FTI Consulting (FCN)

We’re wary of FTI Consulting. Its decelerating growth and falling cash conversion suggest it’s struggling to scale down costs as demand fades.― StockStory Analyst Team

1. News

2. Summary

Why FTI Consulting Is Not Exciting

With a team of experts deployed across 30+ countries to tackle complex business challenges, FTI Consulting (NYSE:FCN) is a global business advisory firm that helps organizations manage change, mitigate risk, and resolve disputes across financial, legal, operational, and regulatory matters.

- On the plus side, its annual revenue growth of 9% over the past five years was outstanding, reflecting market share gains this cycle

FTI Consulting is in the penalty box. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than FTI Consulting

FTI Consulting is trading at $163.48 per share, or 17.4x forward P/E. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. FTI Consulting (FCN) Research Report: Q4 CY2025 Update

Business advisory firm FTI Consulting (NYSE:FCN) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 10.7% year on year to $990.7 million. The company’s full-year revenue guidance of $4.02 billion at the midpoint came in 1.4% above analysts’ estimates. Its non-GAAP profit of $1.78 per share was 21.6% above analysts’ consensus estimates.

FTI Consulting (FCN) Q4 CY2025 Highlights:

- Revenue: $990.7 million vs analyst estimates of $918.6 million (10.7% year-on-year growth, 7.9% beat)

- Adjusted EPS: $1.78 vs analyst estimates of $1.46 (21.6% beat)

- Adjusted EBITDA: $106.2 million vs analyst estimates of $74.5 million (10.7% margin, 42.6% beat)

- Operating Margin: 9.4%, up from 5.9% in the same quarter last year

- Free Cash Flow Margin: 35.5%, up from 33.7% in the same quarter last year

- Market Capitalization: $4.84 billion

Company Overview

With a team of experts deployed across 30+ countries to tackle complex business challenges, FTI Consulting (NYSE:FCN) is a global business advisory firm that helps organizations manage change, mitigate risk, and resolve disputes across financial, legal, operational, and regulatory matters.

FTI Consulting operates through five distinct segments, each addressing different aspects of business challenges. The Corporate Finance & Restructuring segment assists clients with business transformation, strategy development, transaction support, and turnaround services for distressed situations. When a retail chain faces bankruptcy, for instance, FTI might step in to negotiate with creditors, develop a restructuring plan, and guide the company through court proceedings.

The Forensic and Litigation Consulting segment provides investigative services and expert testimony for disputes and regulatory matters. Their Data and Analytics team might analyze millions of financial transactions to identify potential fraud patterns for a banking client facing regulatory scrutiny.

Through their Economic Consulting segment, FTI delivers economic analyses for antitrust cases, financial disputes, and international arbitration. For example, when two major telecommunications companies propose a merger, FTI economists might assess potential market impacts to help regulators determine if the deal should proceed.

The Technology segment offers digital risk management and e-discovery services, helping clients manage electronic data during litigation or investigations. Their Strategic Communications practice develops messaging strategies for situations like corporate crises, leadership transitions, or major transactions.

FTI generates revenue through billable hours and project-based fees, serving Fortune 500 corporations, global banks, law firms, private equity firms, and government agencies. The company maintains offices throughout the Americas, Europe, the Middle East, Africa, and Asia-Pacific regions, allowing it to support multinational clients with cross-border matters while providing local expertise in each market.

4. Business Process Outsourcing & Consulting

The sector stands to benefit from ongoing digital transformation, increasing corporate demand for cost efficiencies, and the growing complexity of regulatory and cybersecurity landscapes. For those that invest wisely, AI and automation capabilities could emerge as competitive advantages, enhancing process efficiencies for the companies themselves as well as their clients. On the flip side, AI could be a headwind as well as the technology could lower the barrier to entry in the space and give rise to more self-service solutions. Additional challenges in the years ahead could include wage inflation for highly skilled consultants and potential regulatory scrutiny on outsourcing practices—especially in industries like finance and healthcare where who has access to certain data matters greatly.

