QuidelOrtho (QDEL)

QuidelOrtho is in for a bumpy ride. Its plummeting sales and returns on capital show its profits are shrinking as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think QuidelOrtho Will Underperform

Born from the 2022 merger of Quidel and Ortho Clinical Diagnostics, QuidelOrtho (NASDAQ:QDEL) develops and manufactures diagnostic testing solutions for healthcare providers, from rapid point-of-care tests to complex laboratory instruments and systems.

- Sales were less profitable over the last five years as its earnings per share fell by 36.1% annually, worse than its revenue declines

- Sales tumbled by 4.6% annually over the last two years, showing market trends are working against its favor during this cycle

- Projected sales growth of 1.4% for the next 12 months suggests sluggish demand

QuidelOrtho is skating on thin ice. There are more promising alternatives.

Why There Are Better Opportunities Than QuidelOrtho

At $14.79 per share, QuidelOrtho trades at 7.2x forward P/E. This is a cheap valuation multiple, but for good reason. You get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. QuidelOrtho (QDEL) Research Report: Q4 CY2025 Update

Healthcare diagnostics company QuidelOrtho (NASDAQ:QDEL) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 2.2% year on year to $723.6 million. The company’s full-year revenue guidance of $2.8 billion at the midpoint came in 1.1% above analysts’ estimates. Its non-GAAP profit of $0.46 per share was 8.8% above analysts’ consensus estimates.

QuidelOrtho (QDEL) Q4 CY2025 Highlights:

- Revenue: $723.6 million vs analyst estimates of $701.2 million (2.2% year-on-year growth, 3.2% beat)

- Adjusted EPS: $0.46 vs analyst estimates of $0.42 (8.8% beat)

- Adjusted EBITDA: $153.3 million vs analyst estimates of $151.6 million (21.2% margin, 1.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $2.21 at the midpoint, missing analyst estimates by 11.1%

- EBITDA guidance for the upcoming financial year 2026 is $650 million at the midpoint, below analyst estimates of $655 million

- Operating Margin: -9.2%, up from -14.2% in the same quarter last year

- Constant Currency Revenue rose 1.1% year on year (-4.4% in the same quarter last year)

- Market Capitalization: $1.98 billion

Company Overview

Born from the 2022 merger of Quidel and Ortho Clinical Diagnostics, QuidelOrtho (NASDAQ:QDEL) develops and manufactures diagnostic testing solutions for healthcare providers, from rapid point-of-care tests to complex laboratory instruments and systems.

QuidelOrtho operates across the entire diagnostic testing spectrum through four main business units: Labs, Molecular Diagnostics, Point of Care, and Transfusion Medicine. The company's products range from clinical chemistry analyzers that measure chemicals in bodily fluids to immunoassay systems that detect proteins related to disease, and from rapid tests that provide results in minutes to sophisticated molecular diagnostic platforms.

The company's customers include hospitals, clinical laboratories, physician offices, urgent care clinics, universities, retail clinics, pharmacies, and blood banks across more than 130 countries. During the COVID-19 pandemic, QuidelOrtho expanded its reach directly to consumers with at-home tests, while also serving school districts and health departments.

A physician might use QuidelOrtho's Sofia rapid test to diagnose a patient with influenza in minutes, allowing for immediate treatment decisions. Meanwhile, a hospital laboratory might run hundreds of patient samples daily on the company's Vitros systems to measure everything from cholesterol levels to thyroid function.

QuidelOrtho employs a "razor/razor blade" business model for much of its revenue, placing instruments with customers under long-term contracts that require the ongoing purchase of proprietary reagents and consumables. This creates a recurring revenue stream, as the instruments are closed systems that only work with QuidelOrtho's supplies.

The company maintains manufacturing facilities in the United States and United Kingdom, with a global network of sales centers, administrative offices, and warehouses. QuidelOrtho complements its product offerings with comprehensive services, including remote monitoring, technical support, and consulting services that help laboratories improve workflow and productivity.

