Richardson Electronics (RELL)

We wouldn’t buy Richardson Electronics. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Richardson Electronics Will Underperform

Founded in 1947, Richardson Electronics (NASDAQ:RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 8% annually over the last two years

- Falling earnings per share over the last two years has some investors worried as stock prices ultimately follow EPS over the long term

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

Richardson Electronics fails to meet our quality criteria. Better businesses are for sale in the market.

Why There Are Better Opportunities Than Richardson Electronics

Richardson Electronics’s stock price of $11.55 implies a valuation ratio of 61.7x forward P/E. The current multiple is quite expensive, especially for the tepid revenue growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Richardson Electronics (RELL) Research Report: Q4 CY2025 Update

Electronics distributor Richardson Electronics (NASDAQ:RELL) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 5.7% year on year to $52.29 million. Its GAAP loss of $0.01 per share was in line with analysts’ consensus estimates.

Richardson Electronics (RELL) Q4 CY2025 Highlights:

- Revenue: $52.29 million vs analyst estimates of $49.9 million (5.7% year-on-year growth, 4.8% beat)

- EPS (GAAP): -$0.01 vs analyst estimates of -$0.01 (in line)

- Adjusted EBITDA: $741,000 vs analyst estimates of $720,000 (1.4% margin, relatively in line)

- Operating Margin: 0.3%, up from -1.4% in the same quarter last year

- Free Cash Flow was -$1.71 million, down from $4.95 million in the same quarter last year

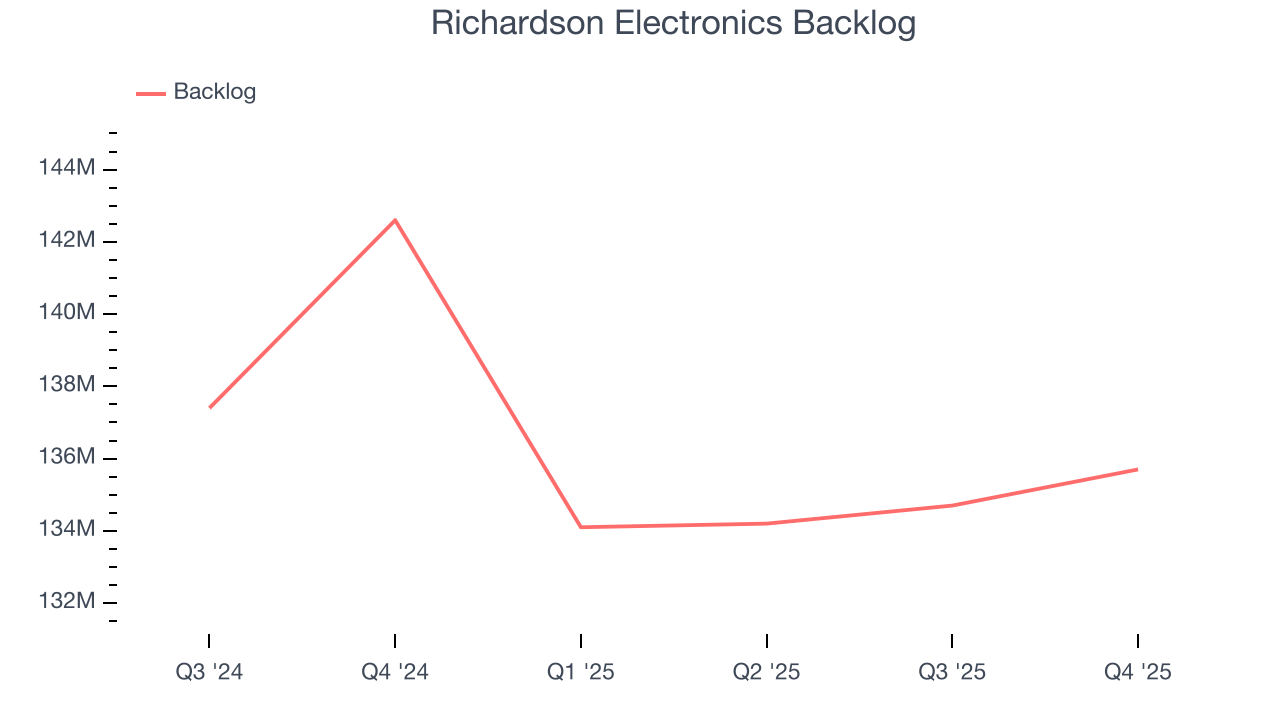

- Backlog: $135.7 million at quarter end, down 4.8% year on year

- Market Capitalization: $167.2 million

Company Overview

Founded in 1947, Richardson Electronics (NASDAQ:RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

