Academy Sports (ASO)

We’re wary of Academy Sports. Its plummeting sales and returns on capital show its profits are shrinking as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Academy Sports Will Underperform

Founded in 1938 as a tire shop before expanding into fishing equipment, Academy Sports & Outdoor (NASDAQ:ASO) sells a broad selection of sporting goods but is still known for its outdoor activity merchandise.

- Products aren't resonating with the market as its revenue declined by 2.4% annually over the last three years

- Gross margin of 34.3% is below its competitors, leaving less money for marketing and promotions

- Ambitious expansion strategy seems risky considering the weak same-store sales performance at existing locations

Academy Sports is skating on thin ice. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Academy Sports

Academy Sports’s stock price of $57.03 implies a valuation ratio of 8.8x forward P/E. This certainly seems like a cheap stock, but we think there are valid reasons why it trades this way.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Academy Sports (ASO) Research Report: Q4 CY2025 Update

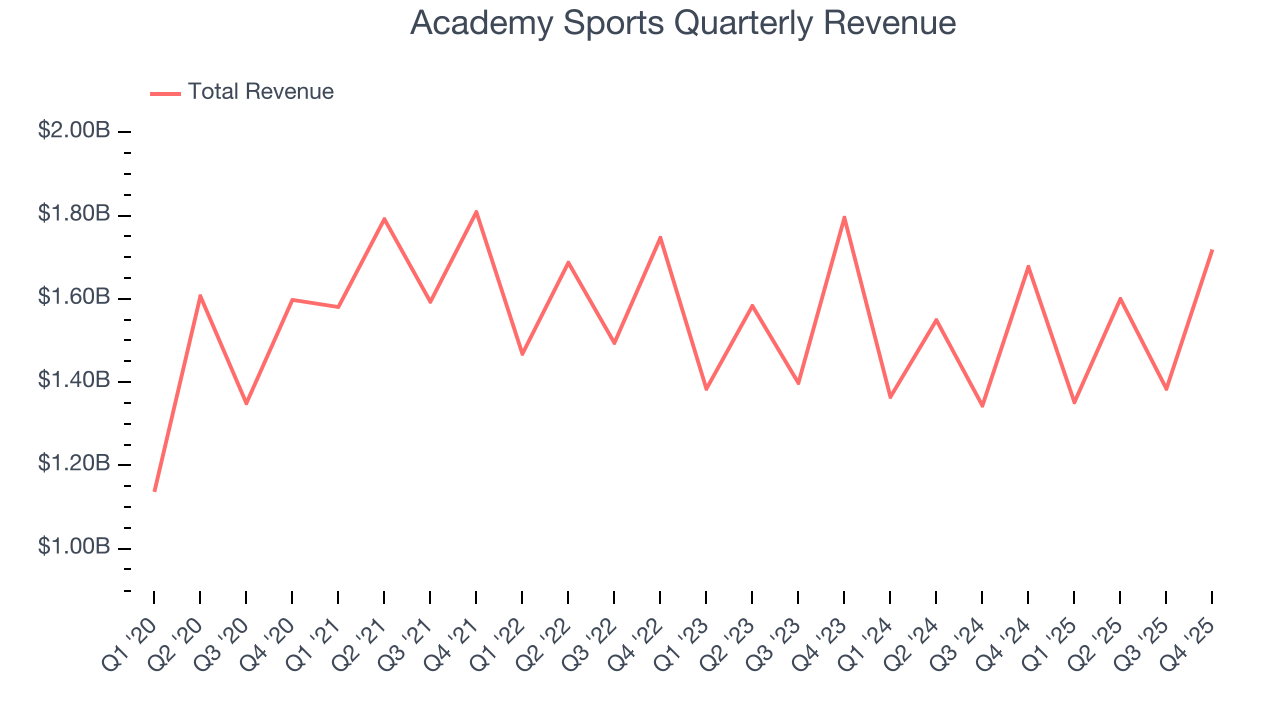

Sporting goods retailer Academy Sports & Outdoor (NASDAQ:ASO) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 2.5% year on year to $1.72 billion. The company’s full-year revenue guidance of $6.27 billion at the midpoint came in 3% below analysts’ estimates. Its non-GAAP profit of $1.97 per share was 4% below analysts’ consensus estimates.

