Watts Water Technologies (WTS)

Watts Water Technologies is a compelling stock. It generates heaps of cash that are reinvested into the business, creating a virtuous cycle of returns.― StockStory Analyst Team

1. News

2. Summary

Why We Like Watts Water Technologies

Founded in 1874, Watts Water (NYSE:WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

- Additional sales over the last five years increased its profitability as the 22.2% annual growth in its earnings per share outpaced its revenue

- Offerings are difficult to replicate at scale and result in a best-in-class gross margin of 46.2%

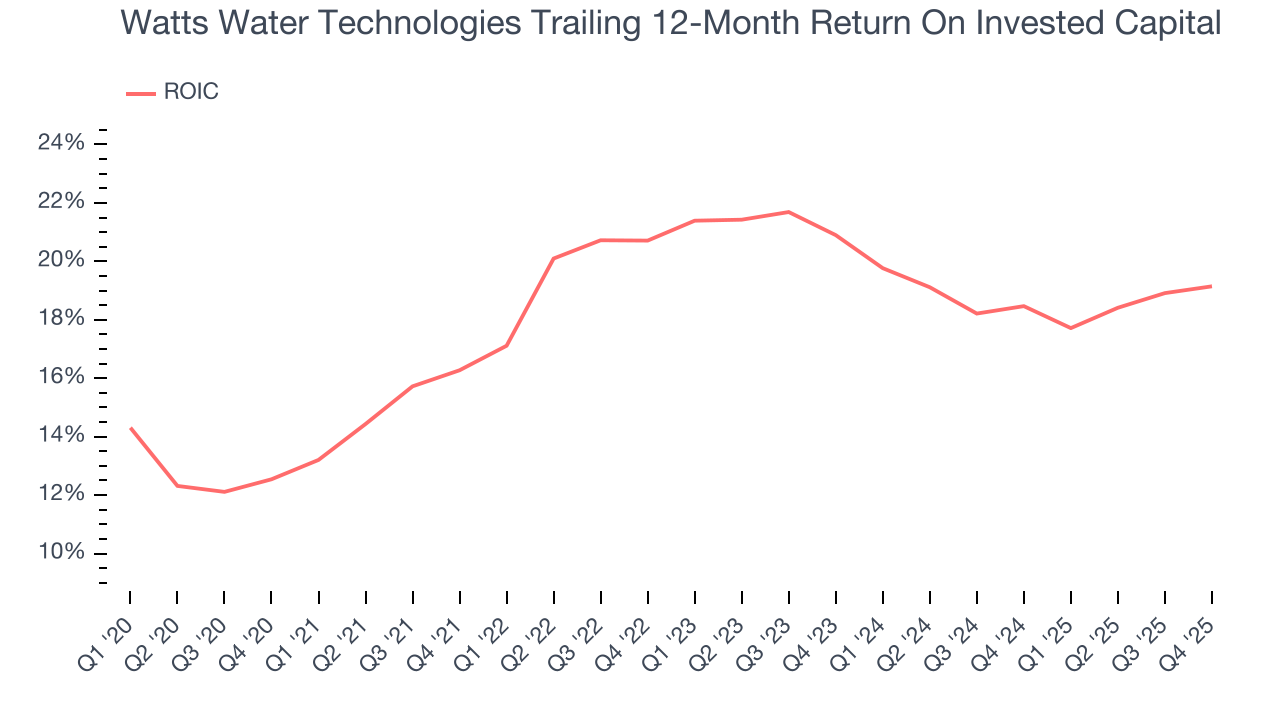

- Industry-leading 19.1% return on capital demonstrates management’s skill in finding high-return investments

We’re fond of companies like Watts Water Technologies. The price seems reasonable in light of its quality, so this might be an opportune time to buy some shares.

Why Is Now The Time To Buy Watts Water Technologies?

Watts Water Technologies is trading at $289.56 per share, or 25.1x forward P/E. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Where you buy a stock impacts returns. Our analysis shows that business quality is a much bigger determinant of market outperformance over the long term compared to entry price, but getting a good deal on a stock certainly isn’t a bad thing.