Richardson Electronics offers products including high-voltage capacitors, microwave tubes, and custom displays. For example, the company supplies specialized components used in MRI machines within the healthcare sector, power control systems for wind turbines in renewable energy, and broadcast transmission equipment in the communications industry. The company also operates Canvys, which provides customized displays as well as EDAC Power America, which specializes in power management systems.

Revenue for Richardson Electronics is generated from the sale of these products and related components. The company sells its products worldwide through direct sales forces, other distributors, and an e-commerce platform. Richardson Electronics mainly targets original equipment manufacturers (OEMs) and end users in high-tech sectors.

While some of the company’s revenue is project-based, the company also benefits from recurring sales through maintenance, replacement parts, and upgrades. This can somewhat lessen the impact of macroeconomic swings on the appetite for projects in end markets such as telecom and healthcare, providing a more predictable and steady source of revenues.

4. Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

Competitors in the electronic distribution industry include Arrow Electronics (NYSE:ARW), Avnet (NASDAQ:AVT), and TTM Technologies (NASDAQ:TTMI).

5. Revenue Growth

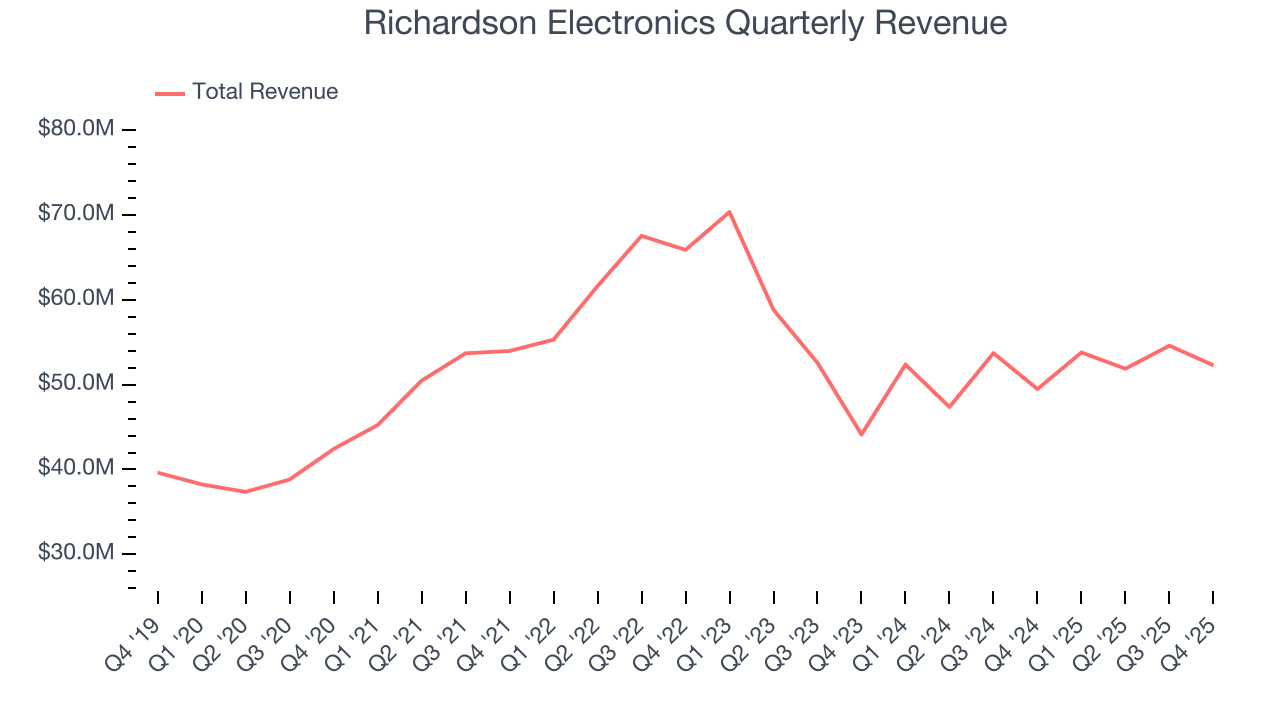

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Richardson Electronics grew its sales at a mediocre 6.3% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a rough starting point for our analysis.

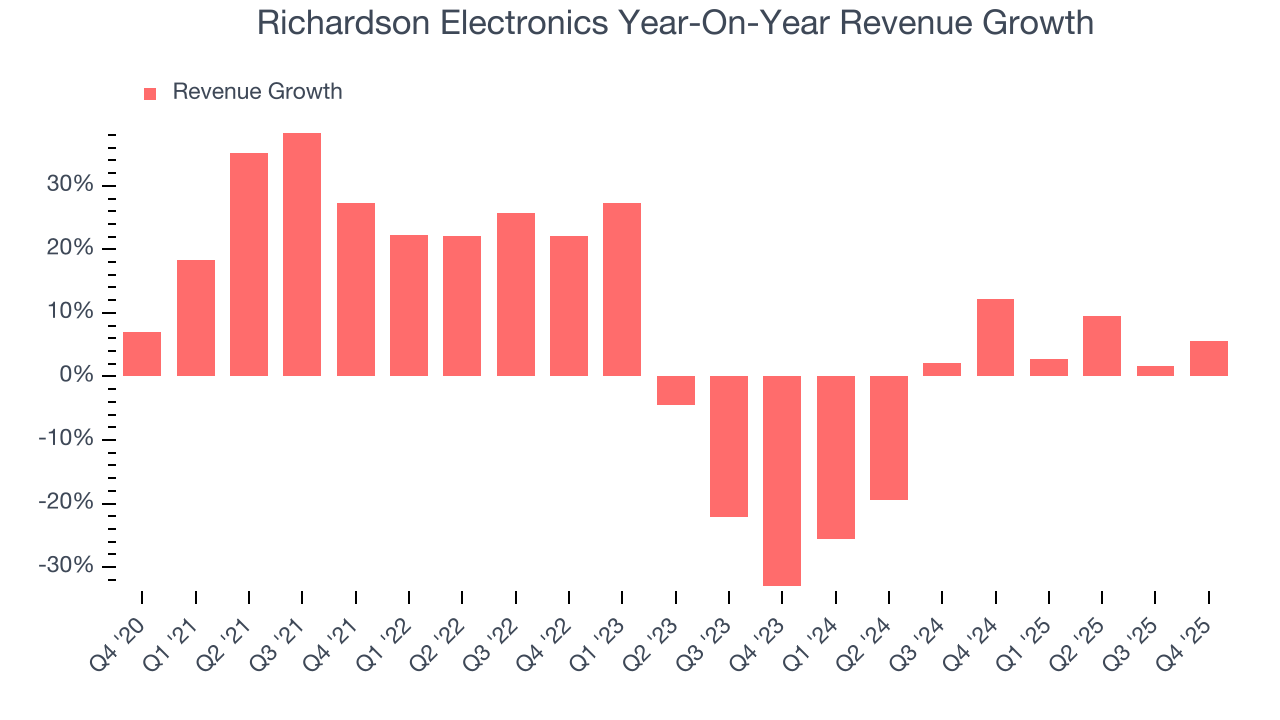

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Richardson Electronics’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3% annually.

Richardson Electronics also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Richardson Electronics’s backlog reached $135.7 million in the latest quarter and averaged 3.4% year-on-year declines over the last two years. Because this number is in line with its revenue growth, we can see the company effectively balanced its new order intake and fulfillment processes.

