New Fortress Energy (NFE)

New Fortress Energy piques our interest, but its cash burn shows it only has 4 months of runway left.― StockStory Analyst Team

1. News

2. Summary

Why New Fortress Energy Is Not Exciting

Building its first floating liquefaction unit off the coast of Mexico in 2024, New Fortress Energy (NASDAQ:NFE) supplies liquefied natural gas (LNG) to power plants and industrial customers in emerging markets.

- Negative free cash flow raises questions about the return timeline for its investments

- Unfavorable liquidity position could lead to additional equity financing that dilutes shareholders

New Fortress Energy has some respectable qualities, but we wouldn’t buy the stock until its EBITDA can comfortably support its debt.

Why There Are Better Opportunities Than New Fortress Energy

At $1.11 per share, New Fortress Energy trades at 81x forward EV-to-EBITDA. We consider this valuation aggressive considering the business fundamentals.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. New Fortress Energy (NFE) Research Report: Q2 CY2025 Update

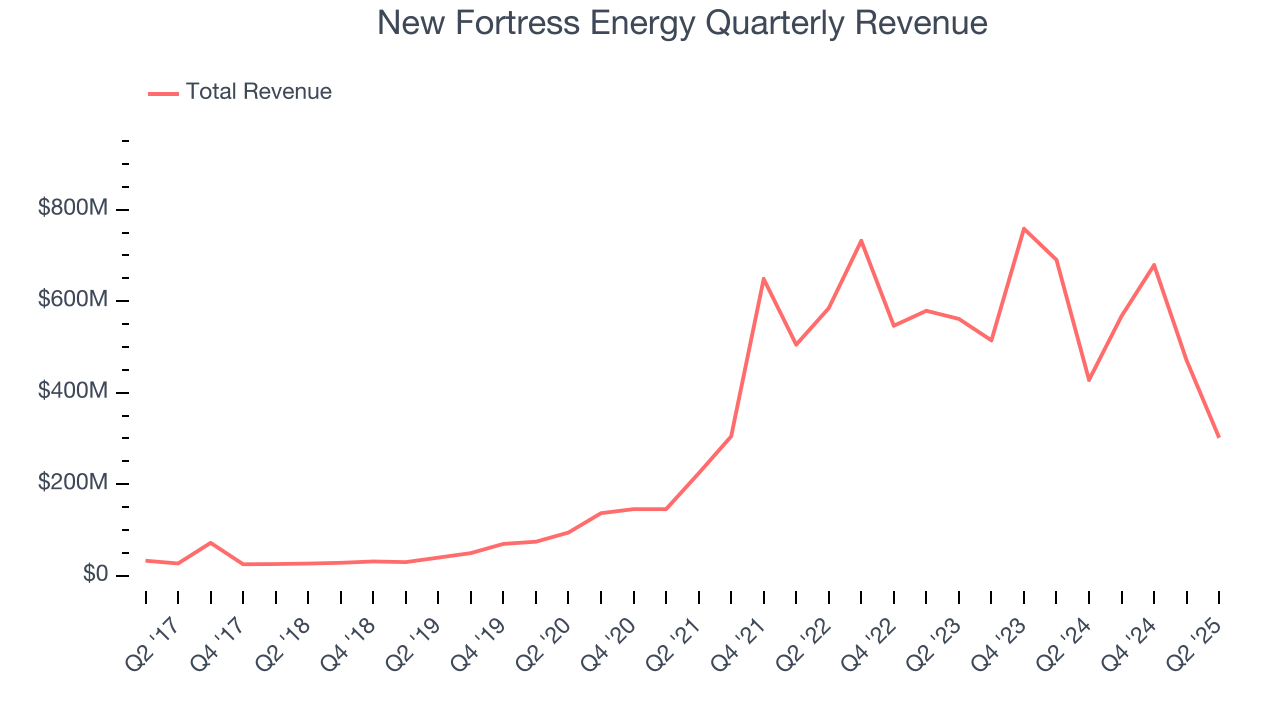

LNG infrastructure company New Fortress Energy (NASDAQ:NFE) fell short of the market’s revenue expectations in Q2 CY2025, with sales falling 29.5% year on year to $301.7 million. Its non-GAAP loss of $0.85 per share was 33.8% below analysts’ consensus estimates.

