Nutanix (NTNX)

Nutanix is a sound business. It’s not only a customer acquisition machine but also sports robust unit economics, a deadly combo.― StockStory Analyst Team

1. News

2. Summary

Why Nutanix Is Interesting

Originally pioneering hyperconverged infrastructure to break down traditional data center silos, Nutanix (NASDAQ:NTNX) provides a unified software platform that enables organizations to run applications and manage data across private, public, and hybrid cloud environments.

- Software is difficult to replicate at scale and leads to a best-in-class gross margin of 87.1%

- Well-designed software integrates seamlessly with other workflows, enabling swift payback periods on marketing expenses and customer growth at scale

- On the other hand, its operating margin improvement of 5 percentage points over the last year demonstrates its ability to scale efficiently

Nutanix has some noteworthy aspects. If you like the story, the valuation seems fair.

Why Is Now The Time To Buy Nutanix?

Nutanix is trading at $39.55 per share, or 3.7x forward price-to-sales. Price is what you pay, and value is what you get. We think the current valuation is quite a good deal considering Nutanix’s business fundamentals.

Now could be a good time to invest if you believe in the story.

3. Nutanix (NTNX) Research Report: Q4 CY2025 Update

Hybrid multicloud computing company Nutanix (NASDAQ:NTNX) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 10.4% year on year to $722.8 million. On the other hand, next quarter’s revenue guidance of $685 million was less impressive, coming in 2% below analysts’ estimates. Its non-GAAP profit of $0.56 per share was 28.1% above analysts’ consensus estimates.

Nutanix (NTNX) Q4 CY2025 Highlights:

- Revenue: $722.8 million vs analyst estimates of $709.9 million (10.4% year-on-year growth, 1.8% beat)

- Adjusted EPS: $0.56 vs analyst estimates of $0.44 (28.1% beat)

- The company dropped its revenue guidance for the full year to $2.82 billion at the midpoint from $2.84 billion, a 0.7% decrease