3. Watts Water Technologies (WTS) Research Report: Q4 CY2025 Update

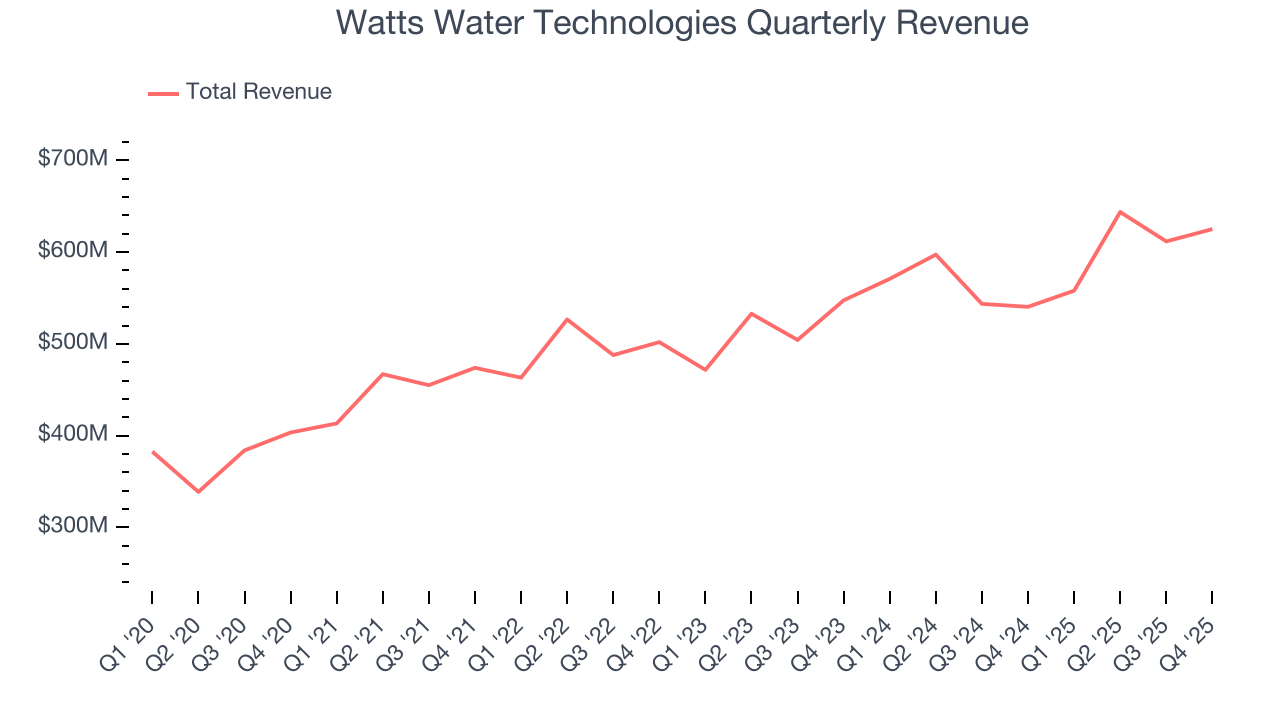

Water management manufacturer Watts Water (NYSE:WTS) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 15.7% year on year to $625.1 million. Its non-GAAP profit of $2.62 per share was 12% above analysts’ consensus estimates.

Watts Water Technologies (WTS) Q4 CY2025 Highlights:

- Revenue: $625.1 million vs analyst estimates of $611.1 million (15.7% year-on-year growth, 2.3% beat)

- Adjusted EPS: $2.62 vs analyst estimates of $2.34 (12% beat)

- Operating Margin: 18.2%, up from 16.5% in the same quarter last year

- Free Cash Flow Margin: 22.4%, down from 23.6% in the same quarter last year

- Organic Revenue rose 8% year on year (beat)

- Market Capitalization: $10.51 billion

Company Overview

Founded in 1874, Watts Water (NYSE:WTS) specializes in manufacturing water products and systems for residential, commercial, and industrial applications globally.

Watts Water Technologies, started as a small machine shop supplying parts to textile mills in Lawrence, Massachusetts. Initially focused on steam regulators to control the pressure and efficiency of steam boilers, the company quickly became recognized for its products in the burgeoning industrial landscape. Over the decades, Watts expanded its offerings to include a variety of water control products. This growth was propelled by strategic acquisitions that broadened its product lines and extended its market reach. Today, Watts Water Technologies is known for its comprehensive range of products aimed at managing water efficiency and safety in residential, commercial, and industrial settings.

Watts Water specializes in products for managing water flow, temperature, and safety across residential and commercial settings. Its offerings include flow control devices like backflow preventers and water pressure regulators, along with safety equipment such as thermostatic mixing valves and leak detection systems. These products are increasingly integrated with smart technology, enabling remote monitoring and management via building management systems or personal devices to prevent water waste and damage.

In the HVAC and gas sector, Watts provides solutions like high-efficiency boilers, water heaters, and various heating systems, including those for under-floor radiant heating and commercial food service applications. Additionally, Watts ventures into water sustainability with its drainage and water re-use segment, offering products like engineered rainwater harvesting systems and drainage products including connected roof drain setups.

Watts Water generates revenue primarily by selling its products through various distribution channels. These include plumbing, heating, and mechanical wholesale distributors and dealers, as well as original equipment manufacturers (OEMs), specialty product distributors, and major DIY and retail chains. The company’s end markets are diverse, encompassing residential and commercial building services, industrial applications, and specialty areas like high-efficiency boilers, water heaters, and food service products.

