Cintas (CTAS)

Cintas is a great business. Its fusion of high growth and profitability makes it an unstoppable force with big upside.― StockStory Analyst Team

1. News

2. Summary

Why We Like Cintas

Starting as a family business collecting and cleaning shop rags in Cincinnati, Cintas (NASDAQ:CTAS) provides corporate identity uniforms, facility services, and safety products to over one million businesses across North America.

- Earnings growth has massively outpaced its peers over the last five years as its EPS has compounded at 16.4% annually

- Disciplined cost controls and effective management have materialized in a strong adjusted operating margin

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends

Cintas is a market leader. This is one of the best business services stocks in the world.

Is Now The Time To Buy Cintas?

Cintas is trading at $176.46 per share, or 33.6x forward P/E. The pricey valuation means expectations are high for this company over the near to medium term.

Are you a fan of the business model? If so, you can own a smaller position, as high-quality companies tend to outperform the market over a long-term period regardless of entry price.

3. Cintas (CTAS) Research Report: Q1 CY2026 Update

Uniform and facility services provider Cintas (NASDAQ:CTAS) reported Q1 CY2026 results topping the market’s revenue expectations, with sales up 8.9% year on year to $2.84 billion. The company expects the full year’s revenue to be around $11.23 billion, close to analysts’ estimates. Its GAAP profit of $1.24 per share was in line with analysts’ consensus estimates.

Cintas (CTAS) Q1 CY2026 Highlights:

- "On March 10, 2026, Cintas entered into an agreement to acquire UniFirst Corporation. We are excited about the substantial value we expect to create for shareholders and customers through the UniFirst transaction and we look forward to welcoming UniFirst Team Partners to Cintas once we complete the transaction"

- Revenue: $2.84 billion vs analyst estimates of $2.82 billion (8.9% year-on-year growth, 0.8% beat)

- EPS (GAAP): $1.24 vs analyst estimates of $1.24 (in line)

- The company slightly lifted its revenue guidance for the full year to $11.23 billion at the midpoint from $11.19 billion

- Operating Margin: 23.2%, in line with the same quarter last year

- Free Cash Flow Margin: 18.7%, down from 20% in the same quarter last year

- Market Capitalization: $71.26 billion

Company Overview

Starting as a family business collecting and cleaning shop rags in Cincinnati, Cintas (NASDAQ:CTAS) provides corporate identity uniforms, facility services, and safety products to over one million businesses across North America.

Cintas operates through two main business segments: Uniform Rental and Facility Services, and First Aid and Safety Services. The company's core uniform business involves not just providing standardized workwear but creating complete corporate identity programs through the rental, cleaning, and maintenance of professional attire. This service allows businesses to maintain consistent professional appearances without managing laundry operations or investing in uniform inventory.

Beyond uniforms, Cintas offers comprehensive facility services including floor mats, mops, shop towels, and restroom cleaning services and supplies. These services help businesses maintain clean, safe environments for both employees and customers. For example, a restaurant chain might rely on Cintas for chef uniforms, kitchen floor mats, and restroom supplies—all delivered and serviced on a regular schedule by the same route driver.

The First Aid and Safety Services segment provides workplace safety products and training. This includes stocking and maintaining first aid cabinets, providing automated external defibrillators (AEDs), and conducting safety training programs. Cintas also offers fire protection services, including the sale and servicing of fire extinguishers and sprinkler systems, helping businesses meet safety regulations.

Cintas generates revenue primarily through service contracts, with route-based delivery drivers visiting customer locations on regular schedules to deliver clean uniforms and supplies while picking up soiled items. This recurring revenue model creates stable, long-term customer relationships.

The company operates a network of processing facilities and local branches throughout North America, with approximately 11,700 local delivery routes serving customers ranging from small service businesses to major corporations with thousands of employees. While primarily focused on the U.S. market, Cintas also serves customers in Canada and Latin America.