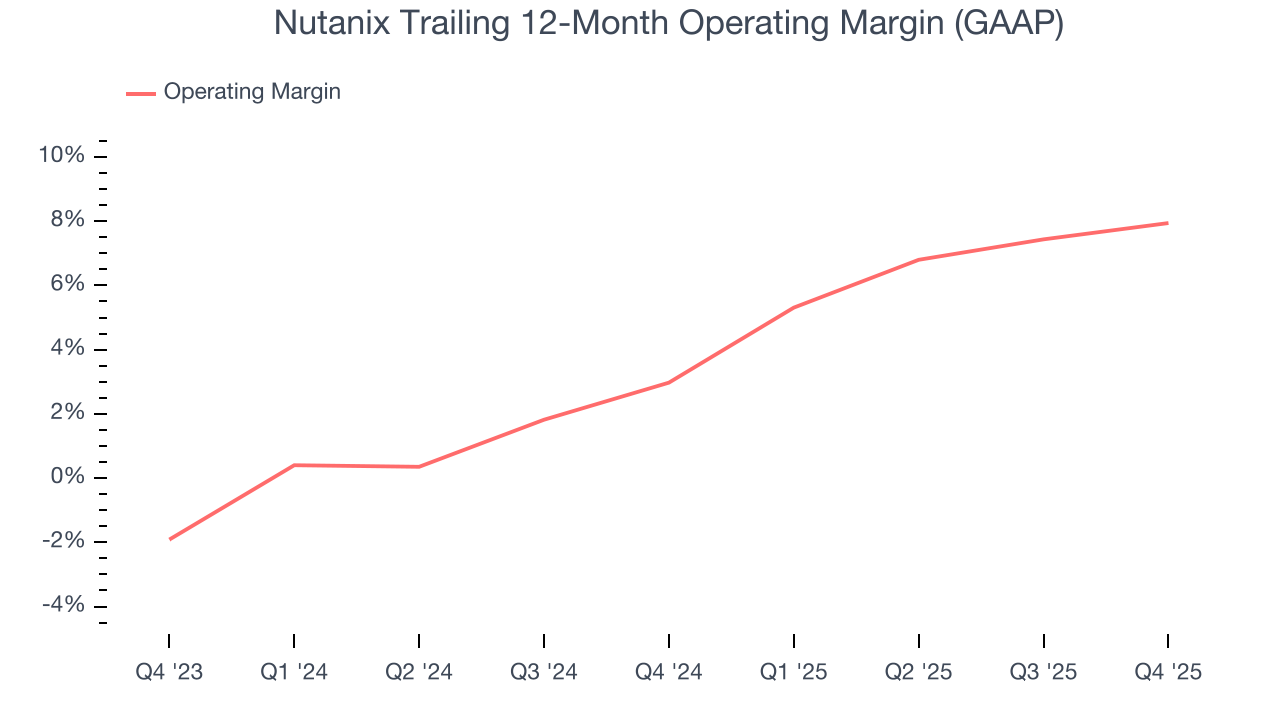

- Operating Margin: 11.6%, up from 10% in the same quarter last year

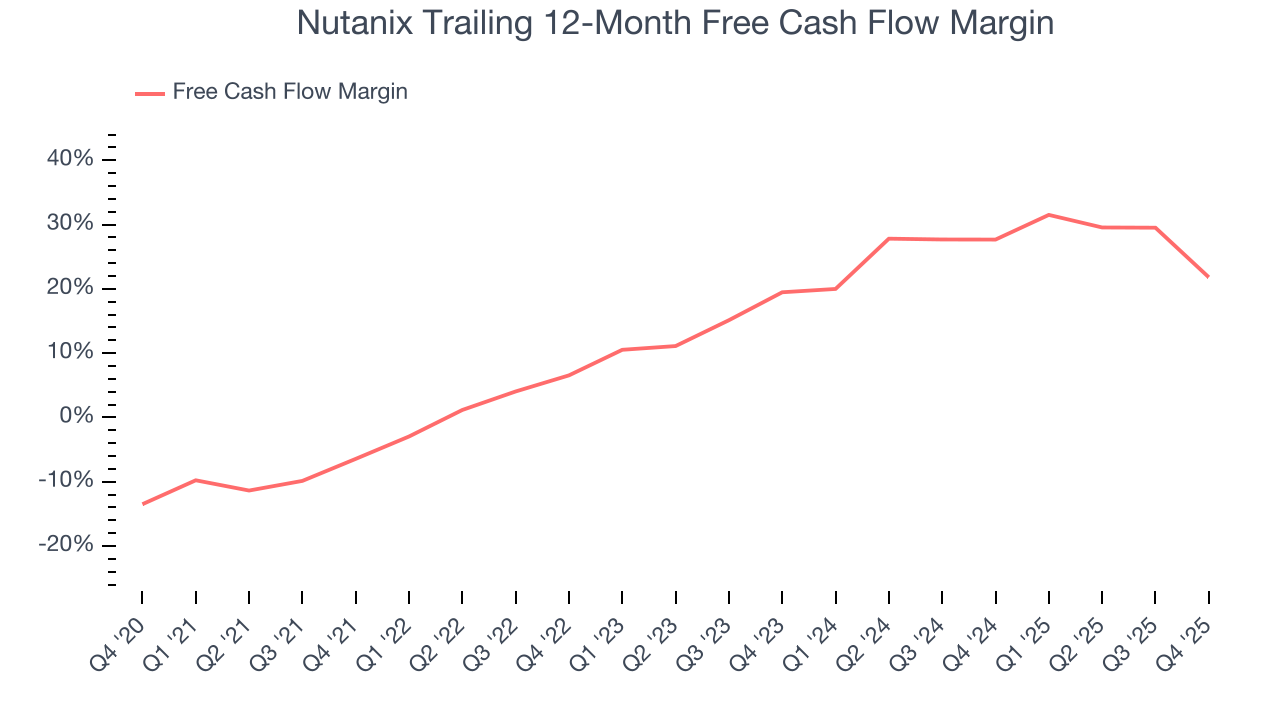

- Free Cash Flow Margin: 0%, down from 26% in the previous quarter

- Annual Recurring Revenue: $2.03 billion vs analyst estimates of $2.34 billion (flat year on year, miss)

- Market Capitalization: $10.24 billion

Company Overview

Originally pioneering hyperconverged infrastructure to break down traditional data center silos, Nutanix (NASDAQ:NTNX) provides a unified software platform that enables organizations to run applications and manage data across private, public, and hybrid cloud environments.