QuidelOrtho's business is subject to seasonal fluctuations, particularly for its respiratory products, which see higher demand during fall and winter cold and flu seasons. The company must navigate complex regulatory requirements across global markets, including FDA clearances in the US and various international approvals.

4. Medical Devices & Supplies - Imaging, Diagnostics

The medical devices and supplies industry, particularly those specializing in imaging and diagnostics, operates with a comparatively stable yet capital-intensive business model. Companies in this space benefit from consistent demand driven by the essential nature of diagnostic tools in patient care, as well as recurring revenue streams from consumables, service contracts, and equipment maintenance. However, the industry faces challenges such as significant upfront development costs, stringent regulatory requirements, and pricing pressures from hospitals and healthcare systems, which are increasingly focused on cost containment. Looking ahead, the industry should enjoy tailwinds from advancements in technology, including the integration of artificial intelligence to enhance diagnostic accuracy and workflow efficiency, as well as rising demand for imaging solutions driven by aging populations. On the other hand, headwinds could arise from a rethinking of healthcare costs potentially resulting in reimbursement cuts and slower capital equipment purchasing. Additionally, cybersecurity concerns surrounding connected medical devices could introduce new risks and complexities for manufacturers.

QuidelOrtho competes with several major players in the diagnostic testing market, including Abbott Laboratories (NYSE:ABT), Roche (OTC:RHHBY), Thermo Fisher Scientific (NYSE:TMO), Danaher (NYSE:DHR), and Siemens Healthineers (OTC:SMMNY).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $2.73 billion in revenue over the past 12 months, QuidelOrtho has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