4. Water Infrastructure

Trends towards conservation and reducing groundwater depletion are putting water infrastructure and treatment products front and center. Companies that can innovate and create solutions–especially automated or connected solutions–to address these thematic trends will create incremental demand and speed up replacement cycles. On the other hand, water infrastructure and treatment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Competitors offering similar products include Mueller Water Products (NYSE:MWA), A.O. Smith (NYSE:AOS), and Pentair (NYSE:PNR).

5. Revenue Growth

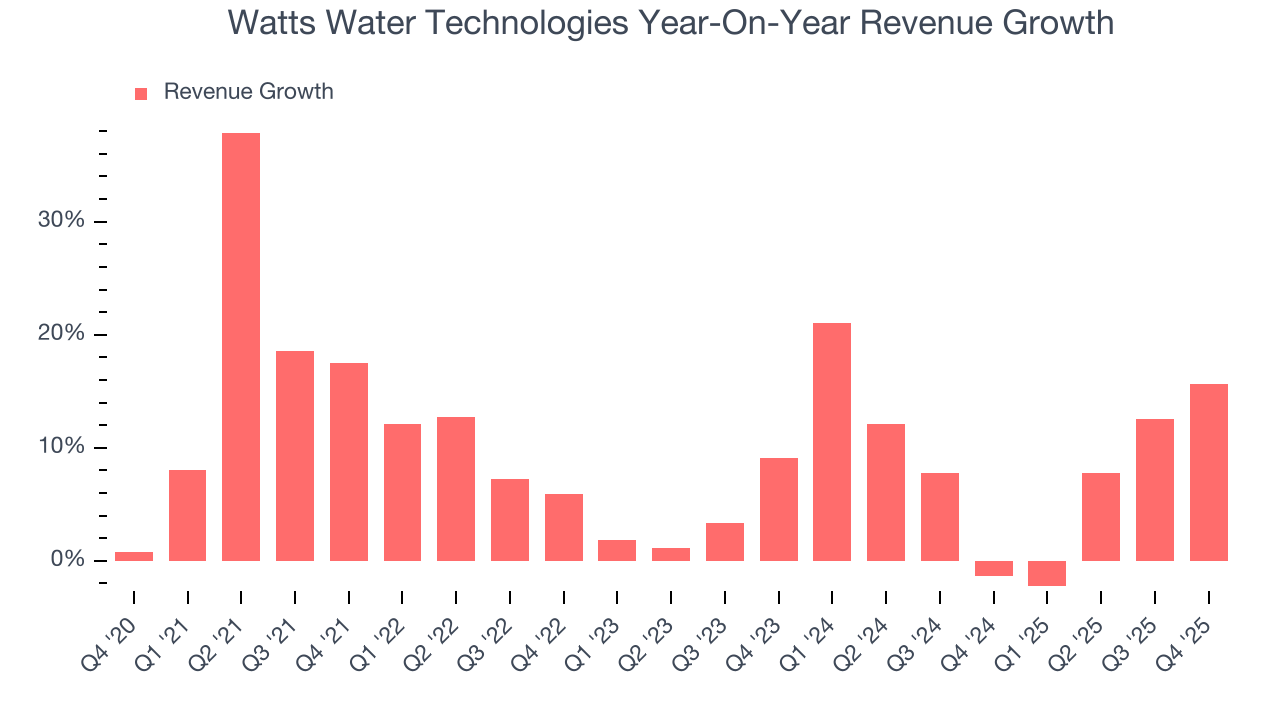

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Watts Water Technologies grew its sales at a solid 10.1% compounded annual growth rate. Its growth surpassed the average industrials company and shows its offerings resonate with customers, a great starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Watts Water Technologies’s annualized revenue growth of 8.9% over the last two years is below its five-year trend, but we still think the results were respectable.

