SiteOne (SITE)

SiteOne keeps us up at night. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think SiteOne Will Underperform

Known for distributing John Deere tractors and LESCO turf care products, SiteOne Landscape Supply (NYSE:SITE) provides landscaping products and services to professionals, including irrigation, lighting, and nursery supplies.

- Incremental sales over the last two years were much less profitable as its earnings per share fell by 3.9% annually while its revenue grew

- Absence of organic revenue growth over the past two years suggests it may have to lean into acquisitions to drive its expansion

- Estimated sales growth of 4.5% for the next 12 months is soft and implies weaker demand

SiteOne’s quality doesn’t meet our bar. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than SiteOne

SiteOne’s stock price of $127.65 implies a valuation ratio of 28.9x forward P/E. Not only is SiteOne’s multiple richer than most industrials peers, but it’s also expensive for its fundamentals.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. SiteOne (SITE) Research Report: Q4 CY2025 Update

Agriculture products company SiteOne Landscape Supply (NYSE:SITE) fell short of the market’s revenue expectations in Q4 CY2025 as sales rose 3.2% year on year to $1.05 billion. Its GAAP loss of $0.20 per share was 35% above analysts’ consensus estimates.

SiteOne (SITE) Q4 CY2025 Highlights:

- Revenue: $1.05 billion vs analyst estimates of $1.06 billion (3.2% year-on-year growth, 0.9% miss)

- EPS (GAAP): -$0.20 vs analyst estimates of -$0.31 (35% beat)

- Adjusted EBITDA: $37.6 million vs analyst estimates of $33.32 million (3.6% margin, 12.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $440 million at the midpoint, below analyst estimates of $453.3 million

- Operating Margin: -0.5%, up from -2.5% in the same quarter last year

- Free Cash Flow Margin: 14.4%, up from 10.8% in the same quarter last year

- Organic Revenue rose 2% year on year (miss)

- Market Capitalization: $6.63 billion

Company Overview

Known for distributing John Deere tractors and LESCO turf care products, SiteOne Landscape Supply (NYSE:SITE) provides landscaping products and services to professionals, including irrigation, lighting, and nursery supplies.

The company was formed in 2001 through the combination of John Deere Landscapes and other landscape supply companies. This gave the new combined company a national footprint rather than smaller regional ones. 2007 marked another milestone, with SiteOne acquiring LESCO, a leading supplier of lawn care, landscape, golf course and pest control products that boasted nearly 350 locations and doubles SiteOne’s distribution footprint.

Today SiteOne offers everything from synthetic turf to sprinkler systems to path lights. It aims to be a one-stop shop for landscape contractors, architects, and other industry professionals. For these customers, time is money, and the last thing they want to do is shop around, encounter out-of-stock positions, or wait for deliveries of product. SiteOne therefore promises broad inventory as well the ability to get these sometimes hard-to-transport products to project sites.

The primary revenue sources for SiteOne come from the sale of landscaping products and equipment. The company's business model focuses on direct sales through its network of branches and online platforms, providing accessibility for customers. While a smaller portion of revenue, SiteOne also offers services such as irrigation consultation to enhance water efficiency and facilitate optimal plant growth, for example.

4. Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

Competitors in the landscape and industrial products industry include Ferguson (NYSE:FERG), Fastenal (NASDAQ:FAST), and Lowe's (NYSE:LOW).