New Fortress Energy (NFE) Q2 CY2025 Highlights:

- Revenue: $301.7 million vs analyst estimates of $558.6 million (29.5% year-on-year decline, 46% miss)

- Adjusted EPS: -$0.85 vs analyst expectations of -$0.64 (33.8% miss)

- Adjusted EBITDA: -$3.66 million vs analyst estimates of $310.6 million (-1.2% margin, significant miss)

- Operating Margin: -128%, down from 10.4% in the same quarter last year

- Free Cash Flow was -$664.8 million compared to -$570 million in the same quarter last year

- Market Capitalization: $301.6 million

Company Overview

Building its first floating liquefaction unit off the coast of Mexico in 2024, New Fortress Energy (NASDAQ:NFE) supplies liquefied natural gas (LNG) to power plants and industrial customers in emerging markets.

New Fortress Energy operates an integrated energy infrastructure model that spans the entire LNG supply chain—from procurement and liquefaction to shipping, regasification, and delivery. The company sources LNG through long-term agreements with third-party suppliers and began producing its own LNG in 2024 through its first Fast LNG (FLNG) floating liquefaction facility deployed off Altamira, Mexico. This modular facility, with a capacity of 1.4 million tons per annum, uses jack-up rigs or similar marine infrastructure to enable faster deployment than traditional land-based liquefaction plants.

The company operates terminals and power facilities across the Caribbean, Latin America, and is developing projects in Ireland. Its terminals receive, store, and regasify LNG for delivery to customers. For example, its Old Harbour facility in Jamaica uses a floating storage and regasification unit (FSRU) to supply natural gas to a 190-megawatt power plant operated by South Jamaica Power Company and to New Fortress Energy's own combined heat and power plant, which provides both electricity to the grid and steam to an alumina refinery. In Puerto Rico, the company supplies natural gas and operates thermal generation assets for the island's electric utility. In Brazil, its Barcarena facility will serve an alumina refinery and support a 630-megawatt power plant under 25-year contracts.

New Fortress Energy generates revenue primarily through long-term supply contracts with utilities and industrial users, typically structured with pricing tied to natural gas indices like Henry Hub plus a fixed fee. The company also owns or leases a fleet of twelve LNG carriers and seven regasification units to transport and deliver gas. Its customer base includes government-affiliated utilities in Jamaica, Puerto Rico, and Mexico, which collectively represented nearly half of its 2024 revenue.

4. Infrastructure

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

New Fortress Energy competes with integrated LNG companies like Cheniere Energy (NYSE:LNG) and NextDecade (NASDAQ:NEXT), as well as diversified energy infrastructure firms such as Sempra Energy (NYSE:SRE).

5. Economies of Scale

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. New Fortress Energy’s $2.02 billion of revenue in the last year lacks scale in an industry where it matters.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Luckily, New Fortress Energy’s sales grew at an incredible 47.6% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Even a long stretch in Energy can be shaped by a single commodity cycle, so extending the view to ten years adds another perspective and reveals which companies are built to grow regardless of the pricing regime. New Fortress Energy’s annualized revenue growth of 37.6% over the last eight years is below its five-year trend, but we still think the results suggest decent demand.

This quarter, New Fortress Energy missed Wall Street’s estimates and reported a rather uninspiring 29.5% year-on-year revenue decline, generating $301.7 million of revenue.

7. Gross Margin

While energy gross margins can be distorted by commodity prices, hedging, and short-term cost swings, sustained margins across a full cycle reflect a producer’s underlying asset quality, infrastructure position, and cost structure.

