Excelerate Energy (EE)

We’re cautious of Excelerate Energy. It not only barely generates profits but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why We Think Excelerate Energy Will Underperform

Operating specialized vessels that can deliver up to 1.2 billion cubic feet of natural gas per day, Excelerate Energy (NYSE:EE) provides liquified natural gas regasification services using floating vessels that convert LNG back into natural gas.

- poor earning stability in the sector may keep investors up at night

- Gross margin of 30.1% reflects its high production costs and unfavorable asset base

- On the bright side, its market share has increased this cycle as its 27.2% annual revenue growth over the last five years was exceptional

Excelerate Energy falls short of our expectations. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Excelerate Energy

Excelerate Energy is trading at $35.86 per share, or 12.9x forward P/E. Excelerate Energy’s multiple may seem like a great deal among energy upstream and integrated energy peers, but we think there are valid reasons why it’s this cheap.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. Excelerate Energy (EE) Research Report: Q4 CY2025 Update

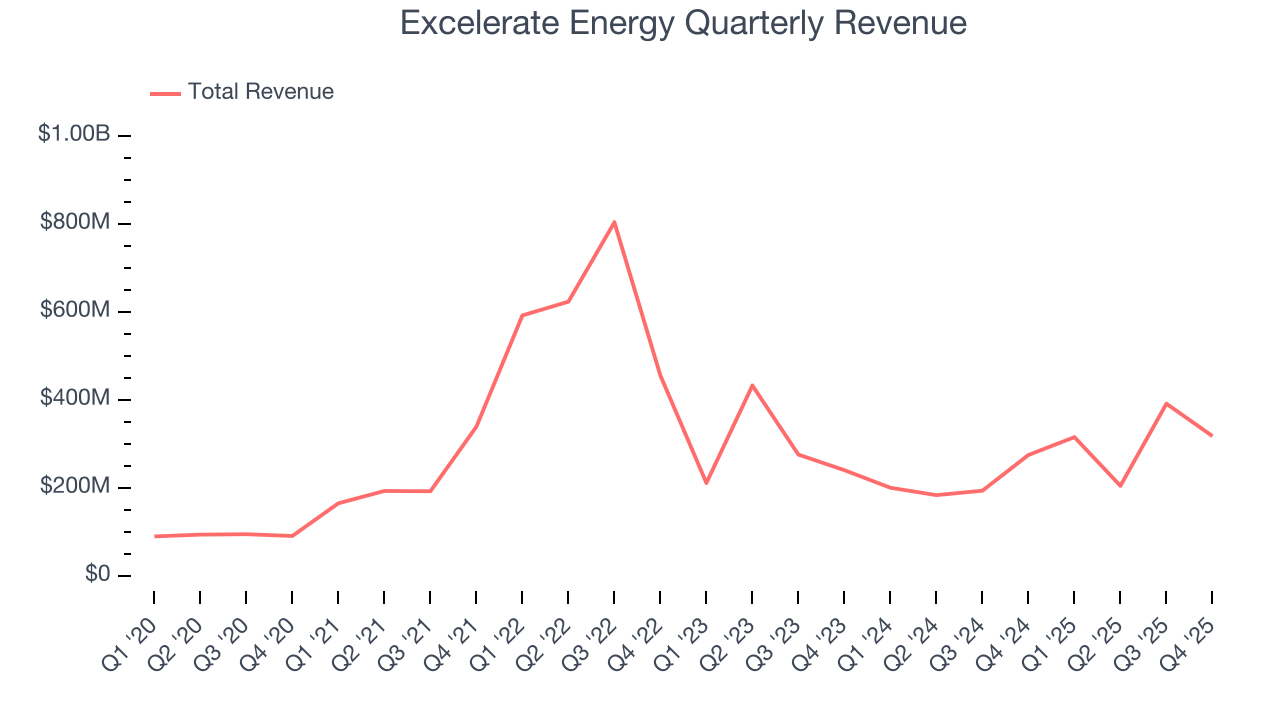

Liquified natural gas infrastructure provider Excelerate Energy (NYSE:EE) announced better-than-expected revenue in Q4 CY2025, with sales up 15.7% year on year to $317.6 million. Its non-GAAP profit of $0.29 per share was 19.7% below analysts’ consensus estimates.