This quarter, Richardson Electronics reported year-on-year revenue growth of 5.7%, and its $52.29 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, an improvement versus the last two years. This projection is above the sector average and indicates its newer products and services will catalyze better top-line performance.

6. Gross Margin & Pricing Power

Cost of sales for an industrials business is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics.

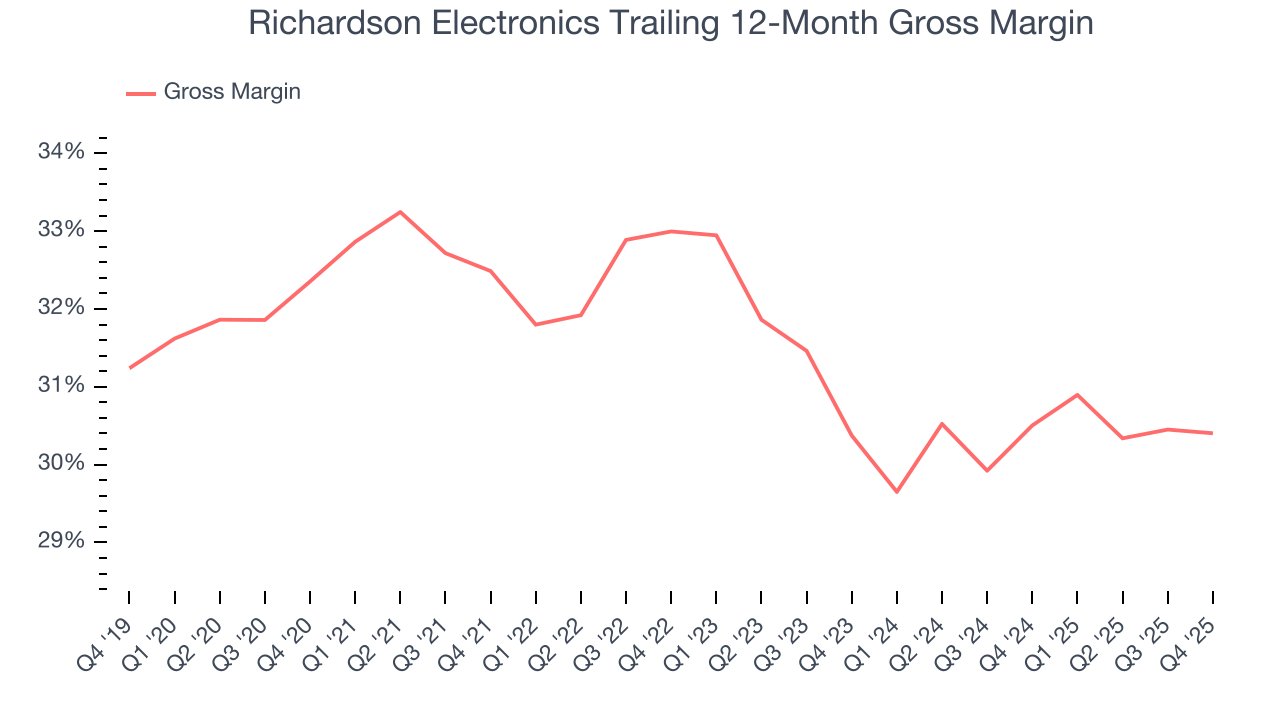

Richardson Electronics’s unit economics are better than the typical industrials business, signaling its products are somewhat differentiated through quality or brand. As you can see below, it averaged a decent 31.4% gross margin over the last five years. Said differently, Richardson Electronics paid its suppliers $68.60 for every $100 in revenue.

