TaskUs (TASK)

TaskUs is a sound business. Although its forecasted growth is weak, its strong margins enable it to navigate pockets of soft demand.― StockStory Analyst Team

1. News

2. Summary

Why TaskUs Is Interesting

Starting as a virtual assistant service in 2008 before evolving into a global digital services provider, TaskUs (NASDAQ:TASK) provides outsourced digital services including customer experience management, content moderation, and AI data services to innovative technology companies.

- Annual revenue growth of 19.9% over the last five years was superb and indicates its market share increased during this cycle

- Successful business model is illustrated by its impressive adjusted operating margin

- One risk is its low returns on capital reflect management’s struggle to allocate funds effectively

TaskUs shows some signs of a high-quality business. If you’ve been itching to buy the stock, the price looks fair.

3. TaskUs (TASK) Research Report: Q4 CY2025 Update

Digital outsourcing company TaskUs (NASDAQ:TASK) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 14.1% year on year to $313 million. The company expects next quarter’s revenue to be around $297 million, close to analysts’ estimates. Its non-GAAP profit of $0.40 per share was 11% above analysts’ consensus estimates.

TaskUs (TASK) Q4 CY2025 Highlights:

- Revenue: $313 million vs analyst estimates of $303.8 million (14.1% year-on-year growth, 3% beat)

- Adjusted EPS: $0.40 vs analyst estimates of $0.36 (11% beat)

- Adjusted EBITDA: $61.4 million vs analyst estimates of $59.82 million (19.6% margin, 2.6% beat)

- Revenue Guidance for Q1 CY2026 is $297 million at the midpoint, roughly in line with what analysts were expecting

- Operating Margin: 12.2%, up from 8% in the same quarter last year

- Free Cash Flow Margin: 4.1%, down from 7.4% in the same quarter last year

- Market Capitalization: $915 million

Company Overview

Starting as a virtual assistant service in 2008 before evolving into a global digital services provider, TaskUs (NASDAQ:TASK) provides outsourced digital services including customer experience management, content moderation, and AI data services to innovative technology companies.

TaskUs operates at the intersection of human expertise and digital innovation, helping clients navigate complex operational challenges. The company's services are organized into three main categories: Digital Customer Experience (Digital CX), Trust and Safety, and Artificial Intelligence Services.

In Digital CX, TaskUs handles customer support across multiple channels, with over 80% of this work occurring through non-voice digital channels like chat, social media, and in-app messaging. The company also provides training programs, sales support, and consulting services to help clients optimize their customer experience strategies.

The Trust and Safety division focuses on content moderation and risk management. Content moderators review user-generated material on digital platforms, identifying and removing policy-violating content while navigating complex cultural contexts. TaskUs has developed specialized wellness programs to support employees in this psychologically demanding work. The Risk and Response team handles identity verification, regulatory compliance, and fraud detection for clients.

TaskUs's AI Services division has become increasingly important as artificial intelligence applications have evolved. The company provides data annotation services that are crucial for training AI algorithms, labeling images, text, audio, and video to create the datasets that power computer vision, natural language processing, and other AI applications. Beyond annotation, TaskUs offers troubleshooting and remediation services for AI systems.

The company employs a flexible delivery model with options for on-site, remote, hybrid, and crowdsourced work. TaskUs maintains a global footprint with operations across 12 countries, with the Philippines serving as its largest market, housing approximately 63% of its workforce. This offshore and nearshore strategy allows TaskUs to provide cost-effective services while maintaining quality through standardized processes and local leadership.

4. Business Process Outsourcing & Consulting

The sector stands to benefit from ongoing digital transformation, increasing corporate demand for cost efficiencies, and the growing complexity of regulatory and cybersecurity landscapes. For those that invest wisely, AI and automation capabilities could emerge as competitive advantages, enhancing process efficiencies for the companies themselves as well as their clients. On the flip side, AI could be a headwind as well as the technology could lower the barrier to entry in the space and give rise to more self-service solutions. Additional challenges in the years ahead could include wage inflation for highly skilled consultants and potential regulatory scrutiny on outsourcing practices—especially in industries like finance and healthcare where who has access to certain data matters greatly.

TaskUs competes with other business process outsourcing companies including Teleperformance (OTCMKTS:TLPFY), TELUS International (NYSE:TIXT), and Concentrix (NASDAQ:CNXC), as well as specialized AI services providers like Scale AI and Appen (ASX:APX).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.18 billion in revenue over the past 12 months, TaskUs is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