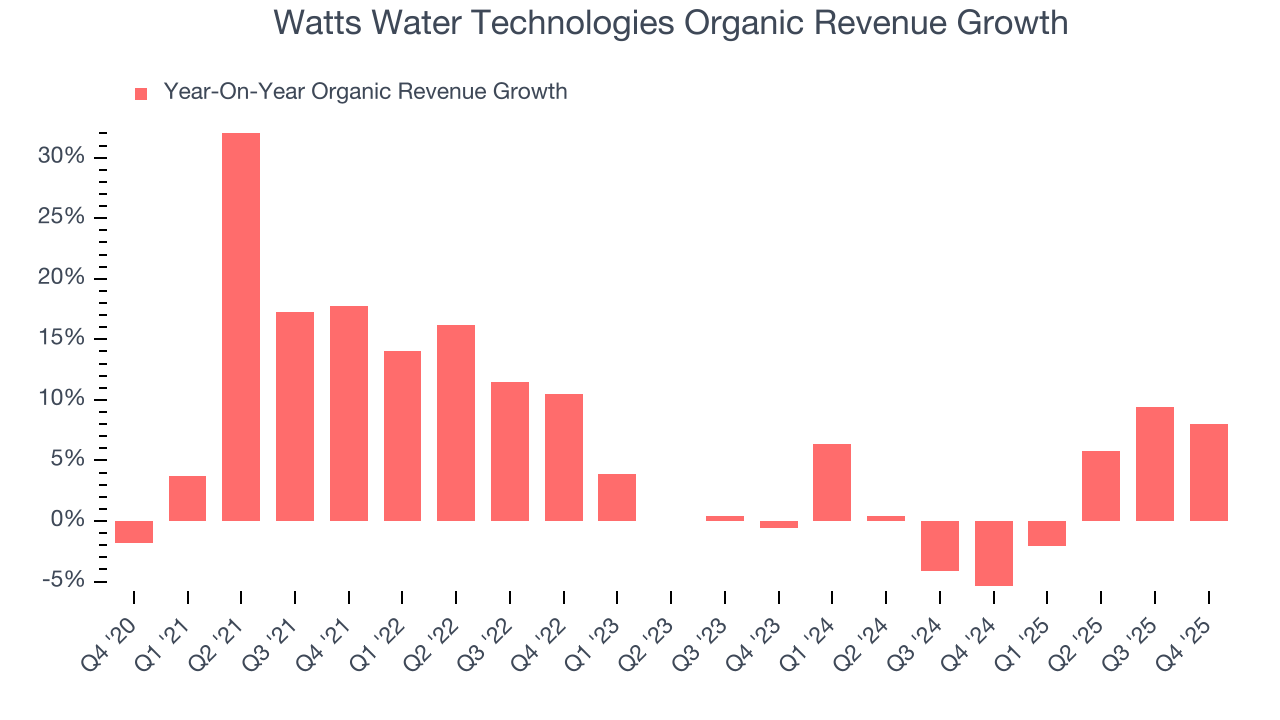

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Watts Water Technologies’s organic revenue averaged 2.3% year-on-year growth. Because this number is lower than its two-year revenue growth, we can see that some mixture of acquisitions and foreign exchange rates boosted its headline results.

This quarter, Watts Water Technologies reported year-on-year revenue growth of 15.7%, and its $625.1 million of revenue exceeded Wall Street’s estimates by 2.3%.

Looking ahead, sell-side analysts expect revenue to grow 6.5% over the next 12 months, a slight deceleration versus the last two years. This projection doesn't excite us and suggests its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

