Centrus Energy (LEU)

Centrus Energy faces an uphill battle. It not only barely generates profits but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why We Think Centrus Energy Will Underperform

Operating the only active U.S. facility licensed to produce high-assay low-enriched uranium (HALEU) for next-generation reactors, Centrus Energy (NYSE:LEU) supplies enriched uranium, the fissile component needed to produce fuel for nuclear power reactors.

- Smaller revenue base of $448.7 million means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- Expenses have increased as a percentage of revenue over the last five years as its EBITDA margin fell by 33.2 percentage points

- poor earning stability in the sector may keep investors up at night

Centrus Energy falls short of our quality standards. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Centrus Energy

Centrus Energy’s stock price of $213.99 implies a valuation ratio of 59.5x forward P/E. This valuation is extremely expensive, especially for the quality you get.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Centrus Energy (LEU) Research Report: Q4 CY2025 Update

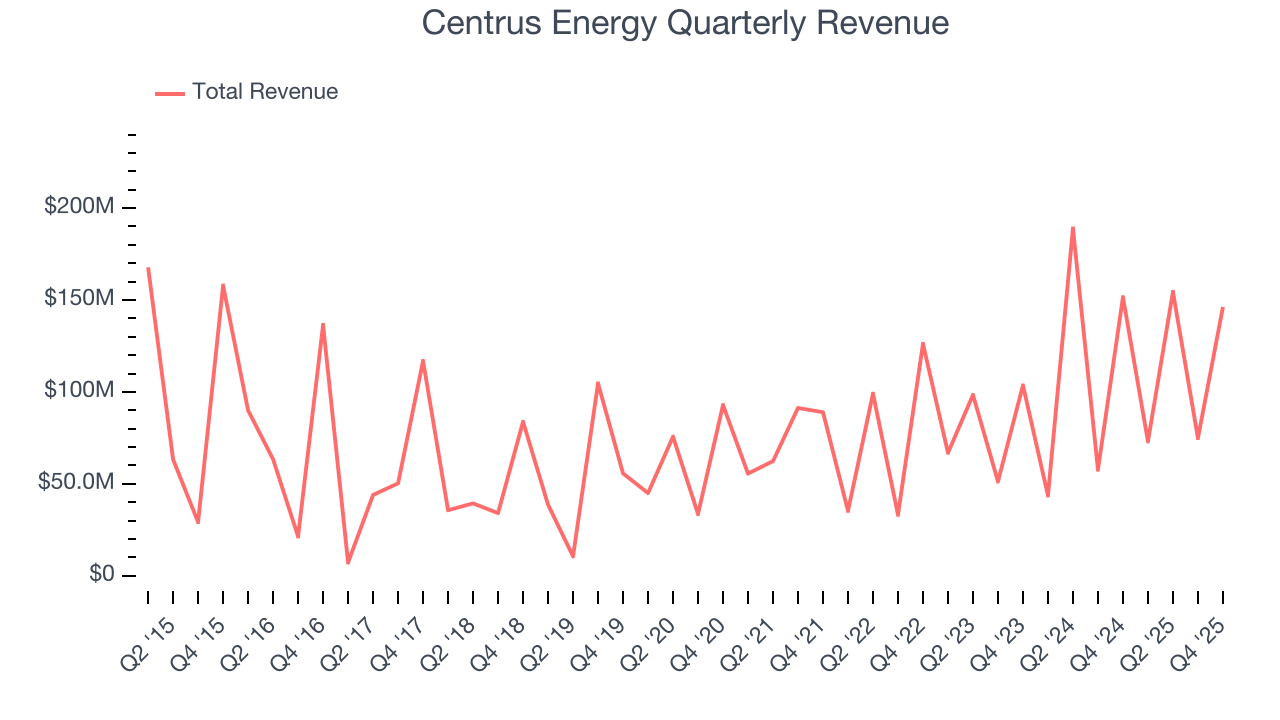

Nuclear fuel supplier Centrus Energy (NYSE:LEU) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 3.6% year on year to $146.2 million. Its non-GAAP profit of $0.79 per share was 51.4% below analysts’ consensus estimates.

