Church & Dwight (CHD)

Church & Dwight doesn’t impress us. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Church & Dwight Is Not Exciting

Best known for its Arm & Hammer baking soda, Church & Dwight (NYSE:CHD) is a household and personal care products company with a vast portfolio that spans laundry detergent to toothbrushes to hair removal creams.

- Absence of organic revenue growth over the past two years suggests it may have to lean into acquisitions to drive its expansion

- Estimated sales growth of 2% for the next 12 months implies demand will slow from its three-year trend

- A positive is that its robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders, and its rising cash conversion increases its margin of safety

Church & Dwight is in the doghouse. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Church & Dwight

Church & Dwight is trading at $95.43 per share, or 24.7x forward P/E. Not only does Church & Dwight trade at a premium to companies in the consumer staples space, but this multiple is also high for its top-line growth.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Church & Dwight (CHD) Research Report: Q4 CY2025 Update

Household products company Church & Dwight (NYSE:CHD) met Wall Streets revenue expectations in Q4 CY2025, with sales up 3.9% year on year to $1.64 billion. The company expects next quarter’s revenue to be around $1.51 billion, close to analysts’ estimates. Its non-GAAP profit of $0.86 per share was 3% above analysts’ consensus estimates.

Church & Dwight (CHD) Q4 CY2025 Highlights:

- Revenue: $1.64 billion vs analyst estimates of $1.64 billion (3.9% year-on-year growth, in line)

- Adjusted EPS: $0.86 vs analyst estimates of $0.83 (3% beat)

- Adjusted EBITDA: $345.6 million vs analyst estimates of $341.9 million (21% margin, 1.1% beat)

- Revenue Guidance for Q1 CY2026 is $1.51 billion at the midpoint, roughly in line with what analysts were expecting

- Adjusted EPS guidance for Q1 CY2026 is $0.92 at the midpoint, below analyst estimates of $0.96

- Operating Margin: 16.2%, in line with the same quarter last year

- Free Cash Flow Margin: 18.7%, up from 15% in the same quarter last year

- Organic Revenue was flat year on year (miss)

- Market Capitalization: $22.08 billion

Company Overview

Best known for its Arm & Hammer baking soda, Church & Dwight (NYSE:CHD) is a household and personal care products company with a vast portfolio that spans laundry detergent to toothbrushes to hair removal creams.

The company traces its history back to 1846, when the brother-in-law founders, John Dwight and Austin Church, started a small business in a New York City tenement. From humble beginnings selling bicarbonate of soda (baking soda), Church & Dwight has grown into a diversified powerhouse with brands such as OxiClean (laundry detergent), Spinbrush (toothbrushes), Nair (hair removal), Trojan (condoms), Vitafusion (vitamins), and many others. As mentioned, Arm & Hammer is highly recognized and versatile, used for baking, cleaning, and deodorizing.

Church & Dwight primarily targets middle-income consumers. These customers are looking for trusted brands since the products will be used on themselves, their family members, and in their own homes. They also want cost-effective products, although many are willing to pay a reasonable premium to buy established brands rather than lesser-known or private-label brands.

It’s not hard to find Church & Dwight’s products in stores. Traditional brick-and-mortar retailers such as supermarkets, mass merchants, drug stores, and specialty stores are the most common sellers of the company’s products. Given Church & Dwight’s scale and traffic-driving brands, the company often has prominent or advantaged placement on retailer shelves.

4. Household Products

Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options. These trends can be double-edged swords that benefit companies who innovate quickly to take advantage of them and hurt companies that don't invest enough to meet consumers where they want to be with regards to trends.

Competitors that offer a wide range of household and personal care products include Proctor & Gamble (NYSE:PG), Unilever (LSE:ULVR), and Colgate-Palmolive (NYSE:CL).

