Tenaris (TEN)

We’re skeptical of Tenaris. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Tenaris Is Not Exciting

Operating industrial facilities across the Americas, Europe, Middle East, and Asia, Tenaris (NYSE:TEN) manufactures seamless and welded steel pipes used in oil and gas drilling and transportation.

- 2.1% annual revenue growth over the last five years was slower than its energy upstream and integrated energy peers

- Modest revenue base of $764.8 million gives it less fixed cost leverage and fewer distribution channels than larger companies

- On the plus side, its EBITDA profits and efficiency rose over the last five years as it benefited from some fixed cost leverage

Tenaris lacks the business quality we seek. We’d search for superior opportunities elsewhere.

Why There Are Better Opportunities Than Tenaris

Tenaris’s stock price of $33.76 implies a valuation ratio of 4.7x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Tenaris (TEN) Research Report: Q3 CY2025 Update

Steel pipe manufacturer Tenaris (NYSE:TEN) reported Q3 CY2025 results topping the market’s revenue expectations, but sales fell by 7% year on year to $186.2 million. Its non-GAAP profit of $0.75 per share was 21% above analysts’ consensus estimates.

Tenaris (TEN) Q3 CY2025 Highlights:

- Revenue: $186.2 million vs analyst estimates of $162.2 million (7% year-on-year decline, 14.8% beat)

- Adjusted EPS: $0.75 vs analyst estimates of $0.62 (21% beat)

- Adjusted EBITDA: $95.57 million vs analyst estimates of $92.56 million (51.3% margin, 3.3% beat)

- Operating Margin: 27.7%, in line with the same quarter last year

- Market Capitalization: $1.05 billion

Company Overview

Operating industrial facilities across the Americas, Europe, Middle East, and Asia, Tenaris (NYSE:TEN) manufactures seamless and welded steel pipes used in oil and gas drilling and transportation.

The company's primary products are oil country tubular goods (OCTG), which include casing pipes that support well walls during drilling and tubing pipes that transport oil and gas to the surface after drilling completes. It also produces line pipes that carry crude oil and natural gas from wells to refineries and distribution centers, along with mechanical and structural pipes for industrial applications. A distinguishing feature of Tenaris's offering is its premium connections—specially engineered joints and couplings that link pipe sections together for use in high-pressure or high-temperature drilling environments, marketed under the TenarisHydril brand following its acquisition of Hydril's premium connections business.

The company serves major international and national oil companies through what it calls "Rig Direct" services, where it manages the entire supply chain from manufacturing to delivery at the drilling rig. Under long-term agreements with customers like Saudi Aramco, Abu Dhabi National Oil Company (ADNOC), YPF in Argentina, and Pemex in Mexico, Tenaris coordinates its global production network with customers' drilling schedules, reducing inventory requirements and providing technical support. For example, an operator drilling in the Permian Basin might contract with Tenaris to deliver threaded and coupled casing pipes directly to multiple rig sites as drilling progresses, with the company monitoring usage patterns and adjusting shipments in real time.

Tenaris generates revenue primarily from selling pipes and related products to oil and gas companies, though it also supplies pipes for geothermal wells, hydrogen storage and transportation infrastructure, and carbon capture projects. The company operates seamless pipe mills in locations including Bay City, Texas; Campana, Argentina; Veracruz, Mexico; and Dalmine, Italy, as well as welded pipe facilities in countries like Brazil, Colombia, and Saudi Arabia. Through its 2023 acquisition of Mattr's pipe coating business, Tenaris added anti-corrosion and thermal insulation coating capabilities for offshore and onshore pipelines. It also provides complementary oilfield services such as hydraulic fracturing in Argentina and manufactures sucker rods used in oil extraction.

4. Infrastructure

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

Tenaris competes with Vallourec (OTCMKTS:VLOUF), U.S. Steel (NYSE:X), Japan's Nippon Steel Corporation and JFE Holdings, Russia's TMK, ArcelorMittal (NYSE:MT), and welded pipe producers including South Korea's SeAH Steel and India's JSW Group.