Richardson Electronics’s gross profit margin came in at 30.7% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

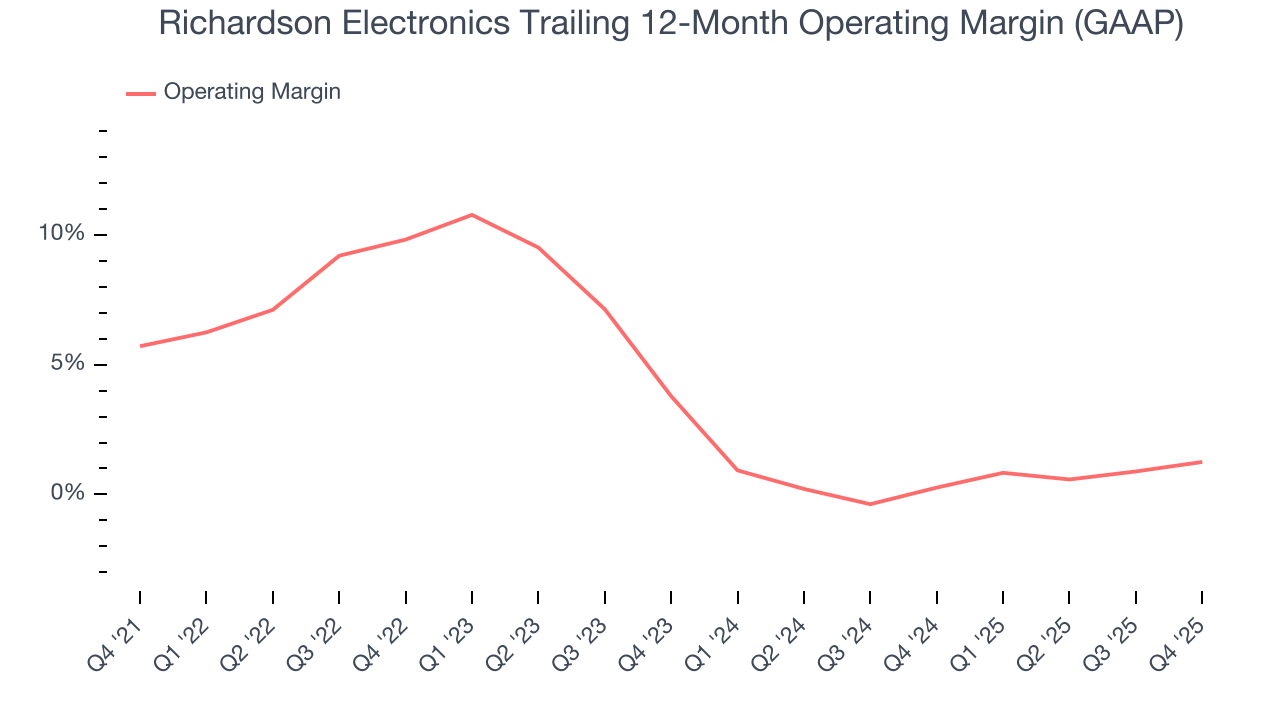

7. Operating Margin

Richardson Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.4% was weak for an industrials business.

Analyzing the trend in its profitability, Richardson Electronics’s operating margin decreased by 4.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Richardson Electronics’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Richardson Electronics’s breakeven margin was up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