Centrus Energy (LEU) Q4 CY2025 Highlights:

- Revenue: $146.2 million vs analyst estimates of $147 million (3.6% year-on-year decline, 0.5% miss)

- Adjusted EPS: $0.79 vs analyst expectations of $1.63 (51.4% miss)

- Adjusted EBITDA: $19.2 million vs analyst estimates of $34.55 million (13.1% margin, 44.4% miss)

- Operating Margin: 6.1%, down from 29.3% in the same quarter last year

- Free Cash Flow was -$58 million, down from $57.2 million in the same quarter last year

- Market Capitalization: $3.95 billion

Company Overview

Operating the only active U.S. facility licensed to produce high-assay low-enriched uranium (HALEU) for next-generation reactors, Centrus Energy (NYSE:LEU) supplies enriched uranium, the fissile component needed to produce fuel for nuclear power reactors.

The company operates through two segments. Its LEU (low-enriched uranium) segment, which generates the majority of revenue, sells enriched uranium primarily to utilities that operate commercial nuclear power plants worldwide. Natural uranium contains only 0.711% of the fissile isotope U-235, but most reactors require uranium enriched to concentrations up to 5% U-235 to sustain a nuclear reaction. The enrichment process is measured in Separative Work Units (SWU), which quantify the effort required to increase the U-235 concentration. While some customers purchase complete fuel packages from Centrus, most provide their own natural uranium feedstock and pay Centrus for the enrichment service, receiving back the enriched uranium ready for fuel fabrication.

Centrus sources its supply from a diverse network, including inventory, long-term contracts with enrichment producers like Russia's TENEX and France's Orano, and spot market purchases. Its largest supplier is TENEX, with deliveries governed by a Russian Suspension Agreement that sets import quotas through 2028. For example, a utility planning to refuel a reactor might contract with Centrus years in advance, delivering natural uranium to the company, which then enriches it to the required specification and returns the low-enriched uranium for the utility to have fabricated into fuel assemblies.

The Technical Solutions segment focuses on advanced nuclear fuel production and engineering services for government and commercial customers. Under a contract with the Department of Energy (DOE), Centrus operates a cascade of centrifuges in Piketon, Ohio to produce HALEU—uranium enriched between 5% and 20% U-235—which is required for many advanced reactor designs under development. The facility began production in October 2023, making Centrus the only company actively enriching uranium to HALEU levels in the United States. This segment also leverages the company's manufacturing capabilities at its Oak Ridge, Tennessee facility to provide precision engineering and fabrication services for next-generation nuclear fuel projects.

4. Mixed or Offshore Upstream E&P

This category includes smaller or niche E&P companies operating in specialized basins, geographies, or resource types outside major classifications. These firms may target unconventional resources, frontier regions, or specific commodity niches. Tailwinds include potential for outsized returns from successful exploration, acquisition opportunities during industry downturns, and specialized expertise commanding premium valuations. Headwinds include higher operational and geological risks, limited scale reducing negotiating power and cost efficiencies, and constrained capital market access during challenging commodity environments. Regulatory risks and ESG concerns may disproportionately affect smaller operators with fewer resources for compliance.

Centrus Energy competes with government-owned enrichment producers including Orano (France), Rosatom/TENEX (Russia), Urenco (Netherlands, UK, and Germany), and China National Nuclear Corporation (China).

5. Revenue Scale

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. Centrus Energy’s $448.7 million of revenue in the last year is pretty small for the industry, suggesting the type of diversification that reduces operational risk.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Thankfully, Centrus Energy’s 12.7% annualized revenue growth over the last five years was decent. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Centrus Energy’s annualized revenue growth of 0.7% over the last ten years is below its five-year trend, but we still think the results were respectable.

This quarter, Centrus Energy missed Wall Street’s estimates and reported a rather uninspiring 3.6% year-on-year revenue decline, generating $146.2 million of revenue.

