Texas Pacific Land (TPL)

Texas Pacific Land is a compelling stock. Its marriage of growth and profitability makes it a financial powerhouse with attractive upside.― StockStory Analyst Team

1. News

2. Summary

Why We Like Texas Pacific Land

One of America's largest private landowners with roughly 868,000 acres in the Permian Basin, Texas Pacific Land (NYSE:TPL) owns land in West Texas and earns revenue from oil and gas royalties, water services, and land leases.

- Market share has increased this cycle as its 26.2% annual revenue growth over the last ten years was exceptional

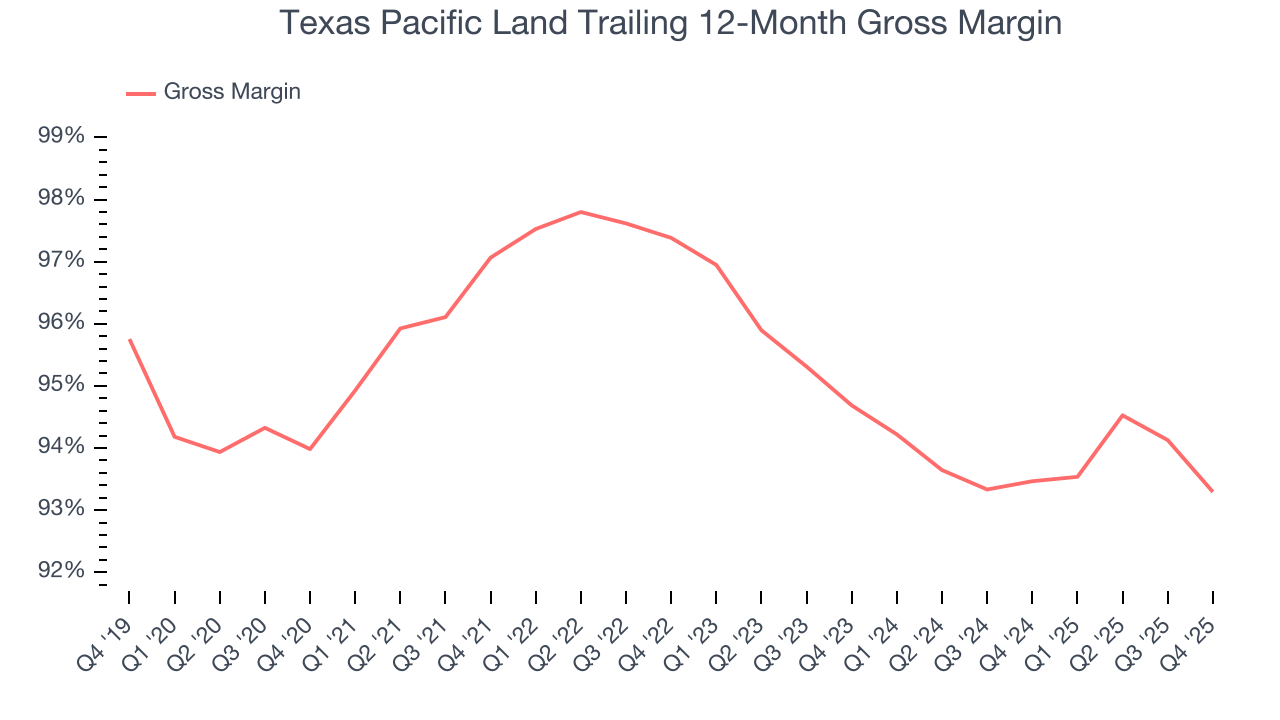

- Attractive asset base leads to wonderful unit economics and a best-in-class gross margin of 95%