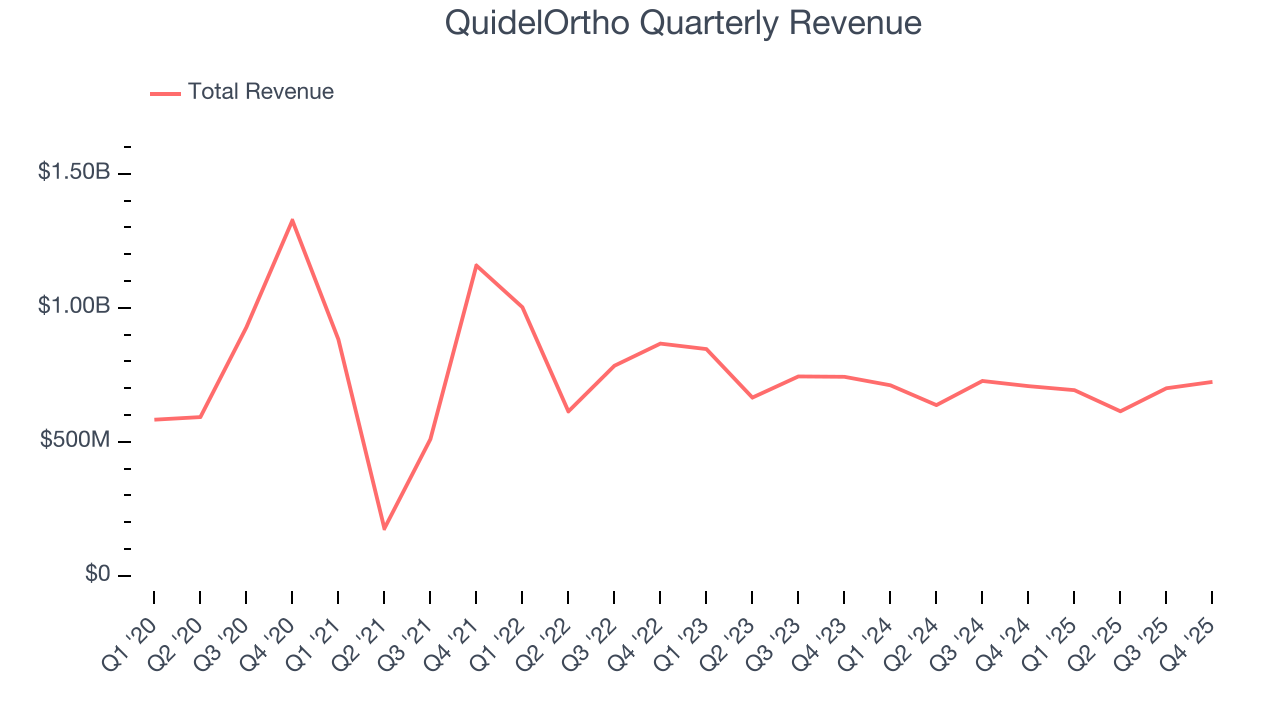

6. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. QuidelOrtho’s demand was weak over the last five years as its sales fell at a 4.4% annual rate. This wasn’t a great result and suggests it’s a low quality business.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. QuidelOrtho’s annualized revenue declines of 4.6% over the last two years align with its five-year trend, suggesting its demand has consistently shrunk.

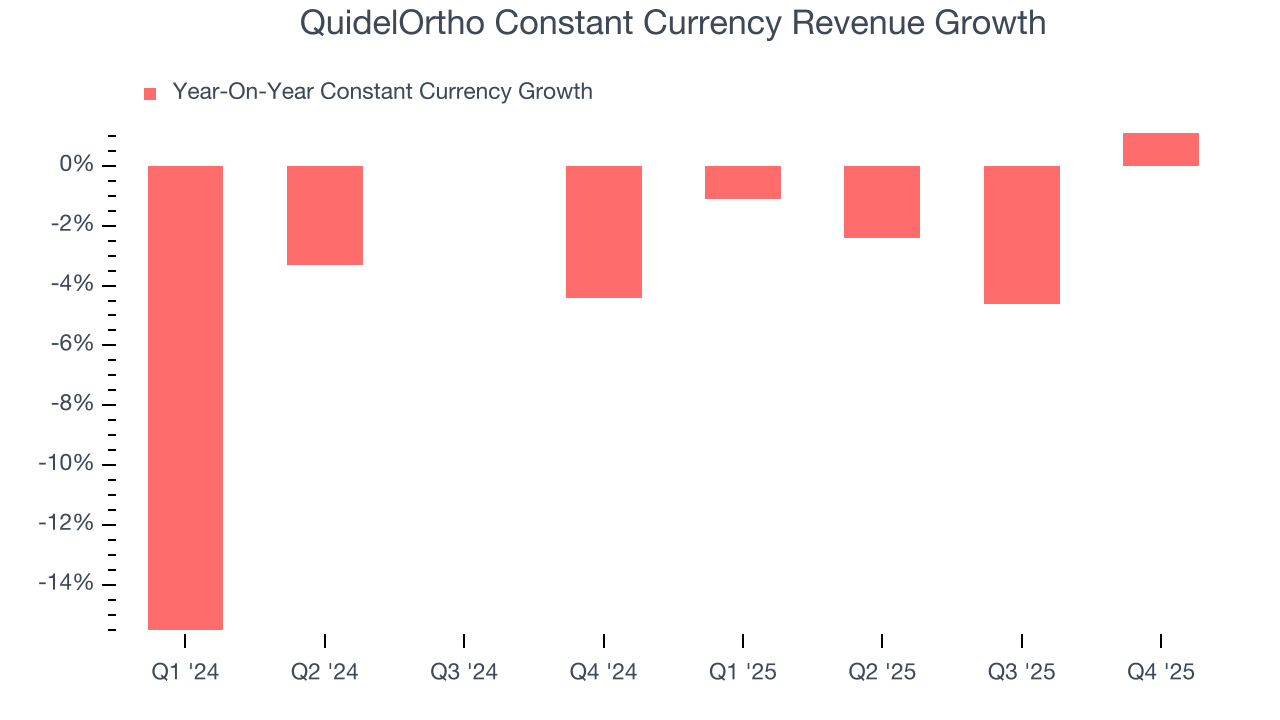

QuidelOrtho also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last two years, its constant currency sales averaged 3.8% year-on-year declines. Because this number aligns with its normal revenue growth, we can see that QuidelOrtho has properly hedged its foreign currency exposure.