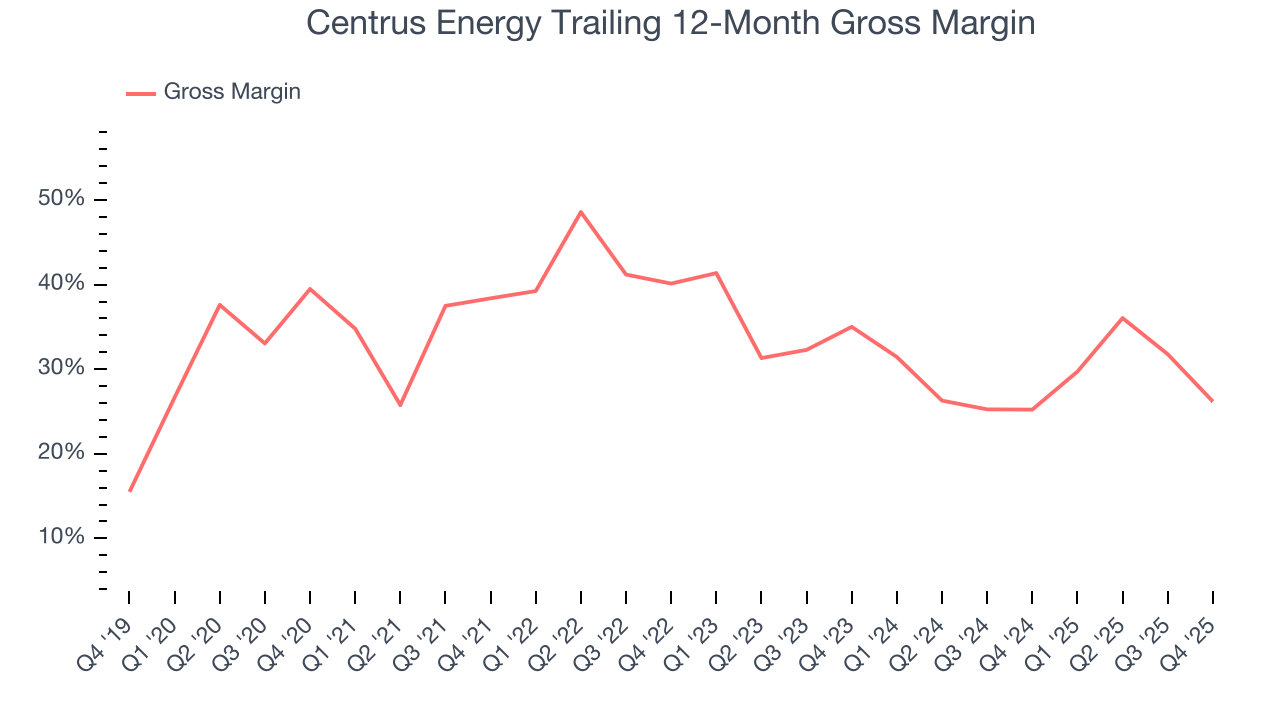

7. Gross Margin

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Centrus Energy, which averaged 31.8% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Centrus Energy produced a 23.9% gross profit margin in Q4, down 16.8 percentage points year on year.

