Mister Car Wash (MCW)

We wouldn’t buy Mister Car Wash. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Mister Car Wash Will Underperform

Formerly known as Hotshine Holdings, Mister Car Wash (NYSE:MCW) offers car washes across the United States through its conveyorized service.

- 12.8% annual revenue growth over the last five years was slower than its consumer discretionary peers

- Earnings per share have contracted by 1.5% annually over the last four years, a headwind for returns as stock prices often echo long-term EPS performance

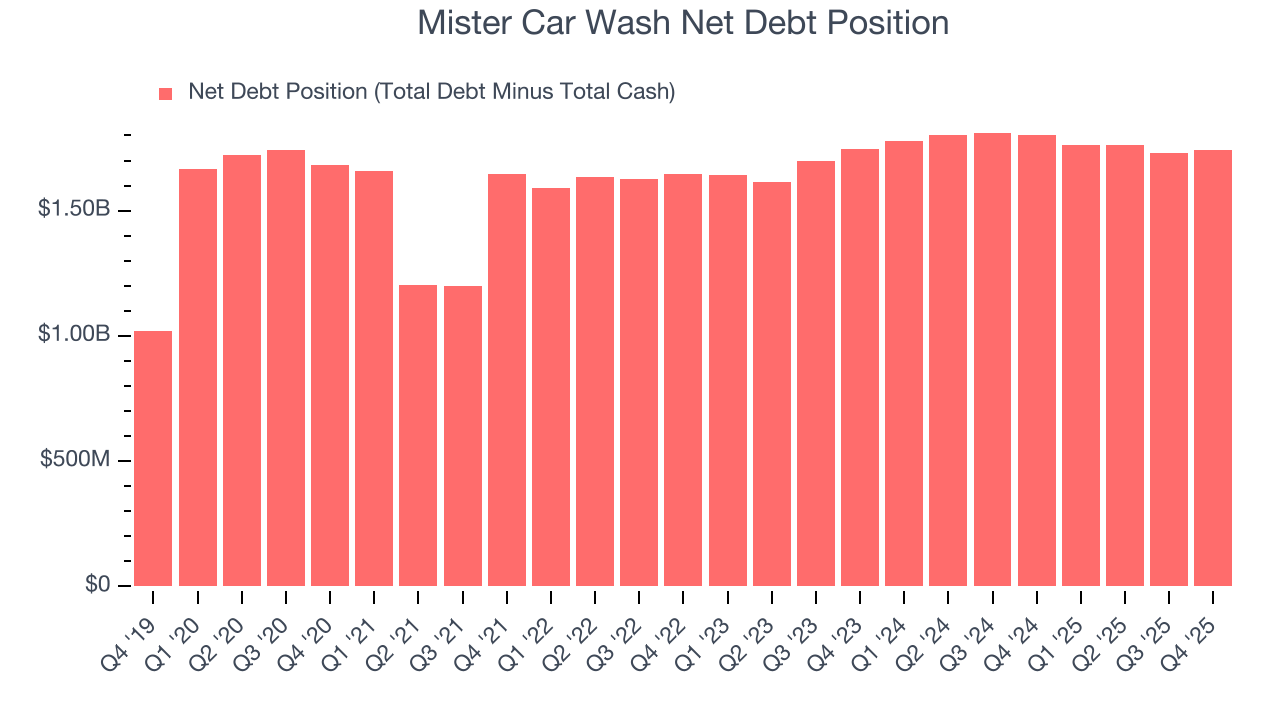

- High net-debt-to-EBITDA ratio of 5× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Mister Car Wash’s quality doesn’t meet our expectations. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Mister Car Wash

At $6.96 per share, Mister Car Wash trades at 14.6x forward P/E. Yes, this valuation multiple is lower than that of other consumer discretionary peers, but we’ll remind you that you often get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Mister Car Wash (MCW) Research Report: Q4 CY2025 Update

