Vestis (VSTS)

We wouldn’t buy Vestis. Its weak sales growth shows demand is soft and its low margins are a cause for concern.― StockStory Analyst Team

1. News

2. Summary

Why We Think Vestis Will Underperform

Operating a network of more than 350 facilities with 3,300 delivery routes serving customers weekly, Vestis (NYSE:VSTS) provides uniform rentals, workplace supplies, and facility services to over 300,000 business locations across the United States and Canada.

- Sales tumbled by 2% annually over the last two years, showing market trends are working against its favor during this cycle

- Falling earnings per share over the last three years has some investors worried as stock prices ultimately follow EPS over the long term

- 5× net-debt-to-EBITDA ratio shows it’s overleveraged and increases the probability of shareholder dilution if things turn unexpectedly

Vestis doesn’t check our boxes. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Vestis

Vestis’s stock price of $7.33 implies a valuation ratio of 21.2x forward P/E. Not only is Vestis’s multiple richer than most business services peers, but it’s also expensive for its revenue characteristics.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Vestis (VSTS) Research Report: Q4 CY2025 Update

Uniform rental provider Vestis Corporation (NYSE:VSTS) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 3.2% year on year to $663.4 million. Its GAAP loss of $0.05 per share was $0.03 below analysts’ consensus estimates.

Vestis (VSTS) Q4 CY2025 Highlights:

- Revenue: $663.4 million vs analyst estimates of $664.7 million (3.2% year-on-year decline, in line)

- EPS (GAAP): -$0.05 vs analyst estimates of -$0.02 ($0.03 miss)

- Adjusted EBITDA: $70.38 million vs analyst estimates of $69.05 million (10.6% margin, 1.9% beat)

- EBITDA guidance for the full year is $300 million at the midpoint, above analyst estimates of $295.8 million

- Operating Margin: 2.5%, down from 4.4% in the same quarter last year

- Free Cash Flow was $28.3 million, up from -$10.6 million in the same quarter last year

- Market Capitalization: $965.9 million

Company Overview

Operating a network of more than 350 facilities with 3,300 delivery routes serving customers weekly, Vestis (NYSE:VSTS) provides uniform rentals, workplace supplies, and facility services to over 300,000 business locations across the United States and Canada.

Vestis offers a comprehensive suite of services centered around its core uniform rental business. The company handles the entire uniform lifecycle - from design and manufacturing to customization, delivery, laundering, sanitization, repair, and replacement. Its uniform options range from basic shirts and pants to specialized garments like flame-resistant clothing, high-visibility wear, and particulate-free garments for cleanroom environments.

Beyond uniforms, Vestis provides complementary workplace essentials including floor mats, towels, linens, restroom supplies, first-aid kits, and safety products. These services are typically delivered on a recurring weekly schedule through multi-year contracts, creating predictable revenue streams.

For a manufacturing client, Vestis might supply flame-resistant uniforms that meet safety regulations, deliver them weekly, handle all cleaning and repairs, and simultaneously restock first-aid stations and replace soiled floor mats - allowing the client to focus on production rather than facility management.

The company operates its own manufacturing facilities in Mexico, producing approximately 60% of its uniforms and linens. This vertical integration helps control quality and costs. Vestis maintains a network of laundry plants, satellite facilities, distribution centers, and a fleet of delivery vehicles operated by route service representatives who both deliver clean items and collect soiled ones.

Vestis serves customers across diverse industries including manufacturing, hospitality, retail, food processing, pharmaceuticals, healthcare, and automotive. Its client base spans from small single-location businesses to large national corporations with multiple facilities. This industry diversification helps insulate the company from downturns in any single sector.

The company emphasizes sustainability in its operations, focusing on minimizing fuel usage in its delivery routes and reducing energy and water consumption in its laundry facilities. By repairing and reusing garments whenever possible, Vestis extends product lifecycles and supports circular economy principles.

4. Industrial & Environmental Services

Growing regulatory pressure on environmental compliance and increasing corporate ESG commitments should buoy the sector for years to come. On the other hand, environmental regulations continue to evolve, and this may require costly upgrades, volatility in commodity waste and recycling markets, and labor shortages in industrial services. As for digitization, a theme that is impacting nearly every industry, the increasing use of data, analytics, and automation will give rise to improved efficiency of operations. Conversely, though, the benefits of digitization also come with challenges of integrating new technologies into legacy systems.