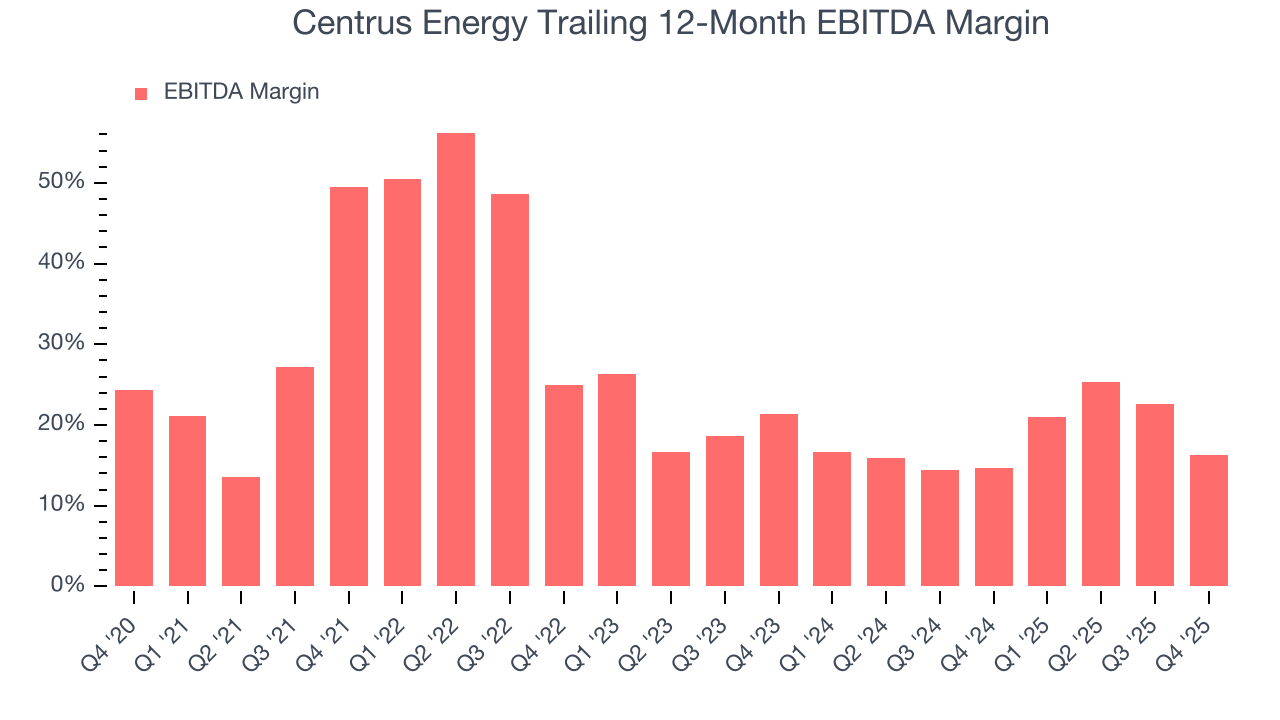

8. Adjusted EBITDA Margin

Centrus Energy was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 23.7% was weak for an upstream and integrated energy business.

Analyzing the trend in its profitability, Centrus Energy’s EBITDA margin decreased by 33.2 percentage points over the last year. Centrus Energy’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Centrus Energy generated an EBITDA margin profit margin of 13.1%, down 19.2 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

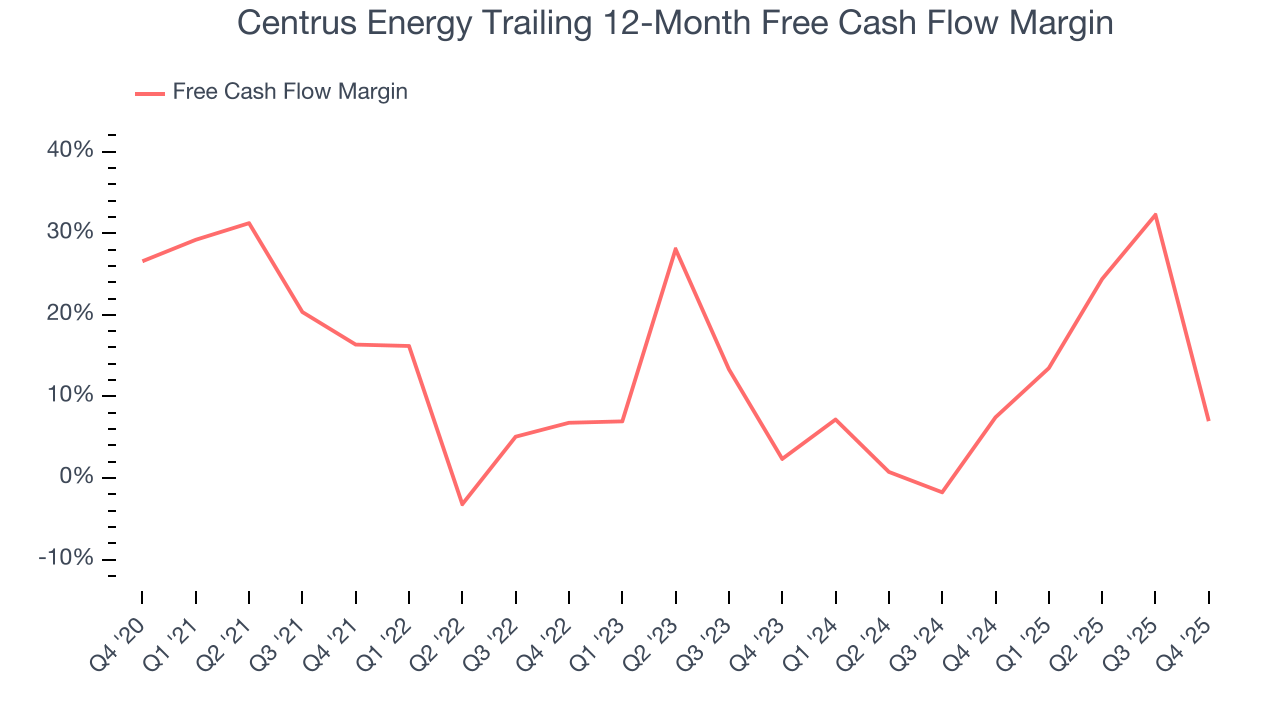

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Centrus Energy has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.8% over the last five years, slightly better than the broader energy upstream and integrated energy sector.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Centrus Energy’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 29.1 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Centrus Energy? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Centrus Energy burned through $58 million of cash in Q4, equivalent to a negative 39.7% margin. The company’s cash flow turned negative after being positive in the same quarter last year, suggesting its historical struggles have dragged on.