4. Industrial & Environmental Services

Growing regulatory pressure on environmental compliance and increasing corporate ESG commitments should buoy the sector for years to come. On the other hand, environmental regulations continue to evolve, and this may require costly upgrades, volatility in commodity waste and recycling markets, and labor shortages in industrial services. As for digitization, a theme that is impacting nearly every industry, the increasing use of data, analytics, and automation will give rise to improved efficiency of operations. Conversely, though, the benefits of digitization also come with challenges of integrating new technologies into legacy systems.

Cintas competes with Aramark (NYSE:ARMK), UniFirst (NYSE:UNF), and G&K Services in the uniform rental space, while facing competition from Grainger (NYSE:GWW) and MSC Industrial (NYSE:MSM) in safety supplies, and Johnson Controls (NYSE:JCI) in fire protection services.

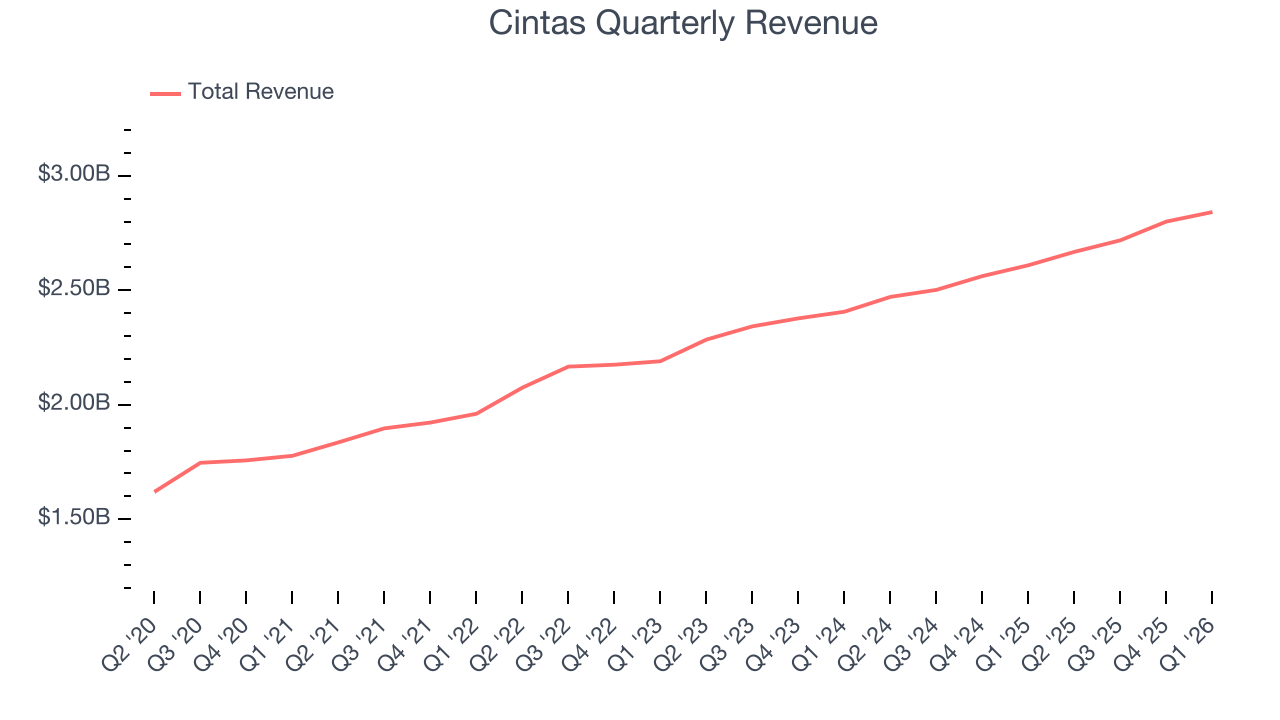