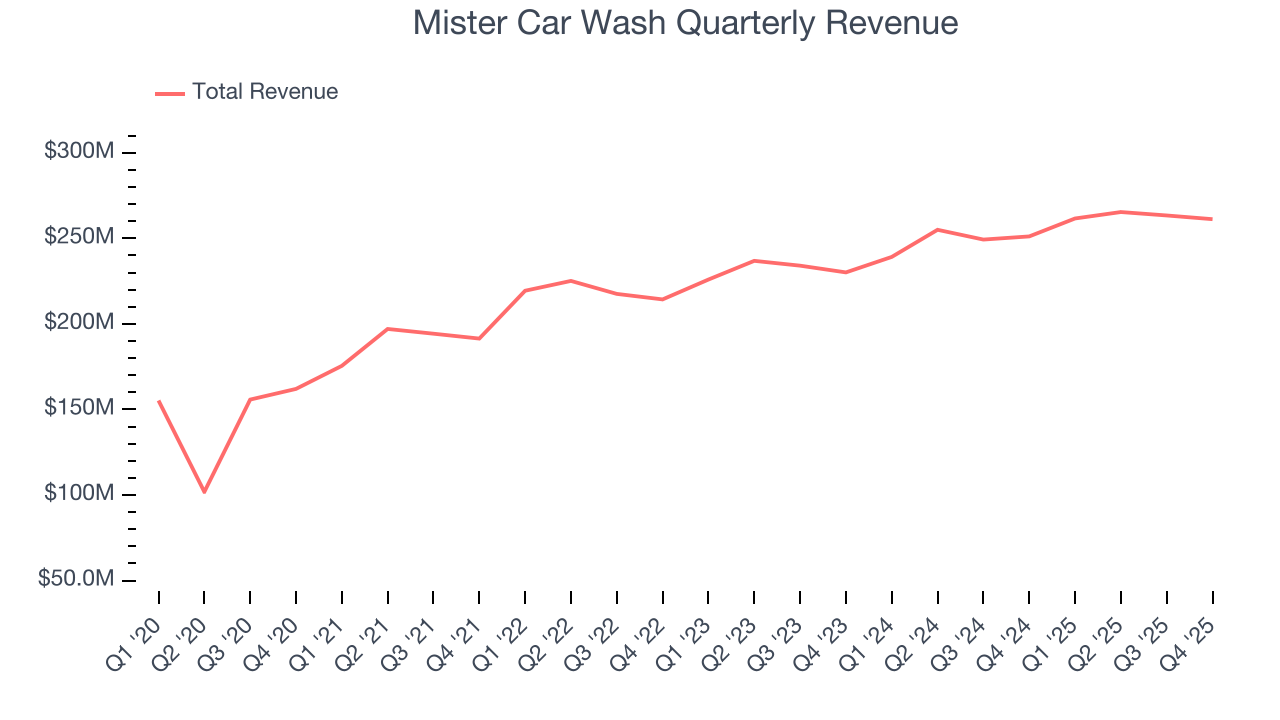

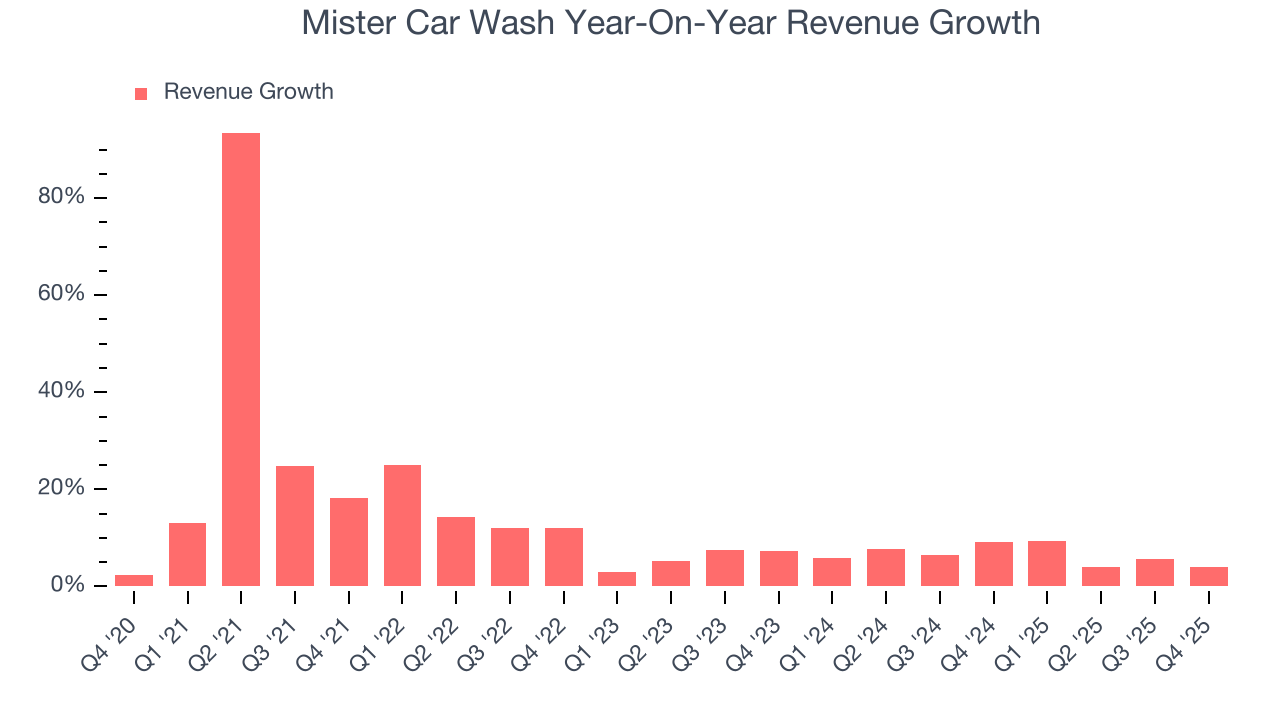

Conveyorized car wash service company Mister Car Wash (NYSE:MCW) met Wall Street’s revenue expectations in Q4 CY2025, with sales up 4% year on year to $261.2 million. Its non-GAAP profit of $0.11 per share was in line with analysts’ consensus estimates.

Mister Car Wash (MCW) Q4 CY2025 Highlights:

- Revenue: $261.2 million vs analyst estimates of $262 million (4% year-on-year growth, in line)

- Adjusted EPS: $0.11 vs analyst estimates of $0.10 (in line)

- Adjusted EBITDA: $85.96 million vs analyst estimates of $82.89 million (32.9% margin, 3.7% beat)

- Operating Margin: 15.8%, up from 12.7% in the same quarter last year

- Free Cash Flow was -$16.77 million compared to -$20.4 million in the same quarter last year