This quarter, QuidelOrtho reported modest year-on-year revenue growth of 2.2% but beat Wall Street’s estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to grow 1.3% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

7. Operating Margin

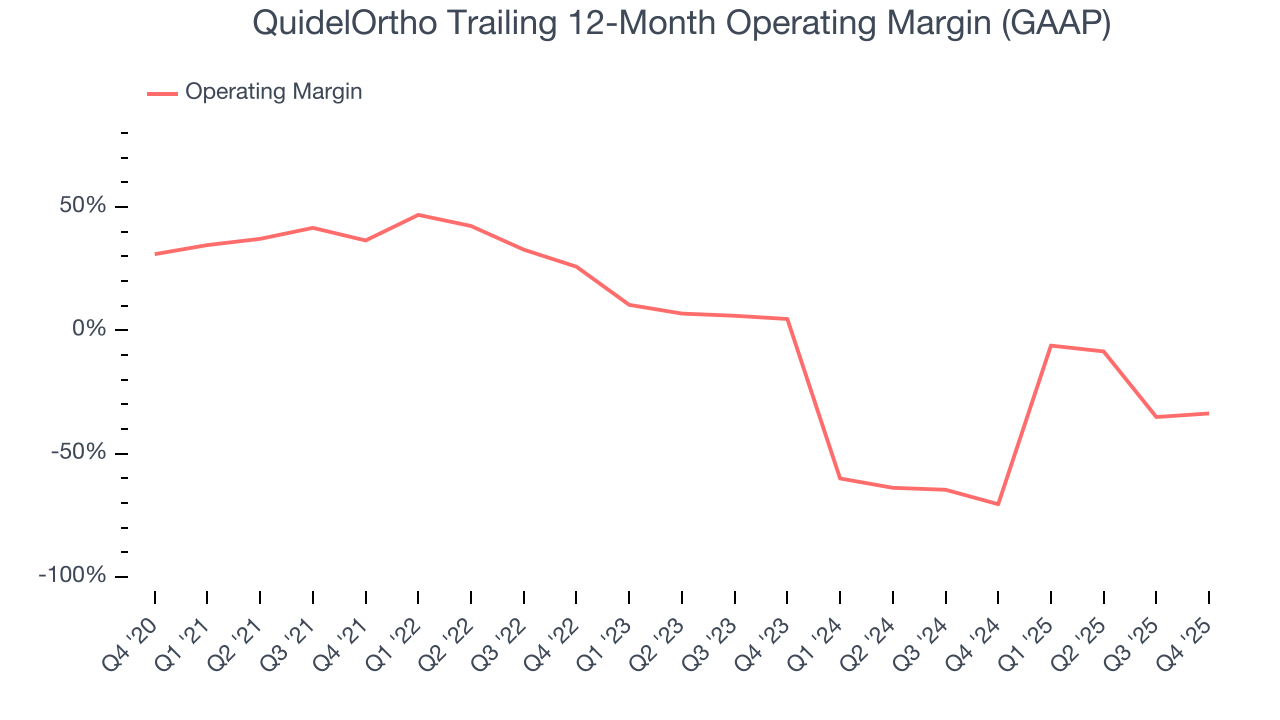

QuidelOrtho’s high expenses have contributed to an average operating margin of negative 6.2% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, QuidelOrtho’s operating margin decreased by 70.1 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 38.3 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

QuidelOrtho’s operating margin was negative 9.2% this quarter. The company's consistent lack of profits raise a flag.