Vestis competes with Cintas Corporation (NASDAQ:CTAS), Aramark (NYSE:ARMK), and UniFirst Corporation (NYSE:UNF) in the uniform rental and workplace supplies industry, along with numerous regional and local providers across North America.

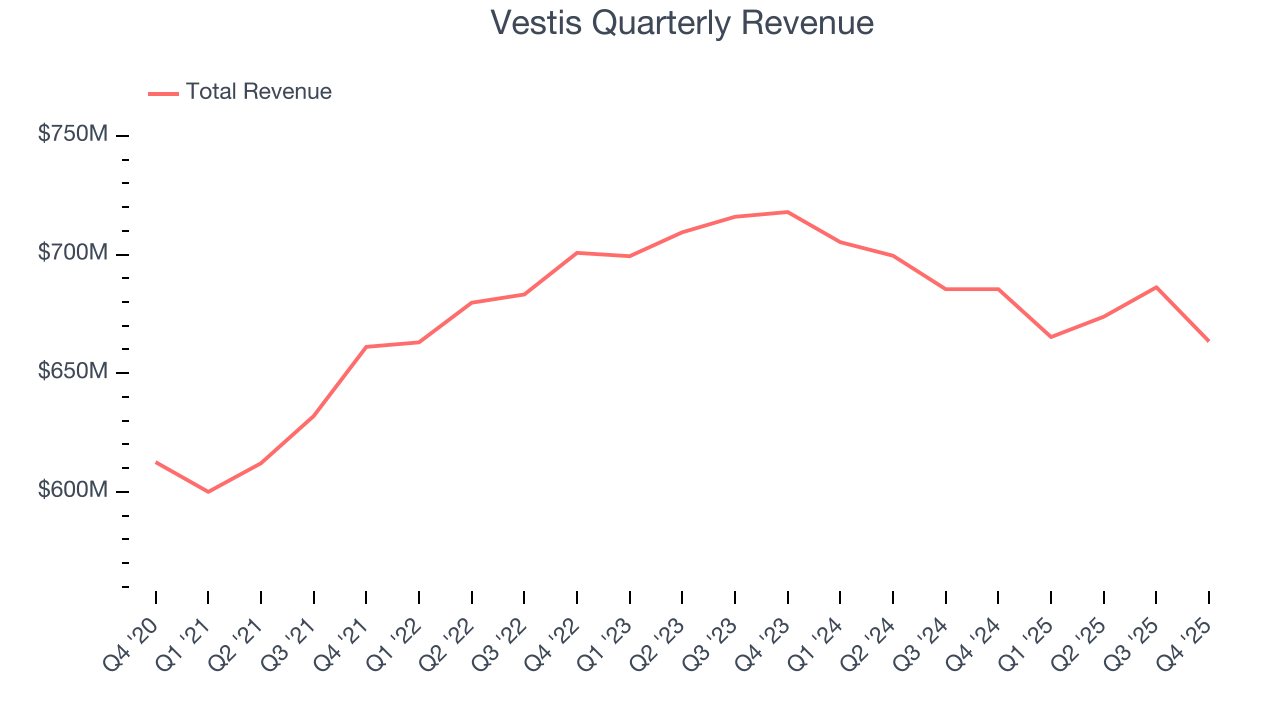

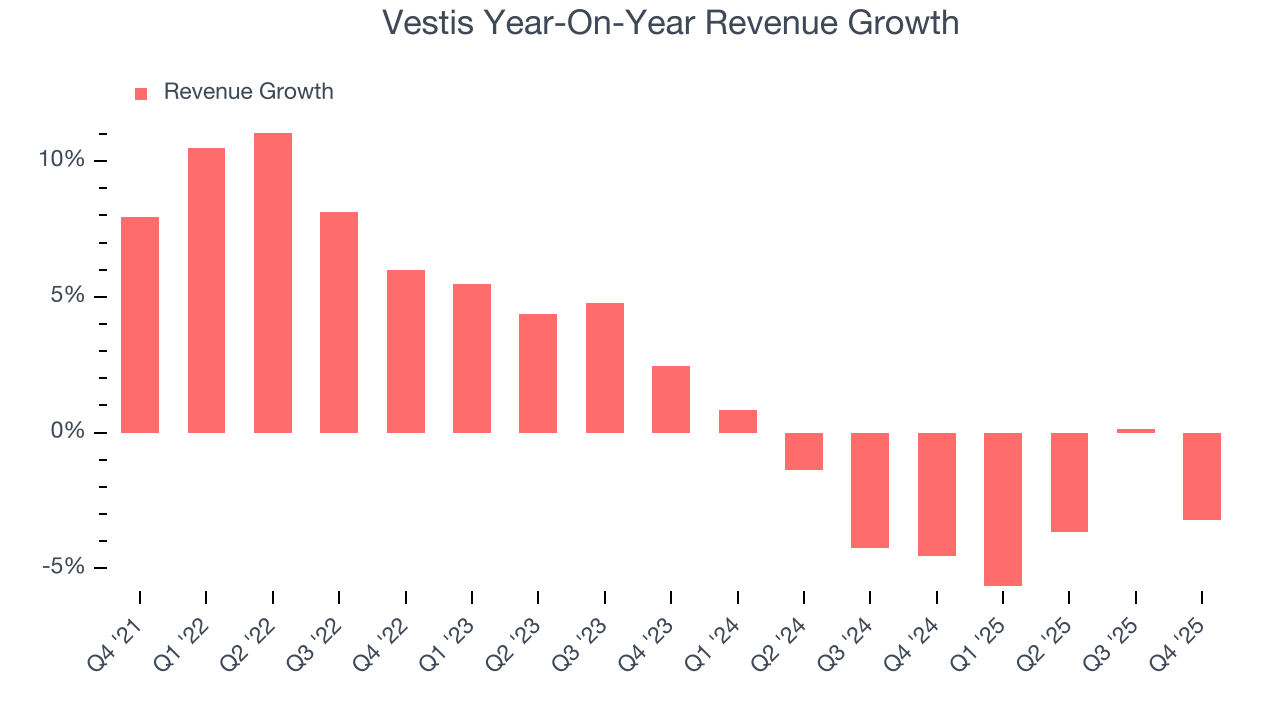

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $2.69 billion in revenue over the past 12 months, Vestis is a mid-sized business services company, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Vestis’s sales grew at a sluggish 1.8% compounded annual growth rate over the last four years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a stretched historical view may miss recent innovations or disruptive industry trends. Vestis’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 2.7% annually.

This quarter, Vestis reported a rather uninspiring 3.2% year-on-year revenue decline to $663.4 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to decline by 1.7% over the next 12 months, similar to its two-year rate. Although this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