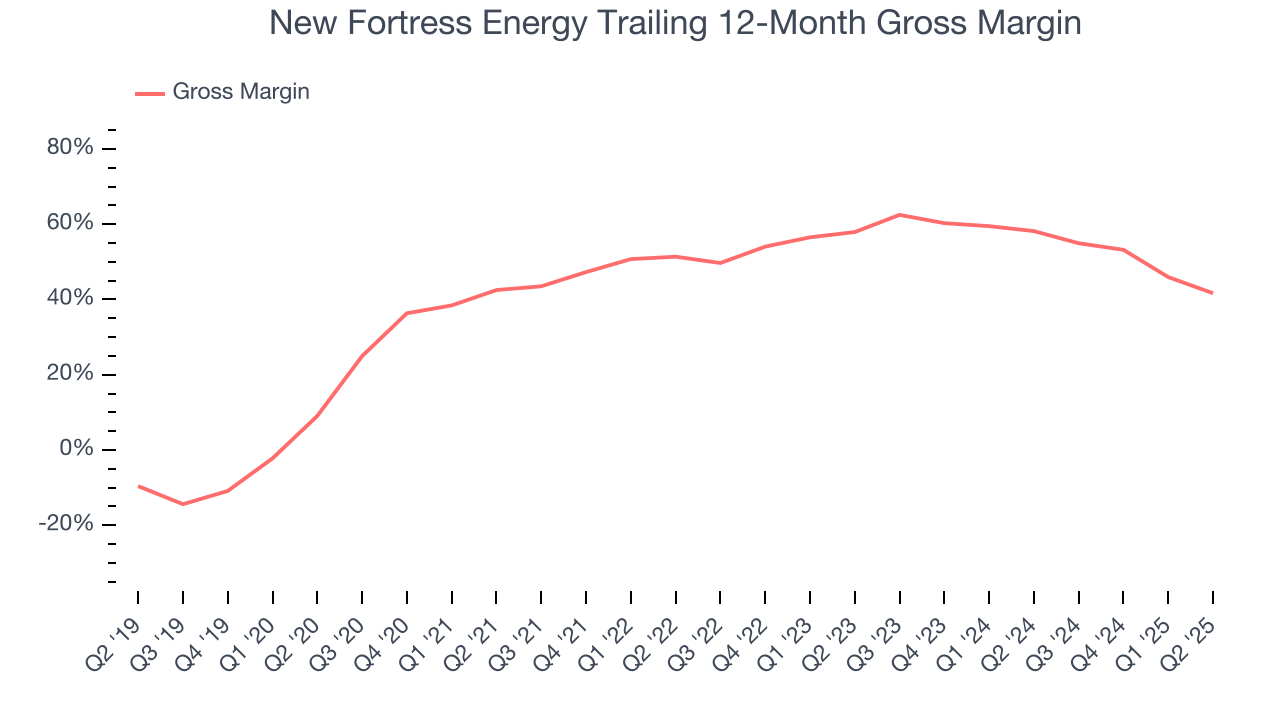

New Fortress Energy, which averaged 52.1% gross margin over the last five years, exhibits decent unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an reasonable starting point for ultimate operating profits and free cash flow generation.

New Fortress Energy produced a 19.6% gross profit margin in Q2 , marking a 28 percentage point decrease from 47.6% in the same quarter last year. Note that energy margins can be volatile due to commodity price changes.

8. Adjusted EBITDA Margin

Adjusted EBITDA margin captures the true operating profitability of an energy producer by removing accounting noise around depletion and capitalized drilling costs. It reveals how much cash the asset base generates before capital structure and reinvestment requirements shape reported earnings.