Academy Sports (ASO) Q4 CY2025 Highlights:

- Revenue: $1.72 billion vs analyst estimates of $1.76 billion (2.5% year-on-year growth, 2.2% miss)

- Adjusted EPS: $1.97 vs analyst expectations of $2.05 (4% miss)

- Adjusted EBITDA: $202.6 million vs analyst estimates of $218.7 million (11.8% margin, 7.4% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $6.35 at the midpoint, missing analyst estimates by 2.6%

- Operating Margin: 9.9%, in line with the same quarter last year

- Free Cash Flow Margin: 8.4%, up from 4.6% in the same quarter last year

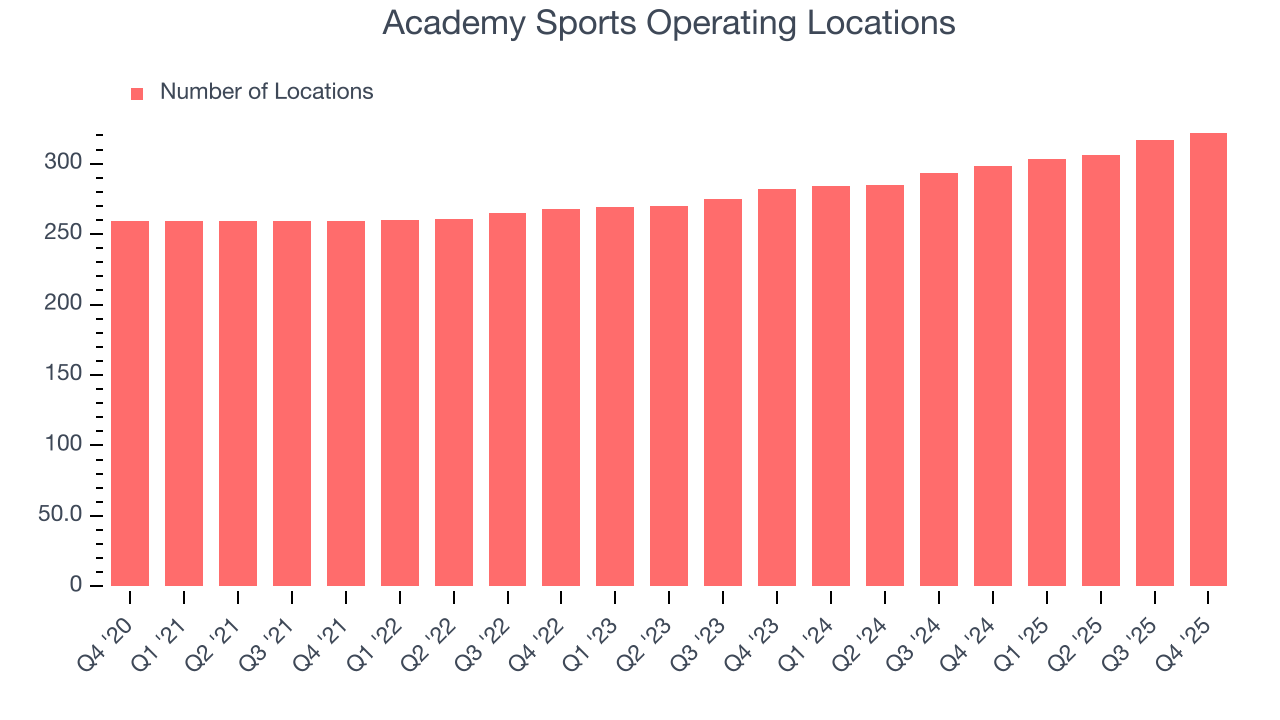

- Locations: 322 at quarter end, up from 298 in the same quarter last year

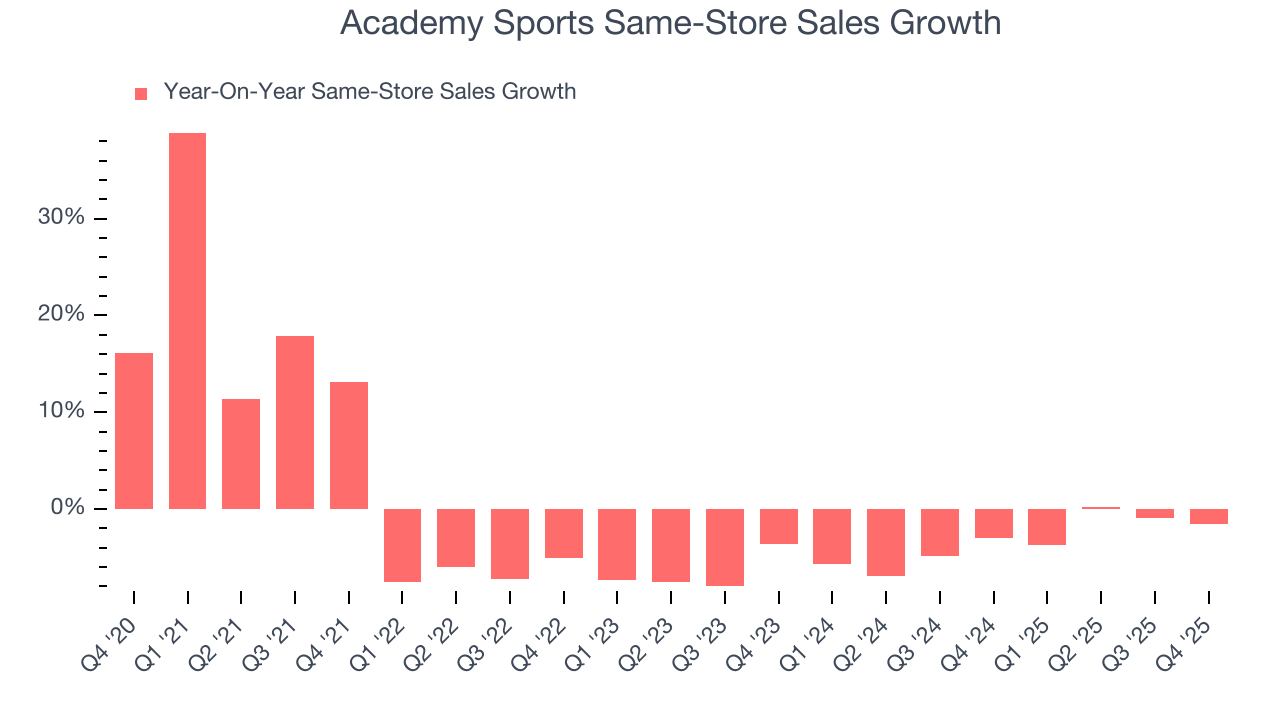

- Same-Store Sales fell 1.6% year on year (-3% in the same quarter last year)

- Market Capitalization: $3.77 billion

Company Overview

Founded in 1938 as a tire shop before expanding into fishing equipment, Academy Sports & Outdoor (NASDAQ:ASO) sells a broad selection of sporting goods but is still known for its outdoor activity merchandise.

The core customer is anyone in need of products for fishing, hunting, camping, or hiking. Despite its heritage in outdoor merchandise, Academy Sports also sells equipment for traditional sports such as baseball, soccer, or football as well as sneakers, apparel, and accessories. It is very much a one-stop shop for sports. The breadth of sporting goods and the depth of product in each category is what differentiates Academy Sports. Sporting goods can be large and cumbersome, so general merchandise retailers who devote limited space have limited selection.