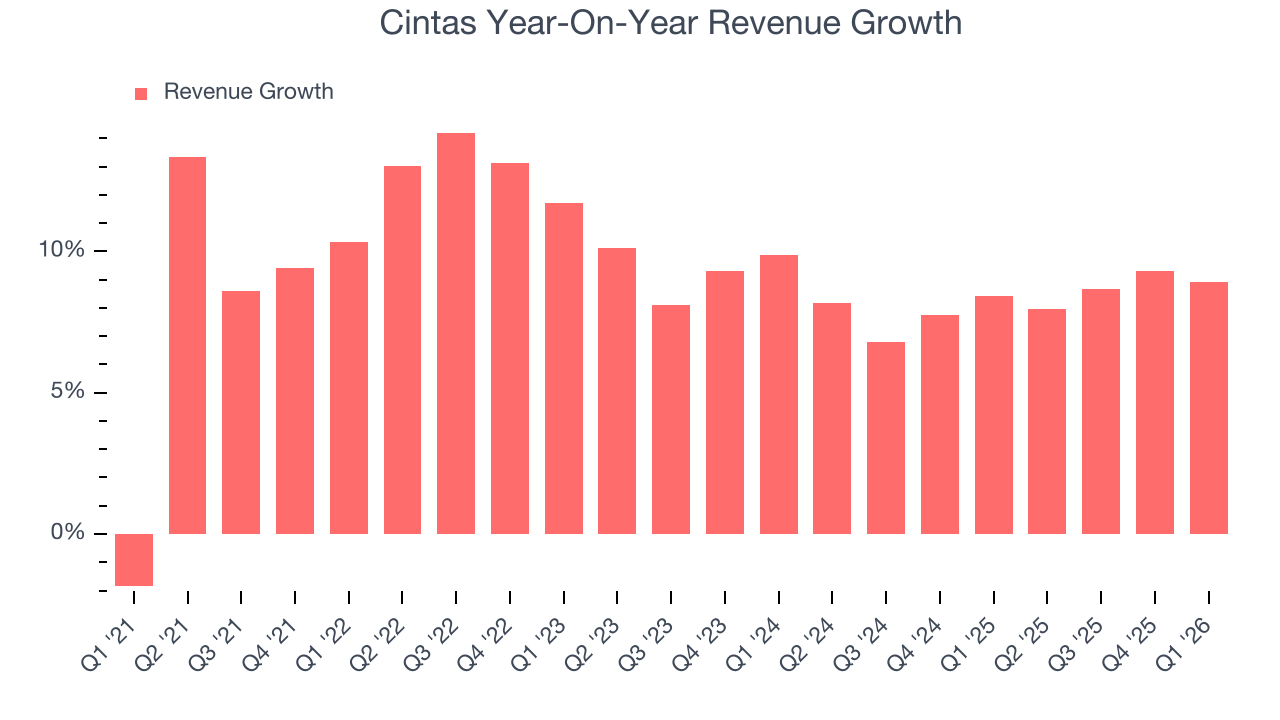

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $11.03 billion in revenue over the past 12 months, Cintas is larger than most business services companies and benefits from economies of scale, enabling it to gain more leverage on its fixed costs than smaller competitors. This also gives it the flexibility to offer lower prices.

As you can see below, Cintas grew its sales at an impressive 9.8% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Cintas’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Cintas’s annualized revenue growth of 8.3% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Cintas reported year-on-year revenue growth of 8.9%, and its $2.84 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 7.2% over the next 12 months, similar to its two-year rate. We still think its growth trajectory is attractive given its scale and indicates the market is forecasting success for its products and services.