The Nutanix Cloud Platform serves as the foundation for an organization's hybrid multicloud strategy, allowing IT teams to create a consistent operating environment regardless of where workloads are deployed. This flexibility enables customers to run diverse workloads—from business-critical applications to modern containerized services and enterprise AI—on their infrastructure of choice, whether in data centers, edge locations, or public clouds like AWS, Azure, and Google Cloud.

The company's software combines compute, storage, networking, and virtualization capabilities into a single platform, eliminating the complexity of managing separate technology stacks. Nutanix's native hypervisor, AHV, provides virtualization for both traditional and cloud-native applications, while additional services like Nutanix Files, Objects, and Database Service deliver specialized data management capabilities. For enterprise AI initiatives, Nutanix offers GPT-in-a-Box, a full-stack solution designed for secure, on-premises AI deployment.

Revenue comes primarily through subscription-based licensing, typically spanning one to five years. Nutanix relies heavily on a network of channel partners and OEMs including Dell, HPE, Lenovo, and Cisco to reach customers. These partners not only resell Nutanix solutions but also integrate them with their hardware offerings, providing customers with multiple deployment options. This partner ecosystem extends to cloud providers, enabling Nutanix workloads to run seamlessly across public cloud environments.

4. Cloud Monitoring

Software is eating the world, increasing organizations’ reliance on digital-only solutions. As more workloads and applications move to the cloud, the reliability of the underlying cloud infrastructure becomes ever more critical and ever more complex. To solve this challenge, companies and their engineering teams have turned to a range of cloud monitoring tools that provide them with the visibility to troubleshoot issues in real-time.

Nutanix competes with virtualization and cloud infrastructure providers like VMware (owned by Broadcom), Microsoft, and Red Hat, public cloud platforms including AWS, Google Cloud, and Microsoft Azure, and traditional IT vendors such as Dell, HPE, NetApp, and Pure Storage that offer integrated systems and standalone storage products.