Academy Sports has a strong presence in the Southern and Midwestern US, areas with strong outdoor activity affinity and traditions. Stores are 70,000 square feet on average and located in suburban or rural shopping centers alongside other retailers. The store is divided into sections based on sports with additional sections for footwear and apparel. Academy Sports also has an e-commerce presence, which the company launched in 2011 as a somewhat late adopter of online shopping. Many customers choose to order online and pick up at their nearest store since shipping is not available or overly costly for large items such as camping tents, canoes, and outdoor grills.

4. Sports & Outdoor Equipment Retailer

Some of us spend our leisure time vegging out, but many others take to the courts, fields, beaches, and campsites; sports equipment retailers cater to the avid sportsman as well as the weekend warrior. Shoppers can find everything from tents to lawn games to baseball bats to satisfy their athletic and leisure needs along with competitive prices and helpful store associates that can talk through brands, sizing, and product quality. This is a category that has moved rapidly online over the last few decades, so these sports and outdoor equipment retailers have needed to be nimble and aggressive with their e-commerce and omnichannel presences.

Retailers offering sporting and outdoor goods include Dick’s Sporting Goods (NYSE:DKS), Sportsman’s Warehouse (NASDAQ:SPWH), and Hibbett (NASDAQ:HIBB).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $6.05 billion in revenue over the past 12 months, Academy Sports is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Academy Sports’s revenue declined by 1.8% per year over the last three years despite opening new stores. This implies its underperformance was driven by lower sales at existing, established locations.

This quarter, Academy Sports’s revenue grew by 2.5% year on year to $1.72 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 7.1% over the next 12 months, an acceleration versus the last three years. This projection is healthy and indicates its newer products will catalyze better top-line performance.

6. Store Performance

Number of Stores

Academy Sports sported 322 locations in the latest quarter. Over the last two years, it has opened new stores at a rapid clip by averaging 6.7% annual growth, among the fastest in the consumer retail sector. This gives it a chance to become a large, scaled business over time.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Academy Sports’s demand has been shrinking over the last two years as its same-store sales have averaged 3.3% annual declines. This performance is concerning - it shows Academy Sports artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

In the latest quarter, Academy Sports’s same-store sales fell by 1.6% year on year. This decrease was an improvement from its historical levels. It’s always great to see a business’s demand trends improve.