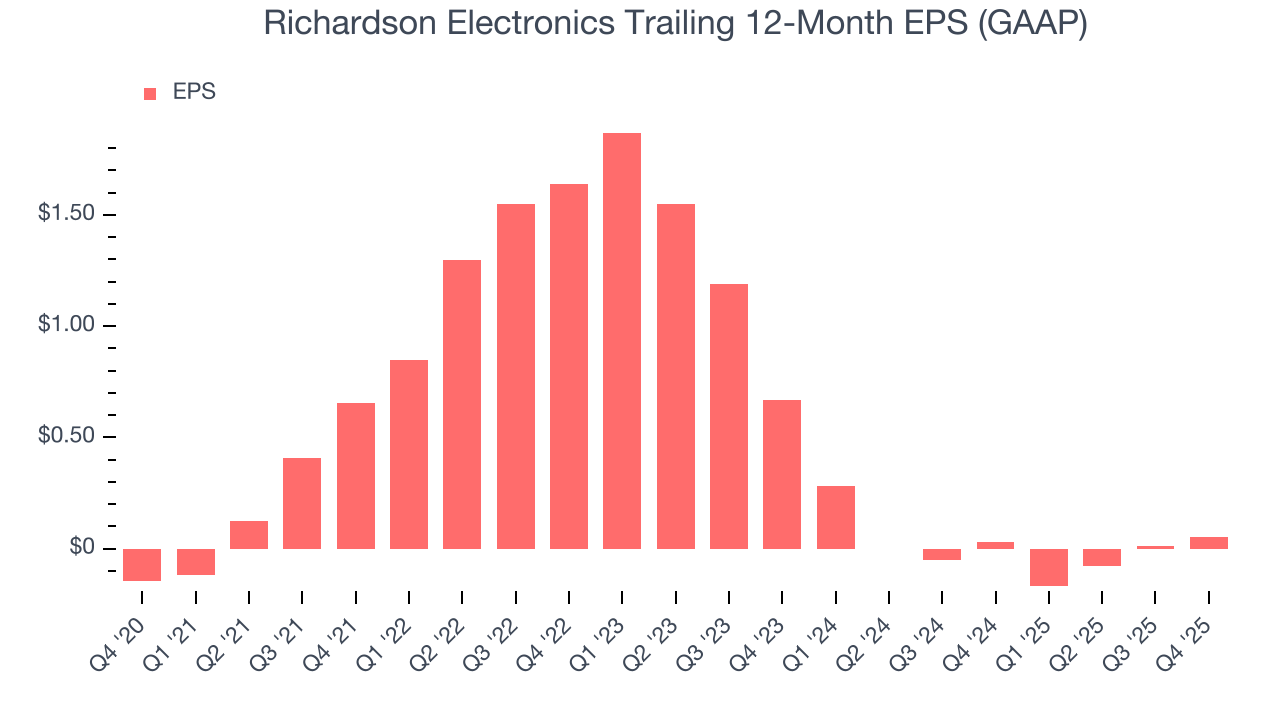

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Richardson Electronics’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Richardson Electronics, its EPS declined by more than its revenue over the last two years, dropping 72.7%. This tells us the company struggled to adjust to shrinking demand.

In Q4, Richardson Electronics reported EPS of negative $0.01, up from negative $0.05 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Richardson Electronics’s full-year EPS of $0.05 to grow 630%.