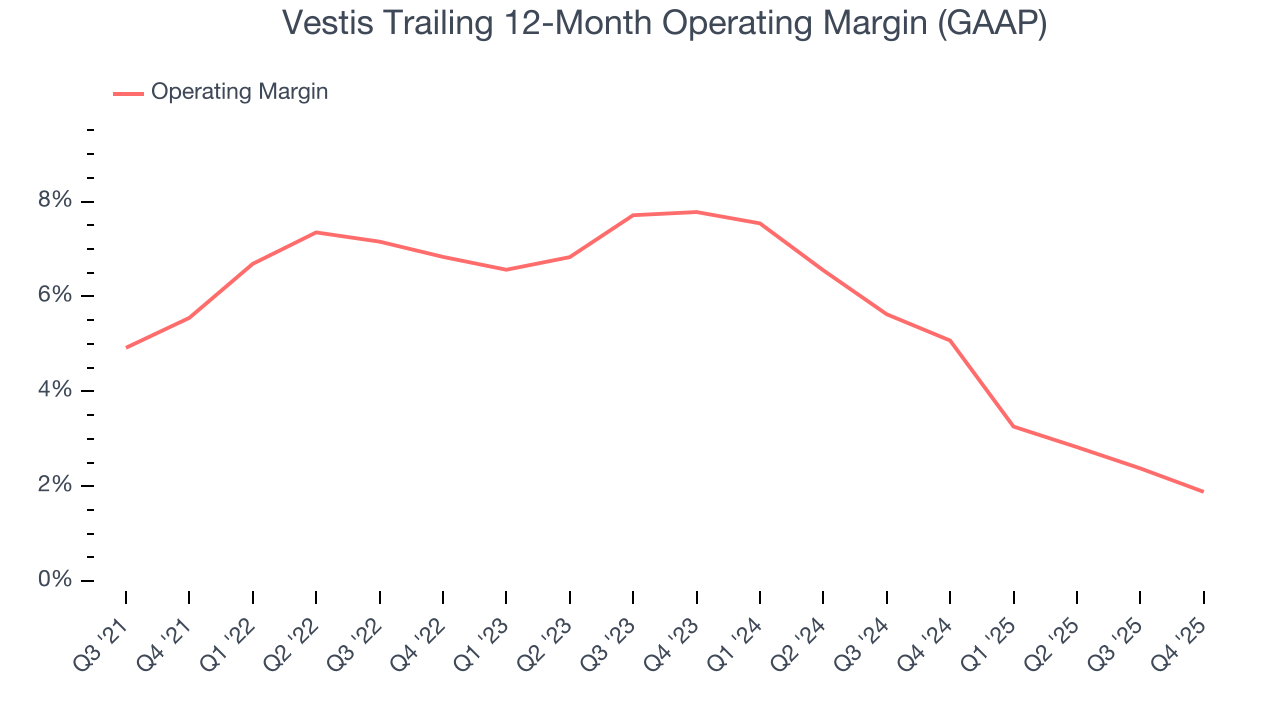

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Vestis was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.5% was weak for a business services business.

Looking at the trend in its profitability, Vestis’s operating margin decreased by 3.7 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Vestis’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, Vestis generated an operating margin profit margin of 2.5%, down 1.9 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