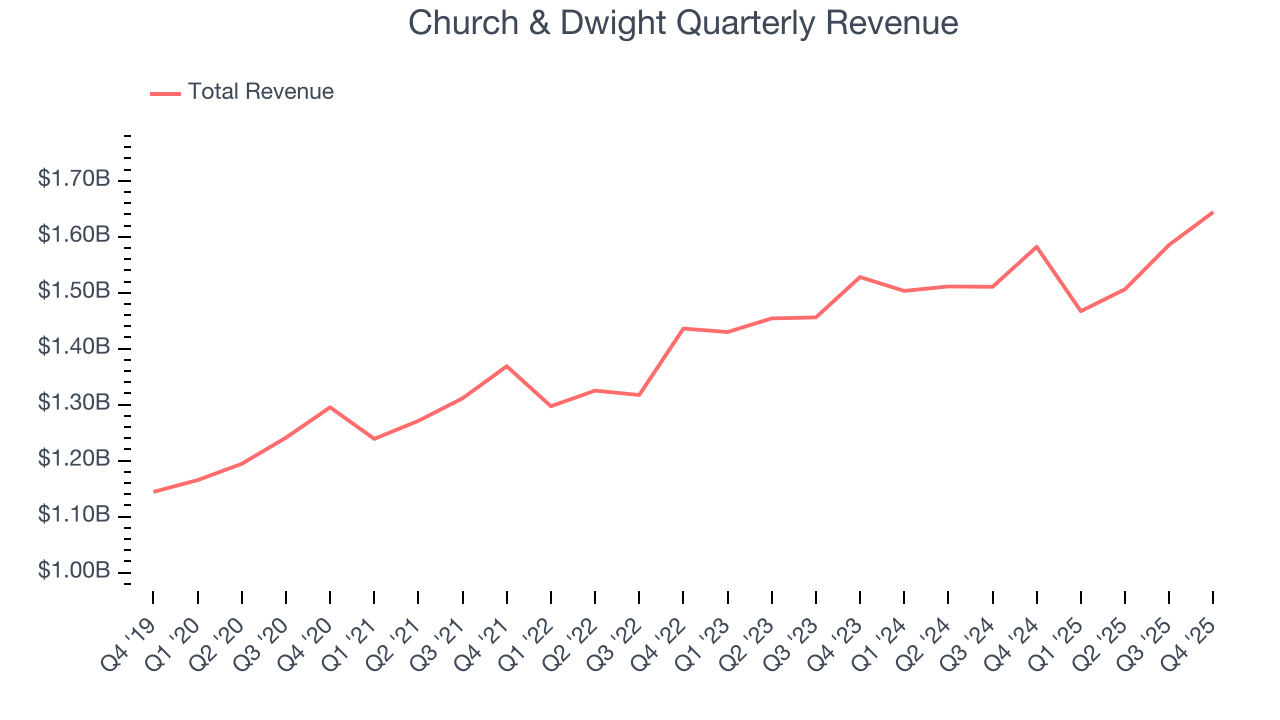

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $6.20 billion in revenue over the past 12 months, Church & Dwight carries some recognizable products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Church & Dwight’s sales grew at a tepid 4.9% compounded annual growth rate over the last three years, but to its credit, consumers bought more of its products.

This quarter, Church & Dwight grew its revenue by 3.9% year on year, and its $1.64 billion of revenue was in line with Wall Street’s estimates. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2% over the next 12 months, a slight deceleration versus the last three years. This projection doesn't excite us and implies its products will see some demand headwinds.