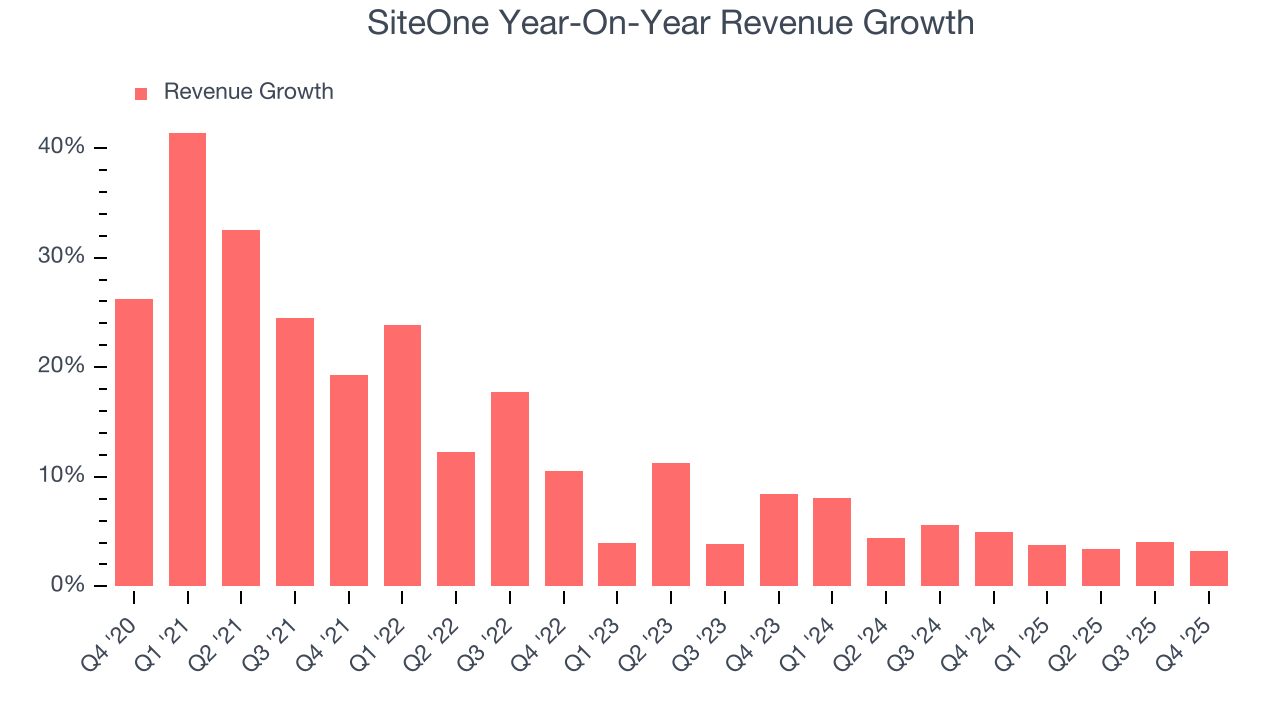

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, SiteOne’s sales grew at an impressive 11.7% compounded annual growth rate over the last five years. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. SiteOne’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.6% over the last two years was well below its five-year trend.