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

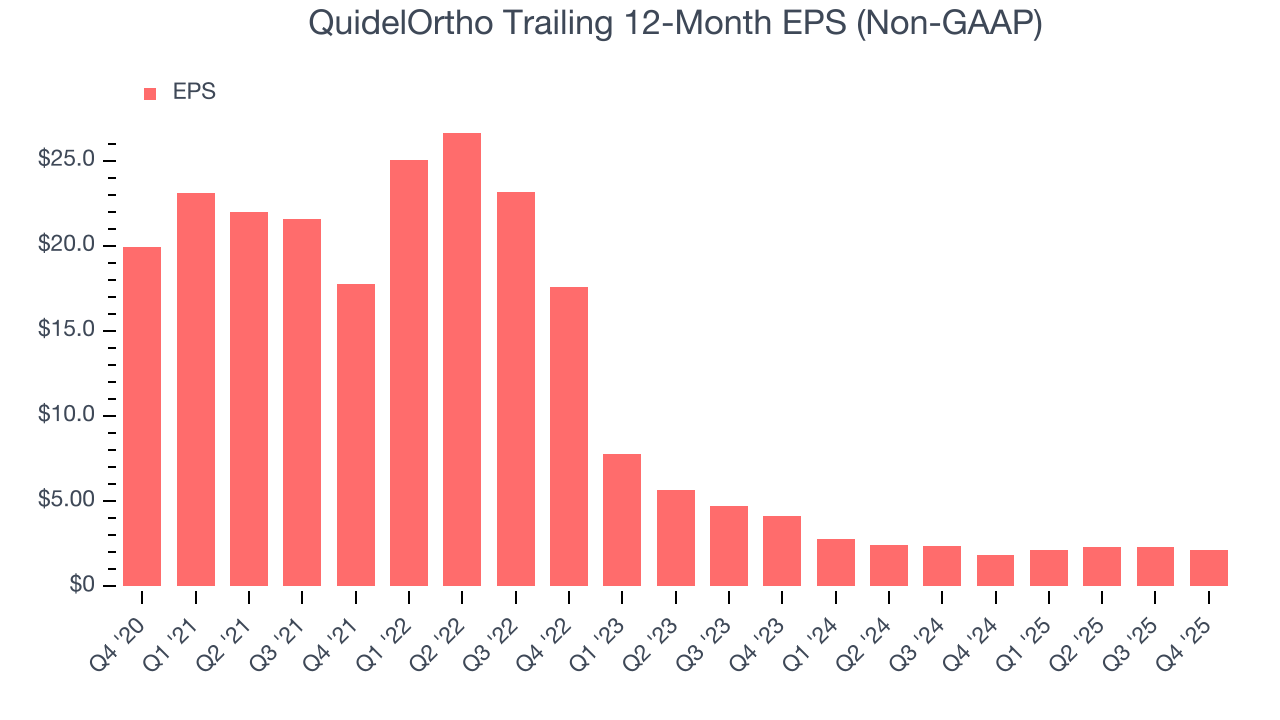

Sadly for QuidelOrtho, its EPS declined by 36.1% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