- Locations: 548 at quarter end, up from 514 in the same quarter last year

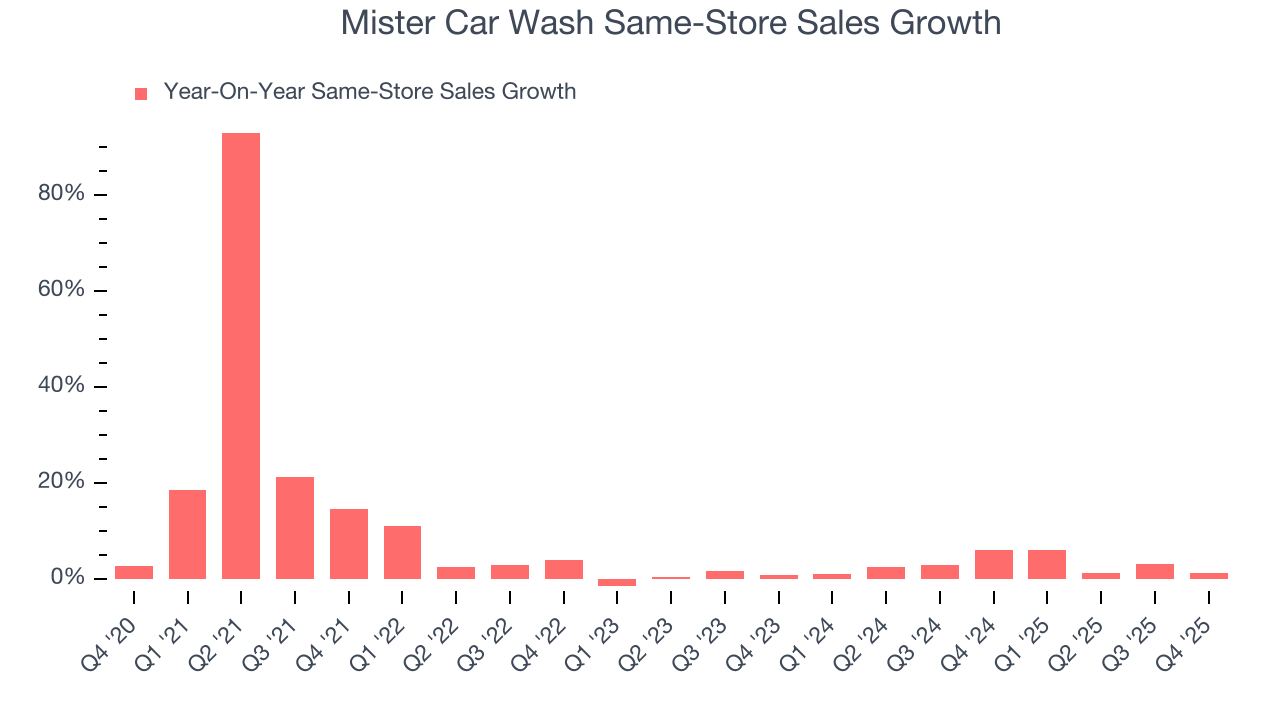

- Same-Store Sales rose 1.2% year on year (6% in the same quarter last year)

- Market Capitalization: $1.97 billion

Company Overview

Formerly known as Hotshine Holdings, Mister Car Wash (NYSE:MCW) offers car washes across the United States through its conveyorized service.

Mister Car Wash fulfills the demand for convenient car cleaning, operating strategically placed locations in urban and suburban areas such as highway interchanges to allow easy customer access.

The company offers external and internal car cleaning services. Exterior wash is fulfilled via the company’s conveyor-belt wash service, with the option for interior vacuuming and window cleaning via its full-service wash at an extra cost. Additional offerings include detailing services, such as waxing and polishing, and a subscription-based plan that gives customers access to unlimited service for a fixed monthly fee.

Mister Car Wash generates revenue through its single-use wash services, package wash service sales, and monthly subscription services. It primarily sells to individual vehicle owners through on-site sales and mobile apps. The company also serves commercial clients through direct negotiations with businesses.

4. Consumer Discretionary - Specialized Consumer Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

Competitors offering conveyorized car washes and detailing services include private companies Autobell Car Wash, Zips Car Wash, and Wash Depot Holdings.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Mister Car Wash grew its sales at a 12.8% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Mister Car Wash’s recent performance shows its demand has slowed as its annualized revenue growth of 6.5% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

Mister Car Wash also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, Mister Car Wash’s same-store sales averaged 3% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Mister Car Wash grew its revenue by 4% year on year, and its $261.2 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 6.6% over the next 12 months, similar to its two-year rate. This projection is underwhelming and suggests its newer products and services will not lead to better top-line performance yet.