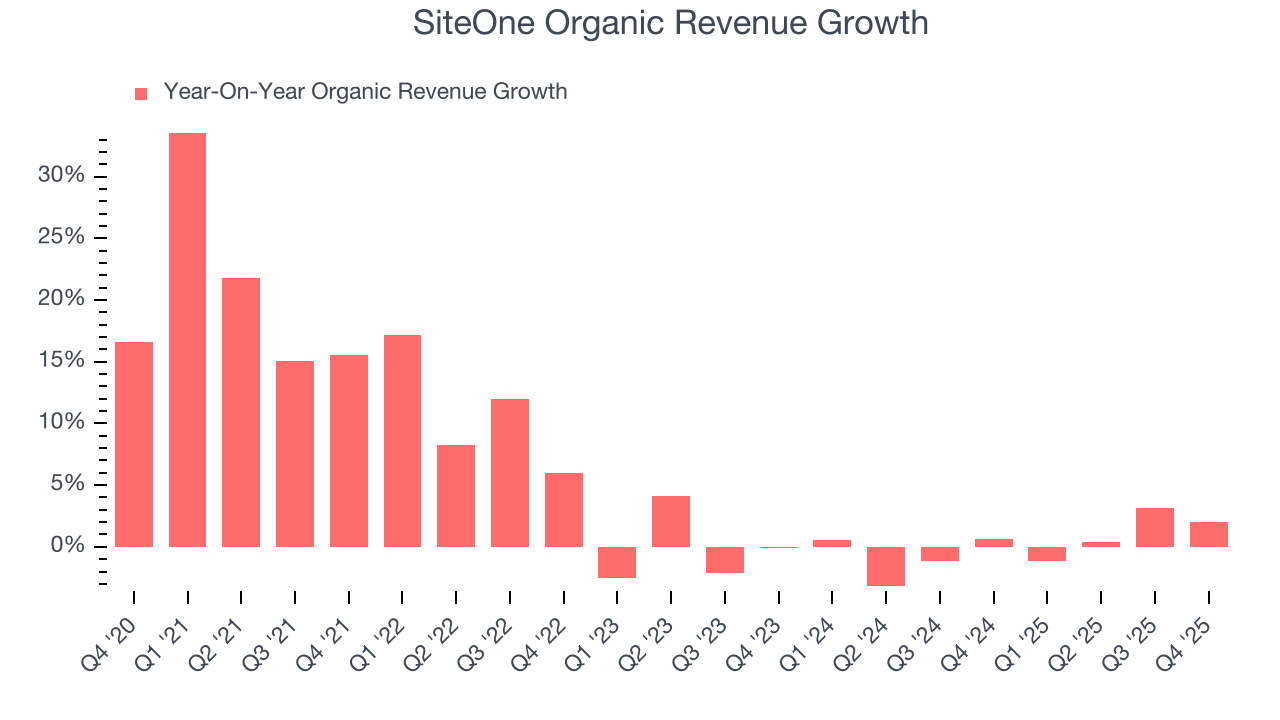

SiteOne also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, SiteOne’s organic revenue was flat. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, SiteOne’s revenue grew by 3.2% year on year to $1.05 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not catalyze better top-line performance yet.

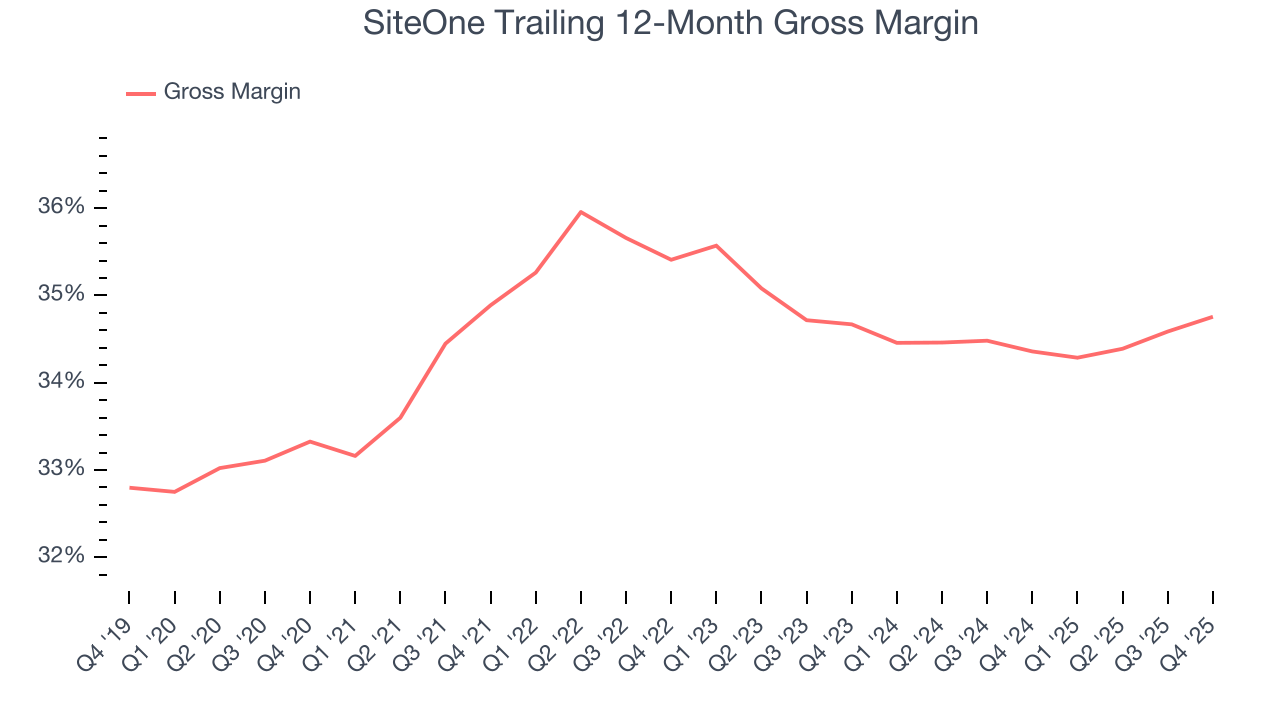

6. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate the company has pricing power or differentiated products, giving it a chance to generate higher operating profits.

SiteOne’s gross margin is good compared to other industrials businesses and signals it sells differentiated products, not commodities. As you can see below, it averaged an impressive 34.8% gross margin over the last five years. That means for every $100 in revenue, roughly $34.80 was left to spend on selling, marketing, R&D, and general administrative overhead.

