Movado (MOV)

Movado is in for a bumpy ride. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Movado Will Underperform

With its watches displayed in 20 museums around the world, Movado (NYSE:MOV) is a watchmaking company with a portfolio of watch brands and accessories.

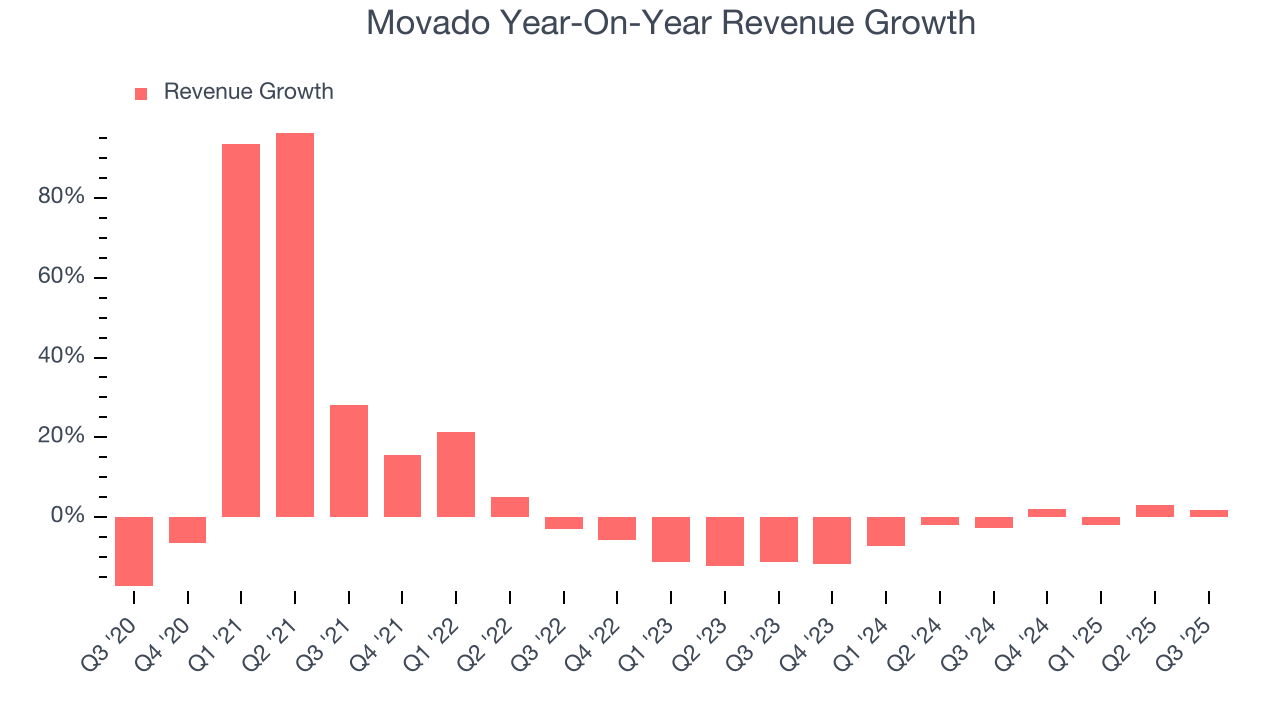

- 4.7% annual revenue growth over the last five years was slower than its consumer discretionary peers

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- Poor free cash flow generation means it has few chances to reinvest for growth, repurchase shares, or distribute capital

Movado fails to meet our quality criteria. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Movado

Movado’s stock price of $25.80 implies a valuation ratio of 15.1x forward P/E. This multiple is lower than most consumer discretionary companies, but for good reason.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Movado (MOV) Research Report: Q3 CY2025 Update