FTI Consulting's competitors include other global professional services firms such as Alvarez & Marsal, AlixPartners, Berkeley Research Group, and segments of the Big Four accounting firms (Deloitte, EY, KPMG, and PwC) that offer advisory and consulting services.

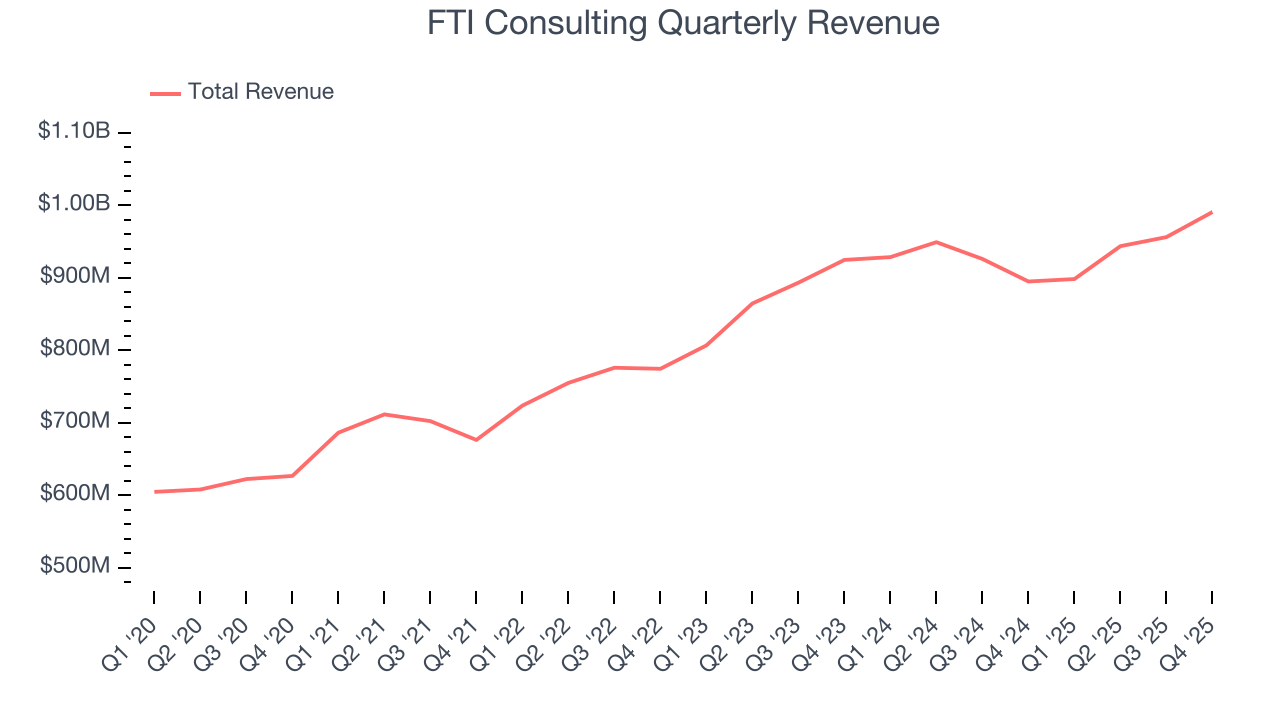

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $3.79 billion in revenue over the past 12 months, FTI Consulting is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

As you can see below, FTI Consulting’s 9% annualized revenue growth over the last five years was impressive. This shows it had high demand, a useful starting point for our analysis.