This quarter, SiteOne’s gross profit margin was 34.1%, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

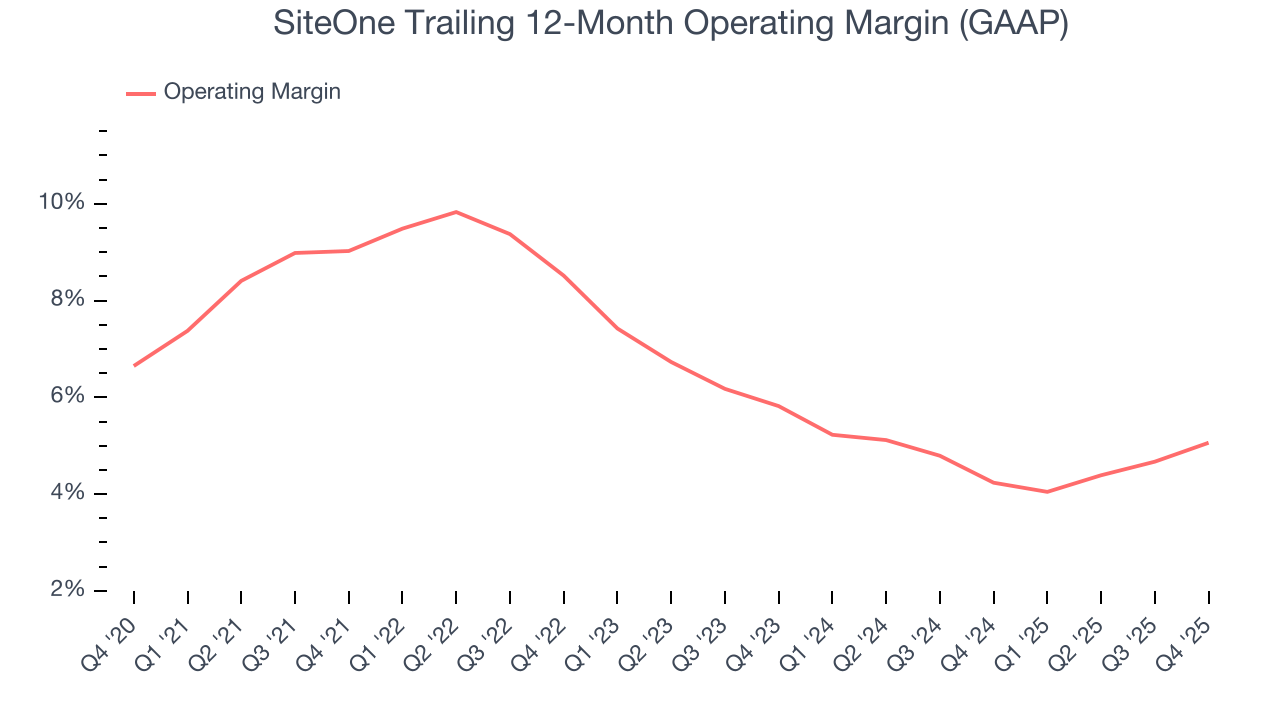

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

SiteOne was profitable over the last five years but held back by its large cost base. Its average operating margin of 6.4% was weak for an industrials business. This result is surprising given its high gross margin as a starting point.

Looking at the trend in its profitability, SiteOne’s operating margin decreased by 4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. SiteOne’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, SiteOne’s breakeven margin was -0.5%, up 2 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