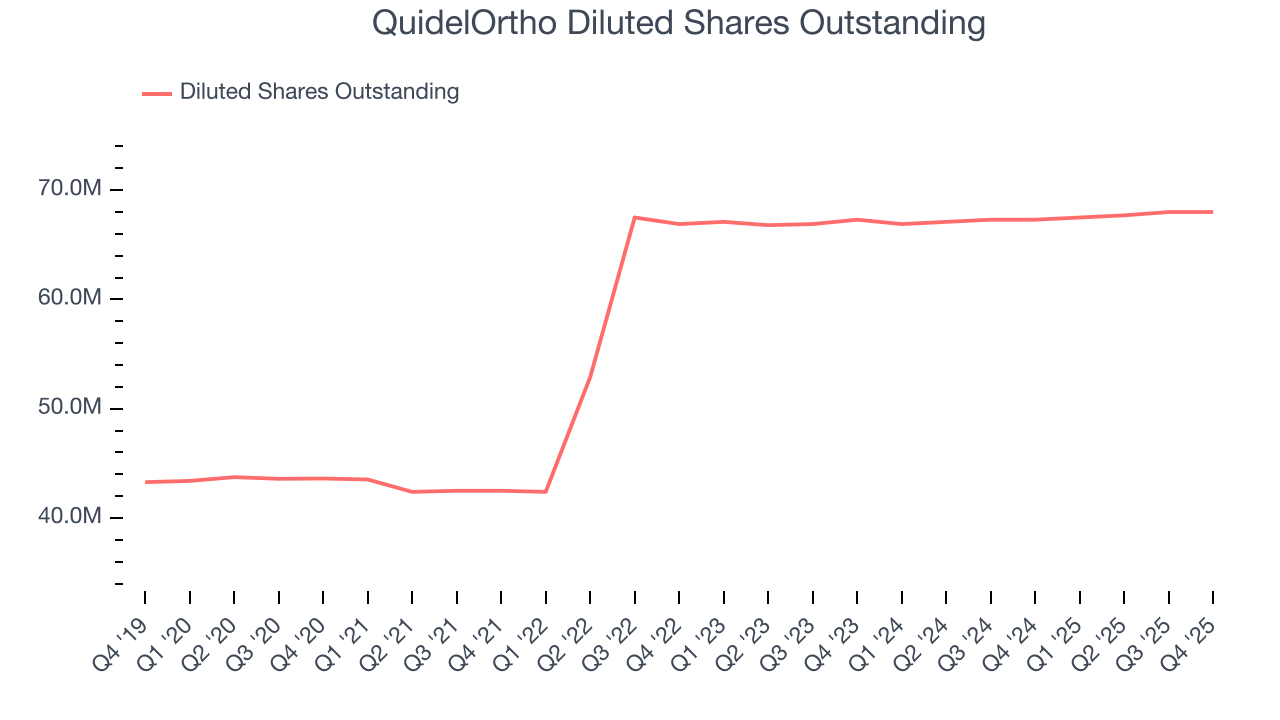

We can take a deeper look into QuidelOrtho’s earnings to better understand the drivers of its performance. As we mentioned earlier, QuidelOrtho’s operating margin expanded this quarter but declined by 70.1 percentage points over the last five years. Its share count also grew by 55.9%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, QuidelOrtho reported adjusted EPS of $0.46, down from $0.63 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects QuidelOrtho’s full-year EPS of $2.12 to grow 18.3%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

