Petco (WOOF)

We wouldn’t buy Petco. Its falling revenue and negative returns on capital suggest it’s destroying value as demand fizzles out.― StockStory Analyst Team

1. News

2. Summary

Why We Think Petco Will Underperform

Historically known for its window displays of pets for sale or adoption, Petco (NASDAQ:WOOF) is a specialty retailer of pet food and supplies as well as a provider of services such as wellness checks and grooming.

- Push for growth has led to negative returns on capital, signaling value destruction, and its decreasing returns suggest its historical profit centers are aging

- Falling earnings per share over the last three years has some investors worried as stock prices ultimately follow EPS over the long term

- 6× net-debt-to-EBITDA ratio shows it’s overleveraged and increases the probability of shareholder dilution if things turn unexpectedly

Petco’s quality isn’t up to par. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Petco

At $3.61 per share, Petco trades at 13.6x forward P/E. This multiple is quite expensive for the quality you get.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Petco (WOOF) Research Report: Q4 CY2025 Update

Pet-focused retailer Petco (NASDAQ:WOOF) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 2.4% year on year to $1.52 billion. The company expects next quarter’s revenue to be around $1.49 billion, close to analysts’ estimates. Its GAAP loss of $0.01 per share was $0.02 below analysts’ consensus estimates.

Petco (WOOF) Q4 CY2025 Highlights:

- Revenue: $1.52 billion vs analyst estimates of $1.51 billion (2.4% year-on-year decline, in line)

- EPS (GAAP): -$0.01 vs analyst estimates of $0.01 ($0.02 miss)

- Adjusted EBITDA: $106.3 million vs analyst estimates of $94.16 million (7% margin, 12.9% beat)

- Revenue Guidance for Q1 CY2026 is $1.49 billion at the midpoint, roughly in line with what analysts were expecting

- EBITDA guidance for the upcoming financial year 2026 is $422.5 million at the midpoint, above analyst estimates of $414.3 million

- Operating Margin: 2.1%, in line with the same quarter last year

- Free Cash Flow Margin: 7.7%, up from 3.8% in the same quarter last year

- Same-Store Sales fell 1.6% year on year (0.5% in the same quarter last year)

- Market Capitalization: $655.3 million

Company Overview

Historically known for its window displays of pets for sale or adoption, Petco (NASDAQ:WOOF) is a specialty retailer of pet food and supplies as well as a provider of services such as wellness checks and grooming.

Since its 1965 founding, the company has evolved from largely a place where consumers could buy or adopt pets such as dogs and fish to a one-stop shop for current and potential pet owners. A cat owner can buy Merrick cat food made from natural ingredients, a dog owner can buy Frontline flea and tick collars, and an aquarium owner can buy Tetra water filters. Additionally, services are available at Petco. Cats can be groomed, dogs can undergo parasite treatments, and small pets such as rabbits can undergo diagnostic tests.

Petco store sizes can vary, but most are 10,000 to 20,000 square feet. They tend to be located in shopping centers and retail plazas that get regular foot traffic. Most stores tend to dedicate the largest percentage of floor space to pet food and supplies such as toys and grooming products, separated by type of animal. There are then special aquatic sections with fish tanks and service areas for pets to be groomed and treated for minor ailments. Most Petco stores partner with local animal shelters or rescue organizations to facilitate adoptions of various animal types.

4. Specialty Retail

Some retailers try to sell everything under the sun, while others—appropriately called Specialty Retailers—focus on selling a narrow category and aiming to be exceptional at it. Whether it’s eyeglasses, sporting goods, or beauty and cosmetics, these stores win with depth of product in their category as well as in-store expertise and guidance for shoppers who need it. E-commerce competition exists and waning retail foot traffic impacts these retailers, but the magnitude of the headwinds depends on what they sell and what extra value they provide in their stores.