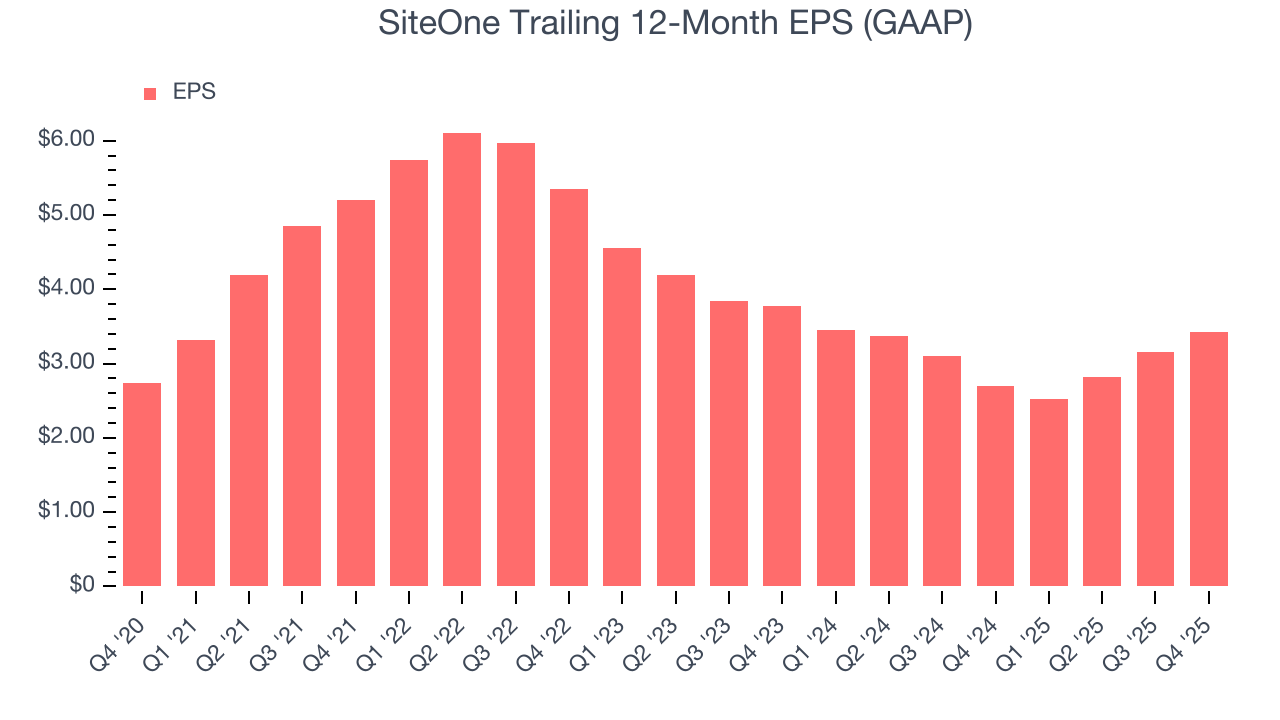

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

SiteOne’s EPS grew at an unimpressive 4.6% compounded annual growth rate over the last five years, lower than its 11.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into SiteOne’s earnings to better understand the drivers of its performance. As we mentioned earlier, SiteOne’s operating margin expanded this quarter but declined by 4 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For SiteOne, its two-year annual EPS declines of 4.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, SiteOne reported EPS of negative $0.20, up from negative $0.48 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects SiteOne’s full-year EPS of $3.43 to grow 20.9%.