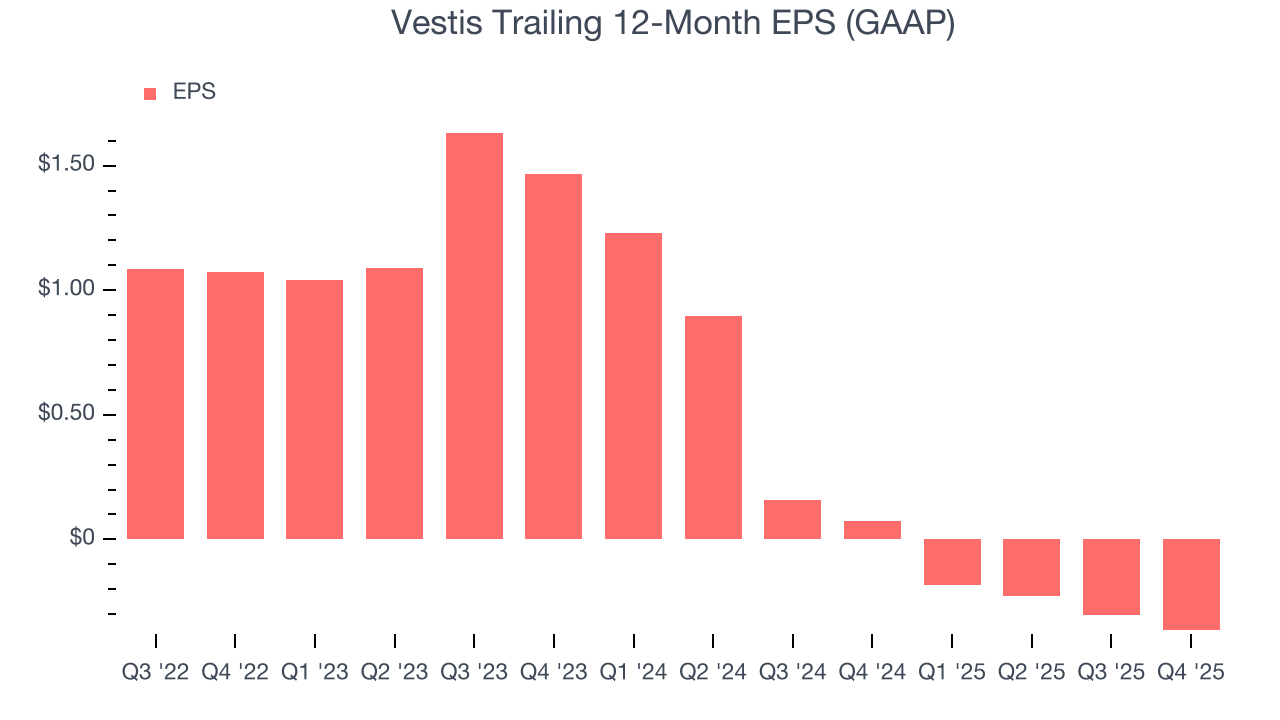

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vestis’s full-year EPS turned negative over the last three years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Vestis’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Vestis, its two-year annual EPS declines of 49.9% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, Vestis reported EPS of negative $0.05, down from $0.01 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street is optimistic. Analysts forecast Vestis’s full-year EPS of negative $0.36 will flip to positive $0.03.

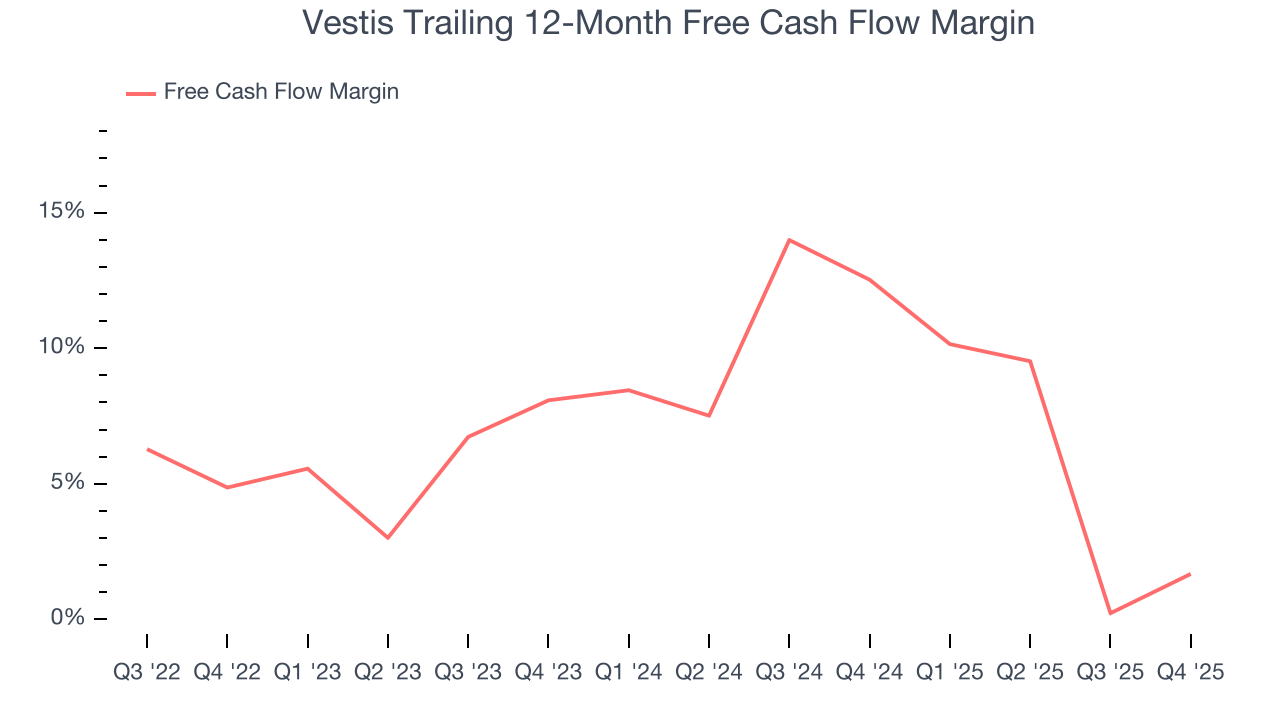

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Vestis has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.7% over the last five years, slightly better than the broader business services sector.