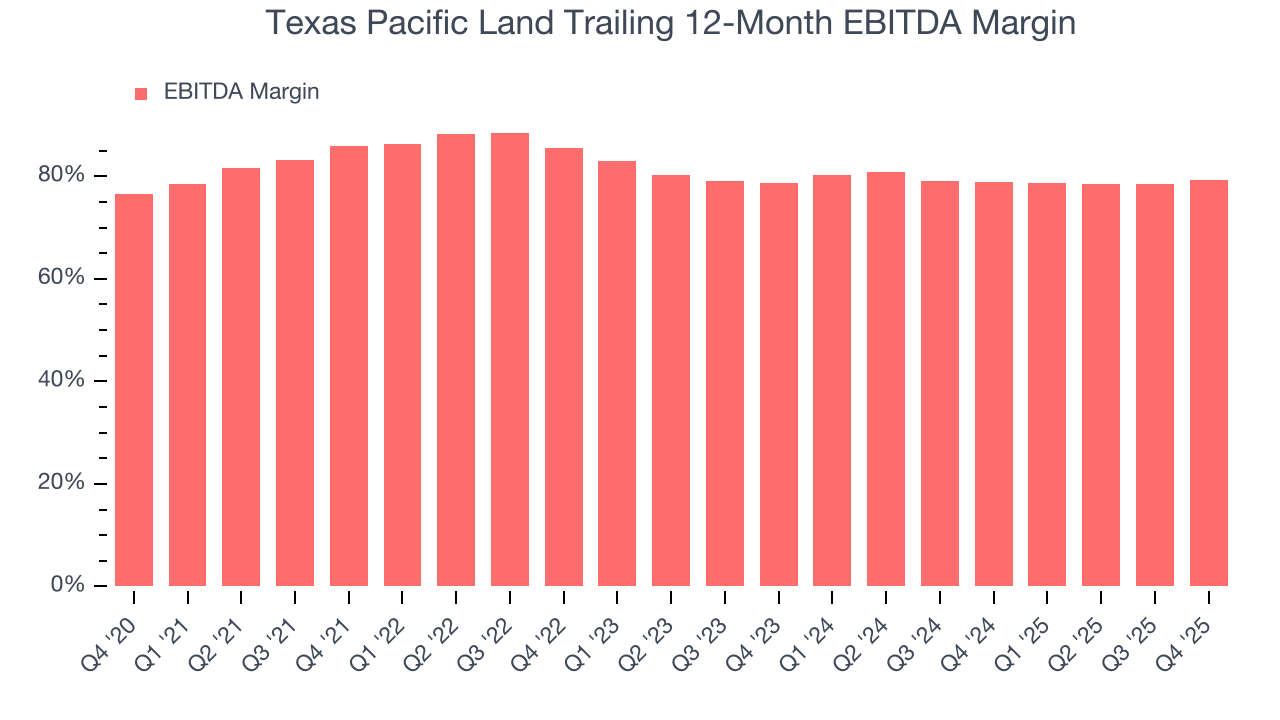

- Healthy EBITDA margin shows it’s a well-run company with efficient processes

We have an affinity for Texas Pacific Land. The valuation looks reasonable based on its quality, so this might be a favorable time to invest in some shares.

Why Is Now The Time To Buy Texas Pacific Land?

Texas Pacific Land’s stock price of $523.58 implies a valuation ratio of 43.8x forward EV-to-EBITDA. Looking at the energy upstream and integrated energy space, we think the valuation is fair - potentially even too low - for the business quality.

It’s an opportune time to buy the stock if you like the business model.