5. Revenue Scale

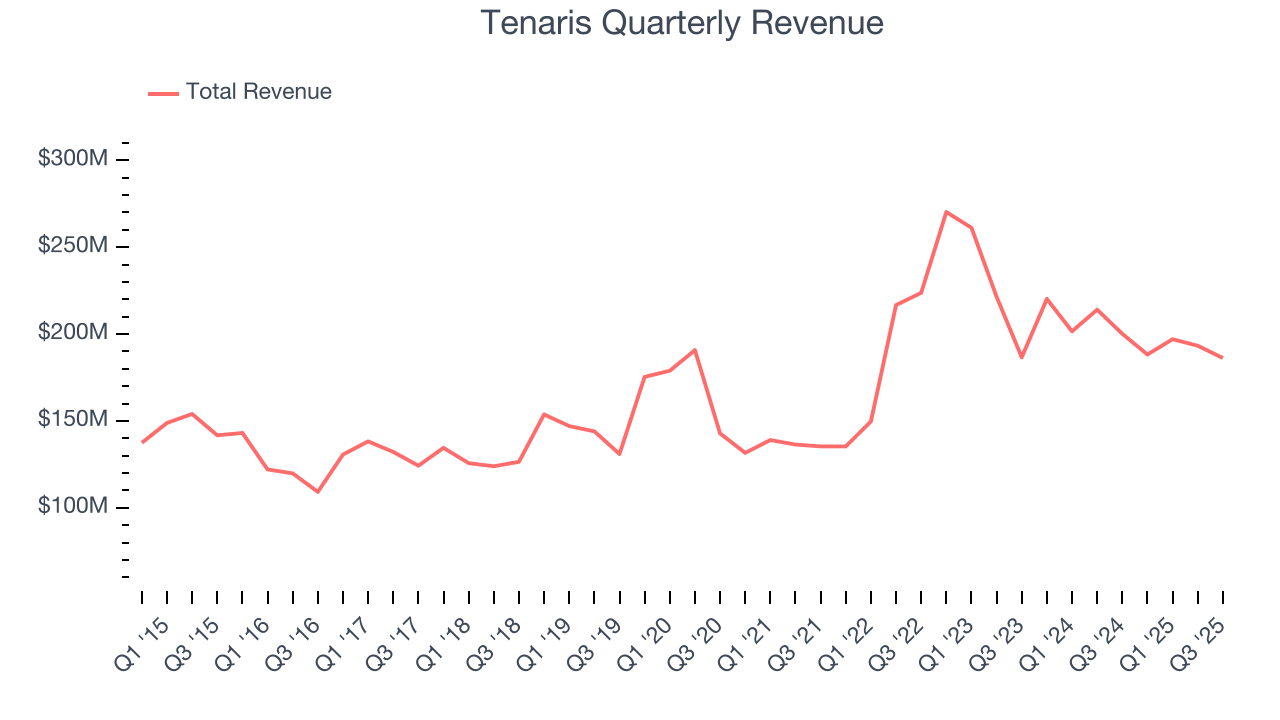

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. Tenaris’s $764.8 million of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night. is a small company in an industry where scale matters.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Unfortunately, Tenaris’s 2.1% annualized revenue growth over the last five years was weak. This was below our standards and is a rough starting point for our analysis.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Tenaris’s annualized revenue growth of 2.8% over the last ten years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Tenaris’s revenue fell by 7% year on year to $186.2 million but beat Wall Street’s estimates by 14.8%.