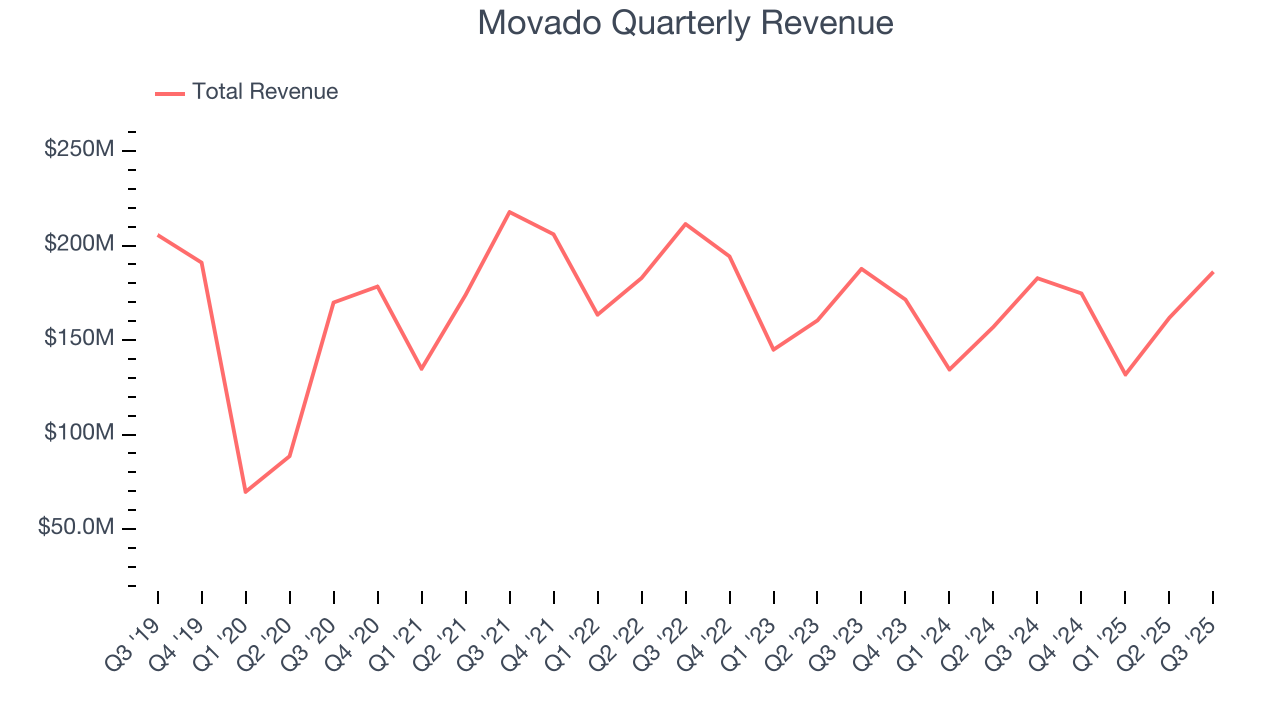

Luxury watch company Movado (NYSE:MOV) met Wall Streets revenue expectations in Q3 CY2025, with sales up 1.9% year on year to $186.1 million. Its GAAP profit of $0.42 per share was 26.8% below analysts’ consensus estimates.

Movado (MOV) Q3 CY2025 Highlights:

- Revenue: $186.1 million vs analyst estimates of $185.9 million (1.9% year-on-year growth, in line)

- EPS (GAAP): $0.42 vs analyst expectations of $0.57 (26.8% miss)

- Adjusted EBITDA: $14.11 million (7.6% margin, 10% year-on-year growth)