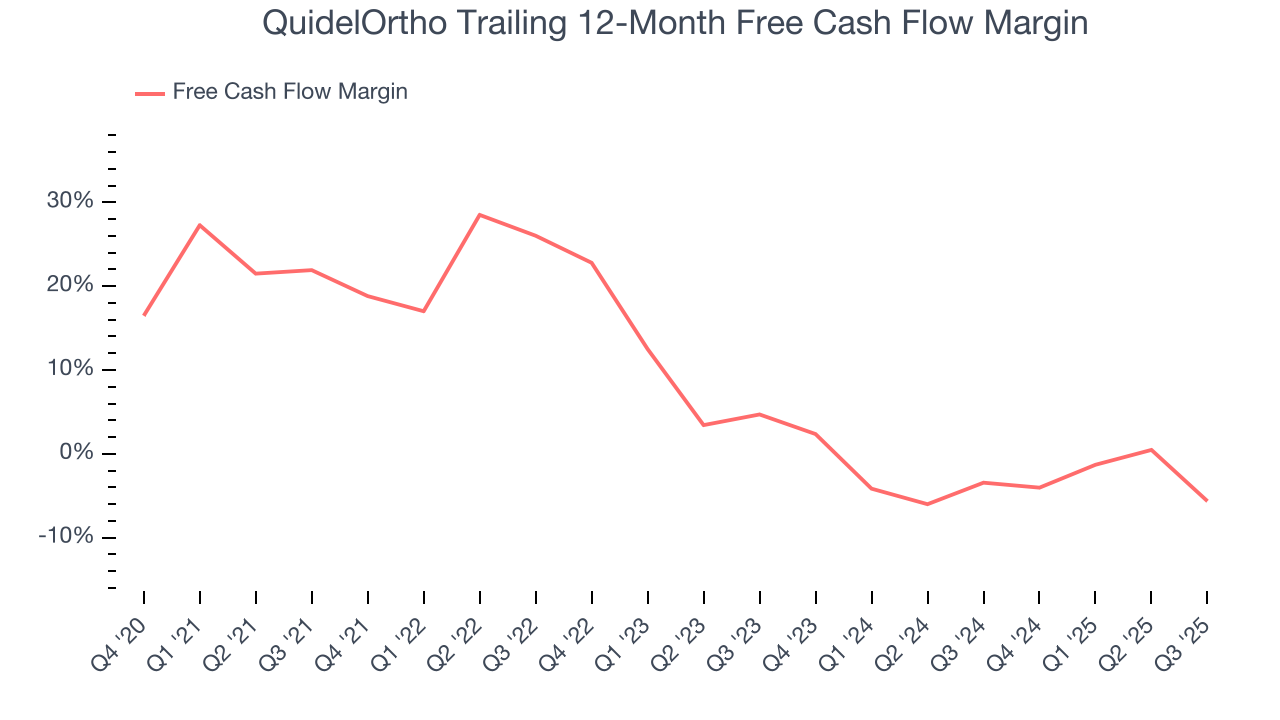

QuidelOrtho has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.6% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that QuidelOrtho’s margin dropped by 22.7 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

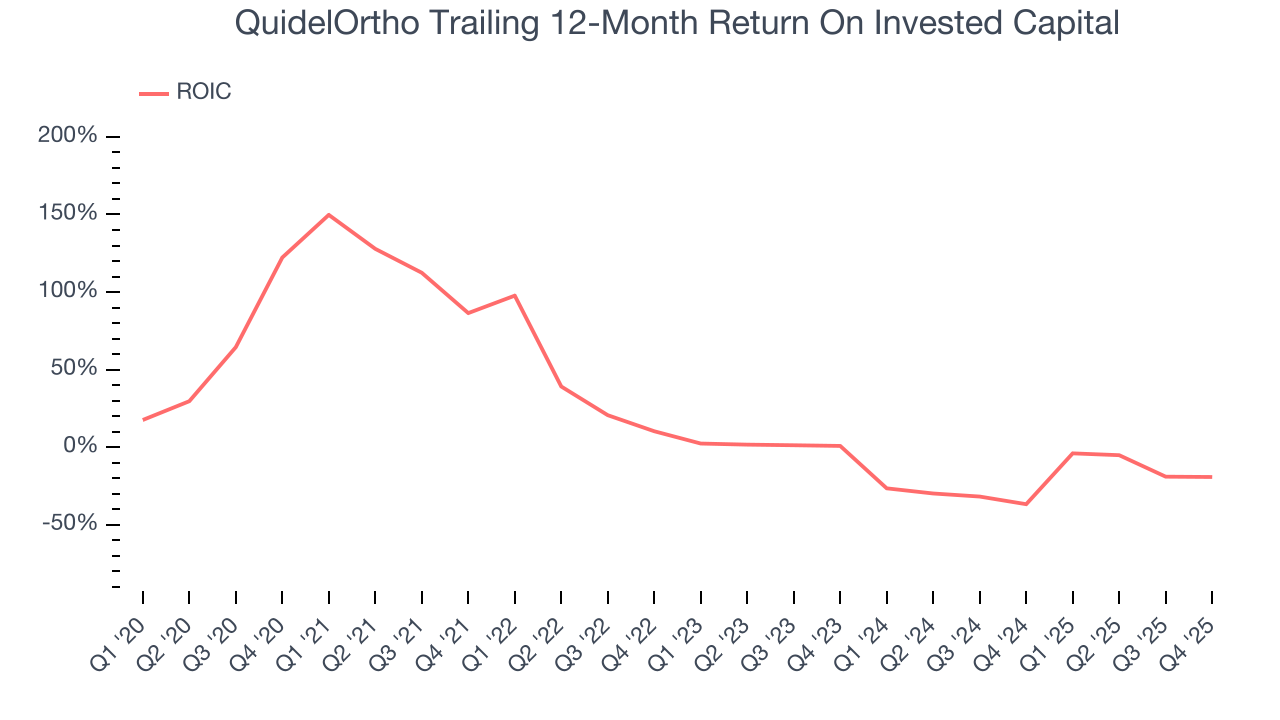

QuidelOrtho’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 8.3%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, QuidelOrtho’s ROIC has unfortunately decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