Competitors that offer pet products and services include Chewy (NYSE:CHWY), Tractor Supply Company (NASDAQ:TSCO), and Academy Sports and Outdoors (NASDAQ:ASO) as well as private companies such as PetSmart.

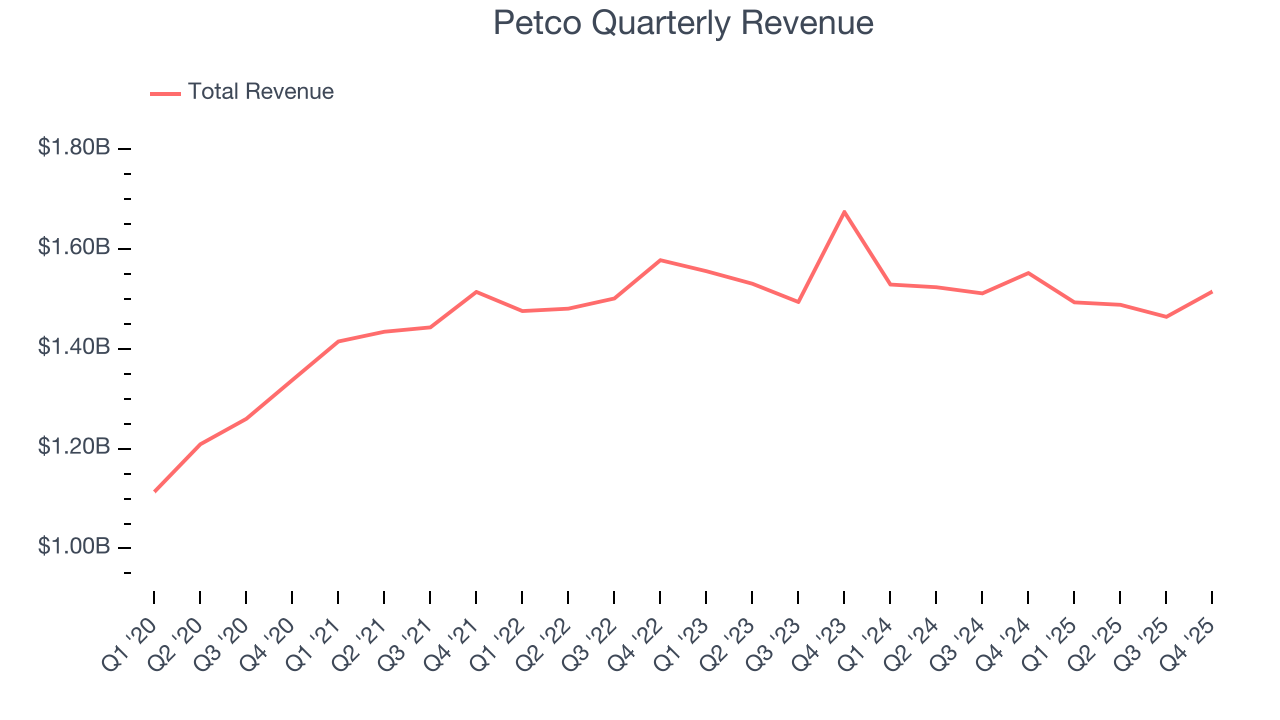

5. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years.

With $5.96 billion in revenue over the past 12 months, Petco is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Petco struggled to increase demand as its $5.96 billion of sales for the trailing 12 months was close to its revenue three years ago. This was mainly because it closed stores.

This quarter, Petco reported a rather uninspiring 2.4% year-on-year revenue decline to $1.52 billion of revenue, in line with Wall Street’s estimates. Company management is currently guiding for flat sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products will spur better top-line performance, it is still below the sector average.