7. Gross Margin

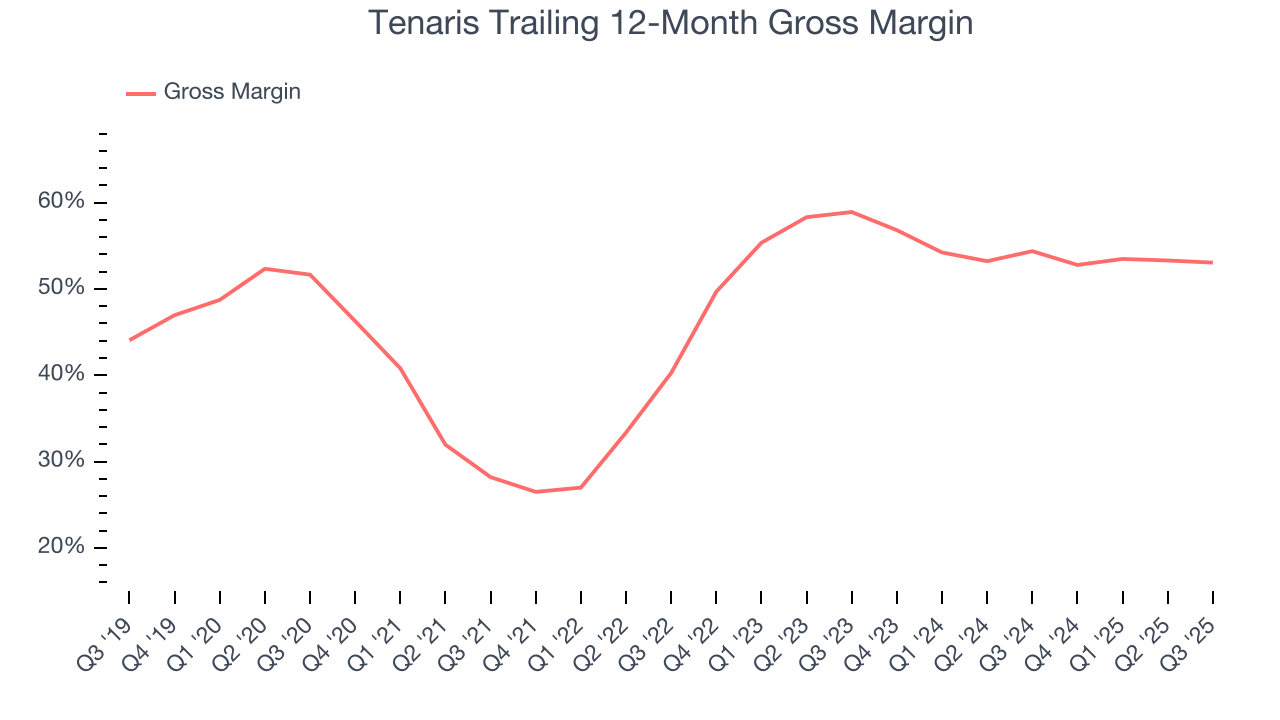

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Tenaris, which averaged 48.8% gross margin over the last five years, exhibits mediocre unit economics in the sector. Energy companies with higher gross margins are more likely to remain profitable when commodity prices decline.

Tenaris produced a 55.4% gross profit margin in Q3, in line with the same quarter last year.

8. Adjusted EBITDA Margin

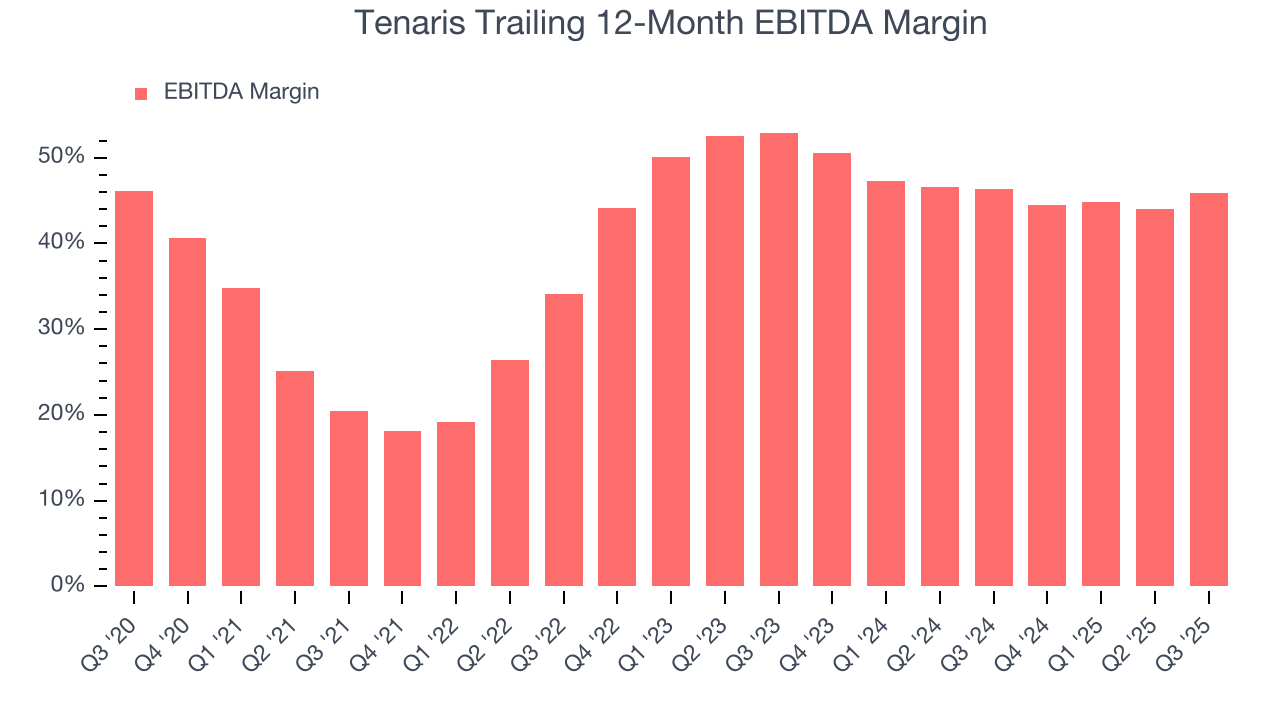

Tenaris has managed its cost base well over the last five years. It demonstrated solid profitability for an upstream and integrated energy business, producing an average EBITDA margin of 41.9%.