6. Gross Margin & Pricing Power

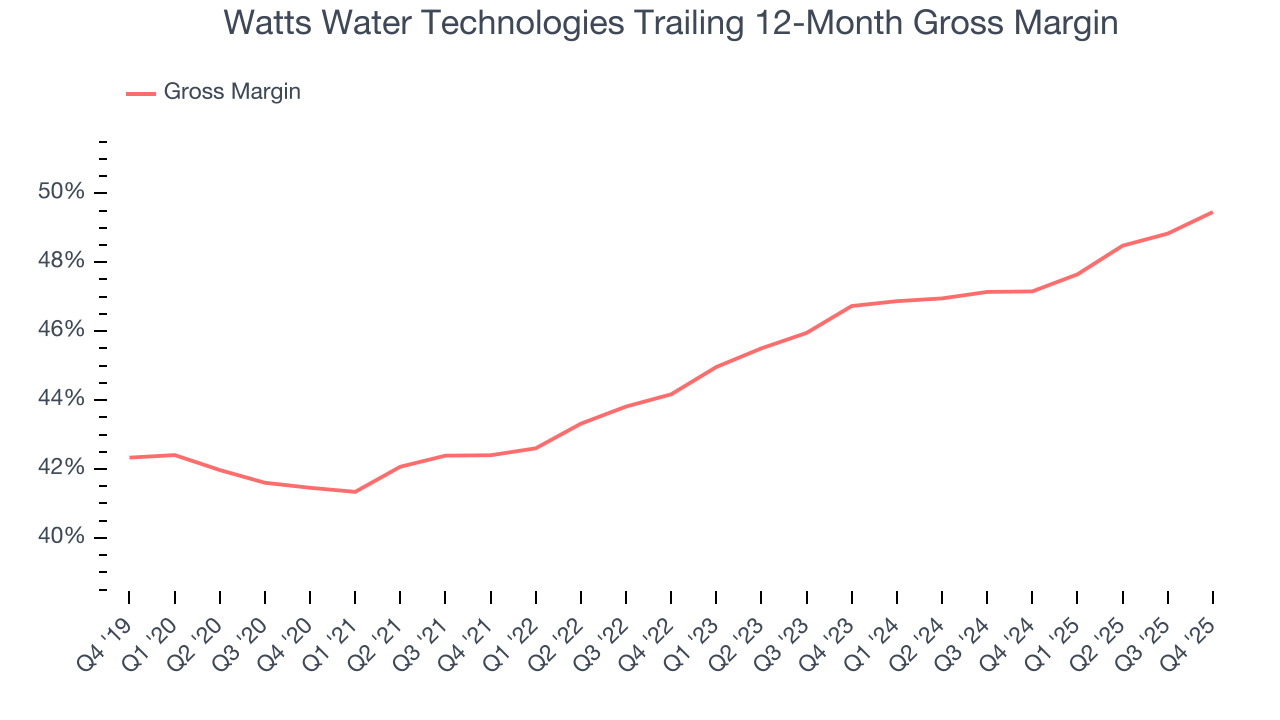

Watts Water Technologies has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 46.2% gross margin over the last five years. Said differently, roughly $46.23 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

Watts Water Technologies’s gross profit margin came in at 49.5% this quarter , marking a 2.7 percentage point increase from 46.7% in the same quarter last year. Watts Water Technologies’s full-year margin has also been trending up over the past 12 months, increasing by 2.3 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

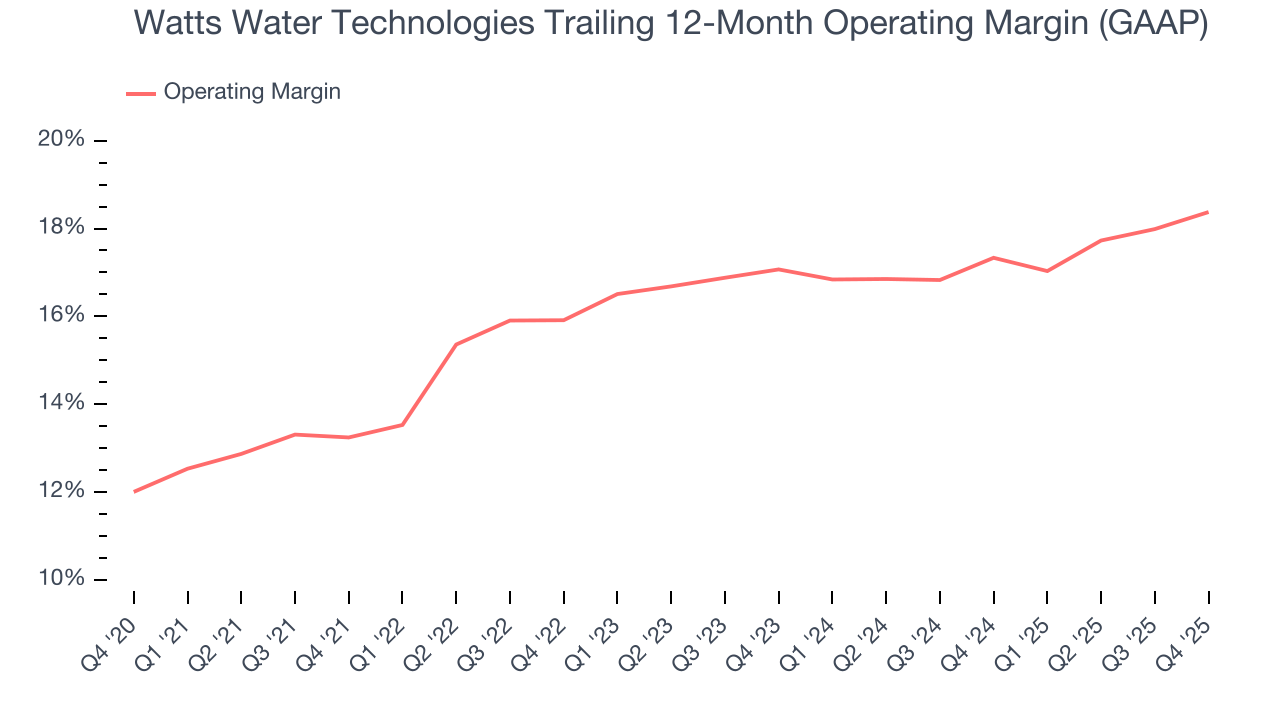

7. Operating Margin

Watts Water Technologies has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.6%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Watts Water Technologies’s operating margin rose by 5.1 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, Watts Water Technologies generated an operating margin profit margin of 18.2%, up 1.7 percentage points year on year. Since its gross margin expanded more than its operating margin, we can infer that leverage on its cost of sales was the primary driver behind the recently higher efficiency.