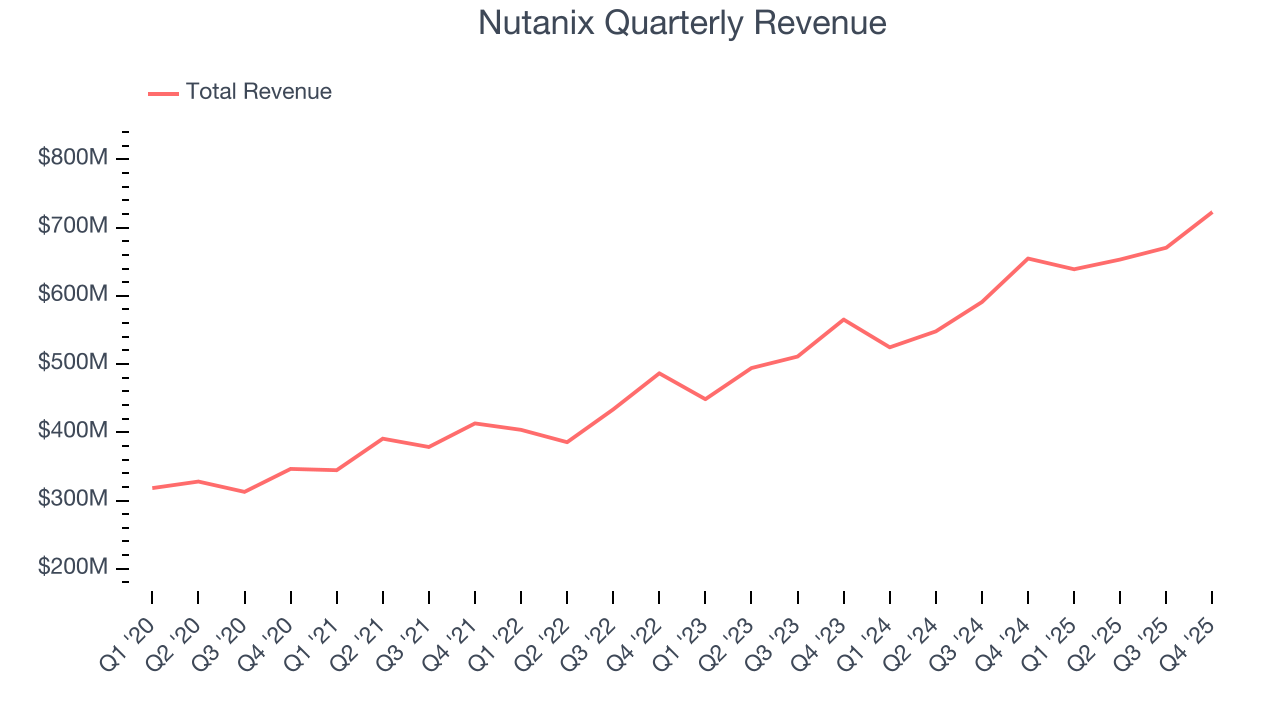

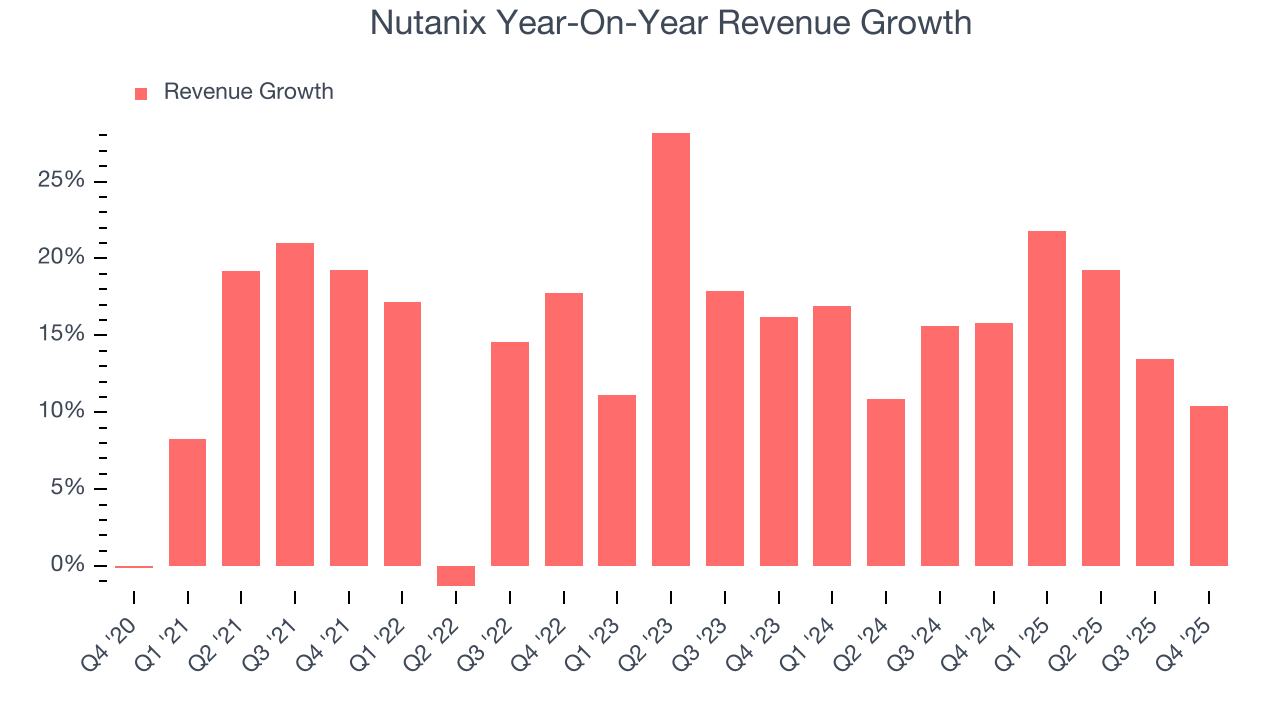

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Nutanix grew its sales at a 15.5% compounded annual growth rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the software sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded. Luckily, there are other things to like about Nutanix.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. Nutanix’s annualized revenue growth of 15.3% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Nutanix reported year-on-year revenue growth of 10.4%, and its $722.8 million of revenue exceeded Wall Street’s estimates by 1.8%. Company management is currently guiding for a 7.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 13.4% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and implies its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