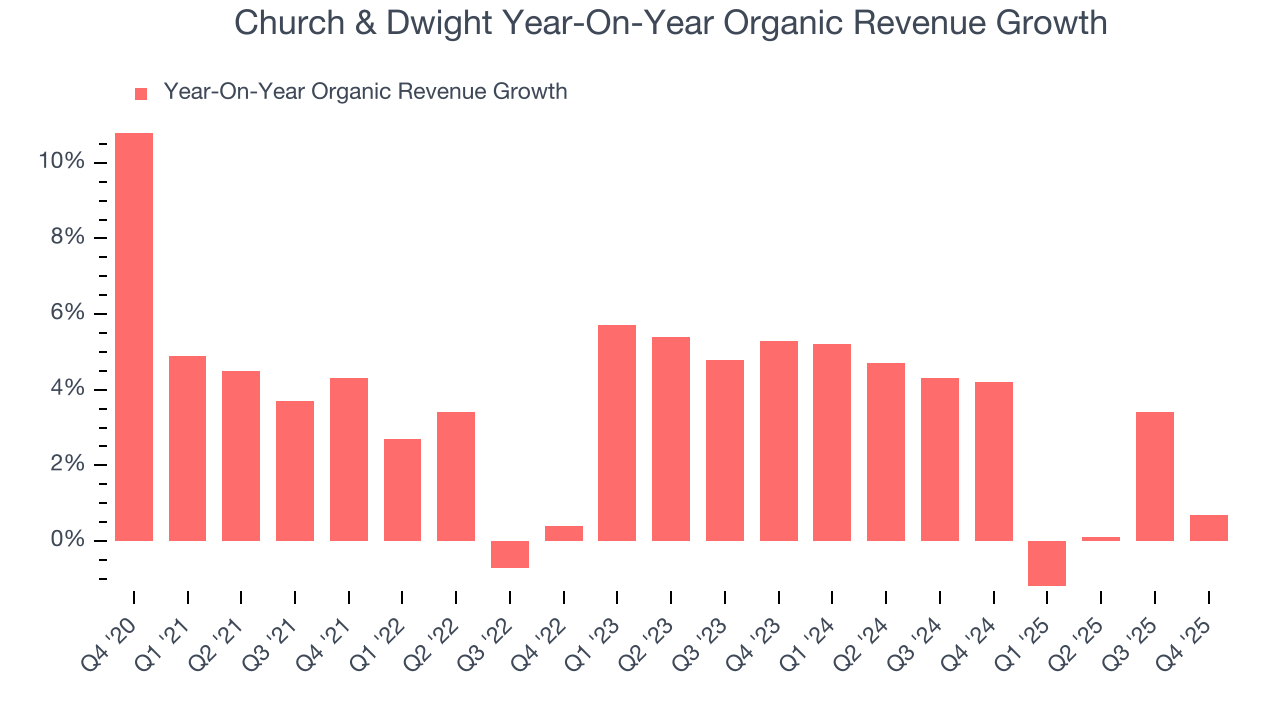

6. Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Church & Dwight’s products has generally risen over the last two years but lagged behind the broader sector. On average, the company’s organic sales have grown by 2.7% year on year.

In the latest quarter, Church & Dwight’s year on year organic sales were flat. This was a meaningful deceleration from its historical levels. We’ll be watching closely to see if Church & Dwight can reaccelerate growth.