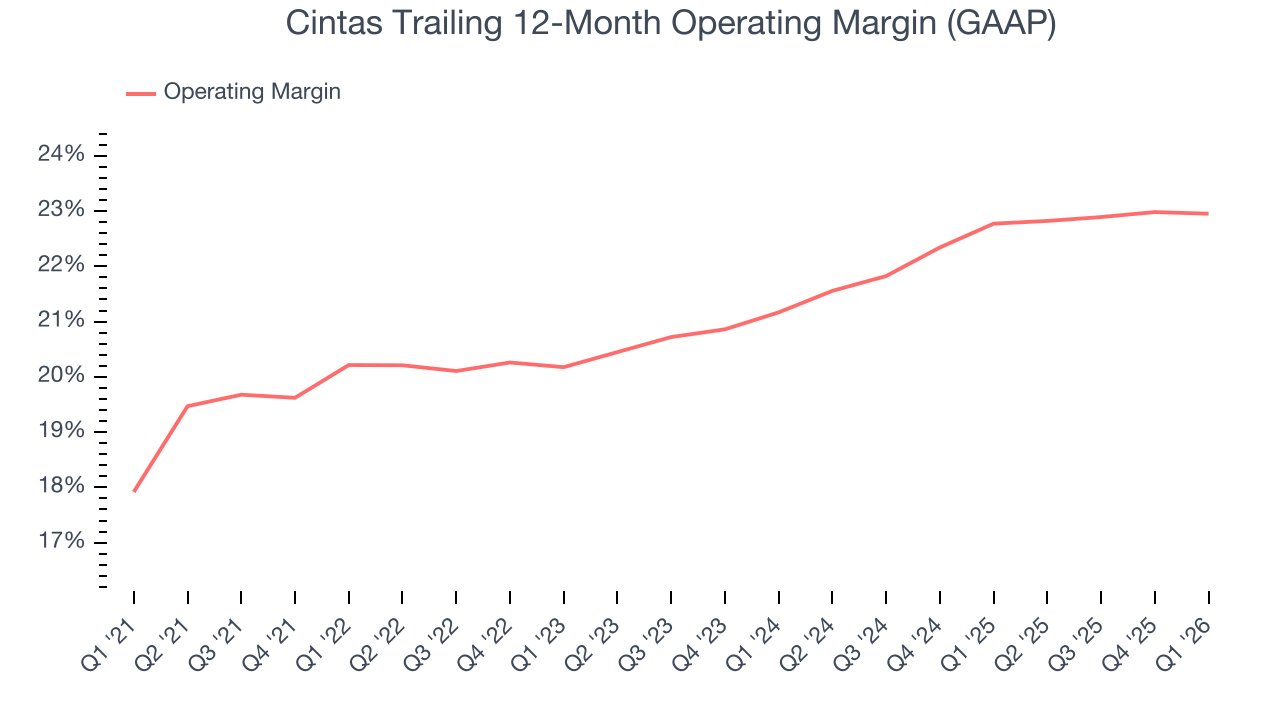

6. Operating Margin

Cintas has been a well-oiled machine over the last five years. It demonstrated elite profitability for a business services business, boasting an average operating margin of 21.6%.

Looking at the trend in its profitability, Cintas’s operating margin rose by 2.7 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q1, Cintas generated an operating margin profit margin of 23.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