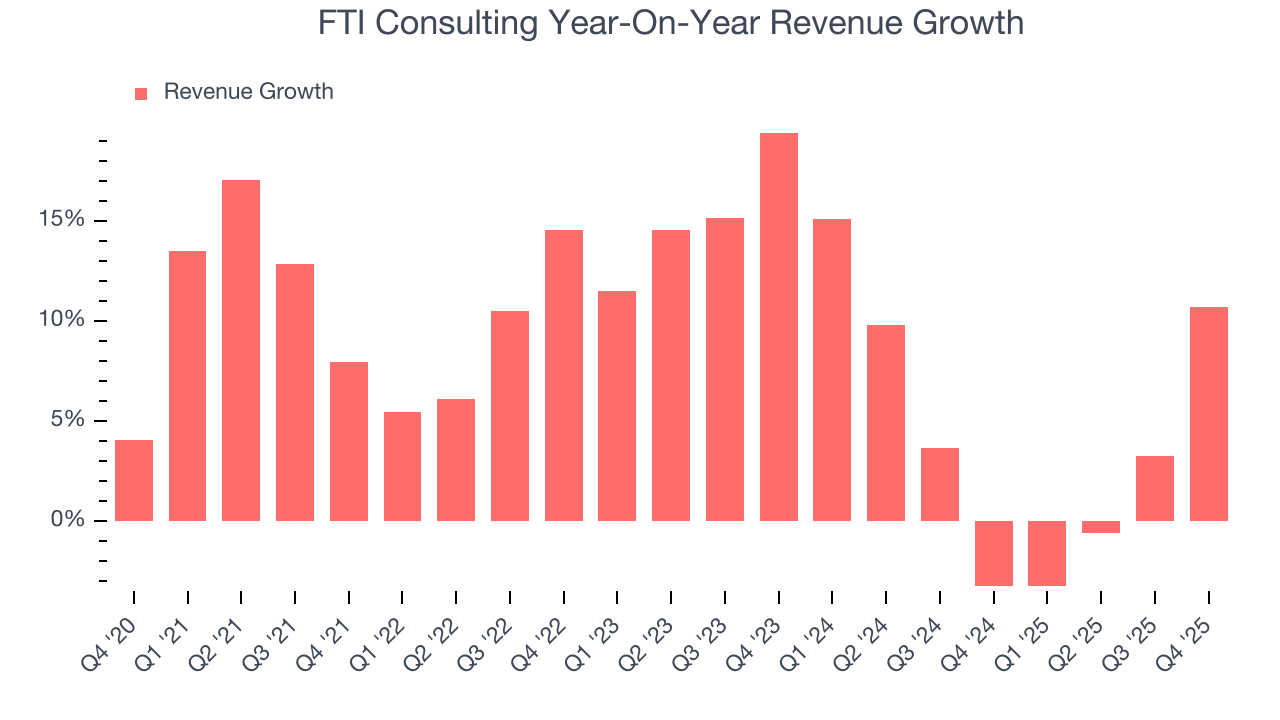

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. FTI Consulting’s recent performance shows its demand has slowed significantly as its annualized revenue growth of 4.2% over the last two years was well below its five-year trend.

This quarter, FTI Consulting reported year-on-year revenue growth of 10.7%, and its $990.7 million of revenue exceeded Wall Street’s estimates by 7.9%.

Looking ahead, sell-side analysts expect revenue to grow 4.6% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