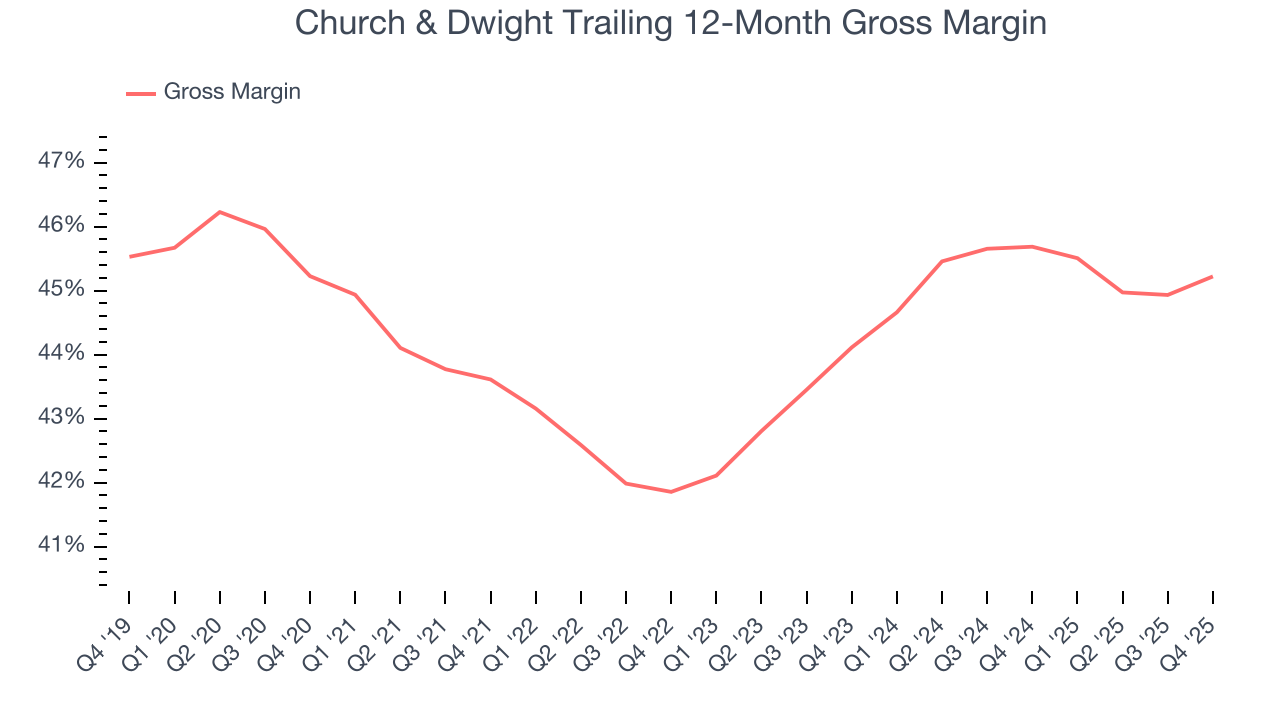

7. Gross Margin & Pricing Power

Church & Dwight has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 45.5% gross margin over the last two years. That means Church & Dwight only paid its suppliers $54.55 for every $100 in revenue.

This quarter, Church & Dwight’s gross profit margin was 45.8%, up 1.1 percentage points year on year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