3. Texas Pacific Land (TPL) Research Report: Q4 CY2025 Update

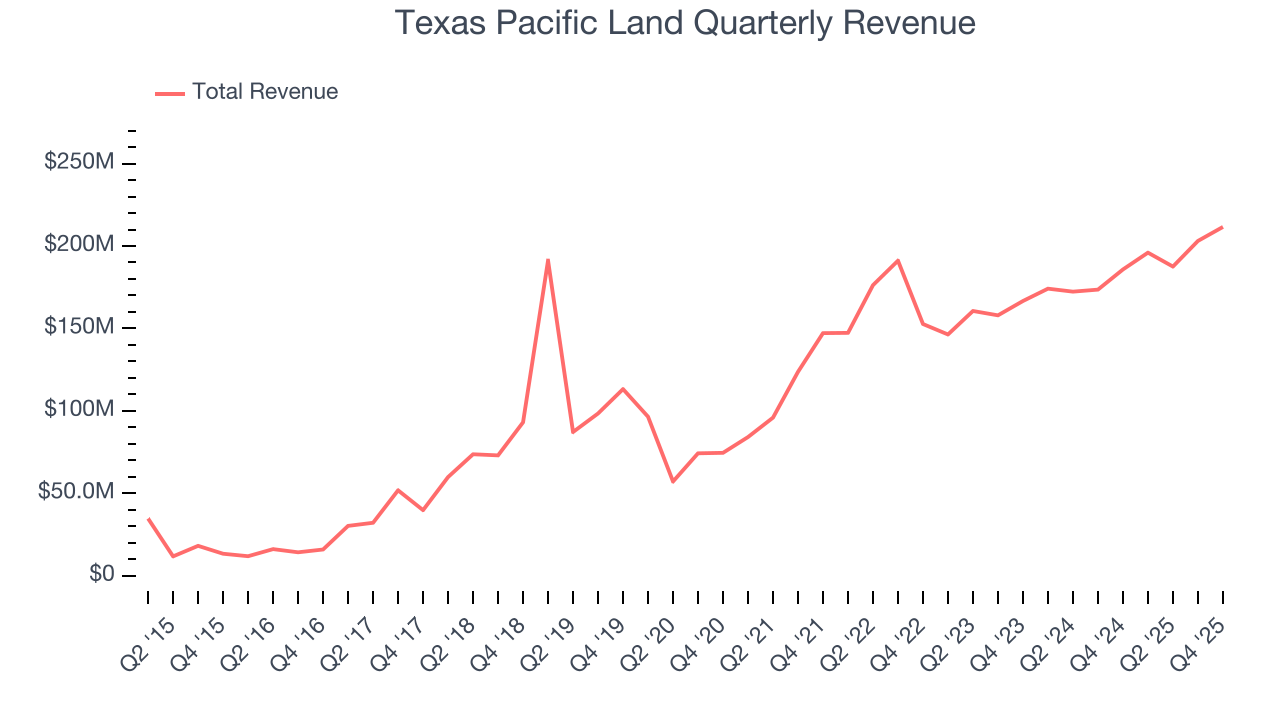

West Texas landowner Texas Pacific Land (NYSE:TPL) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 13.9% year on year to $211.6 million. Its GAAP profit of $1.79 per share was 50.2% below analysts’ consensus estimates.

Texas Pacific Land (TPL) Q4 CY2025 Highlights:

- Revenue: $211.6 million vs analyst estimates of $204 million (13.9% year-on-year growth, 3.7% beat)

- EPS (GAAP): $1.79 vs analyst expectations of $3.60 (50.2% miss)

- Adjusted EBITDA: $178.1 million vs analyst estimates of $172 million (84.2% margin, 3.6% beat)