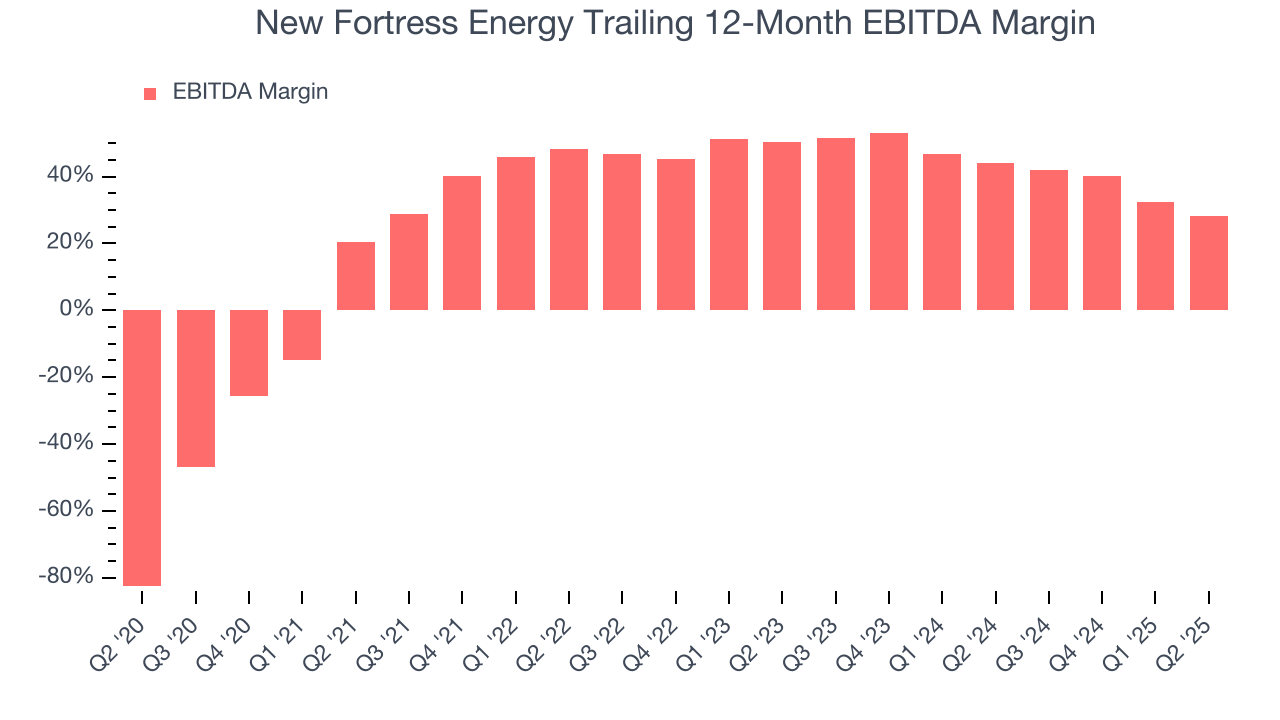

New Fortress Energy has managed its cost base well over the last five years. It demonstrated solid profitability for an upstream and integrated energy business, producing an average EBITDA margin of 41.6%.

Analyzing the trend in its profitability, New Fortress Energy’s EBITDA margin rose by 7.8 percentage points over the last year, as its sales growth gave it operating leverage.

In Q2, New Fortress Energy generated an EBITDA margin profit margin of negative 1.2%, down 29.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

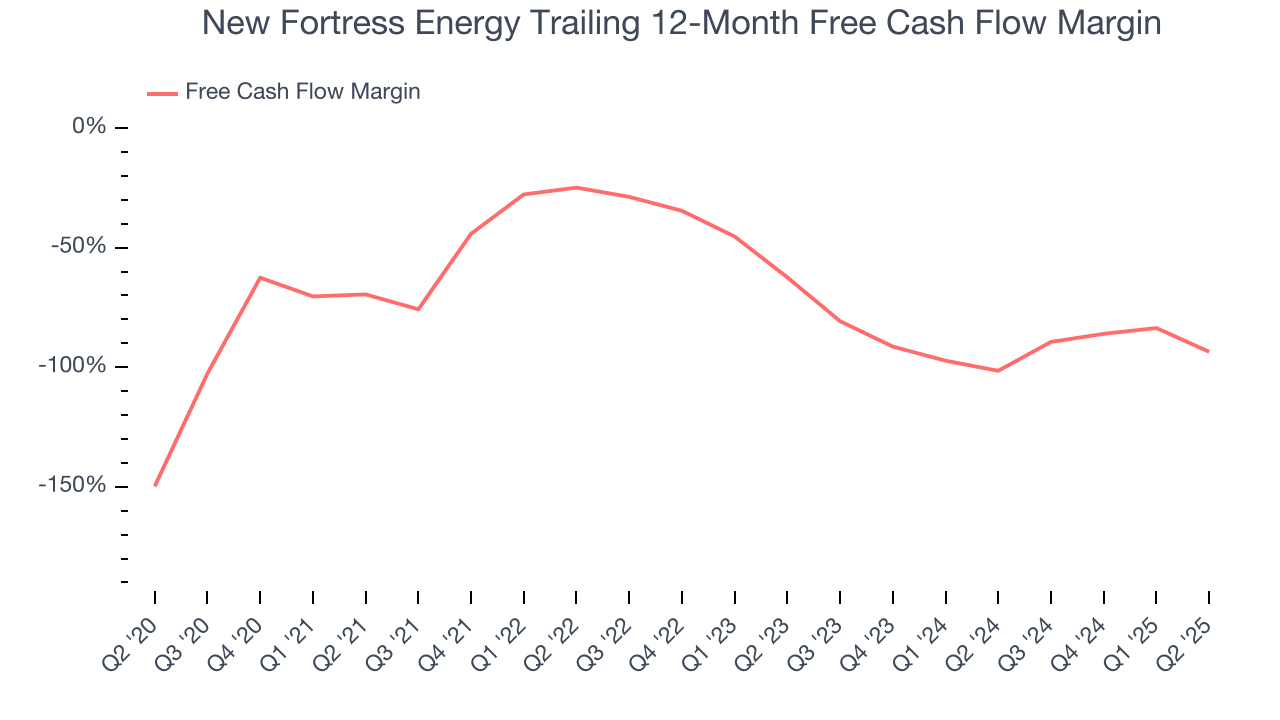

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

New Fortress Energy’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 71.3%, meaning it lit $71.26 of cash on fire for every $100 in revenue.

While the level of free cash flow margins is important, their consistency matters just as much.