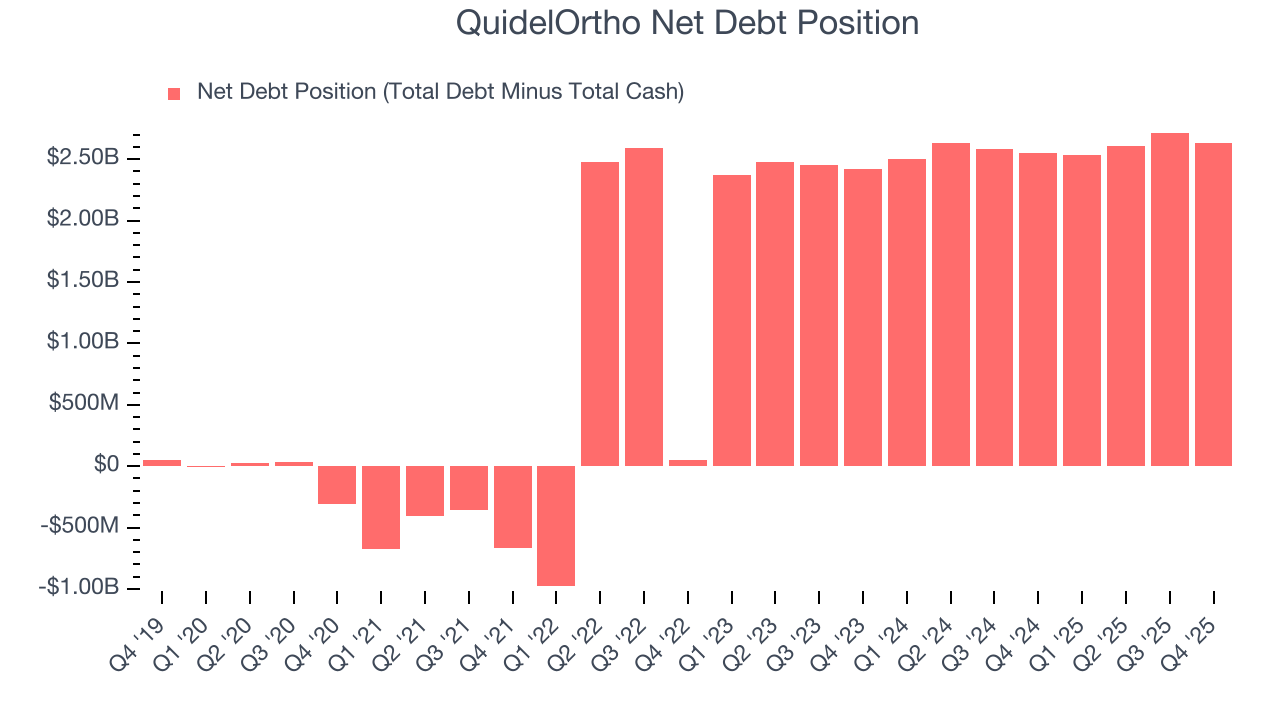

QuidelOrtho reported $169.8 million of cash and $2.80 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $597 million of EBITDA over the last 12 months, we view QuidelOrtho’s 4.4× net-debt-to-EBITDA ratio as safe. We also see its $83.1 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from QuidelOrtho’s Q4 Results

We enjoyed seeing QuidelOrtho beat analysts’ revenue expectations this quarter. We were also glad its full-year revenue guidance slightly exceeded Wall Street’s estimates. On the other hand, its full-year EPS guidance missed. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 2.6% to $28.05 immediately following the results.

13. Is Now The Time To Buy QuidelOrtho?

Updated: March 30, 2026 at 12:18 AM EDT

Are you wondering whether to buy QuidelOrtho or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

QuidelOrtho doesn’t pass our quality test. For starters, its revenue has declined over the last five years. While its strong operating margins show it’s a well-run business, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

QuidelOrtho’s P/E ratio based on the next 12 months is 7.2x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $34.67 on the company (compared to the current share price of $14.79).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.