quarter could have been better. The stock traded down 4.3% to $7.36 immediately after reporting.

13. Is Now The Time To Buy Organon?

Updated: March 16, 2026 at 12:18 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Organon.

Organon isn’t a terrible business, but it doesn’t pass our bar. To begin with, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. While its impressive operating margins show it has a highly efficient business model, the downside is its declining EPS over the last four years makes it a less attractive asset to the public markets. On top of that, its cash profitability fell over the last five years.

Organon’s P/E ratio based on the next 12 months is 1.8x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $9 on the company (compared to the current share price of $6.37).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.