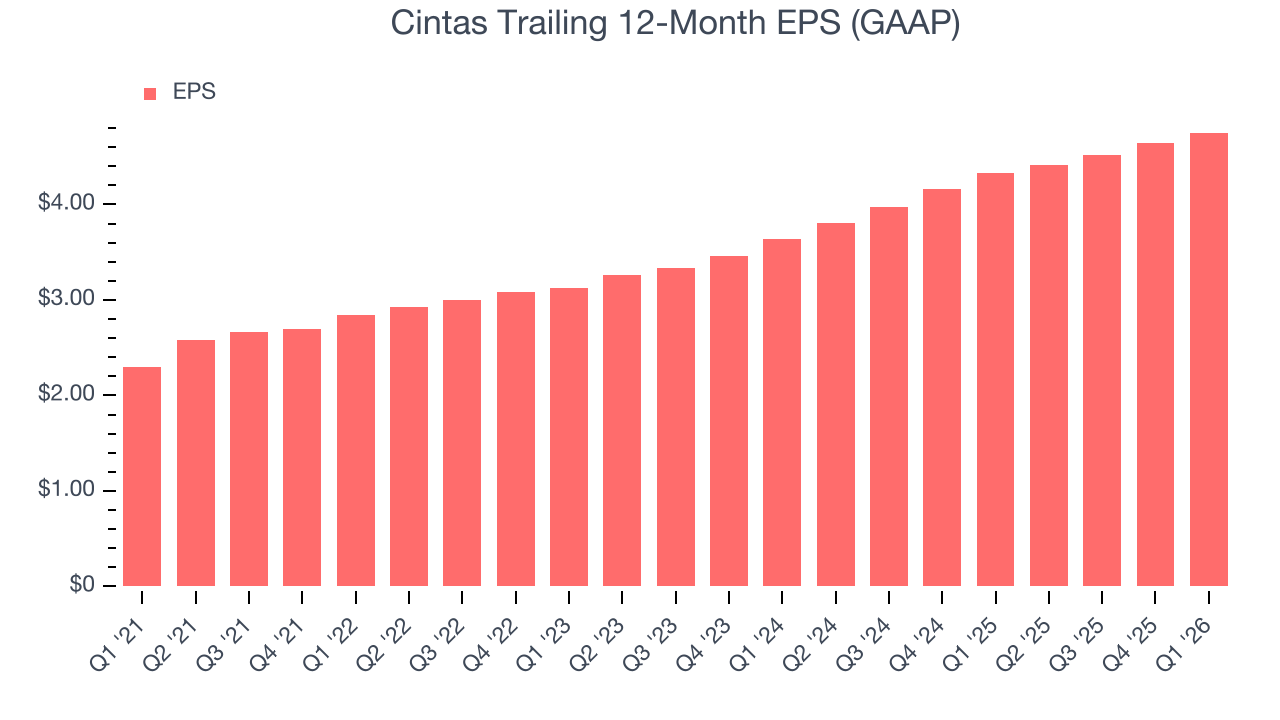

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Cintas’s EPS grew at 15.6% compounded annual growth rate over the last five years, higher than its 9.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