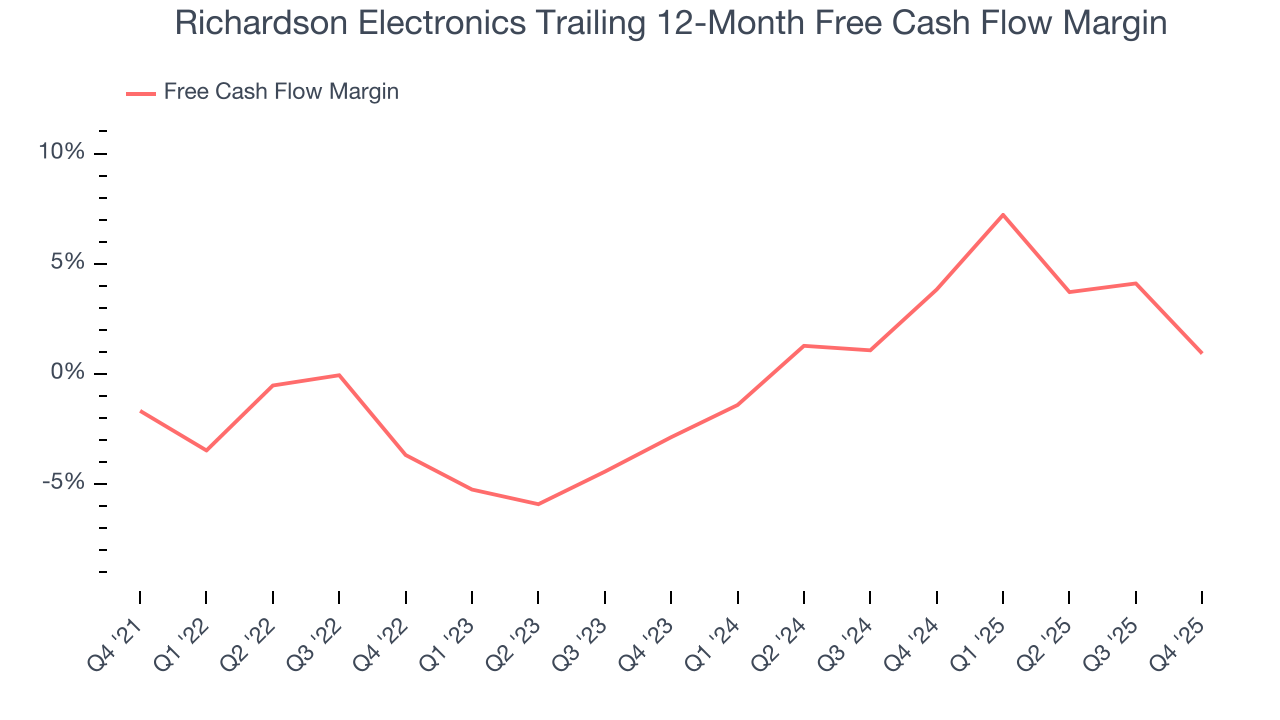

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Richardson Electronics broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that Richardson Electronics’s margin expanded by 2.6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Richardson Electronics burned through $1.71 million of cash in Q4, equivalent to a negative 3.3% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

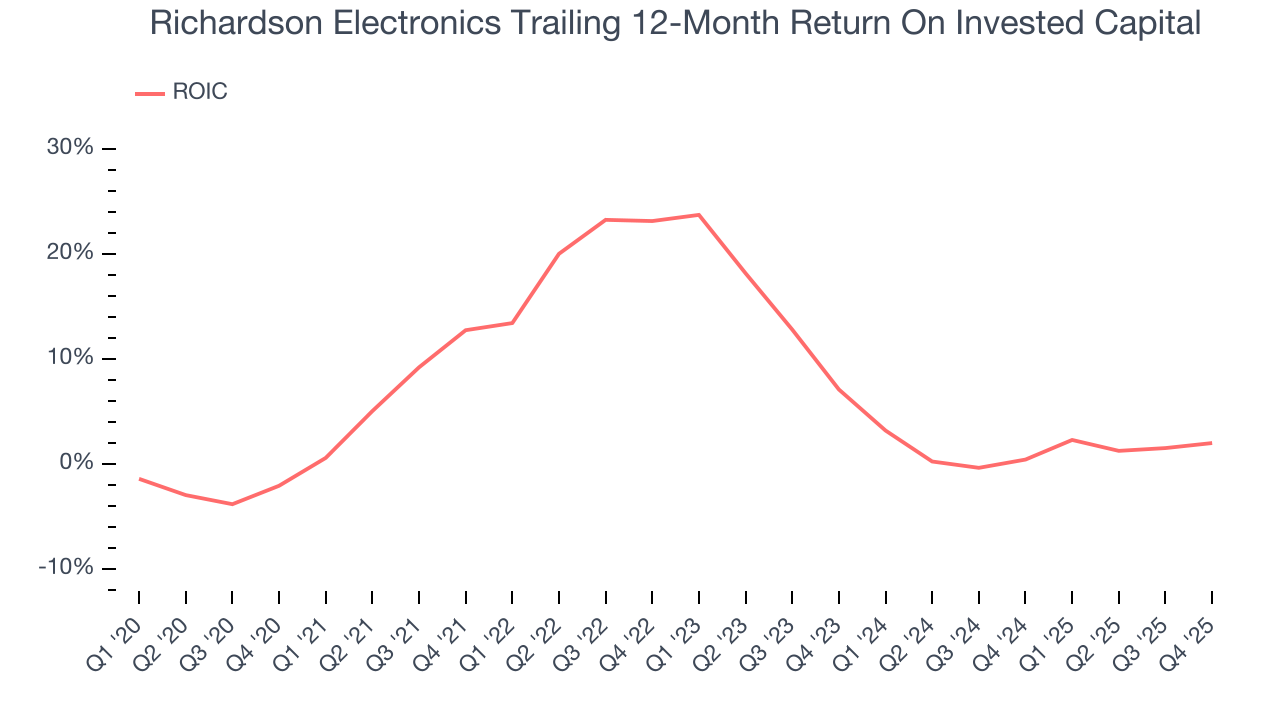

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Richardson Electronics historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9.1%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Richardson Electronics’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