- Operating Margin: 70.6%, down from 79.3% in the same quarter last year

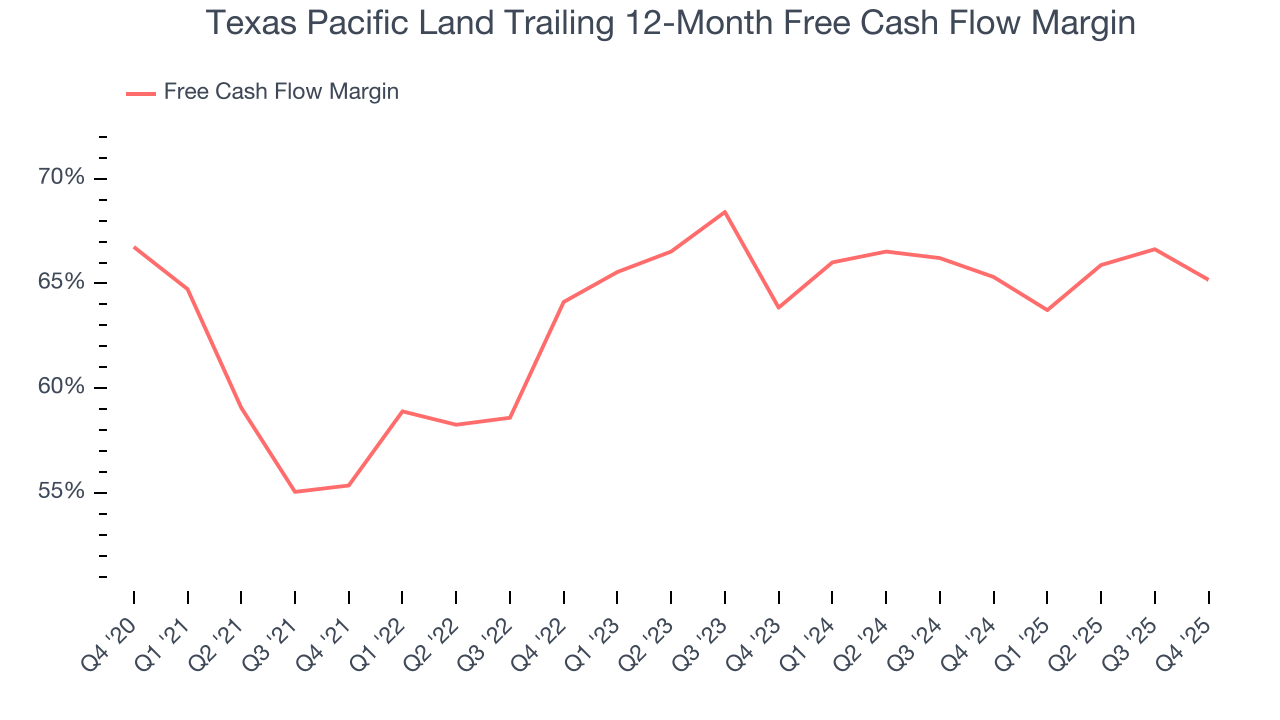

- Free Cash Flow Margin: 56.2%, down from 61% in the same quarter last year

- Market Capitalization: $36.2 billion

Company Overview

One of America's largest private landowners with roughly 868,000 acres in the Permian Basin, Texas Pacific Land (NYSE:TPL) owns land in West Texas and earns revenue from oil and gas royalties, water services, and land leases.

The company's business model differs from traditional oil and gas producers—rather than drilling wells itself, Texas Pacific Land acts as a landlord to energy companies operating in the Permian Basin, one of the most productive oil-producing regions in the United States. Its revenue streams span the entire lifecycle of oil and gas development. When companies build roads and infrastructure, Texas Pacific Land sells them caliche, a calcium carbonate material used for construction, and charges fees for land use. During drilling and production, it provides sourced and treated water needed for hydraulic fracturing operations. Once wells are producing, the company collects royalty payments on the oil and gas extracted from its mineral rights—typically a percentage of production value without bearing any of the drilling costs.

Beyond energy activities, the company generates steady income from easements granted to pipeline operators, power companies, and utilities crossing its land. These agreements often span thirty years or more and include renewal payments. It also leases land for processing facilities, storage operations, and other commercial uses. Through its Water Services and Operations segment, operated as Texas Pacific Water Resources, the company has built a water infrastructure business that sources fresh water and treats produced water—the salty wastewater that comes up with oil and gas—for disposal or reuse by operators.