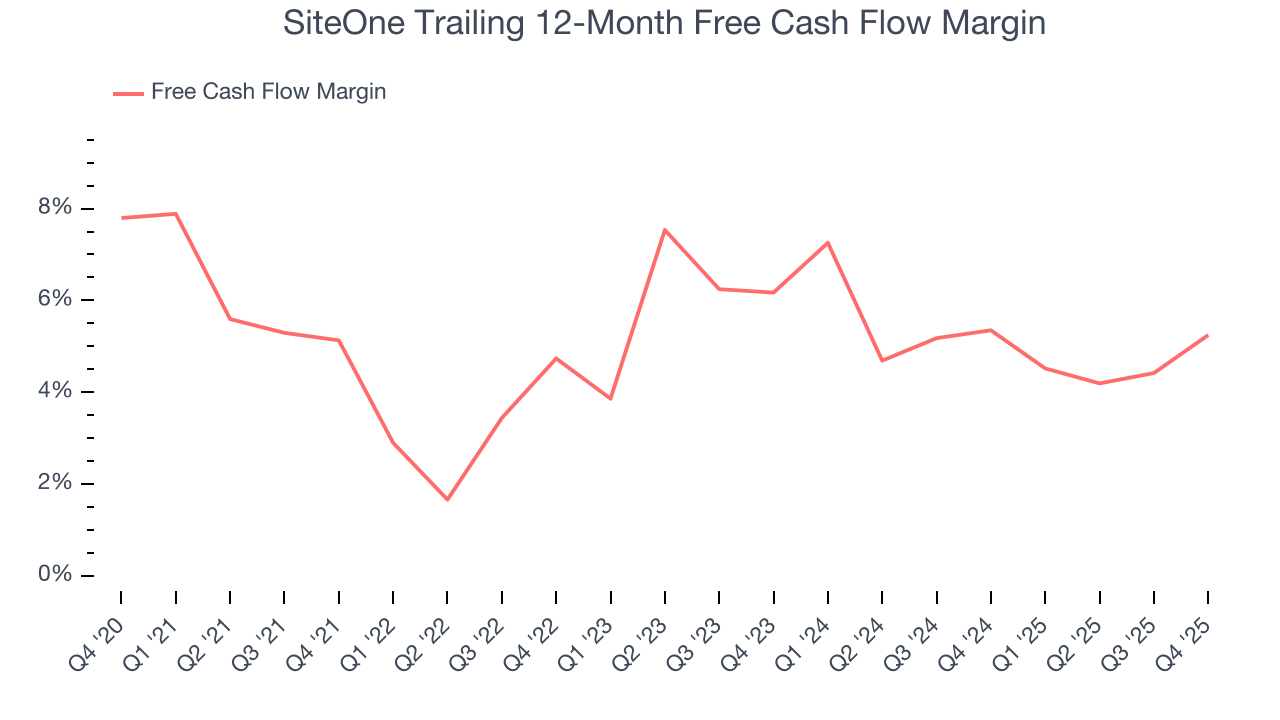

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

SiteOne has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 5.3%, subpar for an industrials business.

SiteOne’s free cash flow clocked in at $150.3 million in Q4, equivalent to a 14.4% margin. This result was good as its margin was 3.5 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

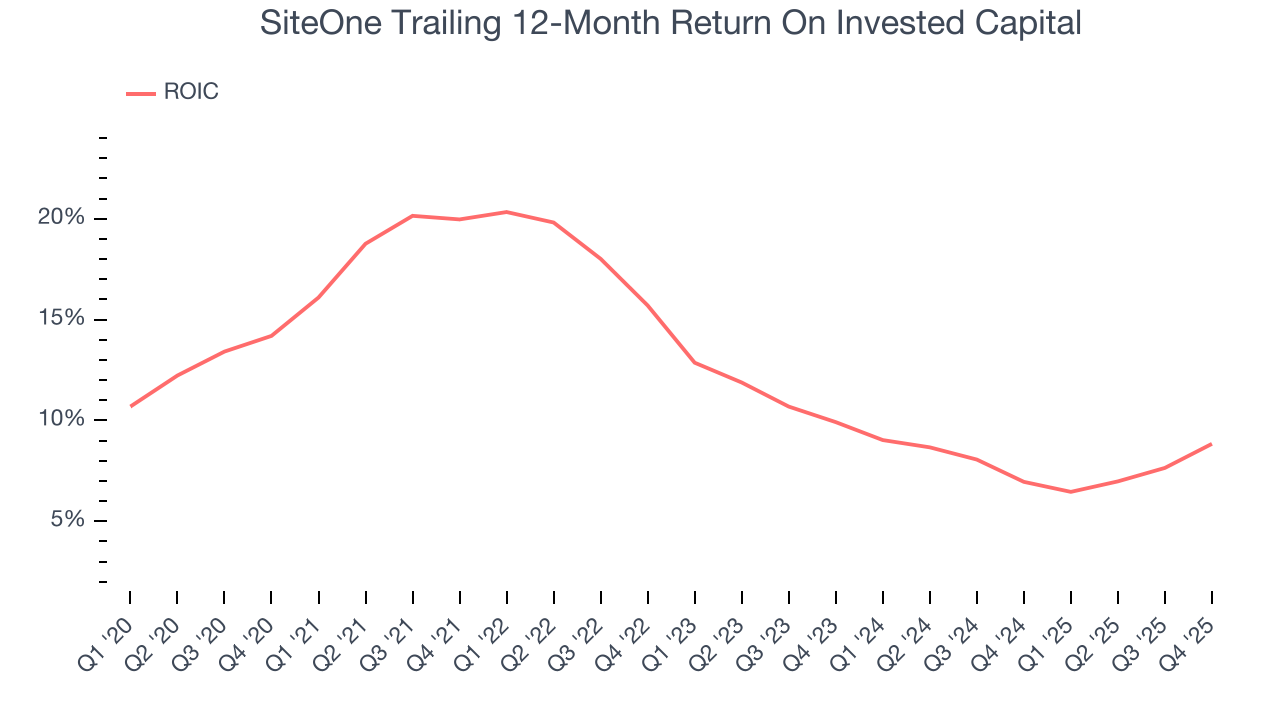

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although SiteOne hasn’t been the highest-quality company lately because of its poor bottom-line (EPS) performance, it historically found a few growth initiatives that worked. Its five-year average ROIC was 12.3%, higher than most industrials businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, SiteOne’s ROIC has decreased over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