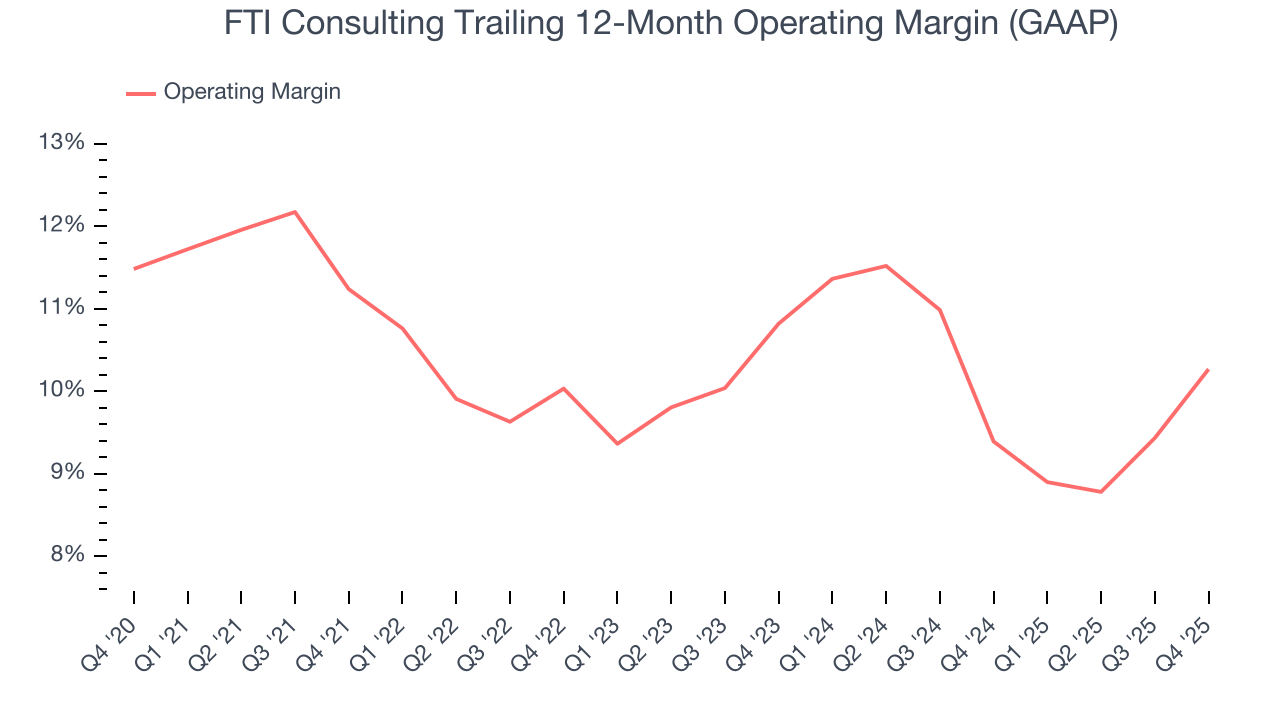

6. Operating Margin

FTI Consulting’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging 10.3% over the last five years. This profitability was higher than the broader business services sector, showing it did a decent job managing its expenses.

Analyzing the trend in its profitability, FTI Consulting’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, FTI Consulting generated an operating margin profit margin of 9.4%, up 3.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