New Fortress Energy’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 3.1 (lower is better), indicating excellent insulation from commodity swings. This stability supports superior capital access in downturns and positions New Fortress Energy to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of New Fortress Energy? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

New Fortress Energy burned through $664.8 million of cash in Q2, equivalent to a negative 220% margin. The company’s cash burn increased from $570 million of lost cash in the same quarter last year.

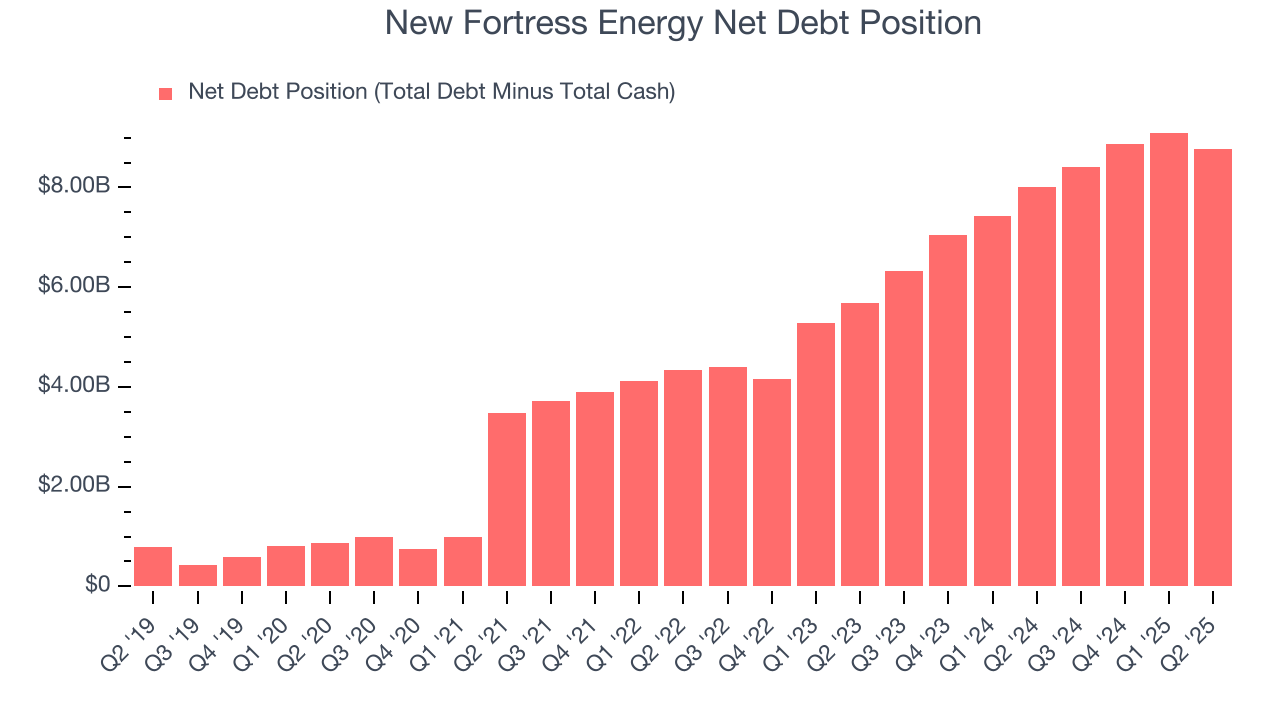

10. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

New Fortress Energy burned through $1.89 billion of cash over the last year, and its $9.33 billion of debt exceeds the $551.1 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the New Fortress Energy’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of New Fortress Energy until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

11. Key Takeaways from New Fortress Energy’s Q2 Results

We struggled to find many positives in these results. Its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $1.07 immediately following the results.

12. Is Now The Time To Buy New Fortress Energy?

Updated: March 17, 2026 at 1:18 AM EDT

Before making an investment decision, investors should account for New Fortress Energy’s business fundamentals and valuation in addition to what happened in the latest quarter.

New Fortress Energy is a pretty good company if you ignore its balance sheet. First of all, the company’s revenue growth over the last five years was top-tier for the sector. And while its cash burn raises the question of whether it can sustainably maintain growth, its revenue growth over the last eight years was top-tier for the sector. Additionally, New Fortress Energy’s free cash flowvolatility compared to commodity price volatility is very low, demonstrating top-tier free cash flow stability.

New Fortress Energy’s EV-to-EBITDA ratio based on the next 12 months is 81x. Despite its notable business characteristics, we’d hold off for now because its balance sheet concerns us. We recommend investors interested in the company wait until it reduces its leverage or increases its profits before getting involved.

Wall Street analysts have a consensus one-year price target of $3.50 on the company (compared to the current share price of $1.11).