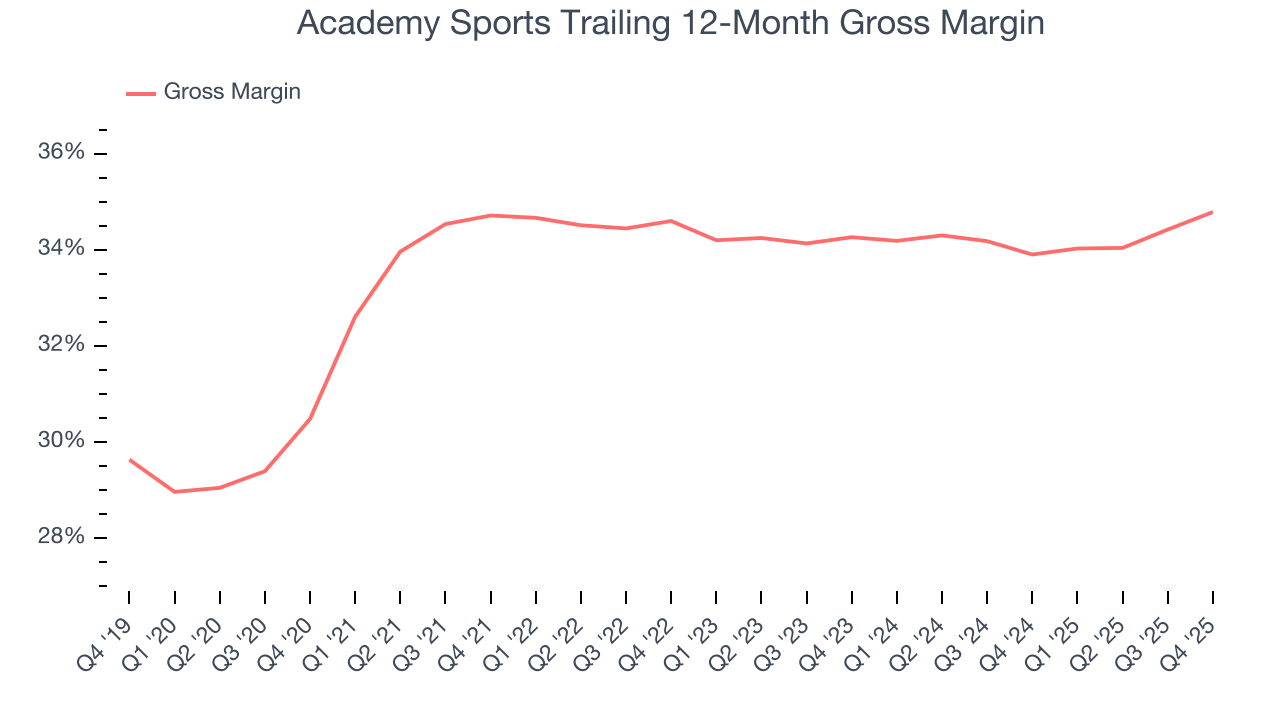

7. Gross Margin & Pricing Power

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Academy Sports has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 34.3% gross margin over the last two years. That means Academy Sports paid its suppliers a lot of money ($65.65 for every $100 in revenue) to run its business.

Academy Sports produced a 33.6% gross profit margin in Q4, up 1.3 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