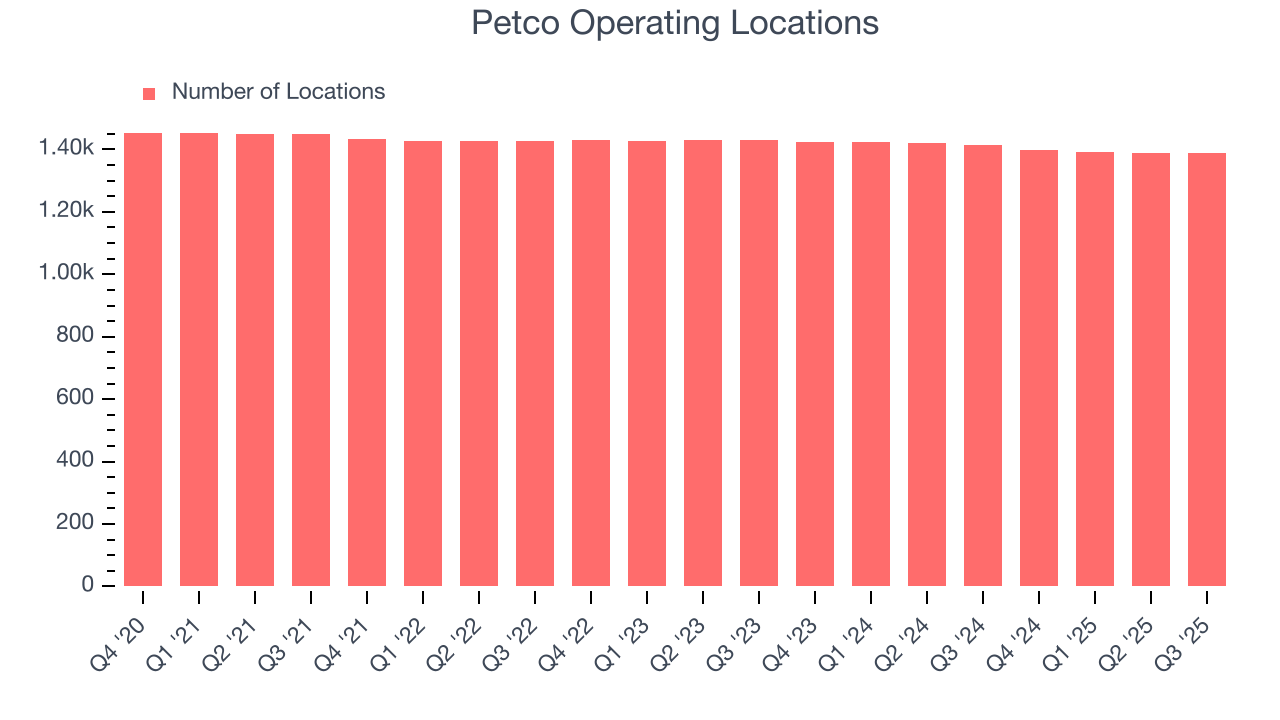

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Over the last two years, Petco has generally closed its stores, averaging 1.4% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Note that Petco reports its store count intermittently, so some data points are missing in the chart below.