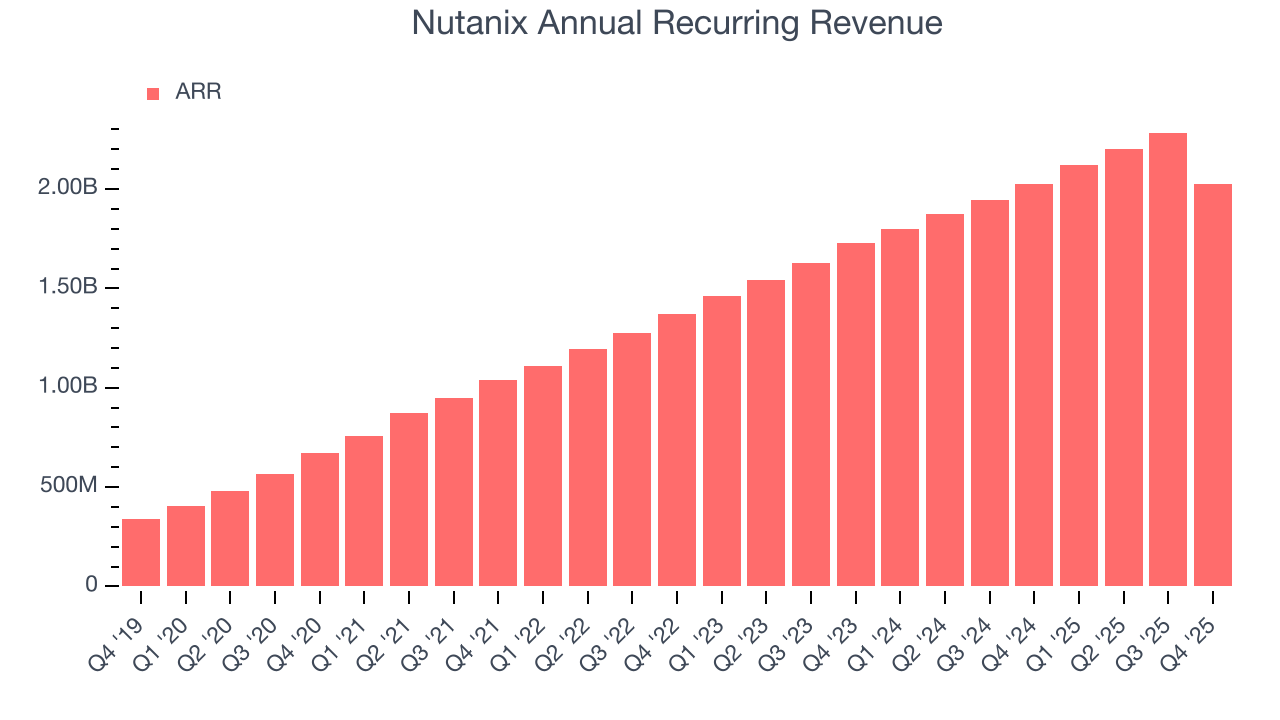

6. Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Nutanix’s ARR came in at $2.03 billion in Q4, and over the last four quarters, its growth slightly lagged the sector as it averaged 13.2% year-on-year increases. This alternate topline metric grew slower than total sales, which likely means that the recurring portions of the business are growing slower than less predictable, choppier ones such as implementation fees. If this continues, the quality of its revenue base could decline.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

Nutanix is extremely efficient at acquiring new customers, and its CAC payback period checked in at 20.1 months this quarter. The company’s rapid recovery of its customer acquisition costs means it can attempt to spur growth by increasing its sales and marketing investments.