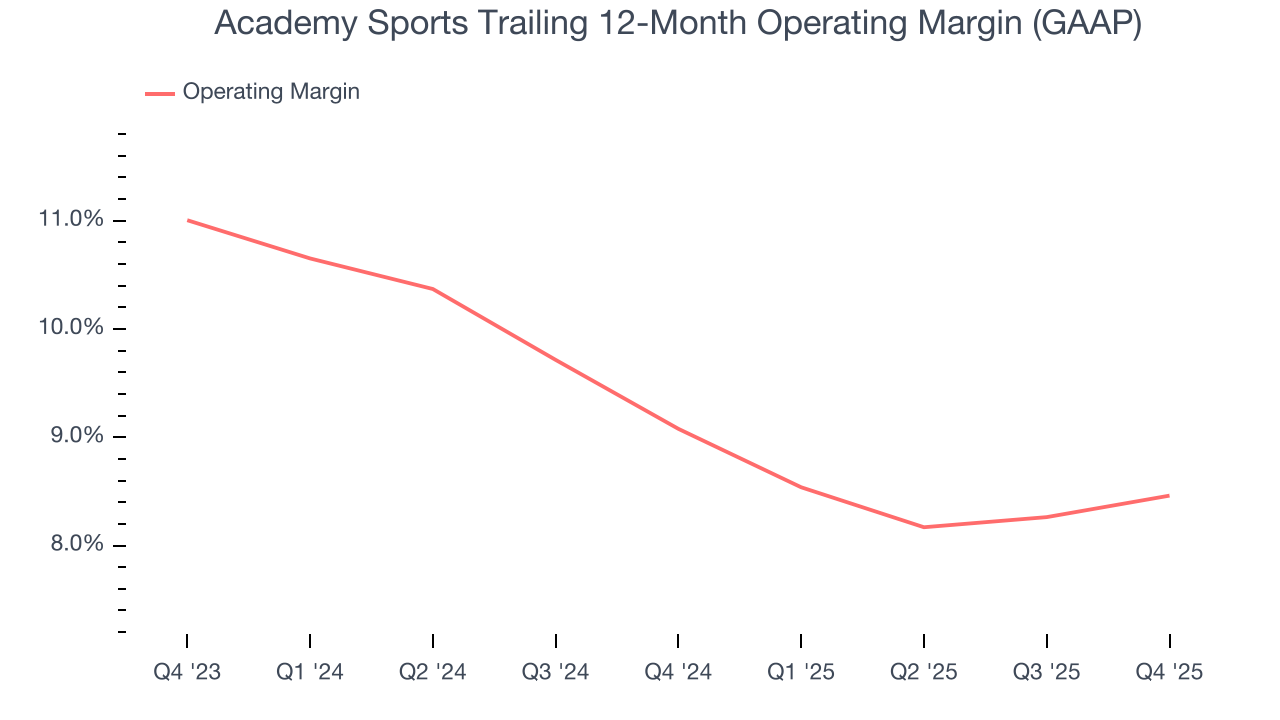

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Academy Sports’s operating margin has more or less stayed the same over the last 12 months , averaging 8.8% over the last two years. This profitability was higher than the broader consumer retail sector, showing it did a decent job managing its expenses.

Looking at the trend in its profitability, Academy Sports’s operating margin might fluctuated slightly but has generally stayed the same over the last year. Shareholders will want to see Academy Sports grow its margin in the future.

In Q4, Academy Sports generated an operating margin profit margin of 9.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

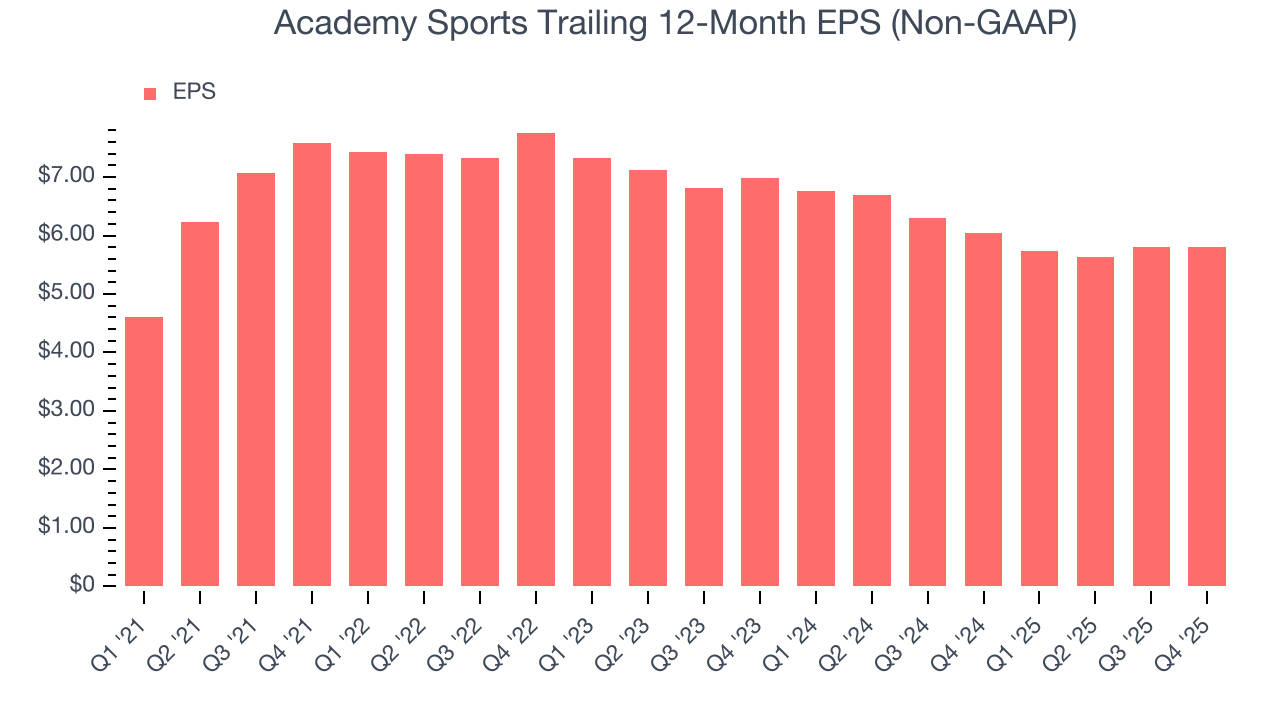

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Academy Sports, its EPS declined by 9.2% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Academy Sports reported adjusted EPS of $1.97, up from $1.96 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Academy Sports’s full-year EPS of $5.81 to grow 12%.