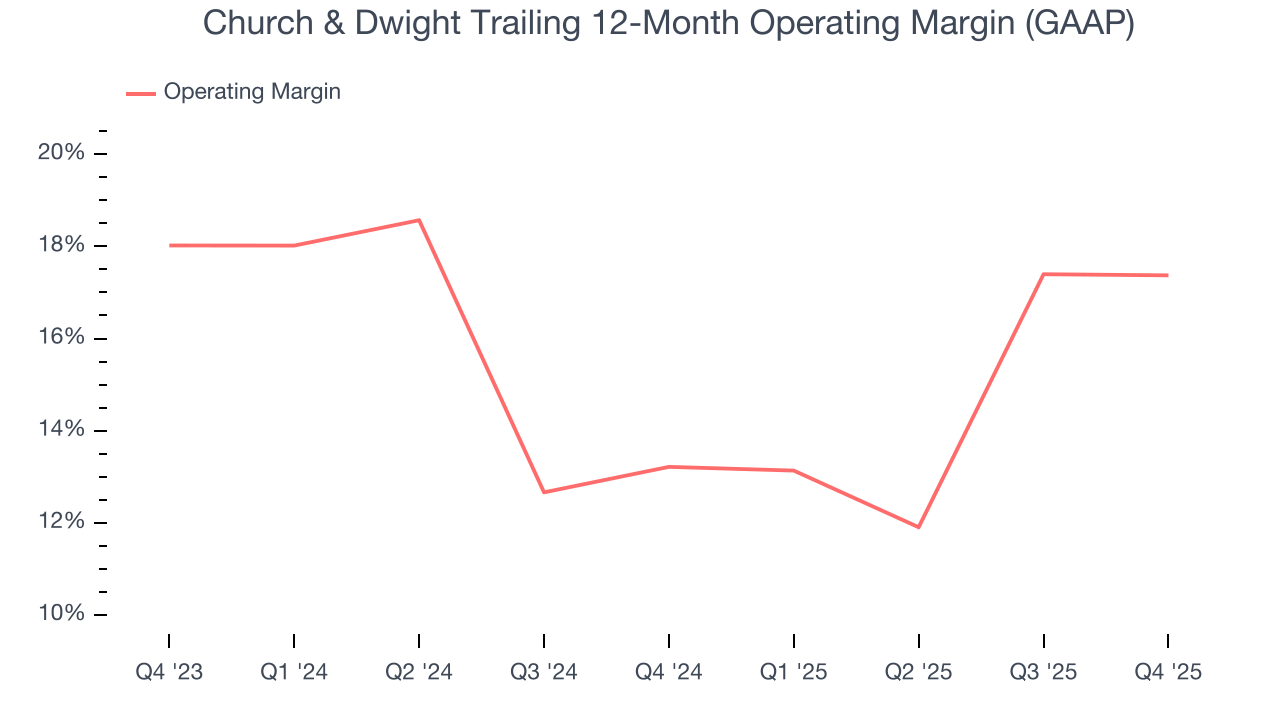

8. Operating Margin

Operating margin is an important measure of profitability accounting for key expenses such as marketing and advertising, IT systems, wages, and other administrative costs.

Church & Dwight has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer staples sector, boasting an average operating margin of 15.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Church & Dwight’s operating margin rose by 4.2 percentage points over the last year, as its sales growth gave it operating leverage.

In Q4, Church & Dwight generated an operating margin profit margin of 16.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