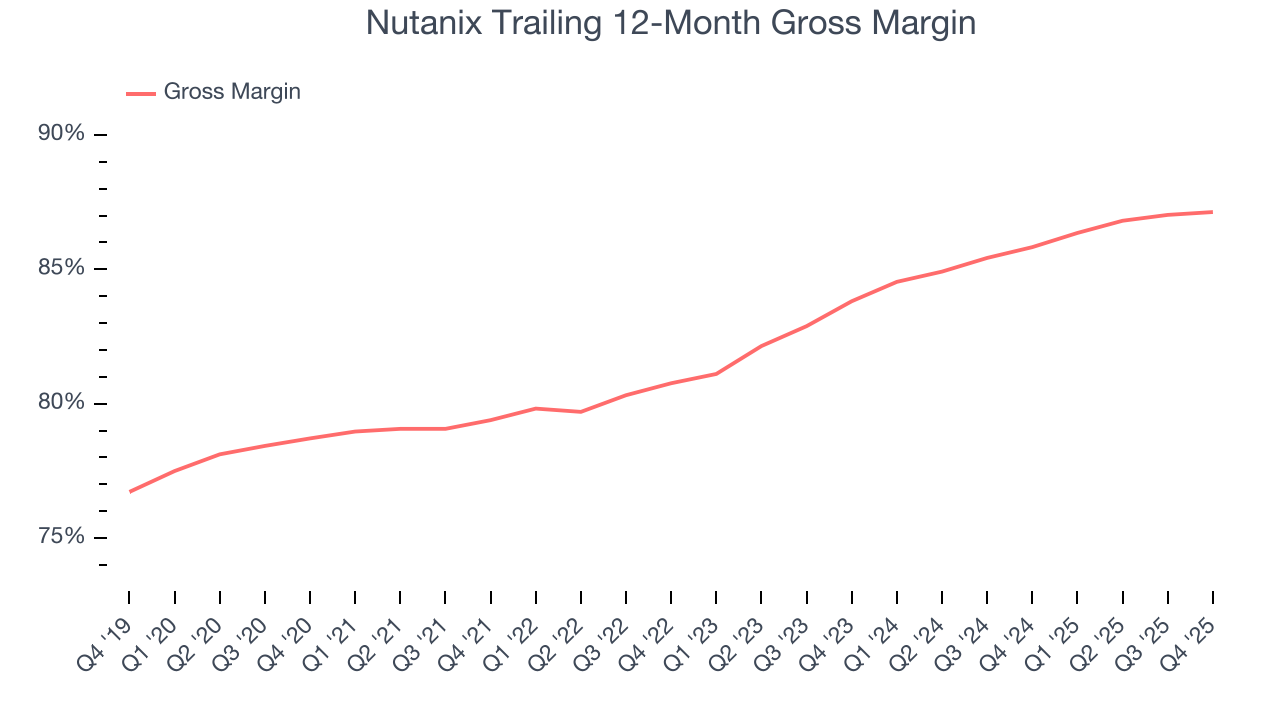

8. Gross Margin & Pricing Power

Software is eating the world. It’s one of our favorite business models because once you develop the product, it usually doesn’t cost much to provide it as an ongoing service. These minimal costs can include servers, licenses, and certain personnel.

Nutanix’s gross margin is one of the highest in the software sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in new products and sales during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 87.1% gross margin over the last year. That means Nutanix only paid its providers $12.87 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. Nutanix has seen gross margins improve by 3.3 percentage points over the last 2 year, which is very good in the software space.

In Q4, Nutanix produced a 87.4% gross profit margin, in line with the same quarter last year. On a wider time horizon, Nutanix’s full-year margin has been trending up over the past 12 months, increasing by 1.3 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as servers).

9. Operating Margin

Many software businesses adjust their profits for stock-based compensation (SBC), but we prioritize GAAP operating margin because SBC is a real expense used to attract and retain engineering and sales talent. This metric shows how much revenue remains after accounting for all core expenses – everything from the cost of goods sold to sales and R&D.

Nutanix has managed its cost base well over the last year. It demonstrated solid profitability for a software business, producing an average operating margin of 7.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Nutanix’s operating margin rose by 5 percentage points over the last two years, as its sales growth gave it operating leverage.

This quarter, Nutanix generated an operating margin profit margin of 11.6%, up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Nutanix has shown impressive cash profitability, driven by its attractive business model and cost-effective customer acquisition strategy that give it the option to invest in new products and services rather than sales and marketing. The company’s free cash flow margin averaged 21.8% over the last year, better than the broader software sector.