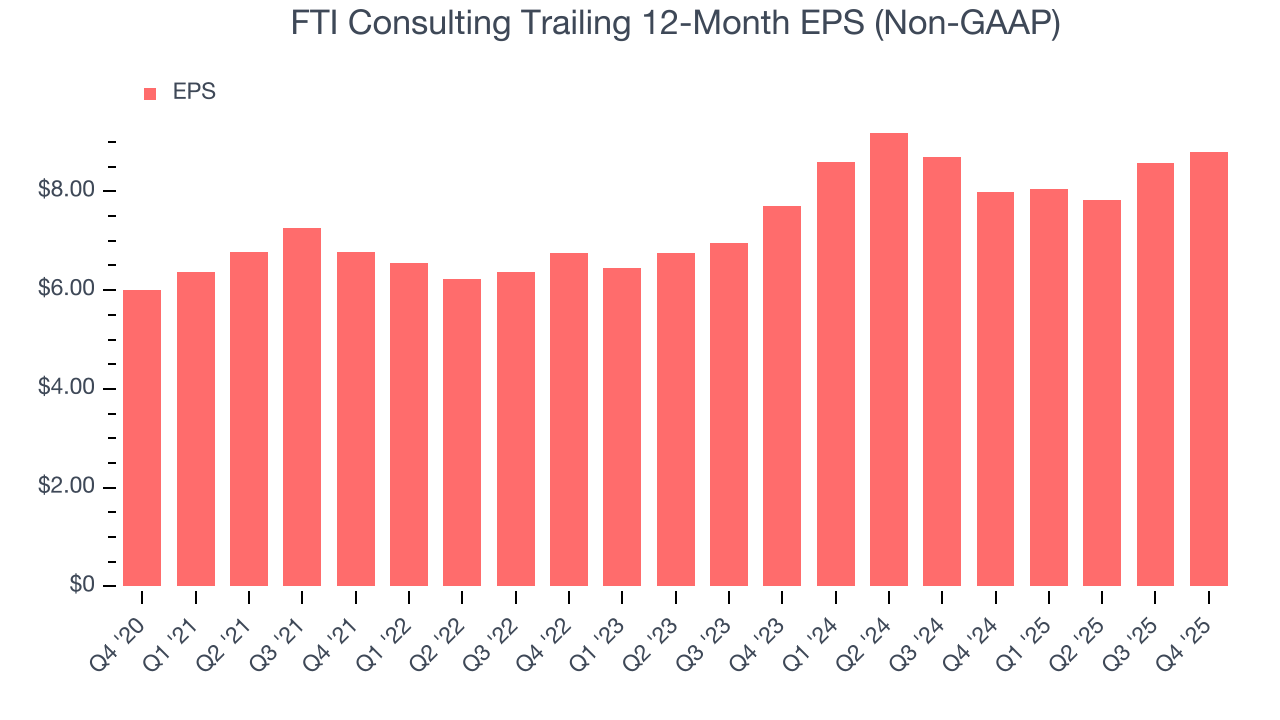

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

FTI Consulting’s decent 8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Although it wasn’t great, FTI Consulting’s two-year annual EPS growth of 6.8% topped its 4.2% two-year revenue growth.