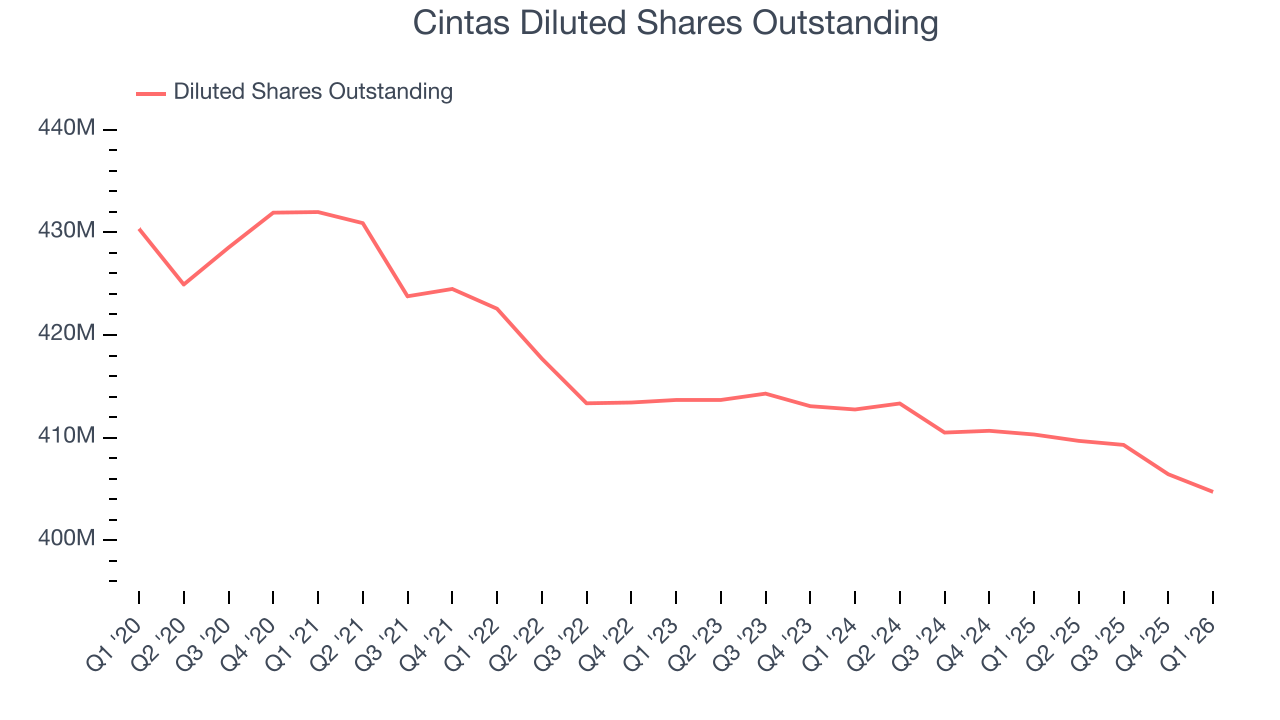

We can take a deeper look into Cintas’s earnings to better understand the drivers of its performance. As we mentioned earlier, Cintas’s operating margin was flat this quarter but expanded by 2.7 percentage points over the last five years. On top of that, its share count shrank by 6.3%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Cintas, its two-year annual EPS growth of 14.3% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Cintas reported EPS of $1.24, up from $1.13 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Cintas’s full-year EPS of $4.75 to grow 10.8%.

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

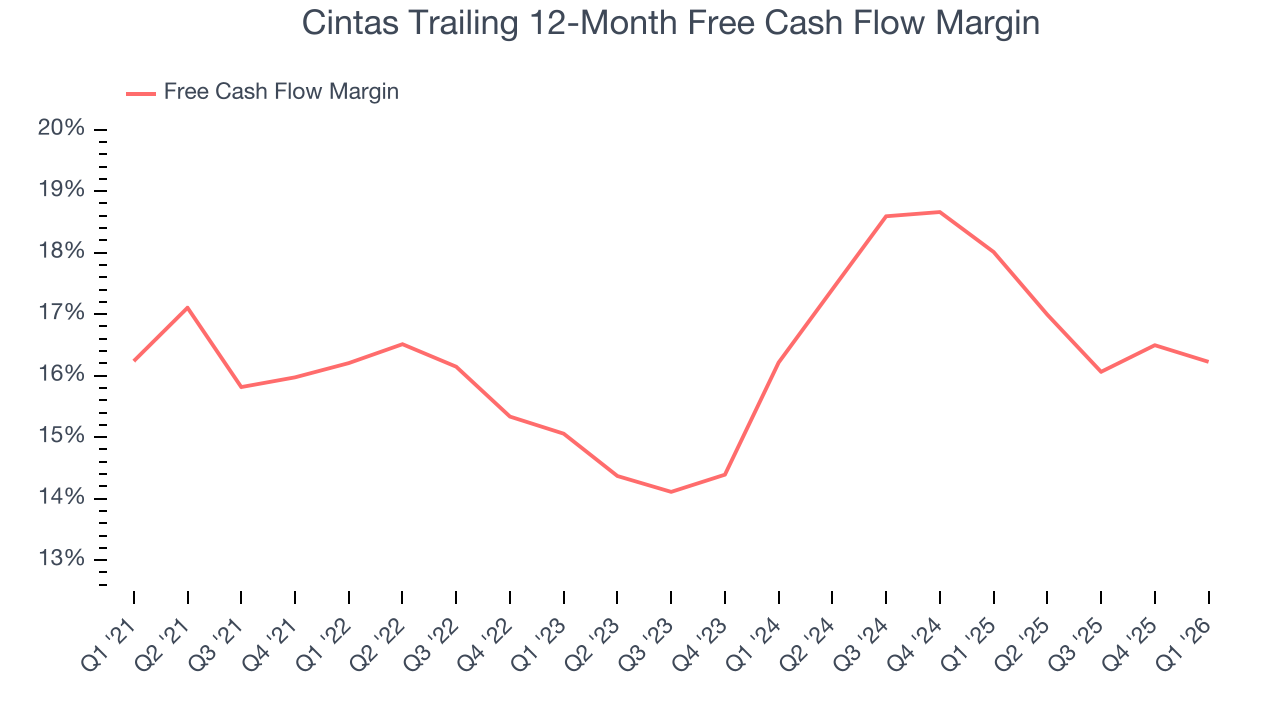

Cintas has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the business services sector, averaging 16.4% over the last five years.