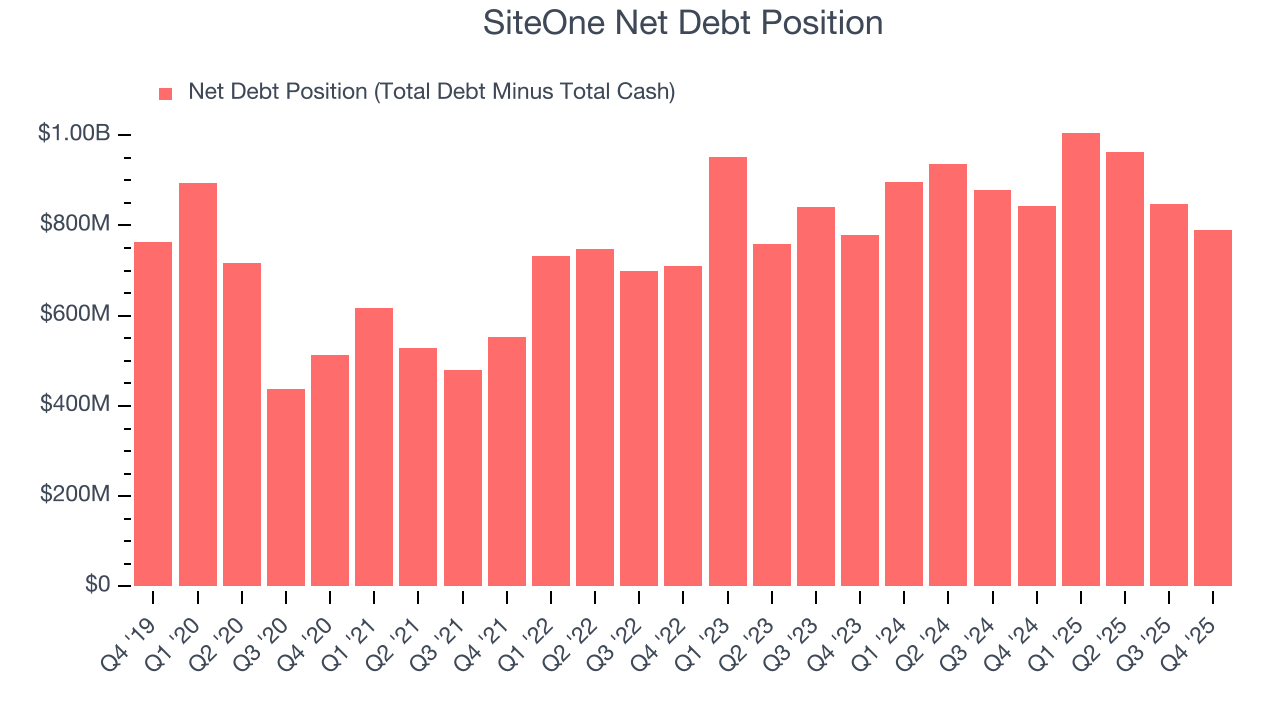

11. Balance Sheet Assessment

SiteOne reported $190.6 million of cash and $980 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $414.2 million of EBITDA over the last 12 months, we view SiteOne’s 1.9× net-debt-to-EBITDA ratio as safe. We also see its $18.6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from SiteOne’s Q4 Results

It was good to see SiteOne beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed and its revenue fell slightly short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 4.5% to $142.10 immediately following the results.

13. Is Now The Time To Buy SiteOne?

Updated: March 23, 2026 at 11:09 PM EDT

When considering an investment in SiteOne, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

SiteOne doesn’t pass our quality test. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s projected EPS for the next year implies the company’s fundamentals will improve, the downside is its flat organic revenue disappointed.

SiteOne’s P/E ratio based on the next 12 months is 28.2x. At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $175.60 on the company (compared to the current share price of $134.20).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.