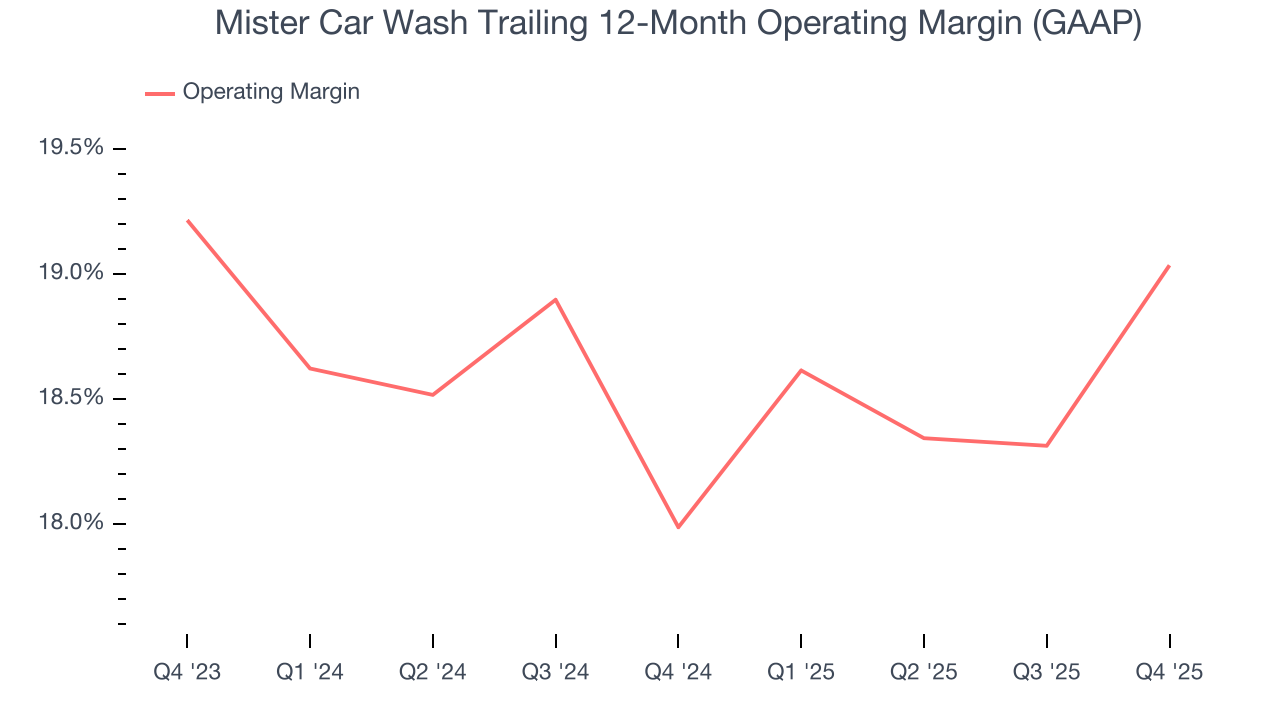

6. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Mister Car Wash’s operating margin has risen over the last 12 months and averaged 18.5% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports inadequate profitability for a consumer discretionary business.

In Q4, Mister Car Wash generated an operating margin profit margin of 15.8%, up 3.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