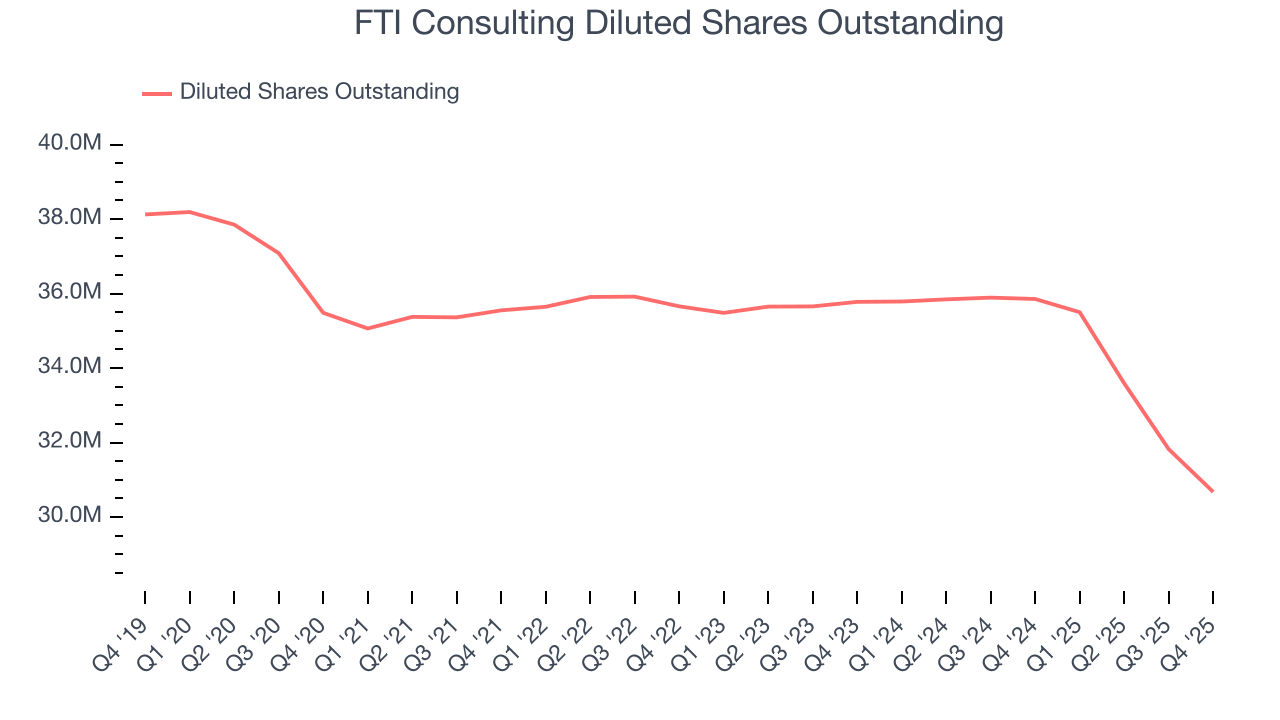

Diving into the nuances of FTI Consulting’s earnings can give us a better understanding of its performance. A two-year view shows that FTI Consulting has repurchased its stock, shrinking its share count by 14.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, FTI Consulting reported adjusted EPS of $1.78, up from $1.56 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects FTI Consulting’s full-year EPS of $8.80 to grow 6.6%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

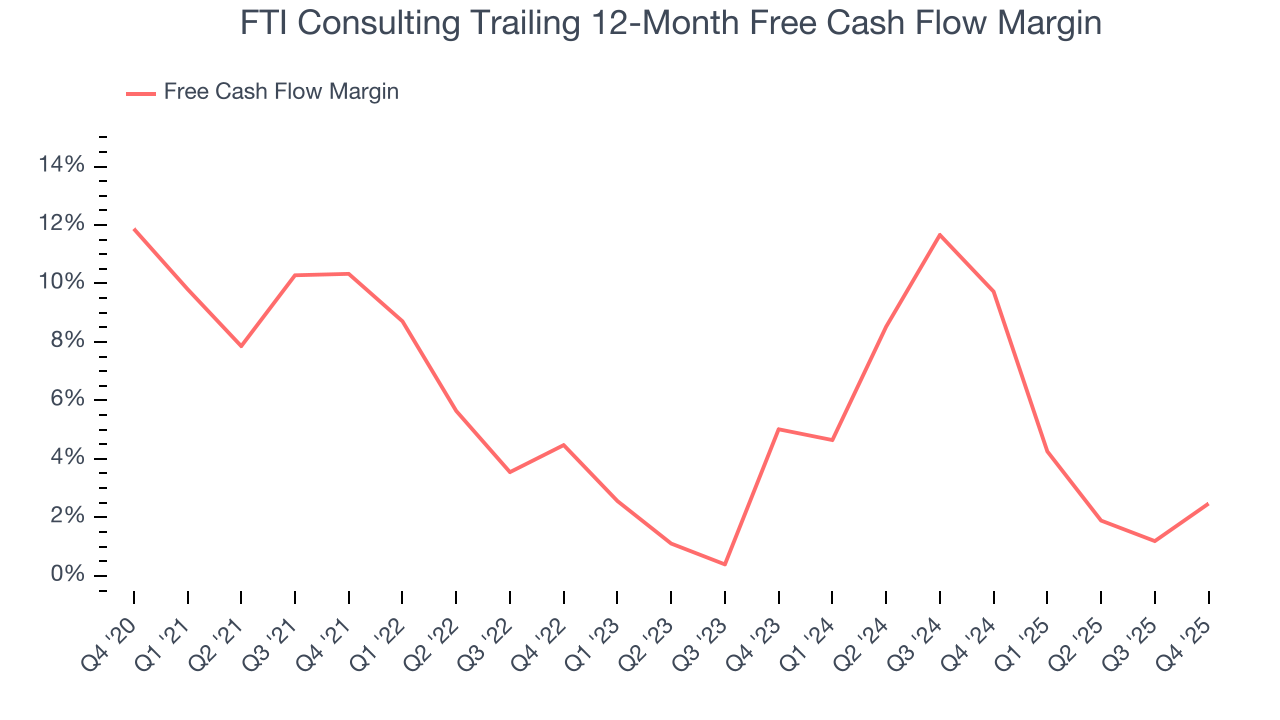

FTI Consulting has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.3% over the last five years, slightly better than the broader business services sector.