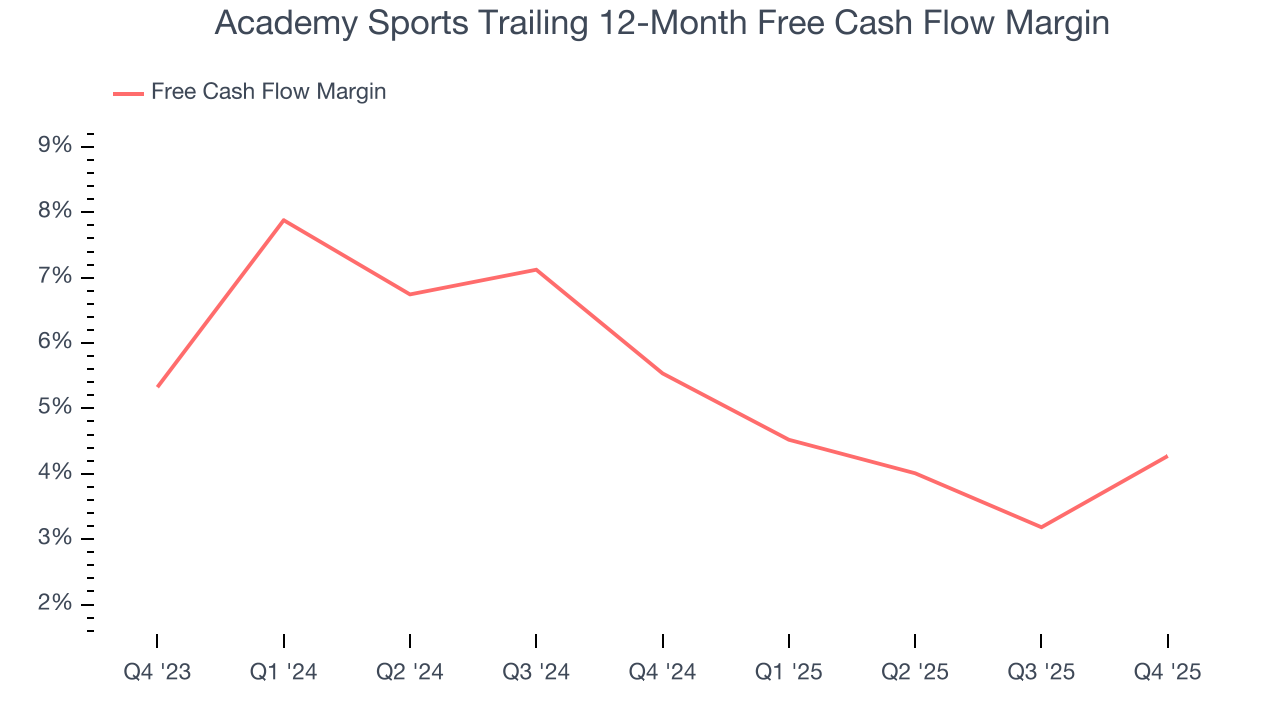

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Academy Sports has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 4.9% over the last two years, better than the broader consumer retail sector.

Taking a step back, we can see that Academy Sports’s margin dropped by 1.3 percentage points over the last year. This decrease came from the higher costs associated with opening more stores.

Academy Sports’s free cash flow clocked in at $143.7 million in Q4, equivalent to a 8.4% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Academy Sports’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 17.3%, slightly better than typical consumer retail business.