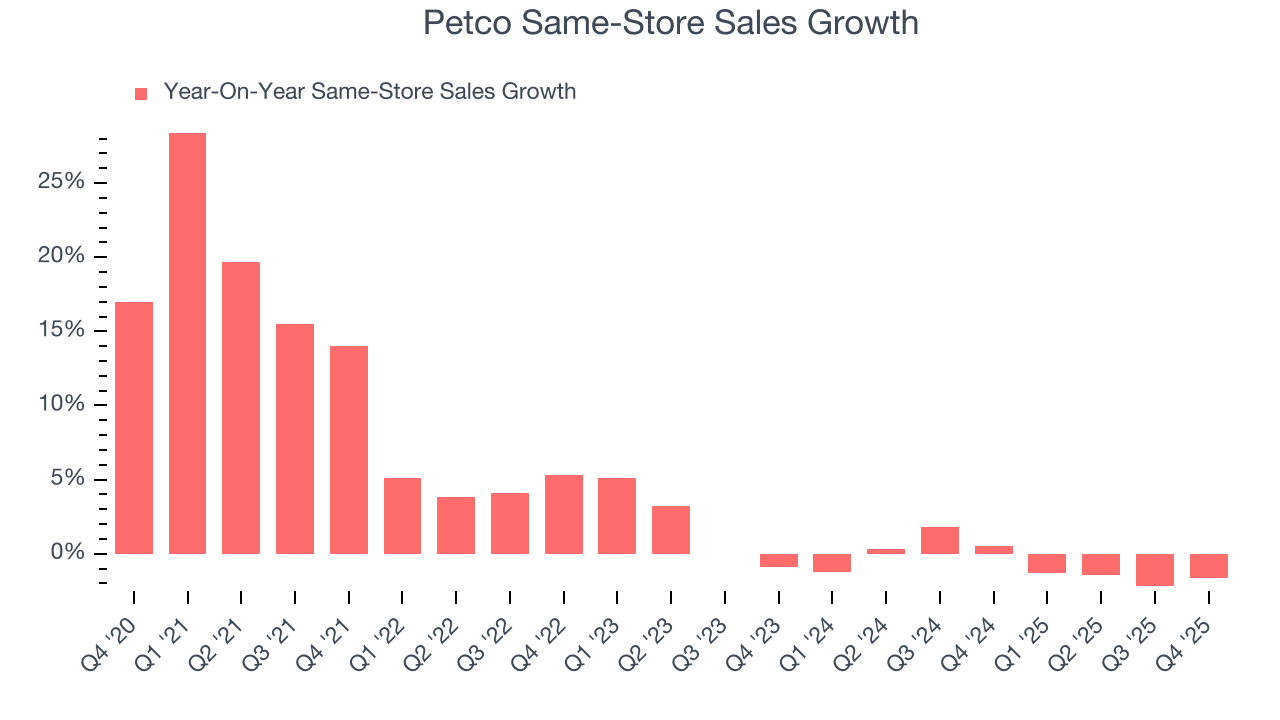

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Petco’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Petco is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Petco’s same-store sales fell by 1.6% year on year. This performance was more or less in line with its historical levels.