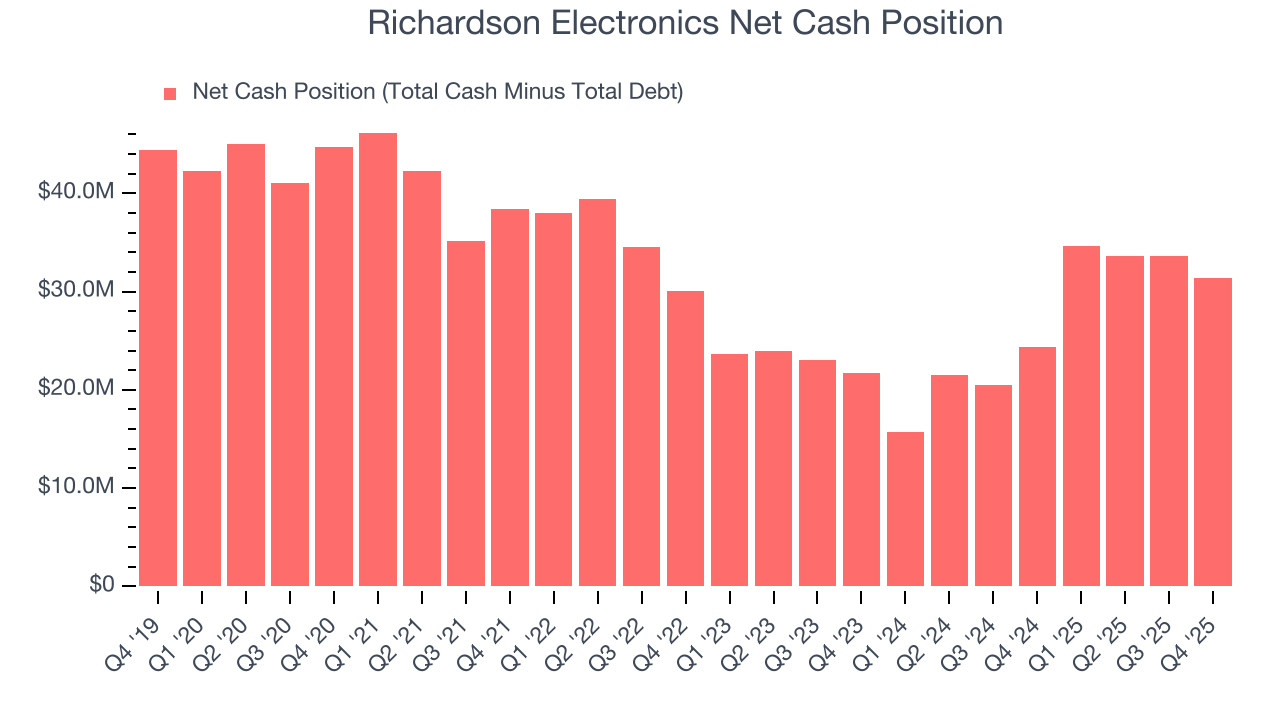

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Richardson Electronics is a profitable, well-capitalized company with $33.14 million of cash and $1.74 million of debt on its balance sheet. This $31.4 million net cash position is 18.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Richardson Electronics’s Q4 Results

We were impressed by how significantly Richardson Electronics blew past analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. Investors were likely hoping for more, and shares traded down 10.5% to $10.45 immediately after reporting.

13. Is Now The Time To Buy Richardson Electronics?

Updated: January 7, 2026 at 4:26 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Richardson Electronics.

We see the value of companies helping their customers, but in the case of Richardson Electronics, we’re out. For starters, its revenue growth was mediocre over the last five years. And while its astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its low free cash flow margins give it little breathing room.

Richardson Electronics’s P/E ratio based on the next 12 months is 36.5x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $12.50 on the company (compared to the current share price of $10.45).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.