Taking a step back, we can see that FTI Consulting’s margin dropped by 7.9 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

FTI Consulting’s free cash flow clocked in at $351.4 million in Q4, equivalent to a 35.5% margin. This result was good as its margin was 1.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

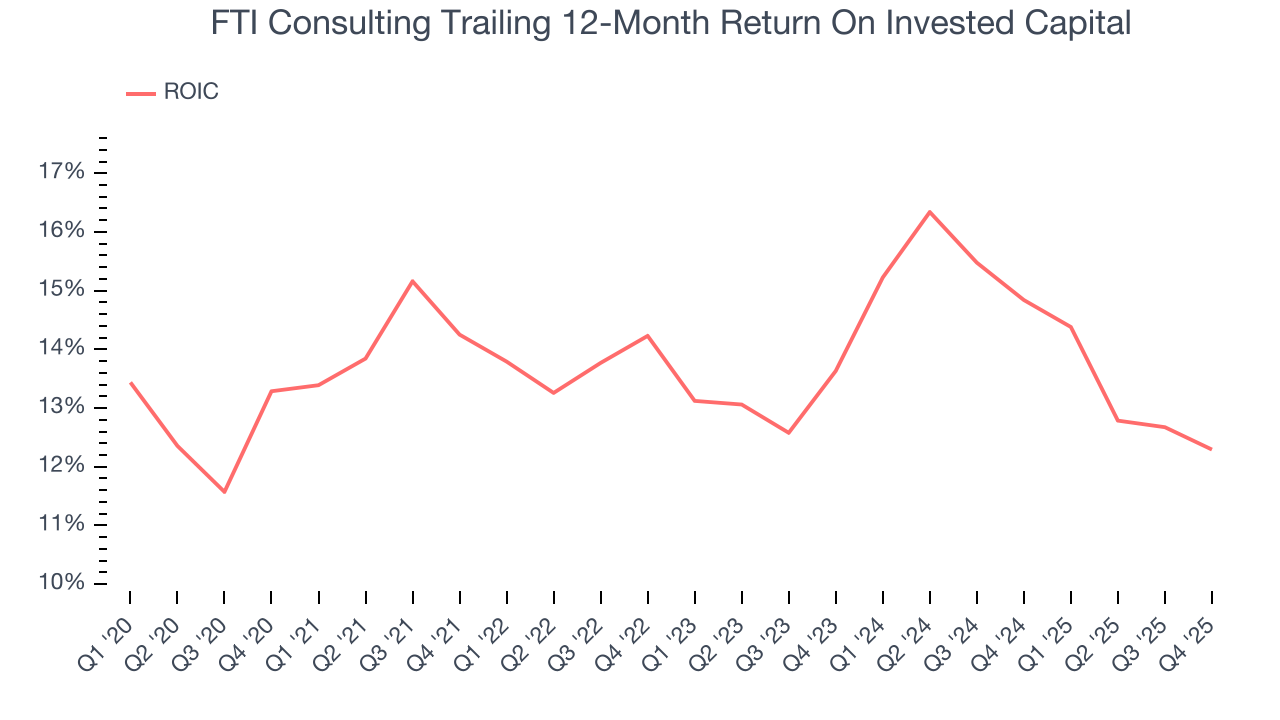

Although FTI Consulting hasn’t been the highest-quality company lately, it historically found a few growth initiatives that worked. Its five-year average ROIC was 13.8%, higher than most business services businesses.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Uneventfully, FTI Consulting’s ROIC has stayed the same over the last few years. Given the company’s underwhelming financial performance in other areas, we’d like to see its returns improve before recommending the stock.