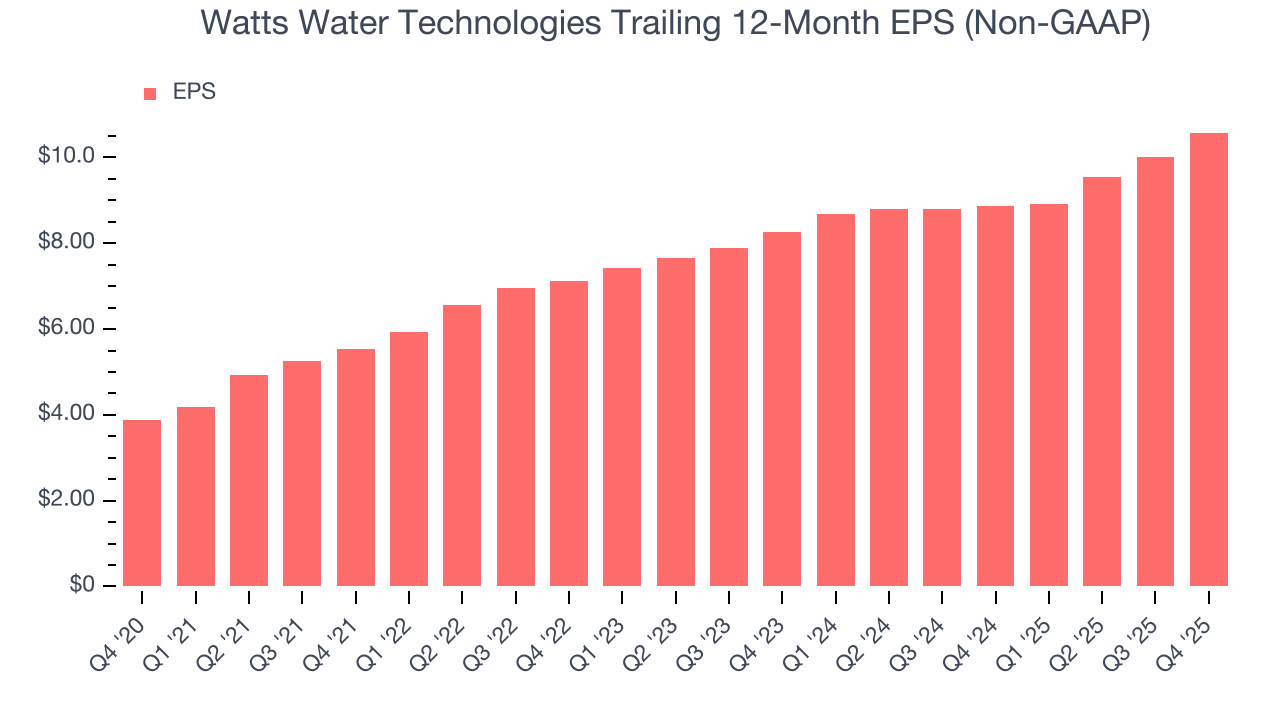

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Watts Water Technologies’s EPS grew at an astounding 22.2% compounded annual growth rate over the last five years, higher than its 10.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