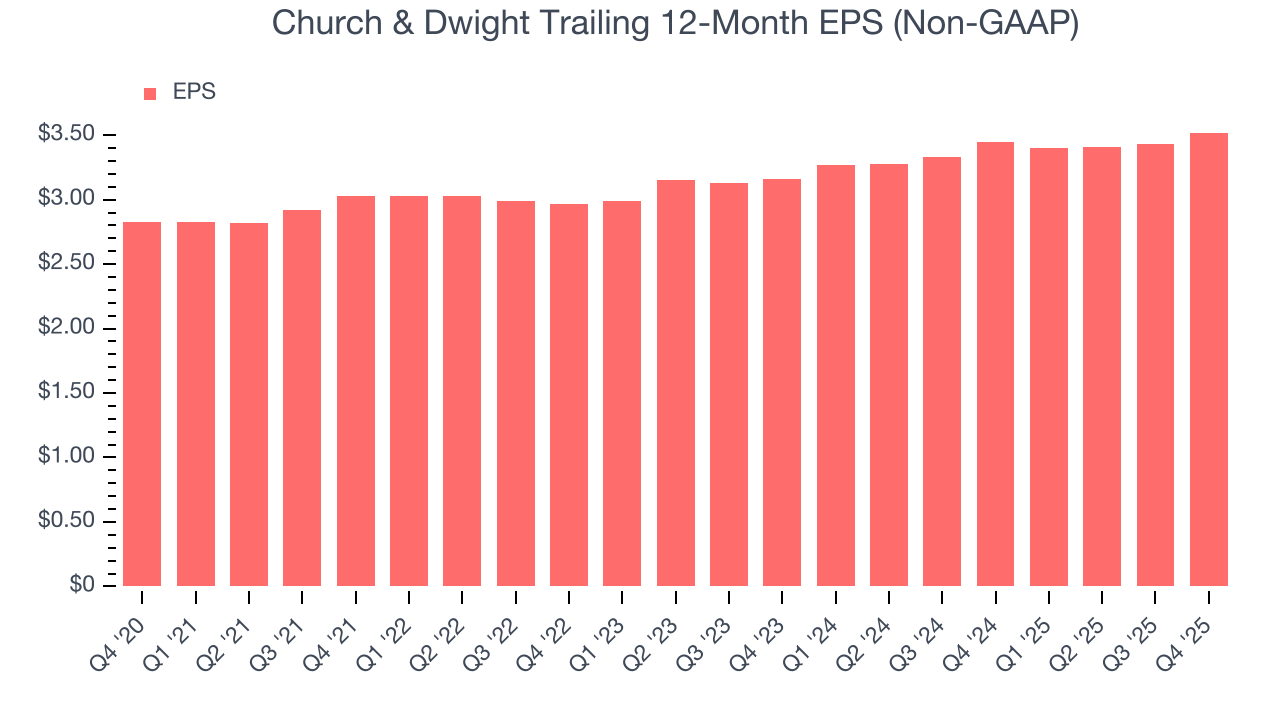

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Church & Dwight’s decent 5.8% annual EPS growth over the last three years aligns with its revenue performance. This tells us its incremental sales were profitable.

In Q4, Church & Dwight reported adjusted EPS of $0.86, up from $0.77 in the same quarter last year. This print beat analysts’ estimates by 3%. Over the next 12 months, Wall Street expects Church & Dwight’s full-year EPS of $3.52 to grow 5.7%.

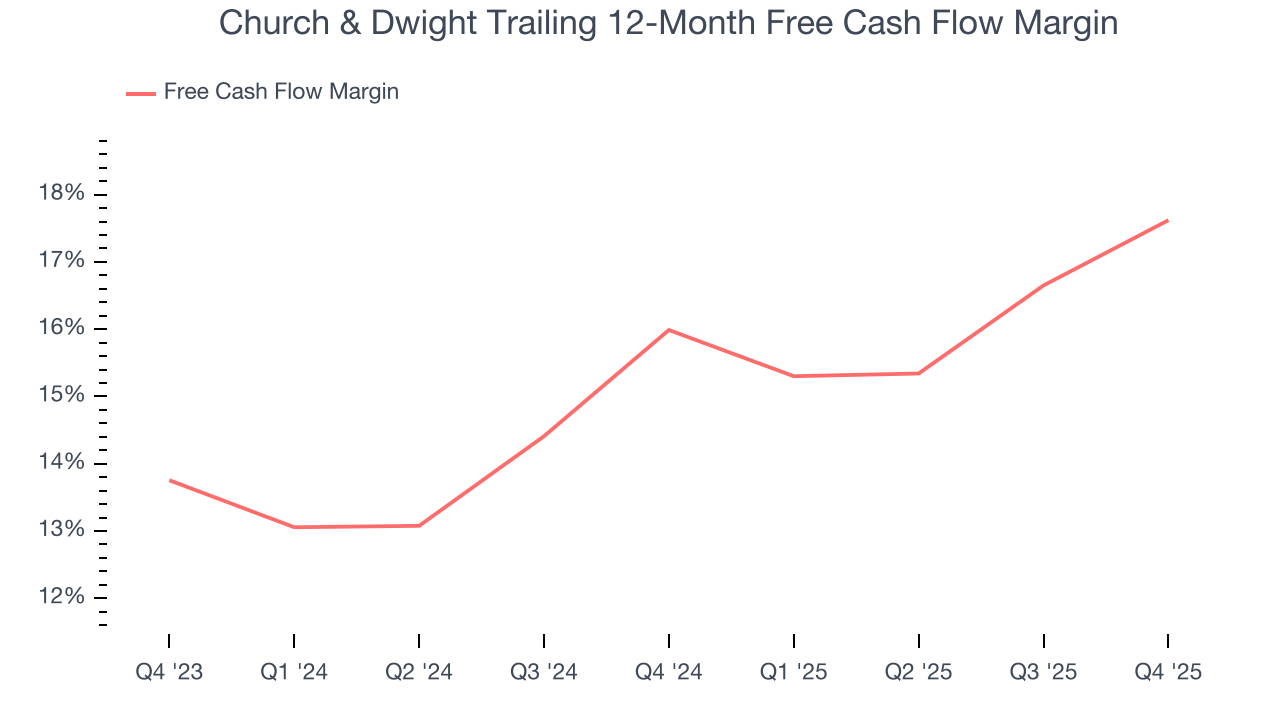

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Church & Dwight has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 16.8% over the last two years.