Excelerate Energy (EE) Q4 CY2025 Highlights:

- Revenue: $317.6 million vs analyst estimates of $253.5 million (15.7% year-on-year growth, 25.3% beat)

- Adjusted EPS: $0.29 vs analyst expectations of $0.36 (19.7% miss)

- Adjusted EBITDA: $112.5 million vs analyst estimates of $110.8 million (35.4% margin, 1.5% beat)

- Operating Margin: 22.2%, in line with the same quarter last year

- Free Cash Flow was $70.78 million, up from -$13.93 million in the same quarter last year

- Market Capitalization: $1.15 billion

Company Overview

Operating specialized vessels that can deliver up to 1.2 billion cubic feet of natural gas per day, Excelerate Energy (NYSE:EE) provides liquified natural gas regasification services using floating vessels that convert LNG back into natural gas.

The company's core business revolves around Floating Storage and Regasification Units (FSRUs), which are specialized vessels that serve a dual purpose. These ships can transport LNG like a conventional carrier, but they also have onboard equipment to warm the super-cooled LNG (stored at minus 260 degrees Fahrenheit) back into gaseous form and send it through pipelines at the pressure needed for distribution networks. As of late 2024, Excelerate operated a fleet of 10 FSRUs under long-term contracts in countries including Argentina, Bangladesh, Brazil, Finland, Germany, Pakistan, and the United Arab Emirates.

The company's customers are typically state-owned oil and gas companies, transmission operators, and industrial natural gas users who need quick access to natural gas supplies without building permanent, land-based regasification terminals that can take years to construct and cost billions of dollars. For example, a utility company in Bangladesh might charter an Excelerate FSRU for 10 years, positioning it offshore where LNG tankers deliver cargoes. The FSRU then converts that LNG to natural gas and pipes it to power plants that generate electricity for the country.

Excelerate enters into time charter contracts where customers pay a fixed daily rate that covers the vessel, crew, and operations, while the customer typically pays for fuel, port fees, and the LNG itself. Most of the company's contracts are structured as take-or-pay agreements, meaning customers must pay whether they use the full capacity or not.

Beyond vessel operations, Excelerate also trades LNG and natural gas through sale and purchase agreements. The company maintains over 70 master agreements with various industry participants, allowing it to source LNG from producers and sell to end users. This includes a 20-year agreement to purchase 0.7 million tonnes annually from Venture Global's facility in Louisiana and a 15-year deal to supply Bangladesh with up to 1 million tonnes per year starting in 2026.

4. Infrastructure

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

Excelerate Energy's competitors include other FSRU operators like Golar LNG (NASDAQ:GLNG) and Höegh LNG Partners, along with land-based LNG terminal developers and operators such as Cheniere Energy (NYSE:LNG).

5. Revenue Scale

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks. Excelerate Energy’s $1.23 billion of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night. is a small company in an industry where scale matters.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Luckily, Excelerate Energy’s sales grew at an incredible 27.2% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

This quarter, Excelerate Energy reported year-on-year revenue growth of 15.7%, and its $317.6 million of revenue exceeded Wall Street’s estimates by 25.3%.