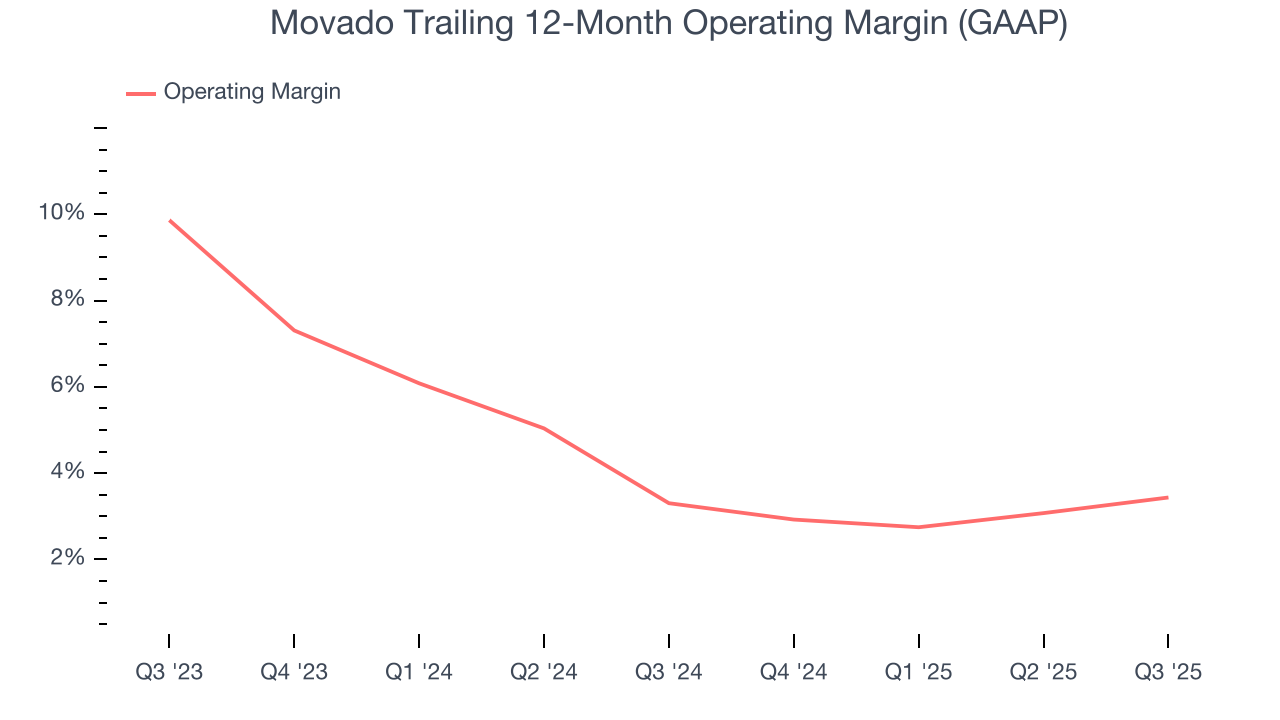

- Operating Margin: 6.3%, up from 5.1% in the same quarter last year

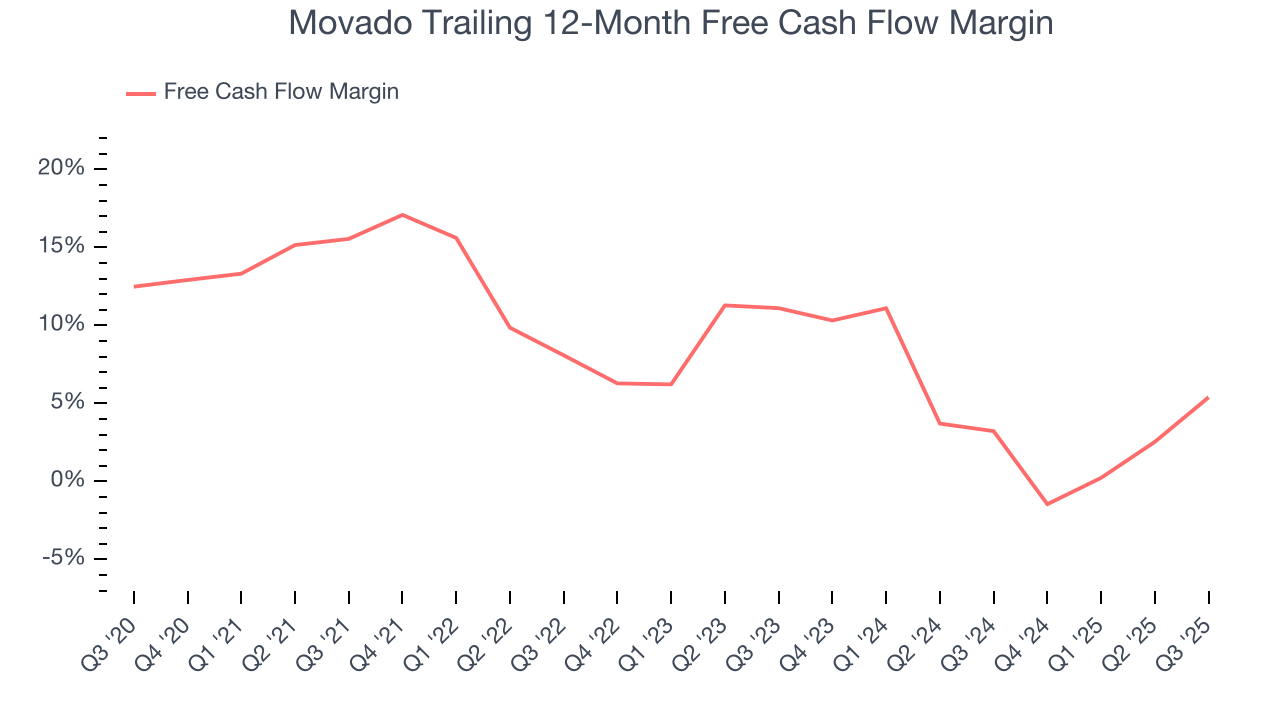

- Free Cash Flow was $11.6 million, up from -$7.17 million in the same quarter last year

- Market Capitalization: $430.6 million

Company Overview

With its watches displayed in 20 museums around the world, Movado (NYSE:MOV) is a watchmaking company with a portfolio of watch brands and accessories.

Movado’s signature Museum Watch is characterized by a singular dot at 12 o'clock, symbolizing the sun at high noon. This iconic design has gained mainstream popularity and is displayed in the Museum of Modern Art’s permanent collection in New York.

Movado’s portfolio extends beyond its flagship brand with labels including Ebel, Concord, Olivia Burton, and MVMT. This multi-brand strategy allows Movado to offer a broad spectrum of watch designs, from classic and luxury timepieces to contemporary and fashion-forward styles. This product breadth captures a wide customer base, from watch enthusiasts to casual wearers. Additionally, the company designs and distributes jewelry, eyewear, and other accessories, broadening its category offerings.

Movado's growth is dependent on the development of new watch designs and its approach to sales and marketing. The brand leverages digital platforms and e-commerce to adapt to changing consumer purchasing behaviors and the evolving retail landscape.

4. Apparel and Accessories

Thanks to social media and the internet, not only are styles changing more frequently today than in decades past but also consumers are shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some apparel and accessories companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Movado’s primary competitors include Omega (owned by Swatch SWX:UHR), Fossil Group (NASDAQ:FOSL), Citizen Watch (TYO:7762), TAG Heuer (owned by LVMH Moët Hennessy Louis Vuitton Euronext:MC), and private company Rolex.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Movado grew its sales at a weak 4.7% compounded annual growth rate. This was below our standard for the consumer discretionary sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Movado’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.4% annually.

This quarter, Movado grew its revenue by 1.9% year on year, and its $186.1 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

6. Operating Margin

Movado’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 3.4% over the last two years. This profitability was inadequate for a consumer discretionary business and caused by its suboptimal cost structure.

This quarter, Movado generated an operating margin profit margin of 6.3%, up 1.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Movado has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.3%, lousy for a consumer discretionary business.