Looking at the trend in its profitability, Tenaris’s EBITDA margin rose by 25.4 percentage points over the last year, as its sales growth gave it immense operating leverage.

In Q3, Tenaris generated an EBITDA margin profit margin of 51.3%, up 7.5 percentage points year on year. This increase was a welcome development, especially since its revenue fell, showing it was more efficient because it scaled down its expenses. This adjusted EBITDA beat Wall Street’s estimates by 1.1%.

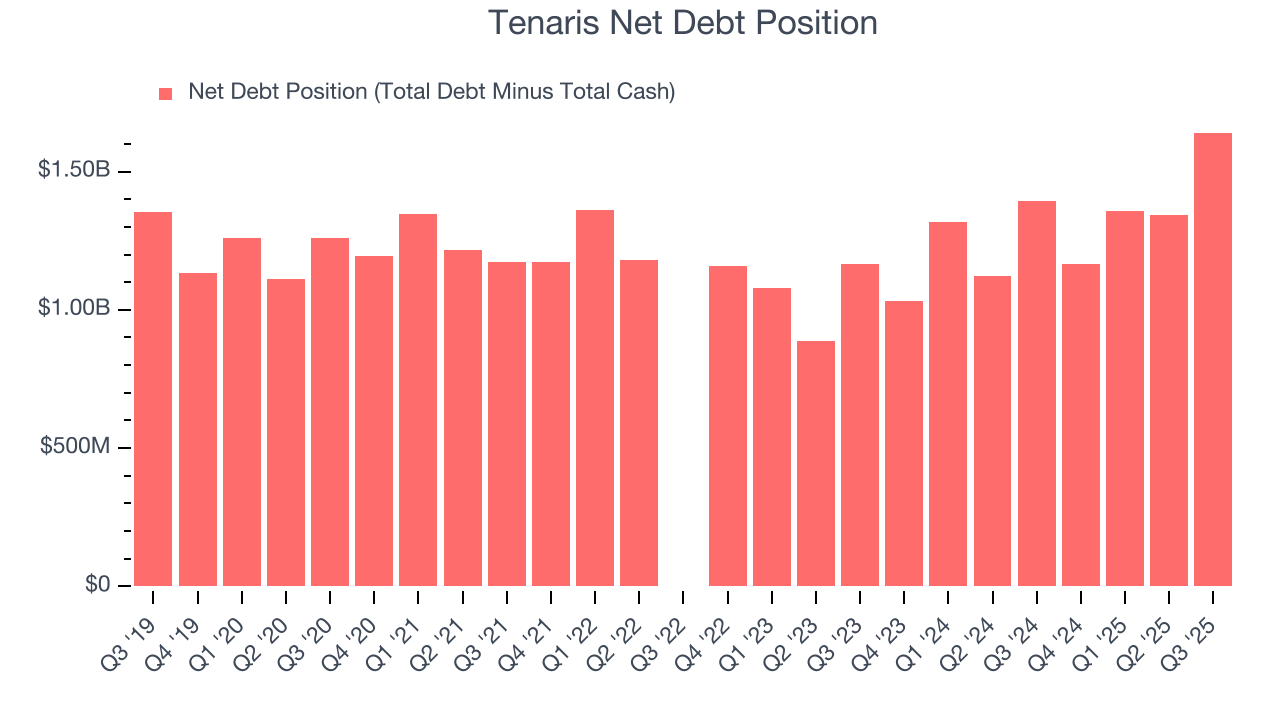

9. Balance Sheet Assessment

Tenaris reported $264.3 million of cash and $1.91 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $350.6 million of EBITDA over the last 12 months, we view Tenaris’s 4.7× net-debt-to-EBITDA ratio as safe. We also see its $86.55 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from Tenaris’s Q3 Results

We were impressed by how significantly Tenaris blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock remained flat at $37.11 immediately after reporting.

11. Is Now The Time To Buy Tenaris?

Updated: March 15, 2026 at 1:02 AM EDT

Are you wondering whether to buy Tenaris or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Tenaris isn’t a terrible business, but it doesn’t pass our bar. For starters, its revenue growth over the last five years was bottom-tier for the sector. And while Tenaris’s expanding EBITDA margin shows the business has become more efficient, its subscale operations hasn't hit a level of diversification where investors can sleep easy at night.

Tenaris’s P/E ratio based on the next 12 months is 4.7x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $46 on the company (compared to the current share price of $33.76).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.