Cintas’s free cash flow clocked in at $530.6 million in Q1, equivalent to a 18.7% margin. The company’s cash profitability regressed as it was 1.3 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t put too much weight on this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

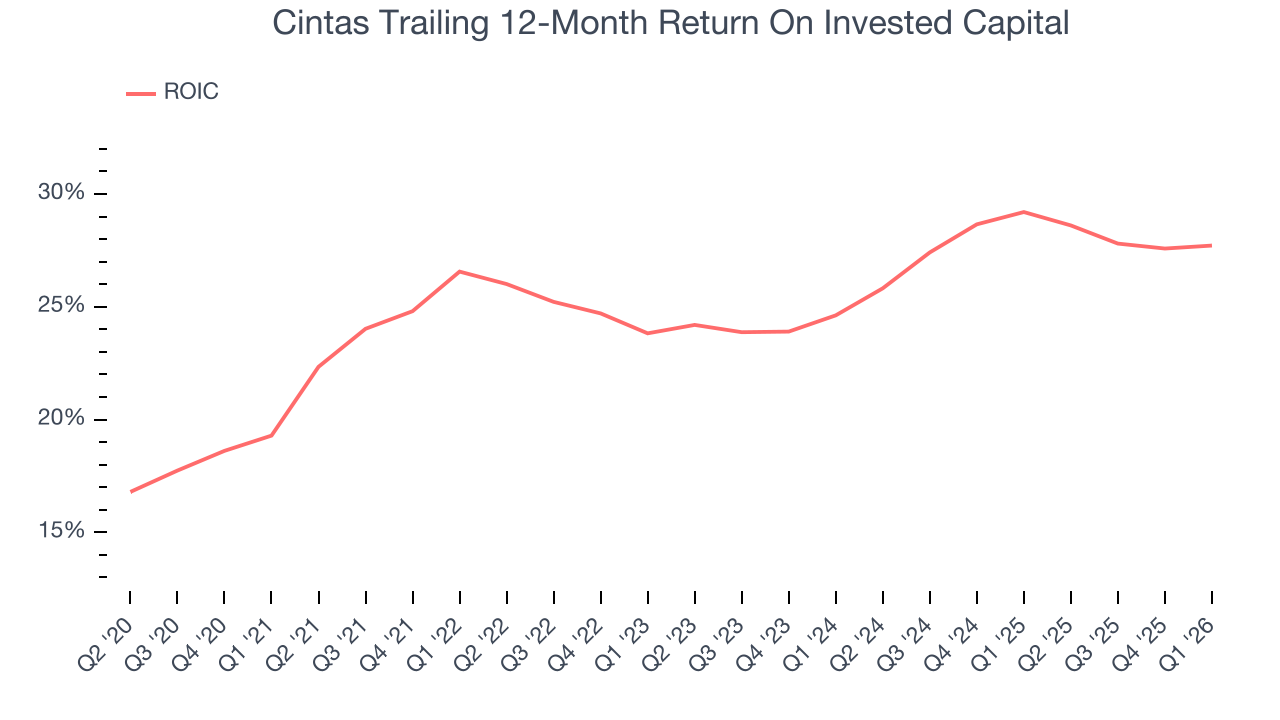

Cintas’s five-year average ROIC was 26.4%, placing it among the best business services companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Cintas’s ROIC increased by 3.3 percentage points annually each year over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Balance Sheet Assessment