Movado’s free cash flow clocked in at $11.6 million in Q3, equivalent to a 6.2% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

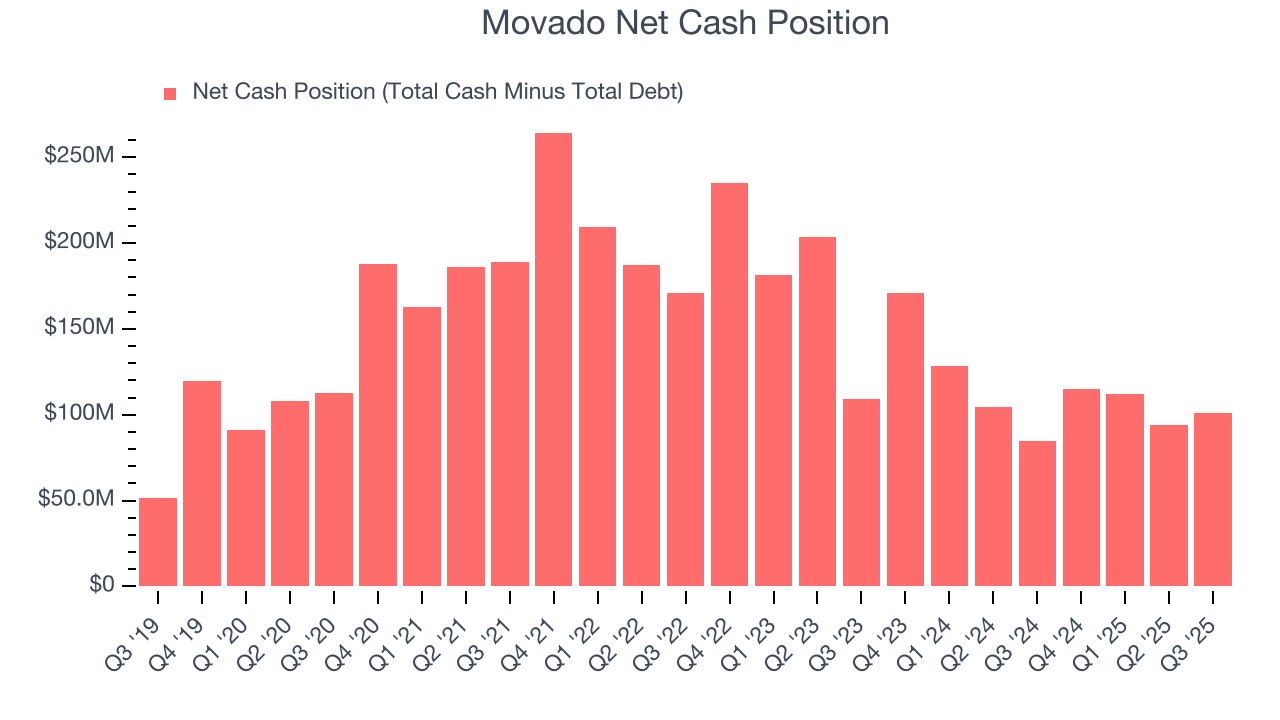

8. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Movado is a profitable, well-capitalized company with $183.9 million of cash and $83.07 million of debt on its balance sheet. This $100.8 million net cash position is 23.4% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

9. Key Takeaways from Movado’s Q3 Results

We struggled to find many resounding positives in these results. Revenue was just in line and EPS missed. Overall, this was a weaker quarter. The stock remained flat at $19.49 immediately after reporting.

10. Is Now The Time To Buy Movado?

Updated: February 20, 2026 at 10:10 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Movado falls short of our quality standards. While its projected EPS for the next year implies the company will start generating shareholder value, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities. On top of that, its low free cash flow margins give it little breathing room.

Movado’s P/E ratio based on the next 12 months is 15.1x. While this valuation is fair, the upside isn’t great compared to the potential downside. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $30.75 on the company (compared to the current share price of $25.80).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.