7. Gross Margin

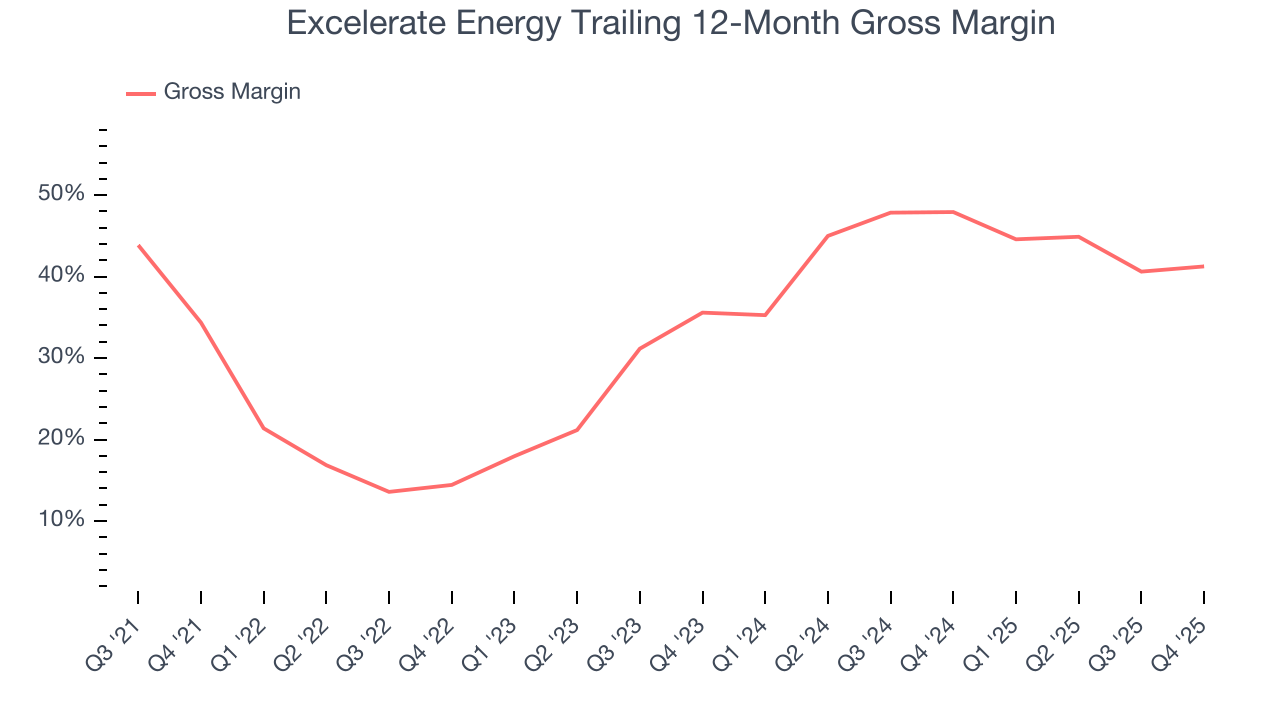

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Excelerate Energy, which averaged 30.1% gross margin over the last five years, exhibits bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

In Q4, Excelerate Energy produced a 41.4% gross profit margin, up 2.7 percentage points year on year.

8. Adjusted EBITDA Margin

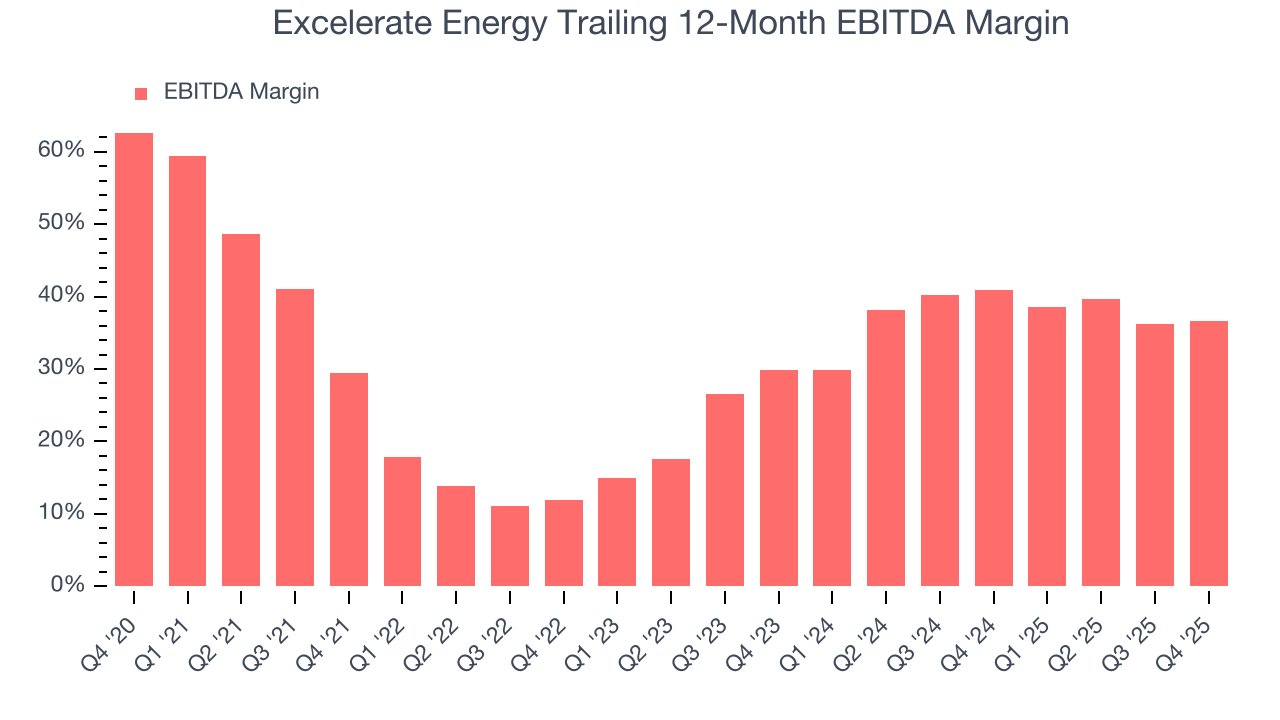

Adjusted EBITDA margin is an important measure of profitability for the sector and accounts for the gross margins and operating costs mentioned previously. Unlike operating margin, it is not distorted by accounting conventions around reserves, drilling costs, and assumptions on commodity consumption from the well or basin. Adjusted EBITDA highlights the economic reality of how much cash the rock produces before the capital structure (debt service) and the drilling budget (capex) are considered.