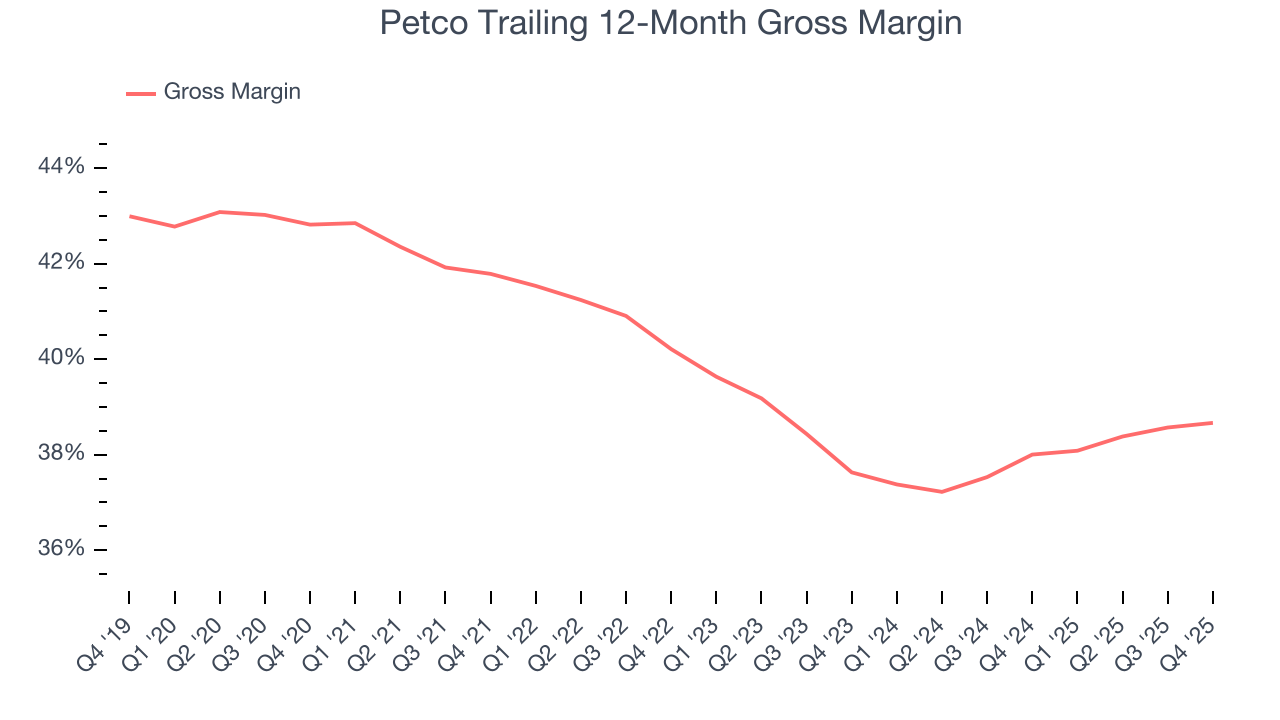

7. Gross Margin & Pricing Power

Petco’s gross margin is slightly below the average retailer, giving it less room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged a 38.3% gross margin over the last two years. Said differently, Petco had to pay a chunky $61.67 to its suppliers for every $100 in revenue.

In Q4, Petco produced a 38.3% gross profit margin, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