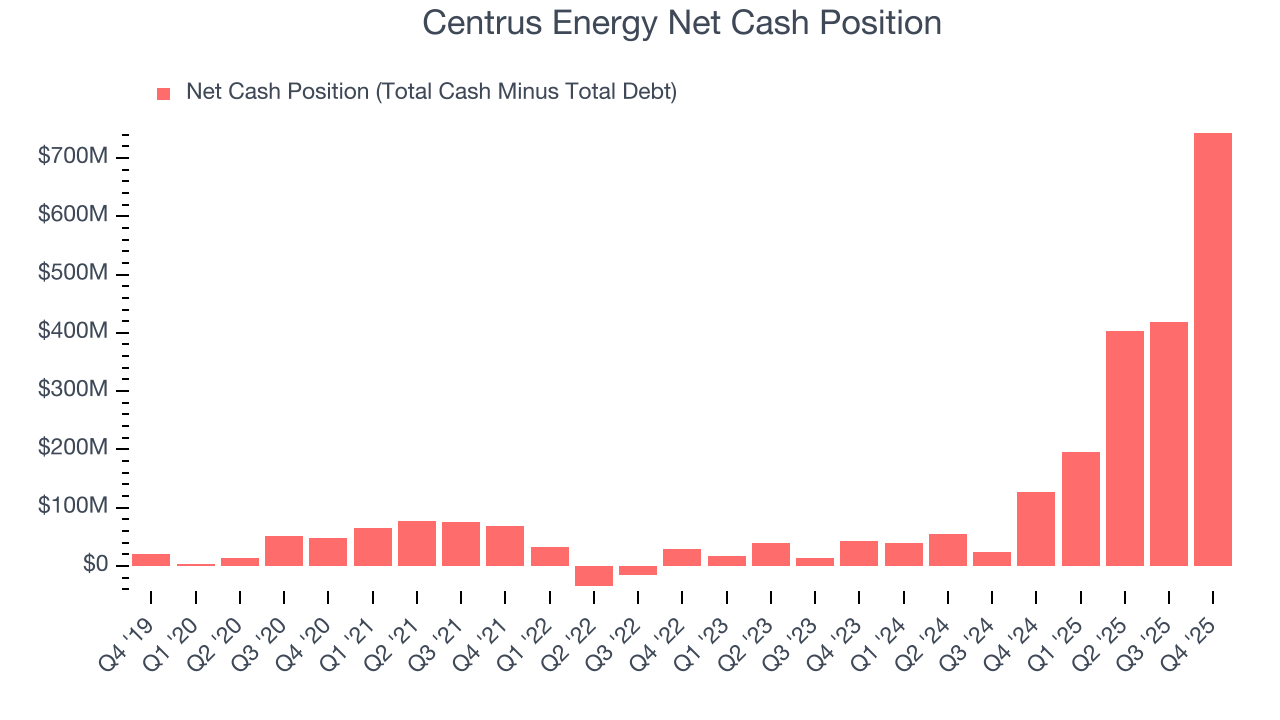

10. Balance Sheet Assessment

Companies with more cash than debt have lower bankruptcy risk.

Centrus Energy is a profitable, well-capitalized company with $1.96 billion of cash and $1.21 billion of debt on its balance sheet. This $743.5 million net cash position is 18.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Centrus Energy’s Q4 Results

We struggled to find many positives in these results. Its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $200.54 immediately after reporting.

12. Is Now The Time To Buy Centrus Energy?

Updated: March 18, 2026 at 1:15 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Centrus Energy.

Centrus Energy falls short of our quality standards. Although its revenue growth over the last five years was average for the sector, it’s expected to deteriorate over the next 12 months and its free cash flow volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow. On top of that, the company’s declining EBITDA margin shows the business has become less efficient.

Centrus Energy’s P/E ratio based on the next 12 months is 59.5x. This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $279.58 on the company (compared to the current share price of $213.99).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.