Nutanix broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 28.5 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict Nutanix’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 21.8% for the last 12 months will increase to 28.3%, giving it more flexibility for investments, share buybacks, and dividends.

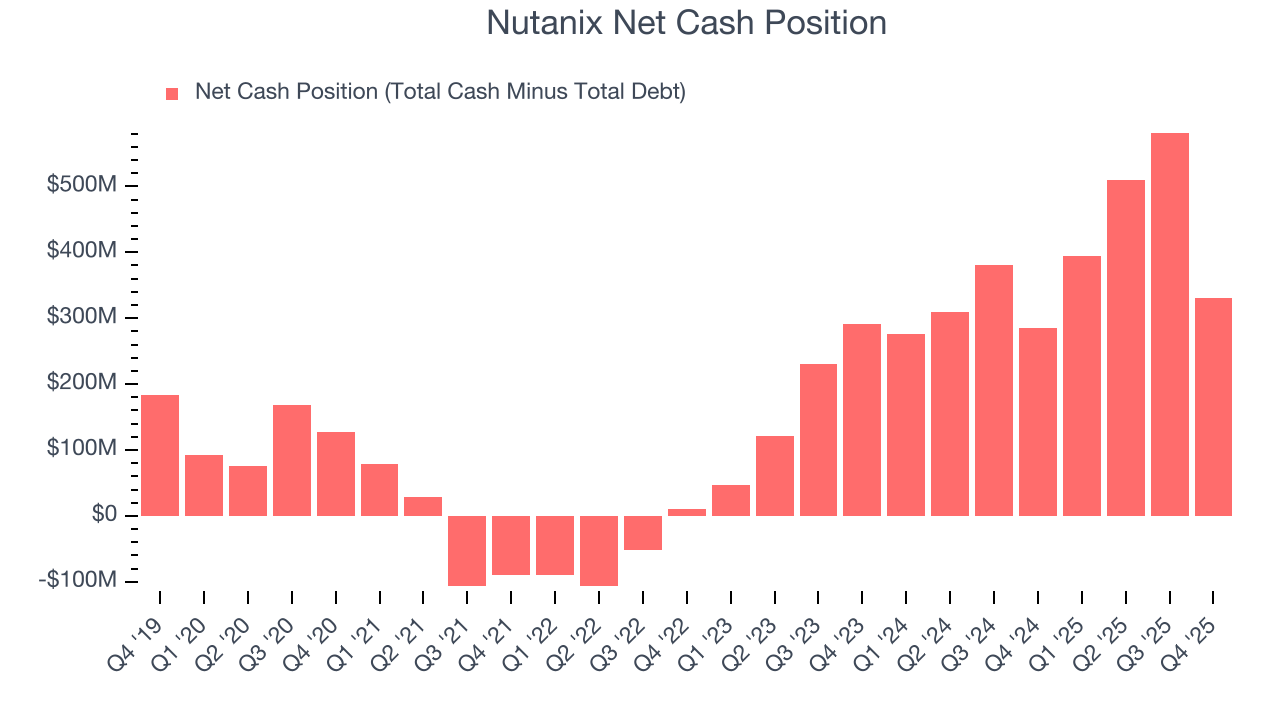

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Nutanix is a profitable, well-capitalized company with $1.87 billion of cash and $1.54 billion of debt on its balance sheet. This $331.1 million net cash position is 3.1% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Nutanix’s Q4 Results

It was encouraging to see Nutanix beat analysts’ revenue expectations this quarter. On the other hand, its revenue guidance for next quarter missed and its annual recurring revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded up 14% to $43.93 immediately after reporting.

13. Is Now The Time To Buy Nutanix?

Updated: February 27, 2026 at 12:09 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Nutanix.

There are things to like about Nutanix. Although its revenue growth was a little slower over the last five years and analysts expect growth to slow over the next 12 months, its admirable gross margin indicates excellent unit economics. And while its expanding operating margin shows it’s becoming more efficient at building and selling its software, its efficient sales strategy allows it to target and onboard new users at scale.

Nutanix’s price-to-sales ratio based on the next 12 months is 3.7x. When scanning the software space, Nutanix trades at a fair valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $59.34 on the company (compared to the current share price of $39.55), implying they see 50% upside in buying Nutanix in the short term.