Excelerate Energy was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 25.8% was weak for an upstream and integrated energy business.

On the plus side, Excelerate Energy’s EBITDA margin rose by 7.1 percentage points over the last year.

In Q4, Excelerate Energy generated an EBITDA margin profit margin of 35.4%, up 2.1 percentage points year on year. This increase was a welcome development and shows it was more efficient. This adjusted EBITDA beat Wall Street’s estimates by 1.5%.

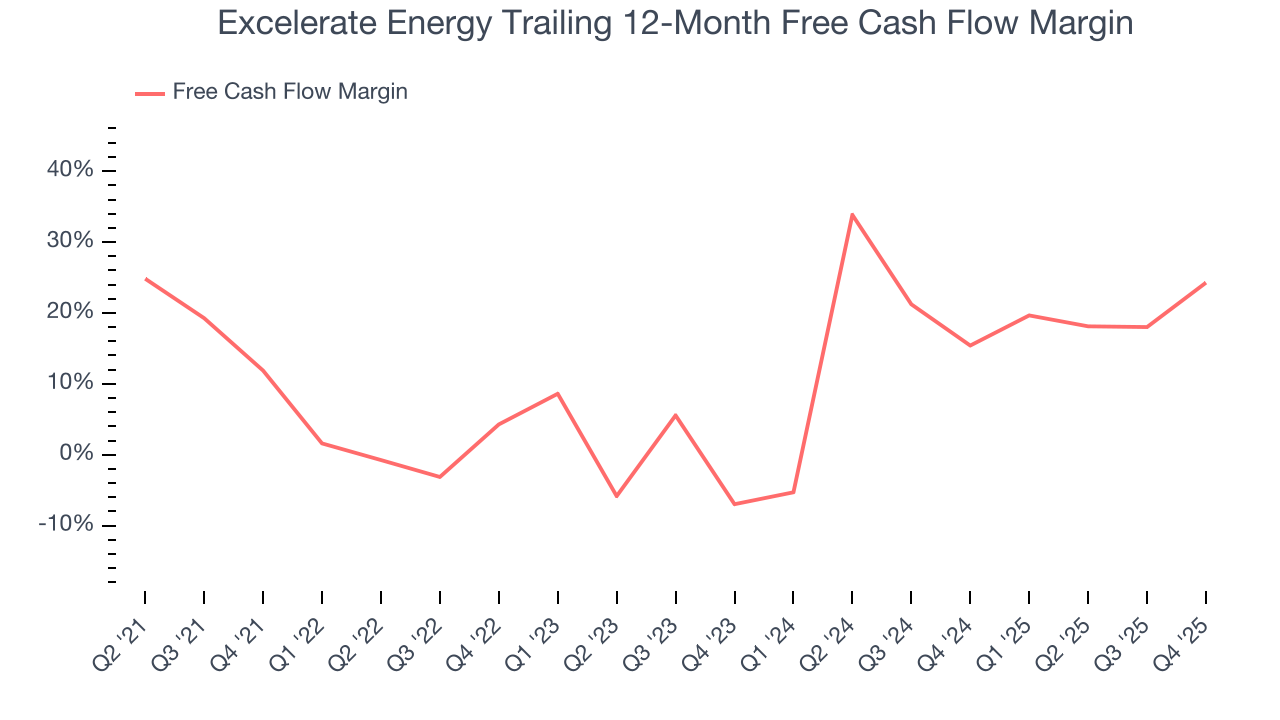

9. Cash Is King

As mentioned above, adjusted EBITDA ignores capital structure and drilling expenditure decisions. These are two huge aspects of an Energy producer, so in order to understand a comprehensive picture of business quality, an investor needs to account for these. Said differently, adjusted EBITDA margins could be solid but free cash flow is abysmal because decline rates of the asset are extreme and the drilling is expensive. Free cash flow tells you about not only the economics of the production that has happened but how much it costs to stay in business as well (further drilling or extraction).