10. Balance Sheet Assessment

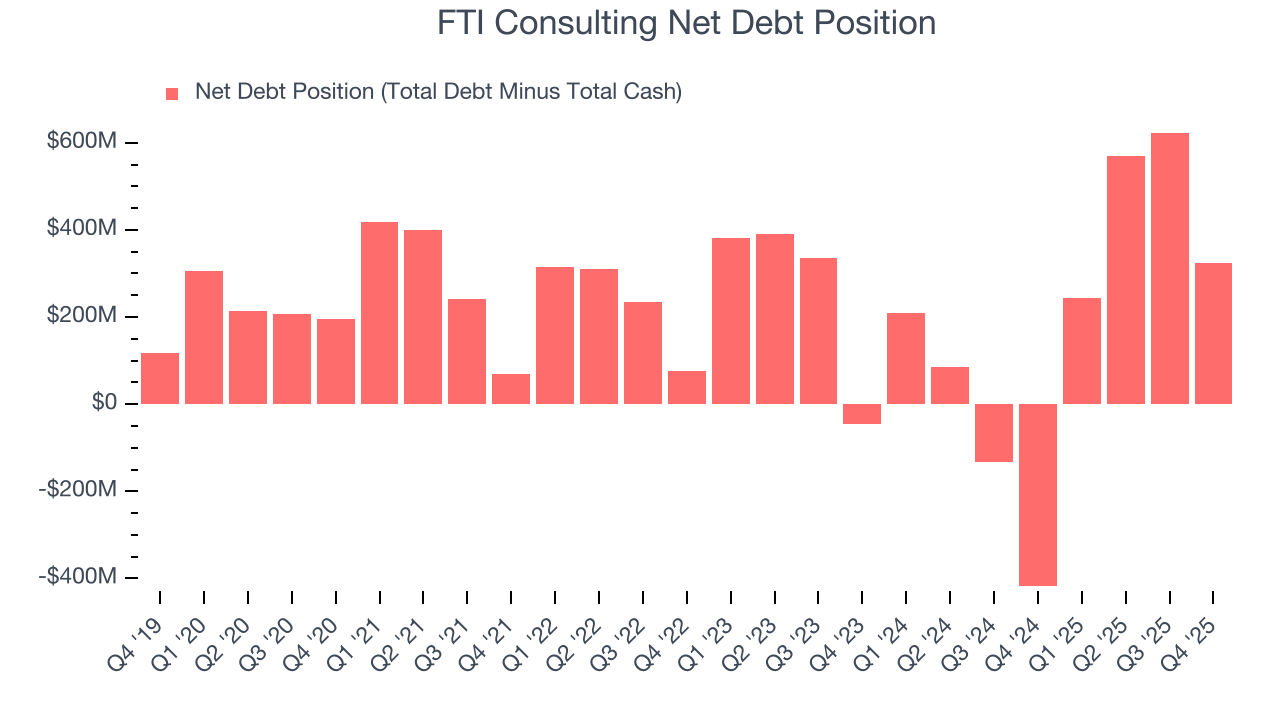

FTI Consulting reported $265.1 million of cash and $589.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $463.6 million of EBITDA over the last 12 months, we view FTI Consulting’s 0.7× net-debt-to-EBITDA ratio as safe. We also see its $2.22 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from FTI Consulting’s Q4 Results

It was good to see FTI Consulting beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock remained flat at $161.50 immediately following the results.

12. Is Now The Time To Buy FTI Consulting?

Updated: March 18, 2026 at 12:22 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

FTI Consulting’s business quality ultimately falls short of our standards. Although its revenue growth was impressive over the last five years, it’s expected to deteriorate over the next 12 months and its cash profitability fell over the last five years.

FTI Consulting’s P/E ratio based on the next 12 months is 17.4x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $174 on the company (compared to the current share price of $163.48).