Taking a step back, we can see that Vestis’s margin dropped by 3.2 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Vestis’s free cash flow clocked in at $28.3 million in Q4, equivalent to a 4.3% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

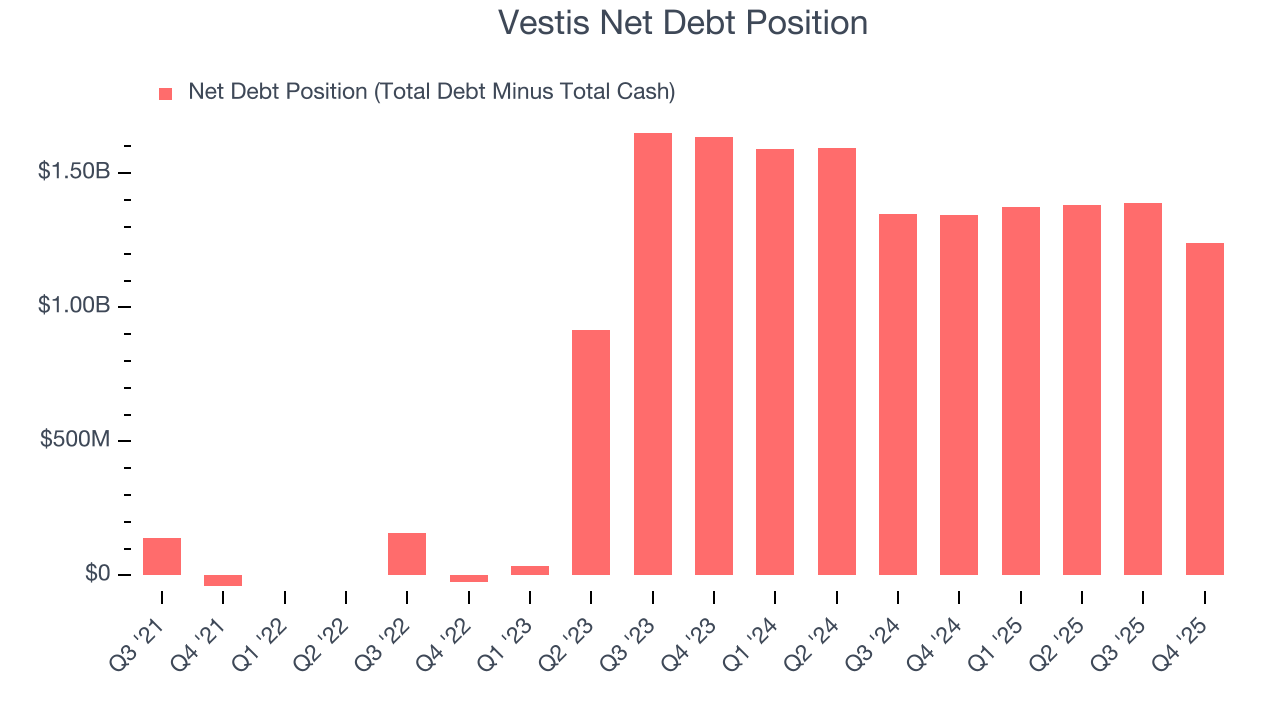

9. Balance Sheet Risk

Debt is a tool that can boost company returns but presents risks if used irresponsibly. As long-term investors, we aim to avoid companies taking excessive advantage of this instrument because it could lead to insolvency.

Vestis’s $1.28 billion of debt exceeds the $41.55 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $246.7 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Vestis could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Vestis can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

10. Key Takeaways from Vestis’s Q4 Results

While revenue was just in line, EBITDA beat and EBITDA guidance also exceeded expectations. Overall, this was a solid quarter. The stock traded up 4.2% to $7.63 immediately after reporting.

11. Is Now The Time To Buy Vestis?

Updated: February 10, 2026 at 7:26 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Vestis.

We see the value of companies helping their customers, but in the case of Vestis, we’re out. To kick things off, its revenue growth was weak over the last four years, and analysts expect its demand to deteriorate over the next 12 months. And while its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its declining operating margin shows the business has become less efficient.

Vestis’s P/E ratio based on the next 12 months is 19.3x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $6.13 on the company (compared to the current share price of $7.63), implying they don’t see much short-term potential in Vestis.