Taking a step back, we can see that Church & Dwight’s margin expanded by 1.6 percentage points over the last year. This is encouraging because it gives the company more optionality.

Church & Dwight’s free cash flow clocked in at $308.2 million in Q4, equivalent to a 18.7% margin. This result was good as its margin was 3.7 percentage points higher than in the same quarter last year, building on its favorable historical trend.

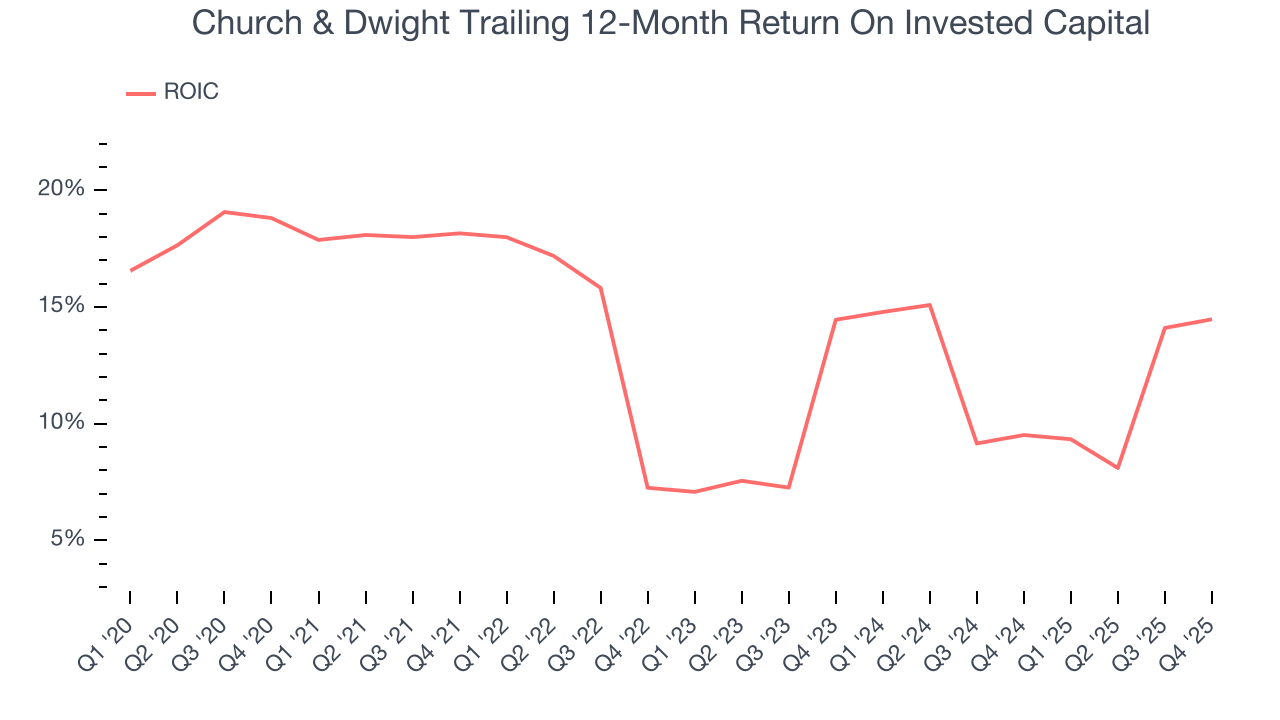

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Church & Dwight’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 12.8%, slightly better than typical consumer staples business.