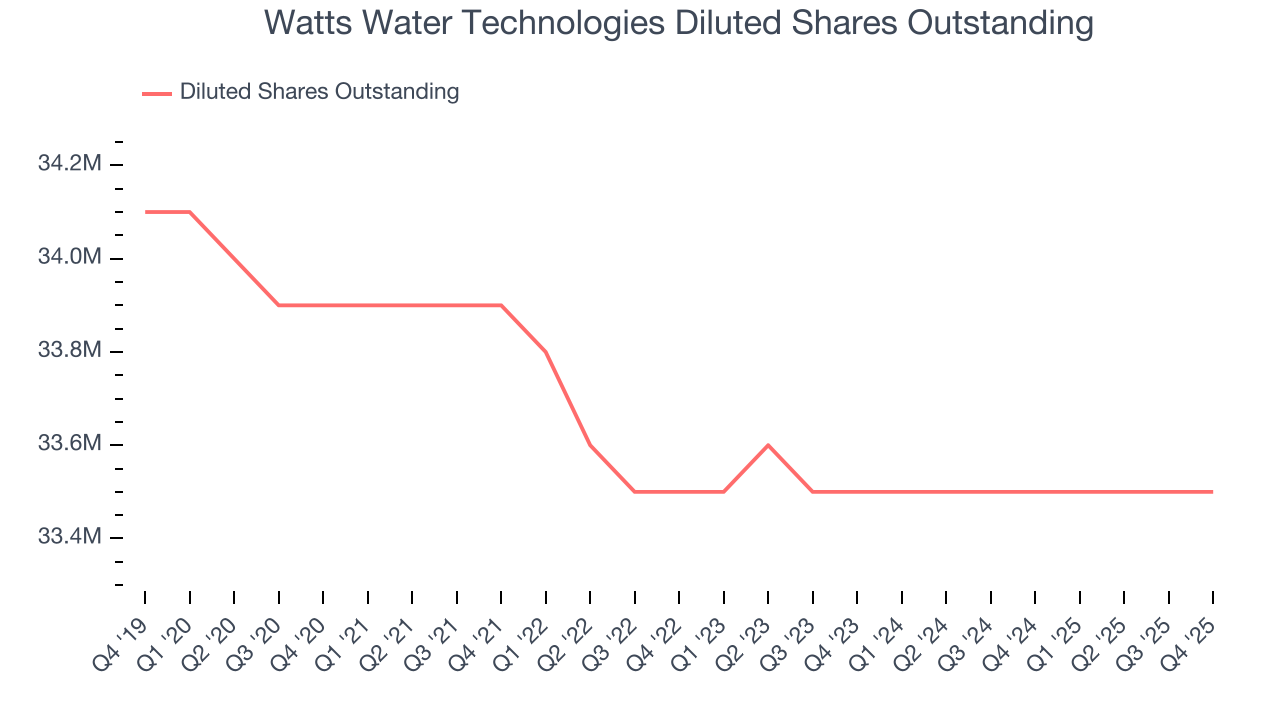

Diving into Watts Water Technologies’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Watts Water Technologies’s operating margin expanded by 5.1 percentage points over the last five years. On top of that, its share count shrank by 1.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Watts Water Technologies, its two-year annual EPS growth of 13.1% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Watts Water Technologies reported adjusted EPS of $2.62, up from $2.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Watts Water Technologies’s full-year EPS of $10.58 to grow 6.9%.

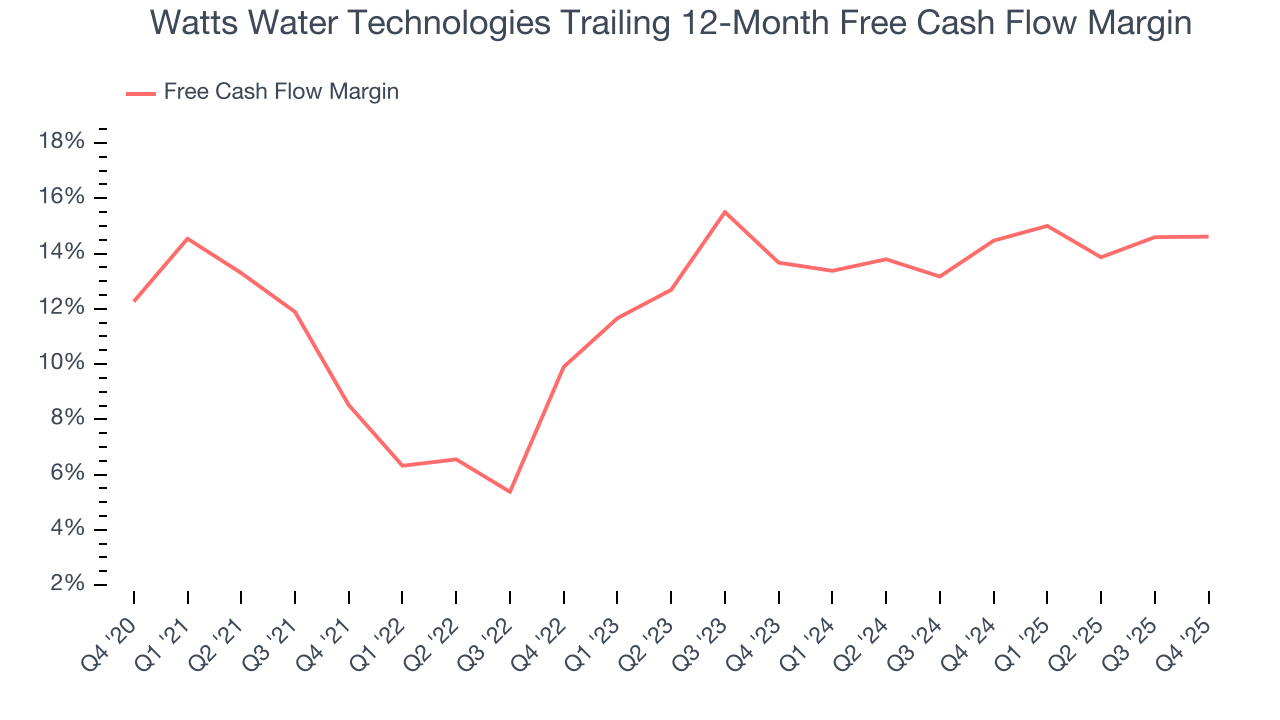

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Watts Water Technologies has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 12.5% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Watts Water Technologies’s margin expanded by 6.1 percentage points during that time. This is encouraging because it gives the company more optionality.