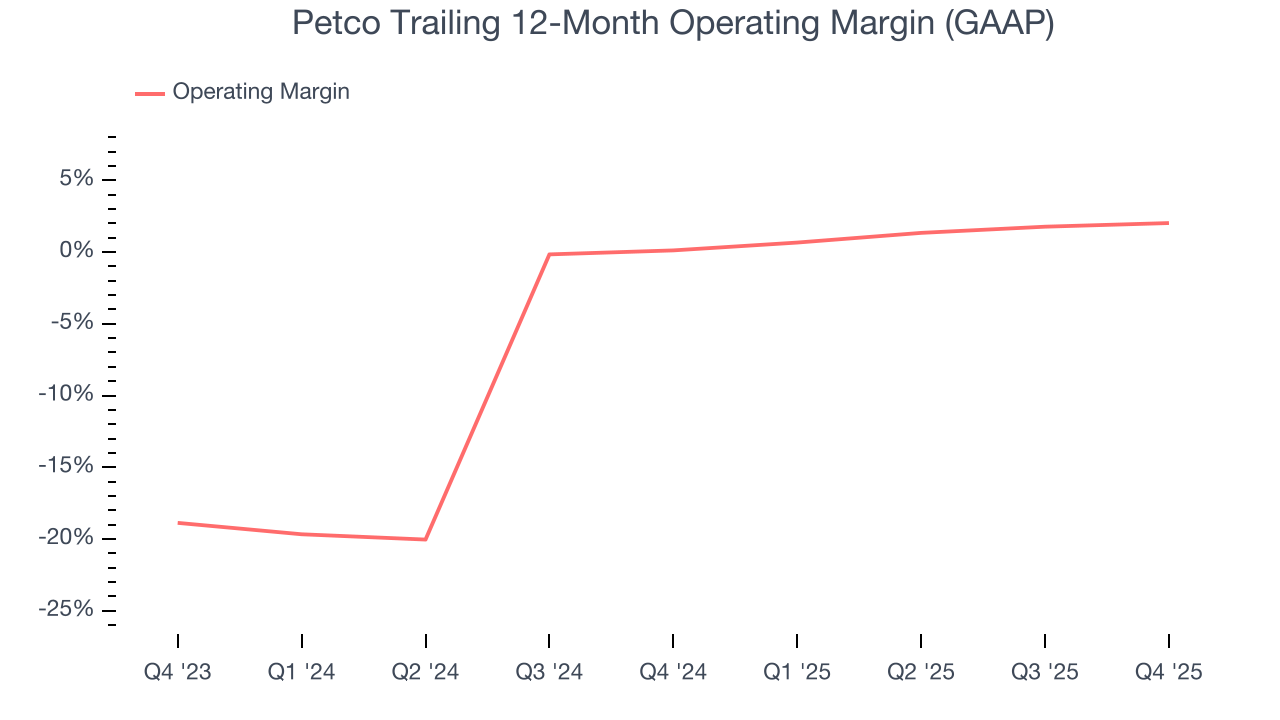

8. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Petco was profitable over the last two years but held back by its large cost base. Its average operating margin of 1.1% was weak for a consumer retail business. This result isn’t too surprising given its low gross margin as a starting point.

On the plus side, Petco’s operating margin rose by 1.9 percentage points over the last year.

This quarter, Petco generated an operating margin profit margin of 2.1%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

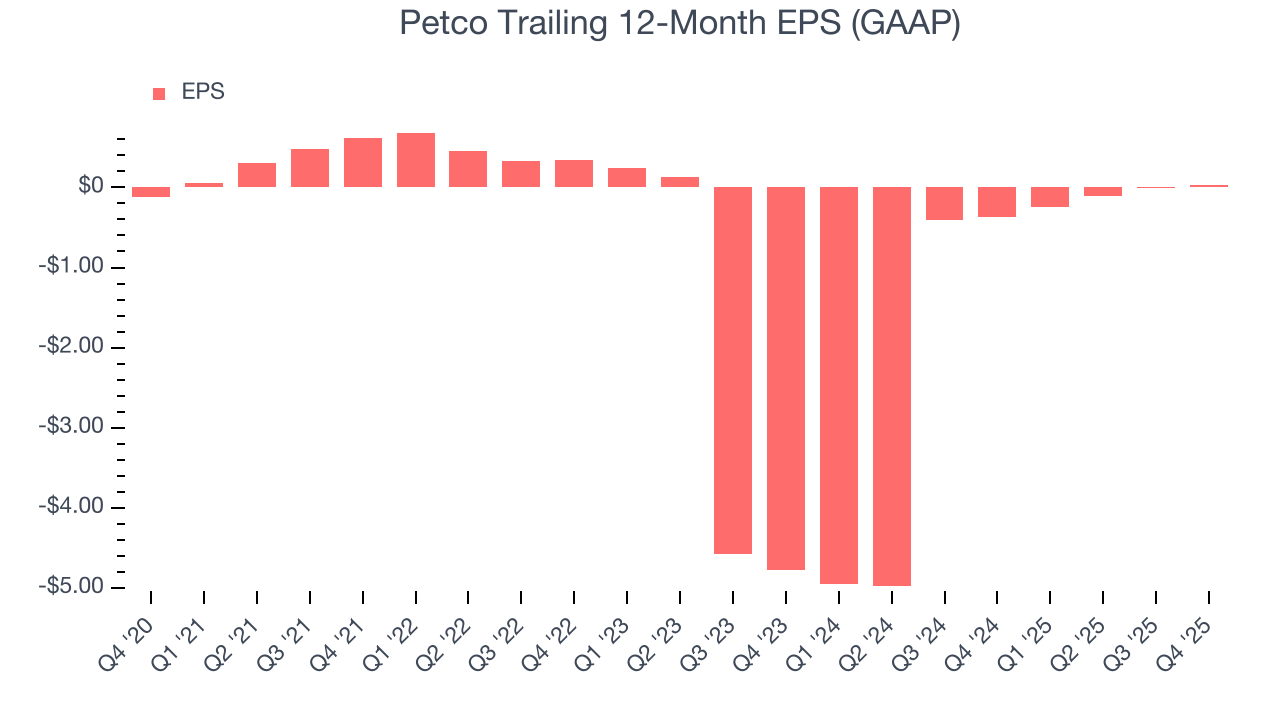

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Petco, its EPS declined by 55.9% annually over the last three years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

In Q4, Petco reported EPS of negative $0.01, up from negative $0.05 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Petco’s full-year EPS of $0.03 to grow 289%.