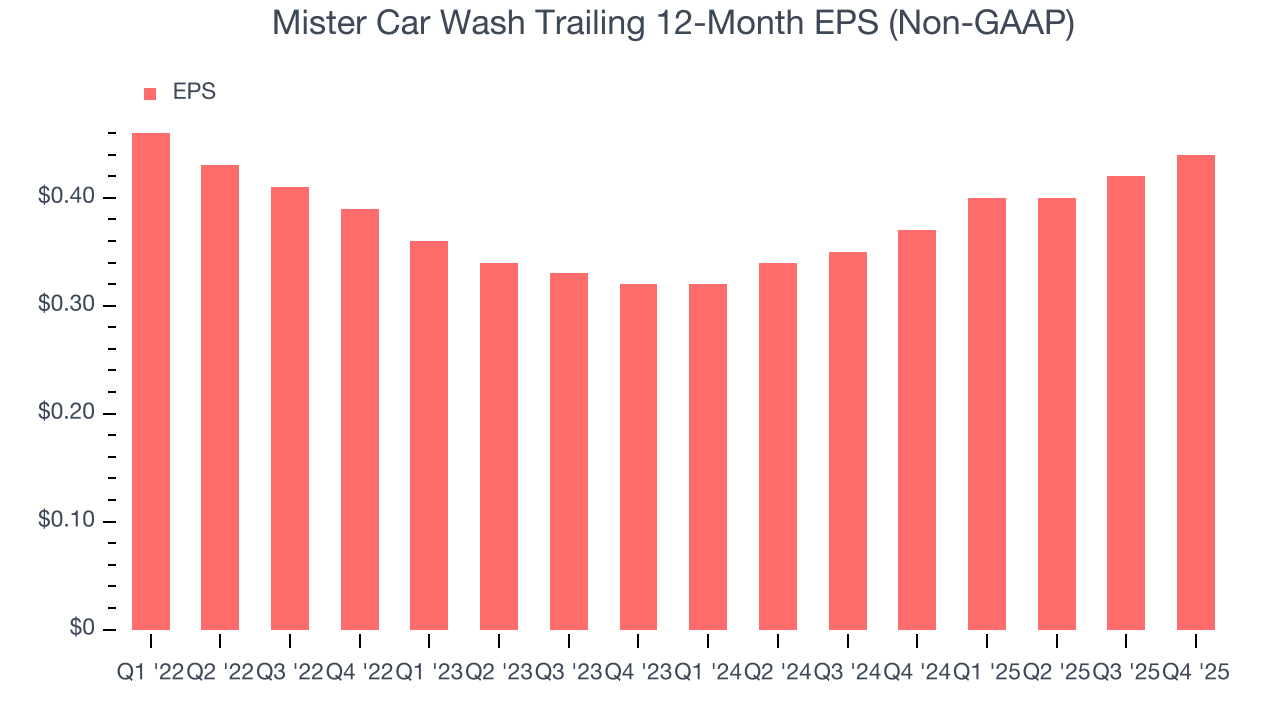

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Mister Car Wash’s full-year EPS dropped 6%, or 1.5% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. Consumer Discretionary companies are particularly exposed to this, and if the tide turns unexpectedly, Mister Car Wash’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Mister Car Wash reported adjusted EPS of $0.11, up from $0.09 in the same quarter last year. This print beat analysts’ estimates by 10%. Over the next 12 months, Wall Street expects Mister Car Wash’s full-year EPS of $0.44 to grow 7.1%.

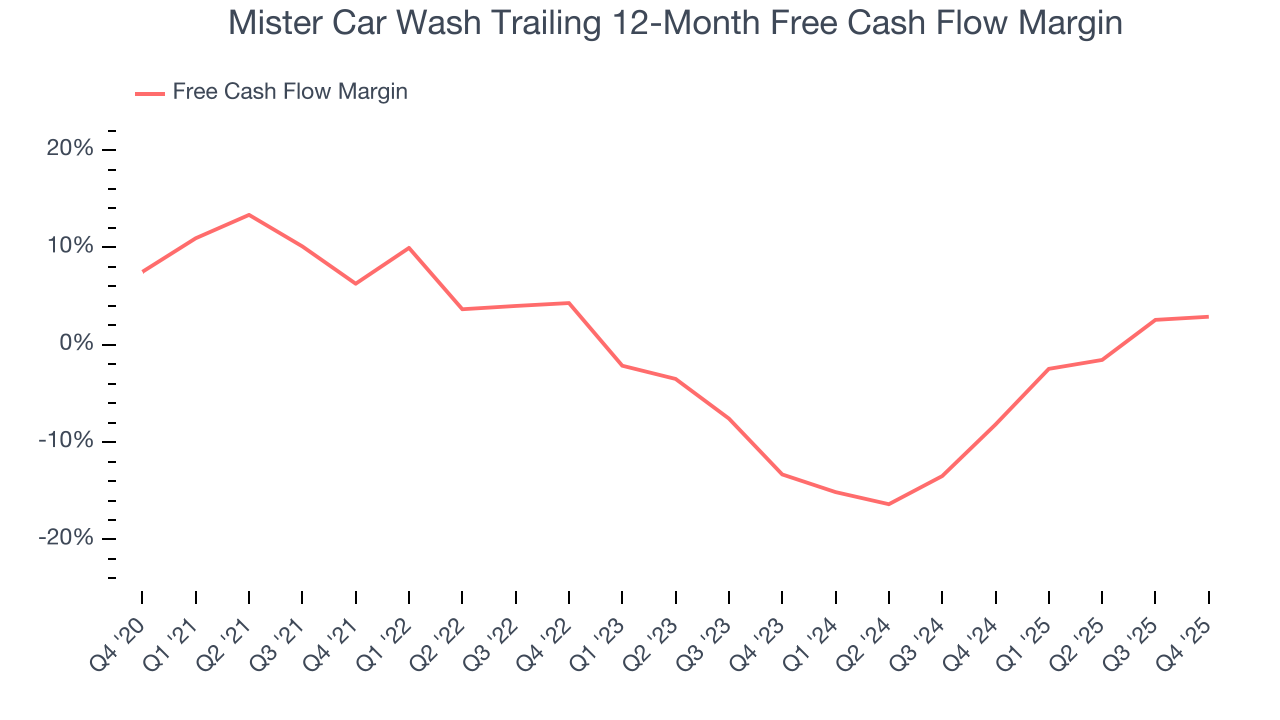

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Over the last two years, Mister Car Wash’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 2.5%, meaning it lit $2.50 of cash on fire for every $100 in revenue.