For example, when an oil company like Occidental Petroleum or Chevron drills a new well on Texas Pacific Land's acreage, it might pay for caliche to build access roads, purchase treated water for fracking operations, secure easements for pipelines to transport the oil, and then pay ongoing royalties on every barrel produced. More recently, the company has begun exploring opportunities in renewable energy, carbon capture, and even bitcoin mining facilities that could utilize its extensive land holdings.

4. U.S. Shale E&P

US shale oil producers extract crude from tight rock formations using horizontal drilling and hydraulic fracturing (fracking) techniques, primarily in basins like the Permian, Bakken, and Eagle Ford. Tailwinds include short-cycle investment flexibility allowing rapid production adjustments, technological improvements enhancing well productivity, and proximity to refining and export infrastructure. Capital discipline has improved financial returns. Headwinds include commodity price sensitivity affecting drilling economics, accelerating well decline rates requiring continuous capital investment, and increasing regulatory and ESG scrutiny. Water usage, induced seismicity concerns, and evolving environmental regulations present ongoing operational challenges.

As a unique landowner-royalty hybrid, Texas Pacific Land has limited direct competitors. Comparable royalty companies include Permian Basin Royalty Trust (NYSE:PBT) and oil and gas royalty trusts, though these typically lack the diversified land-use revenue streams.

5. Revenue Scale

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks. Texas Pacific Land’s $798.2 million of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night. is a small company in an industry where scale matters.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, Texas Pacific Land grew its sales at an excellent 21.4% compounded annual growth rate. Its growth surpassed the average energy upstream and integrated energy company and shows its offerings resonate with customers, a great starting point for our analysis.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Texas Pacific Land’s annualized revenue growth of 26.2% over the last ten years is above its five-year trend.

This quarter, Texas Pacific Land reported year-on-year revenue growth of 13.9%, and its $211.6 million of revenue exceeded Wall Street’s estimates by 3.7%.

7. Gross Margin

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

Texas Pacific Land, which averaged 95% gross margin over the last five years, exhibits enviable unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an advantaged starting point for ultimate operating profits and free cash flow generation.

Texas Pacific Land produced a 91.7% gross profit margin in Q4, down 3.2 percentage points year on year.

8. Adjusted EBITDA Margin

Texas Pacific Land has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 81.3%.

Analyzing the trend in its profitability, Texas Pacific Land’s EBITDA margin decreased by 6.6 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Texas Pacific Land generated an EBITDA margin profit margin of 84.2%, up 2.9 percentage points year on year. This increase was a welcome development and shows it was more efficient. This adjusted EBITDA beat Wall Street’s estimates by 3.6%.

9. Cash Is King

As mentioned above, adjusted EBITDA ignores capital structure and drilling expenditure decisions. These are two huge aspects of an Energy producer, so in order to understand a comprehensive picture of business quality, an investor needs to account for these. Said differently, adjusted EBITDA margins could be solid but free cash flow is abysmal because decline rates of the asset are extreme and the drilling is expensive. Free cash flow tells you about not only the economics of the production that has happened but how much it costs to stay in business as well (further drilling or extraction).

Texas Pacific Land has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging an eye-popping 63.4% over the last five years.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Texas Pacific Land’s ratio of quarterly free cash flow volatility to WTI Crude price volatility over the past five years was 1.7 (lower is better), indicating unusually strong insulation from commodity swings. This stability supports superior capital access in downturns and positions Texas Pacific Land to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Texas Pacific Land? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Texas Pacific Land’s free cash flow clocked in at $118.9 million in Q4, equivalent to a 56.2% margin. The company’s cash profitability regressed as it was 4.8 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends carry greater meaning.