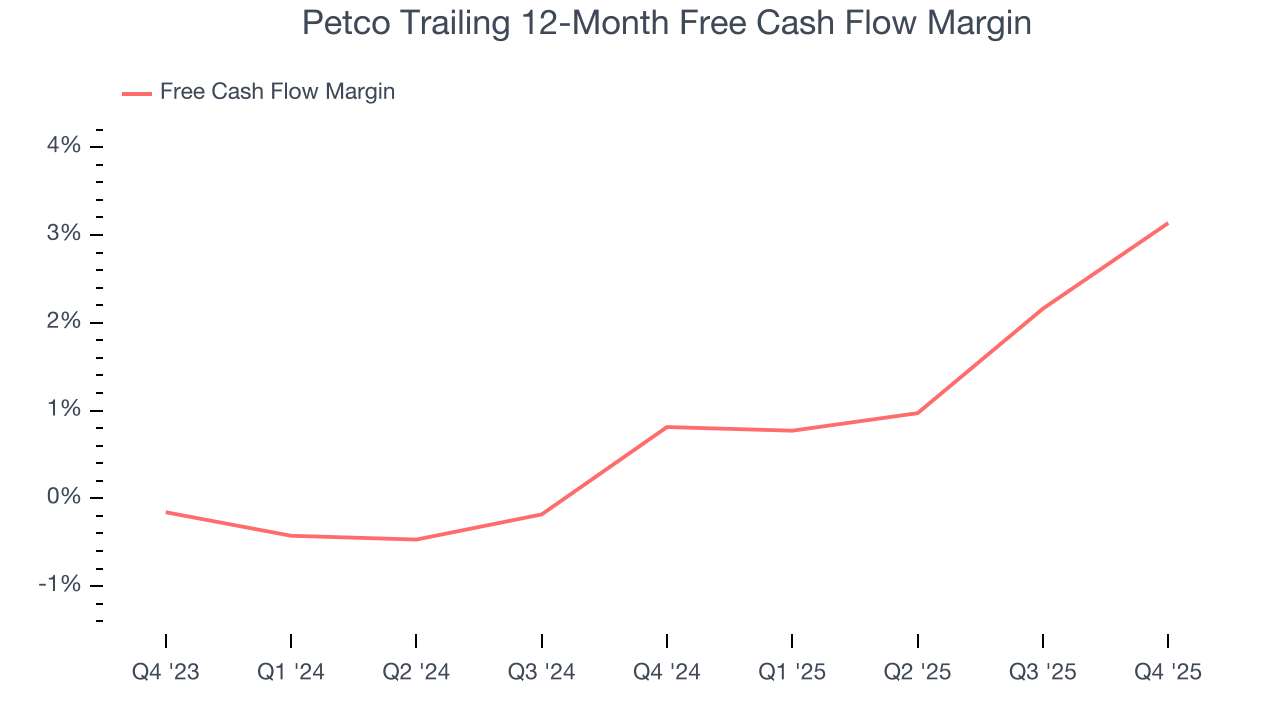

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Petco has shown mediocre cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 2%, below what we’d expect for a consumer retail business.