Mister Car Wash burned through $16.77 million of cash in Q4, equivalent to a negative 6.4% margin. The company’s cash burn was similar to its $20.4 million of lost cash in the same quarter last year.

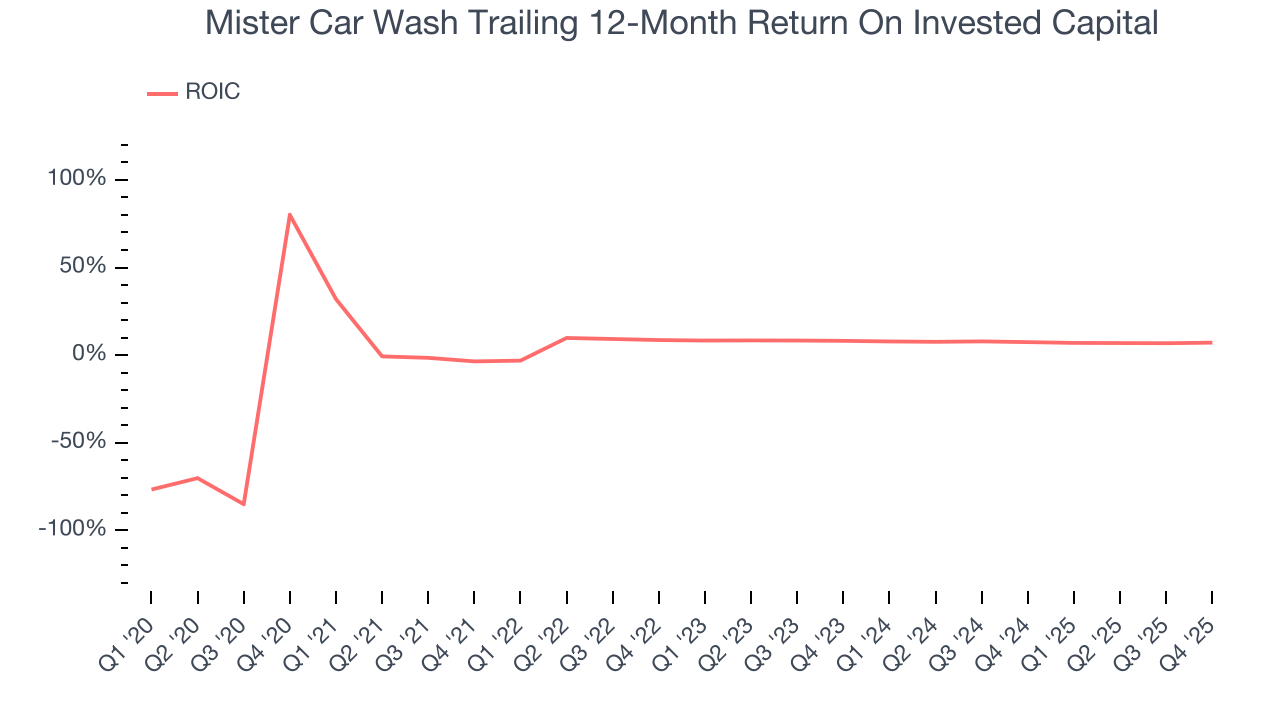

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Mister Car Wash historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.6%, somewhat low compared to the best consumer discretionary companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Mister Car Wash’s ROIC averaged 4.8 percentage point increases each year over the last few years. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Mister Car Wash’s $1.77 billion of debt exceeds the $28.45 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $345.4 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Mister Car Wash could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Mister Car Wash can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

11. Key Takeaways from Mister Car Wash’s Q4 Results

It was encouraging to see Mister Car Wash meet analysts’ EPS expectations this quarter. We were also happy its adjusted operating income outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $6.99 immediately following the results.

12. Is Now The Time To Buy Mister Car Wash?

Updated: March 13, 2026 at 10:09 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

We see the value of companies helping consumers, but in the case of Mister Car Wash, we’re out. On top of that, Mister Car Wash’s same-store sales performance has disappointed, and its declining EPS over the last four years makes it a less attractive asset to the public markets.

Mister Car Wash’s P/E ratio based on the next 12 months is 14.6x. At this valuation, there’s a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $7.06 on the company (compared to the current share price of $6.96).