10. Balance Sheet Assessment

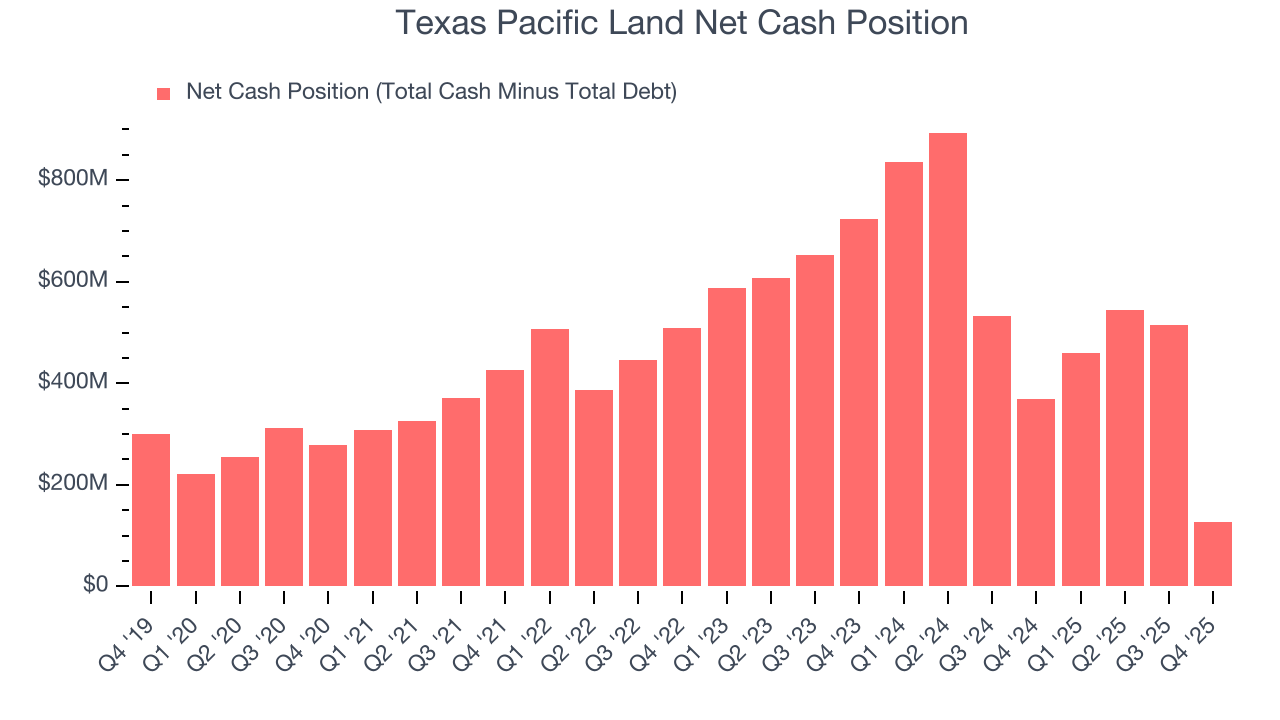

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Texas Pacific Land is a profitable, well-capitalized company with $144.8 million of cash and $17.79 million of debt on its balance sheet. This $127 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Texas Pacific Land’s Q4 Results

We enjoyed seeing Texas Pacific Land beat analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS missed. Zooming out, we think this was a mixed quarter. The stock traded up 2.6% to $538.93 immediately following the results.

12. Is Now The Time To Buy Texas Pacific Land?

Updated: March 12, 2026 at 1:13 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Texas Pacific Land, you should also grasp the company’s longer-term business quality and valuation.

There is a lot to like about Texas Pacific Land. First, the company’s revenue growth over the last five years was top-tier for the sector, and analysts believe it can continue growing at these levels. And while its subscale operations hasn't hit a level of diversification where investors can sleep easy at night, its revenue growth over the last ten years was top-tier for the sector. On top of that, Texas Pacific Land’s admirable gross margin indicates excellent unit economics.

Texas Pacific Land’s EV-to-EBITDA ratio based on the next 12 months is 43.8x. Looking across the spectrum of energy upstream and integrated energy companies today, Texas Pacific Land’s fundamentals shine bright. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $444.50 on the company (compared to the current share price of $523.58).