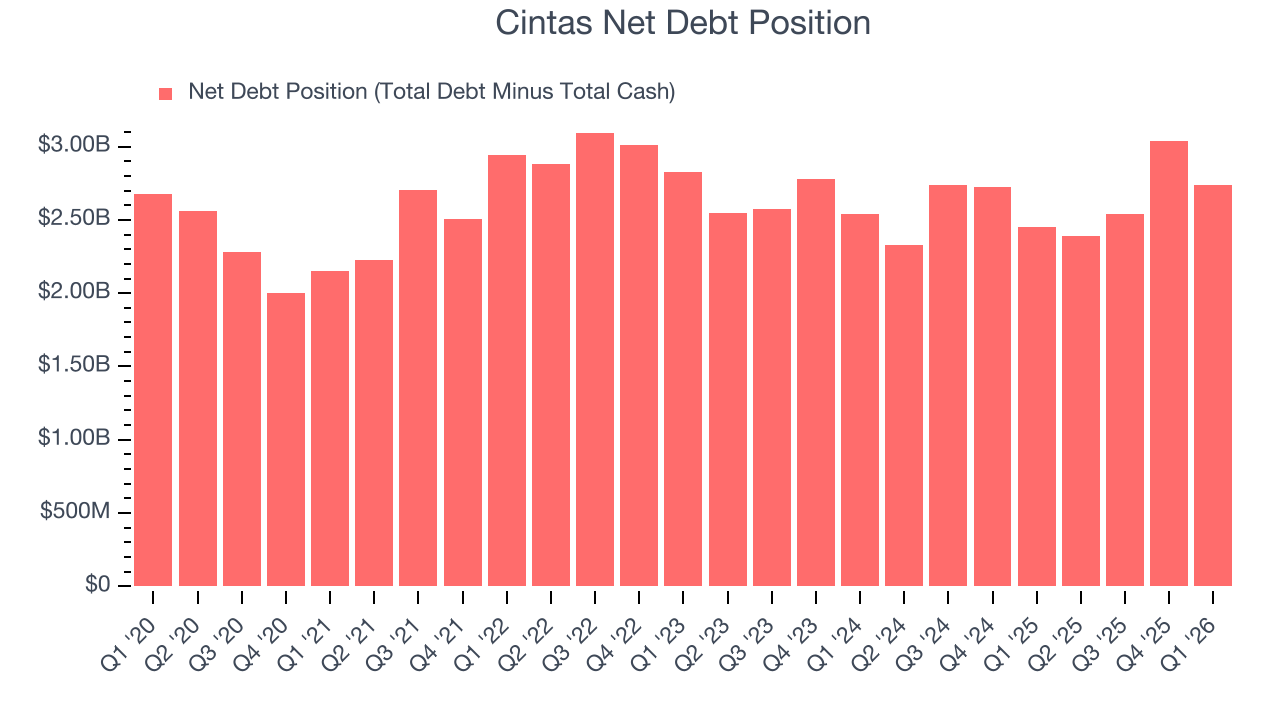

Cintas reported $183.2 million of cash and $2.92 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $3.03 billion of EBITDA over the last 12 months, we view Cintas’s 0.9× net-debt-to-EBITDA ratio as safe. We also see its $98.61 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Cintas’s Q1 Results

It was good to see Cintas narrowly top analysts’ revenue expectations this quarter. This company also lifted its full-year revenue and EPS guidance. The UniFirst acquisition seems to be moving towards closing later in 2026. Zooming out, we think this was a decent quarter. The stock traded up 2.7% to $181.75 immediately following the results.

12. Is Now The Time To Buy Cintas?

Updated: March 26, 2026 at 12:19 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Cintas.

Cintas is a high-quality business worth owning. First of all, the company’s revenue growth was impressive over the last five years. On top of that, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits, and its impressive operating margins show it has a highly efficient business model.

Cintas’s P/E ratio based on the next 12 months is 33.6x. This multiple isn’t necessarily cheap, but we’ll happily own Cintas as its fundamentals shine bright. We’re in the camp that investments like this should be held for at least three to five years to negate the short-term price volatility that can come with relatively high valuations.

Wall Street analysts have a consensus one-year price target of $216.53 on the company (compared to the current share price of $176.46).