Excelerate Energy has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.5% over the last five years, slightly better than the broader energy upstream and integrated energy sector.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Excelerate Energy’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 21.3 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Excelerate Energy? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Excelerate Energy’s free cash flow clocked in at $70.78 million in Q4, equivalent to a 22.3% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

10. Balance Sheet Assessment

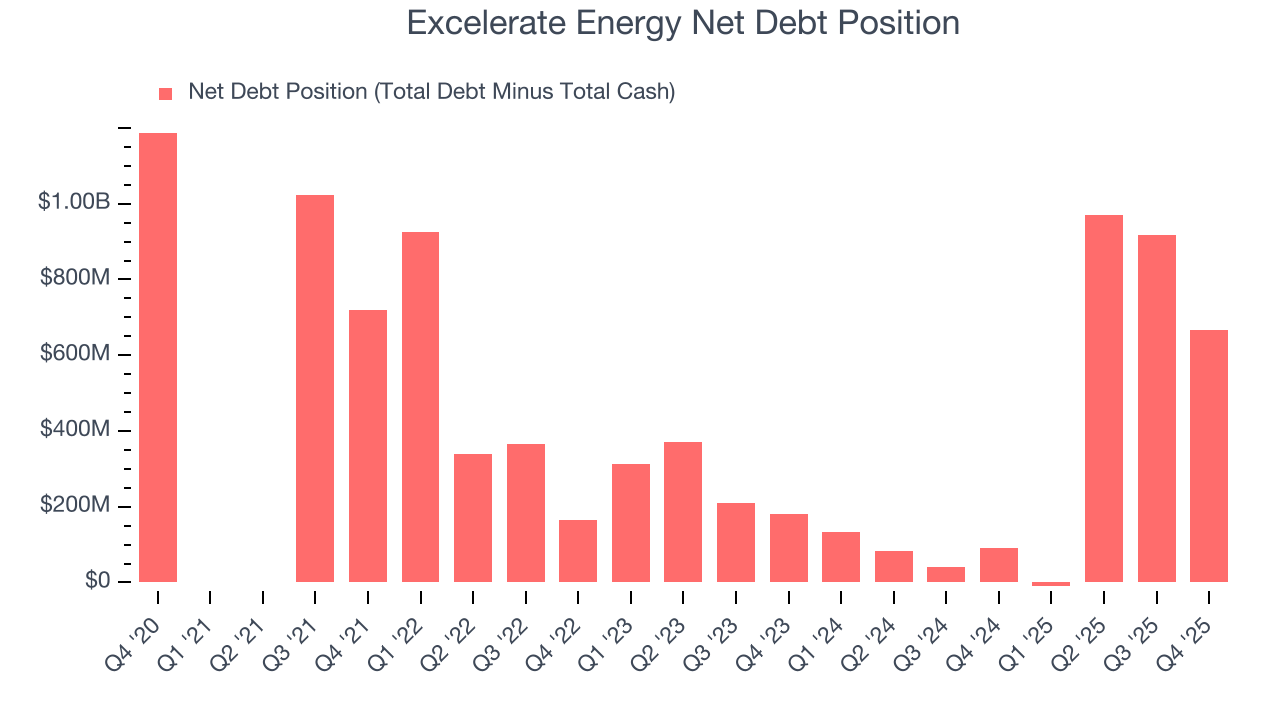

Excelerate Energy reported $577.1 million of cash and $1.24 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $449.3 million of EBITDA over the last 12 months, we view Excelerate Energy’s 1.5× net-debt-to-EBITDA ratio as safe. We also see its $94.14 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Excelerate Energy’s Q4 Results

We were impressed by how significantly Excelerate Energy blew past analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this was a weaker quarter. The stock traded up 3.2% to $37.13 immediately after reporting.

12. Is Now The Time To Buy Excelerate Energy?

Updated: March 17, 2026 at 12:59 AM EDT

Before deciding whether to buy Excelerate Energy or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Excelerate Energy isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth over the last five years was top-tier for the sector, it’s expected to deteriorate over the next 12 months and its free cash flow volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow. And while the company’s expanding EBITDA margin shows the business has become more efficient, the downside is its gross margins show its business model is much less lucrative than other companies.

Excelerate Energy’s P/E ratio based on the next 12 months is 12.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $43.08 on the company (compared to the current share price of $35.86).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.