Taking a step back, an encouraging sign is that Petco’s margin expanded by 2.3 percentage points over the last year. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Petco’s free cash flow clocked in at $116.4 million in Q4, equivalent to a 7.7% margin. This result was good as its margin was 3.9 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Petco’s five-year average ROIC was negative 3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

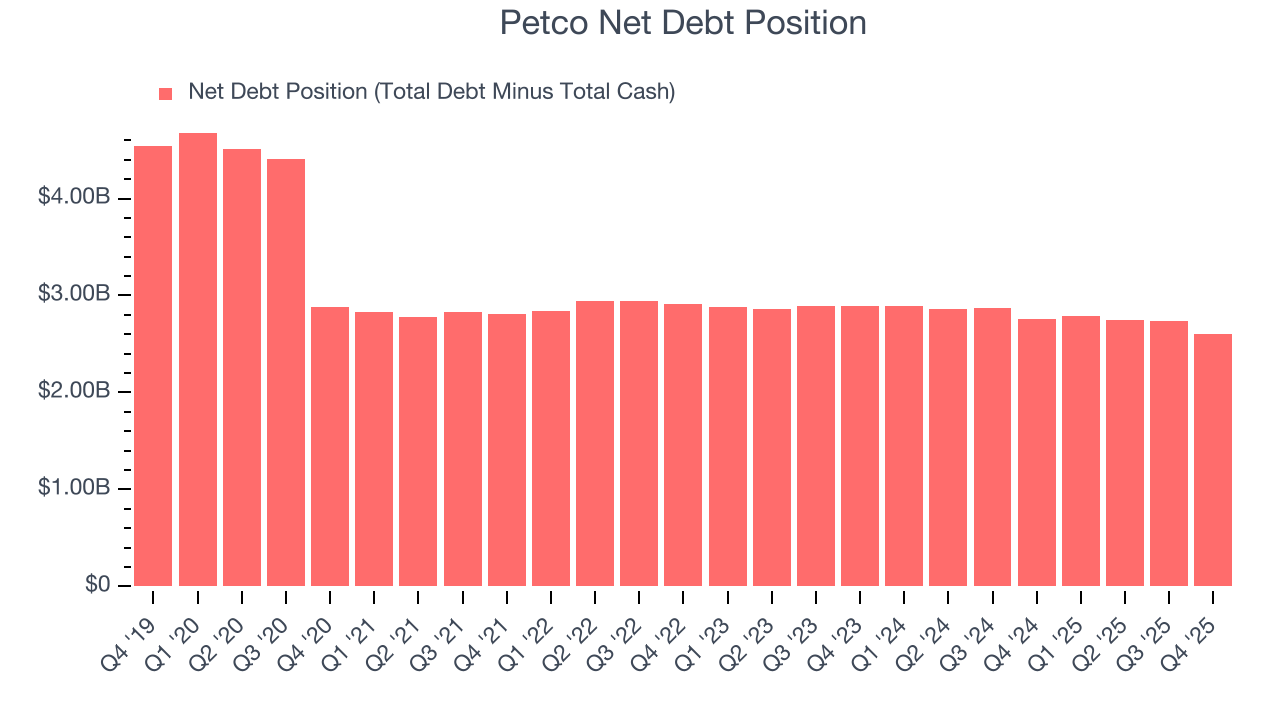

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Petco’s $2.86 billion of debt exceeds the $256.7 million of cash on its balance sheet. Furthermore, its 6× net-debt-to-EBITDA ratio (based on its EBITDA of $408.2 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Petco could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Petco can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

13. Key Takeaways from Petco’s Q4 Results

We were impressed by how significantly Petco blew past analysts’ EBITDA expectations this quarter. We were also glad its EBITDA guidance for next quarter exceeded Wall Street’s estimates. On the other hand, its EPS was in line. Overall, this print had some key positives. The stock traded up 14.2% to $2.81 immediately after reporting.

14. Is Now The Time To Buy Petco?

Updated: March 15, 2026 at 10:49 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Petco falls short of our quality standards. For starters, its revenue has declined over the last three years, and analysts don’t see anything changing over the next 12 months. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Petco’s P/E ratio based on the next 12 months is 13.6x. This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $3.53 on the company (compared to the current share price of $3.61), implying they don’t see much short-term potential in Petco.