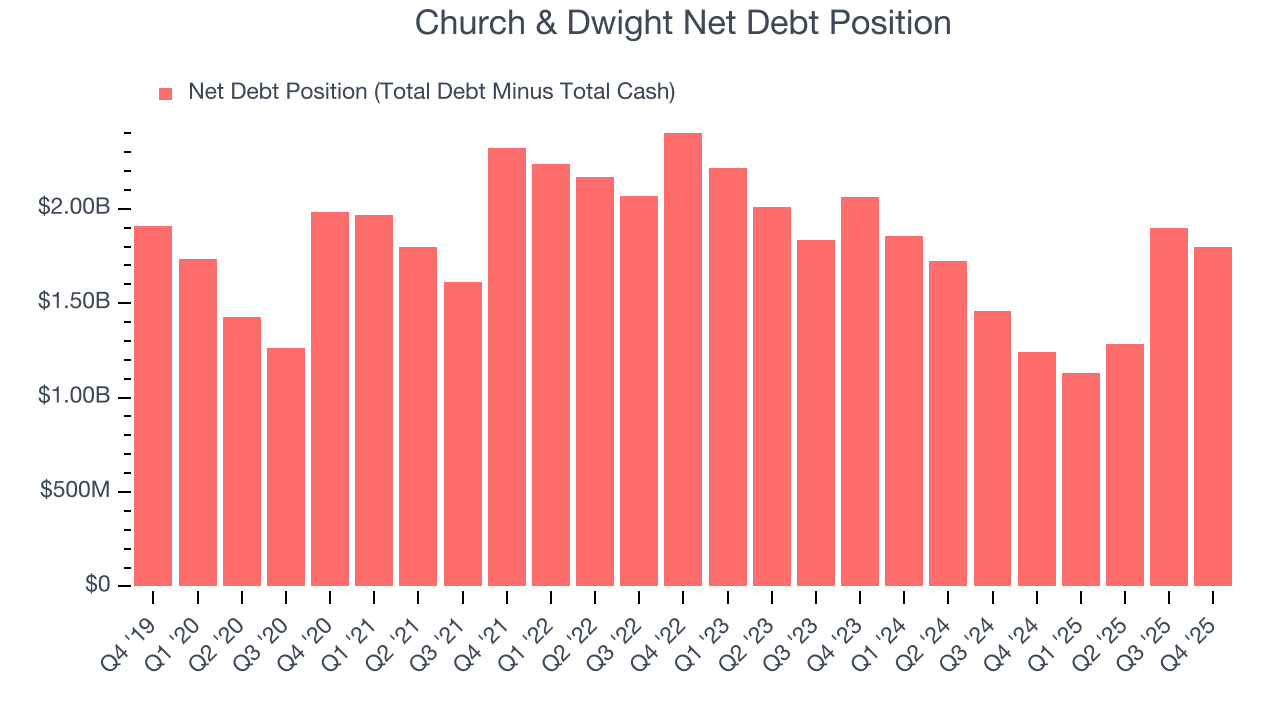

12. Balance Sheet Assessment

Church & Dwight reported $409 million of cash and $2.21 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.42 billion of EBITDA over the last 12 months, we view Church & Dwight’s 1.3× net-debt-to-EBITDA ratio as safe. We also see its $49.2 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Church & Dwight’s Q4 Results

It was encouraging to see Church & Dwight beat analysts’ gross margin expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its organic revenue slightly missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a mixed quarter. The stock traded up 3.2% to $94.89 immediately after reporting.

14. Is Now The Time To Buy Church & Dwight?

Updated: January 30, 2026 at 11:27 AM EST

When considering an investment in Church & Dwight, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Church & Dwight has a few positive attributes, but it doesn’t top our wishlist. Although its revenue growth was a little slower over the last three years and analysts expect growth to slow over the next 12 months, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. Be wary, however, as Church & Dwight’s projected EPS for the next year is lacking.

Church & Dwight’s P/E ratio based on the next 12 months is 24.7x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $96.05 on the company (compared to the current share price of $95.27).