Watts Water Technologies’s free cash flow clocked in at $140.3 million in Q4, equivalent to a 22.4% margin. The company’s cash profitability regressed as it was 1.1 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Watts Water Technologies’s five-year average ROIC was 19.1%, placing it among the best industrials companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Uneventfully, Watts Water Technologies’s ROIC has stayed the same over the last few years. Rising returns would be ideal, but this is still a noteworthy feat since they're already high.

11. Balance Sheet Assessment

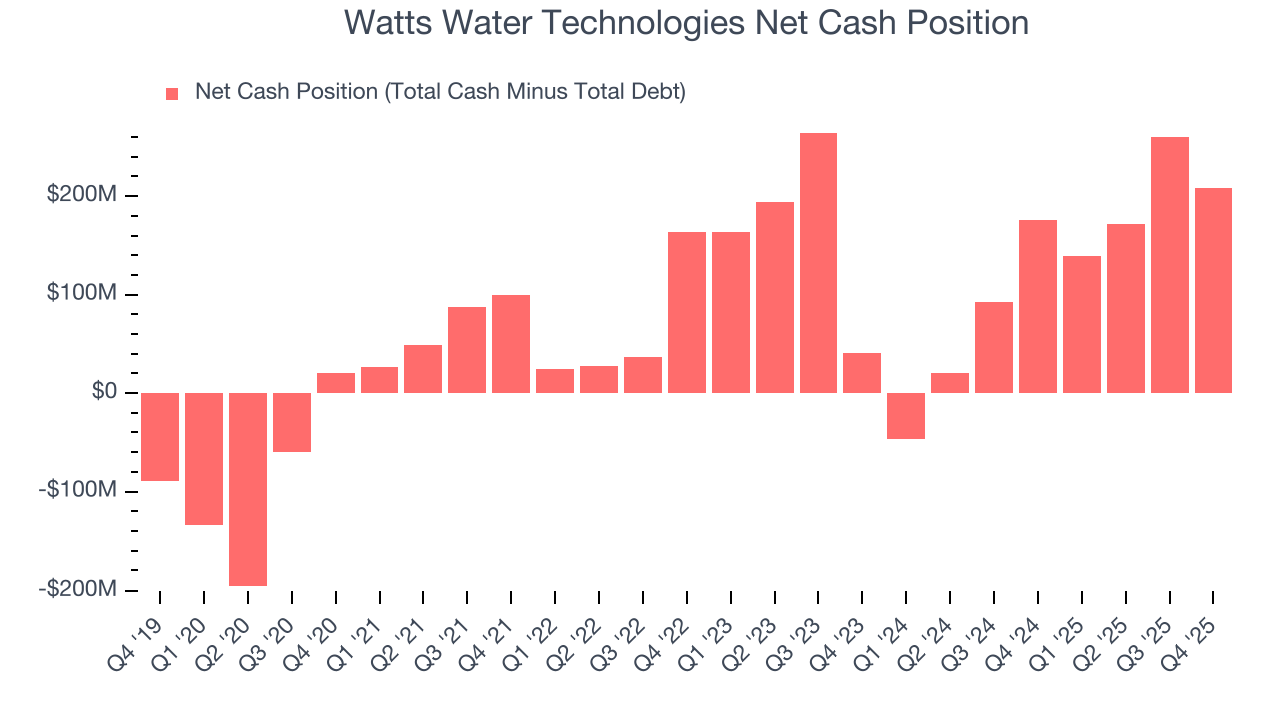

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Watts Water Technologies is a profitable, well-capitalized company with $405.5 million of cash and $197.7 million of debt on its balance sheet. This $207.8 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Watts Water Technologies’s Q4 Results

We enjoyed seeing Watts Water Technologies beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 1.9% to $320.80 immediately following the results.

13. Is Now The Time To Buy Watts Water Technologies?

Updated: March 23, 2026 at 12:12 AM EDT

When considering an investment in Watts Water Technologies, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Watts Water Technologies is a high-quality business worth owning. First, the company’s revenue growth was solid over the last five years, and analysts believe this will continue. And while its organic revenue growth has disappointed, its admirable gross margins indicate the mission-critical nature of its offerings. On top of that, Watts Water Technologies’s rising cash profitability gives it more optionality.

Watts Water Technologies’s P/E ratio based on the next 12 months is 25.1x. Looking at the industrials landscape today, Watts Water Technologies’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $338.56 on the company (compared to the current share price of $289.56), implying they see 16.9% upside in buying Watts Water Technologies in the short term.