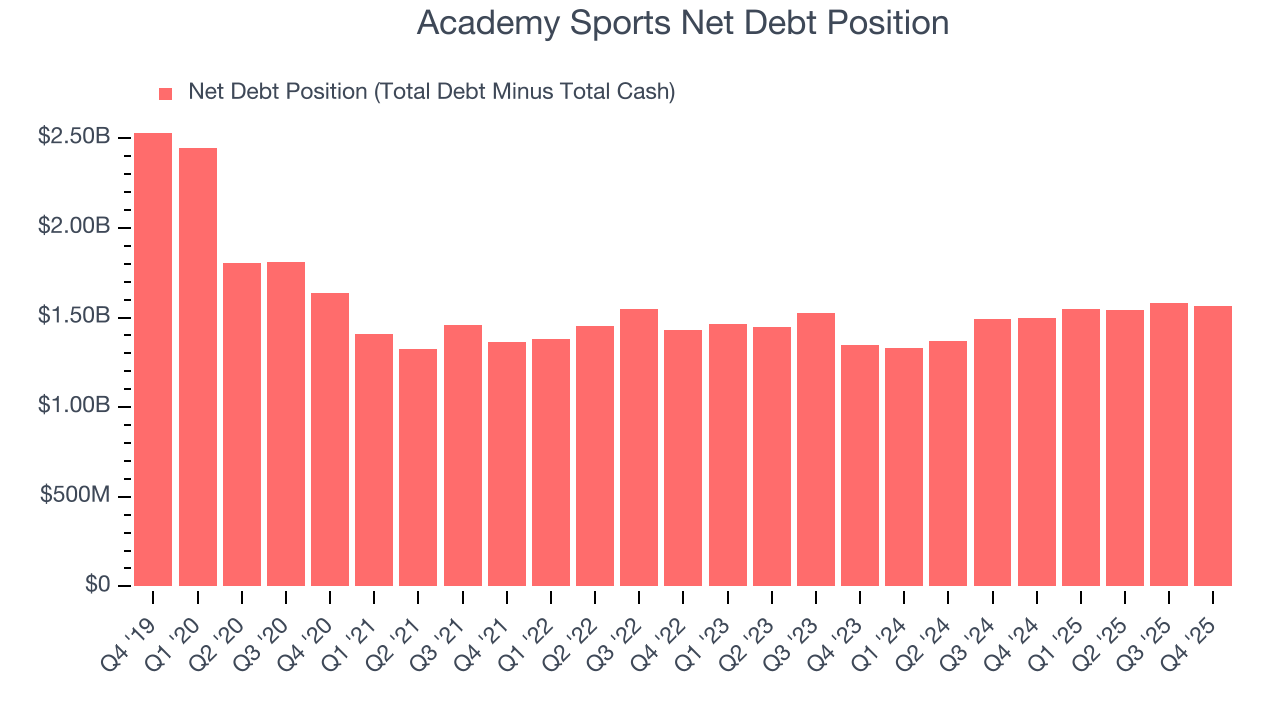

12. Balance Sheet Assessment

Academy Sports reported $330.3 million of cash and $1.89 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $666.3 million of EBITDA over the last 12 months, we view Academy Sports’s 2.3× net-debt-to-EBITDA ratio as safe. We also see its $17.9 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Academy Sports’s Q4 Results

We enjoyed seeing Academy Sports beat analysts’ gross margin expectations this quarter. On the other hand, its EBITDA missed and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 4.9% to $53.72 immediately following the results.

14. Is Now The Time To Buy Academy Sports?

Updated: March 17, 2026 at 8:16 AM EDT

Before deciding whether to buy Academy Sports or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Academy Sports isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue has declined over the last three years. While its new store openings have increased its brand equity, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its gross margins make it more challenging to reach positive operating profits compared to other consumer retail businesses.

Academy Sports’s P/E ratio based on the next 12 months is 8.7x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $60.56 on the company (compared to the current share price of $53.72).