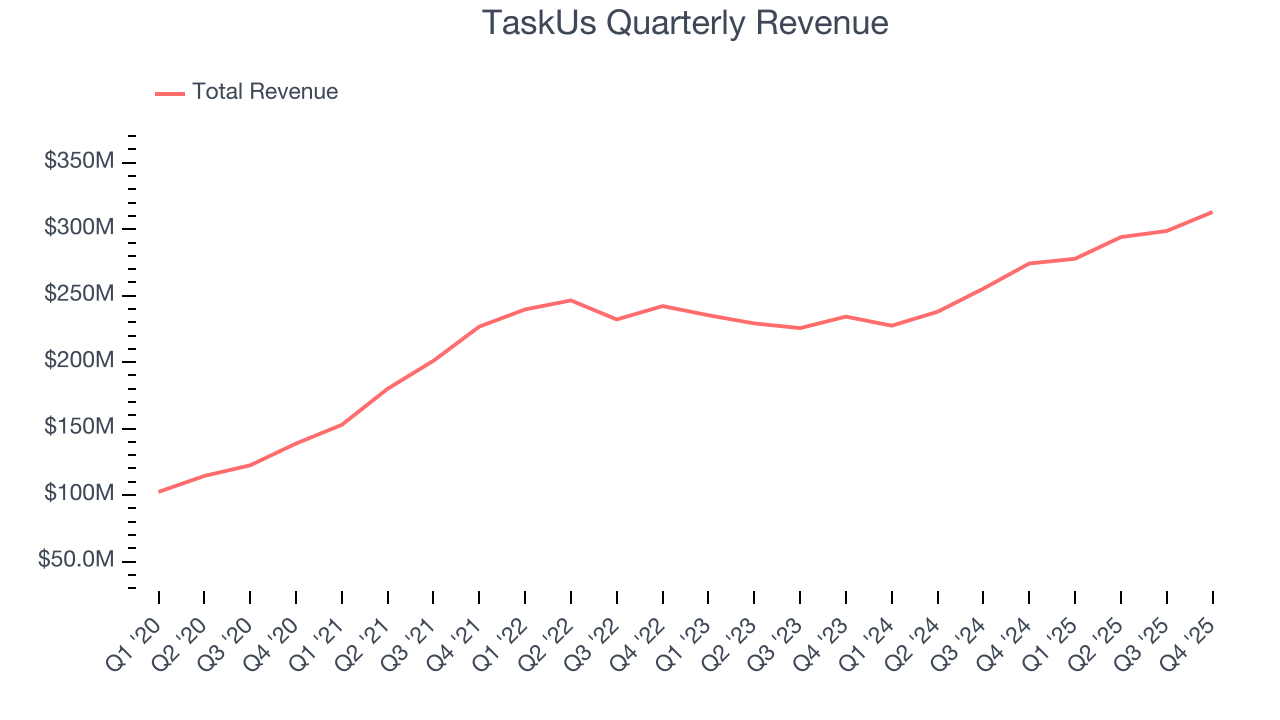

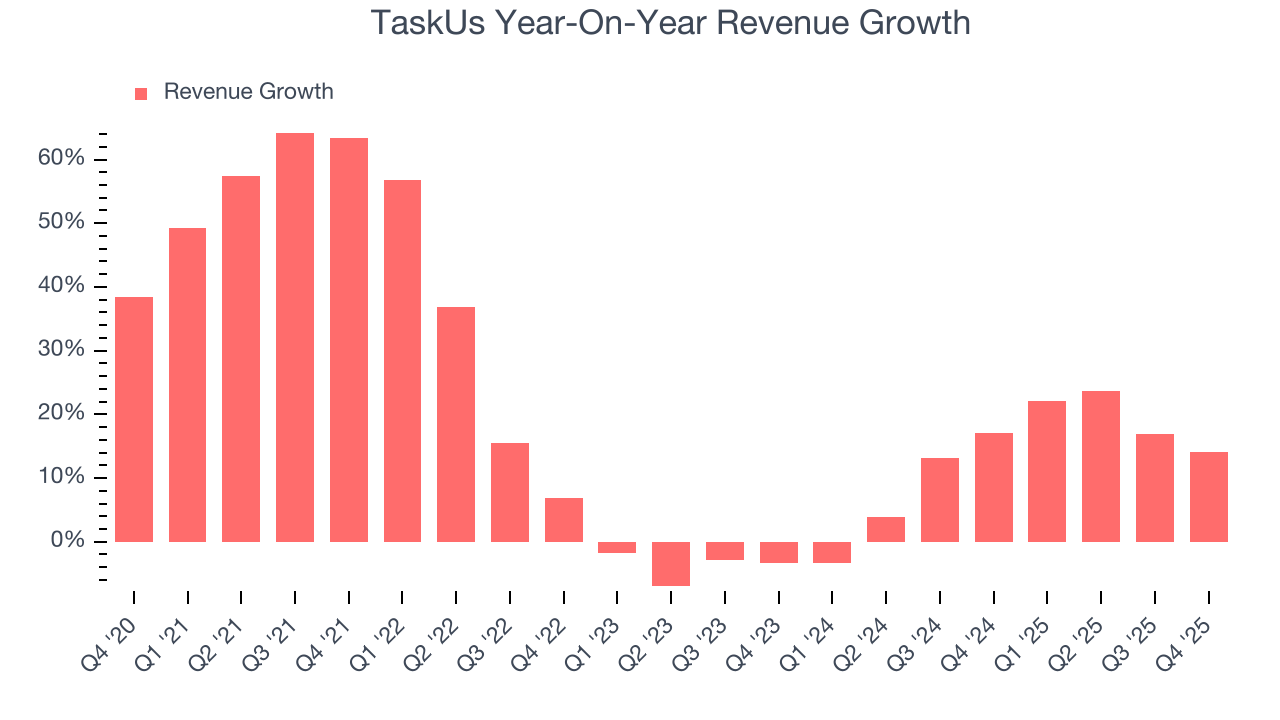

As you can see below, TaskUs’s 19.9% annualized revenue growth over the last five years was incredible. This is an encouraging starting point for our analysis because it shows TaskUs’s demand was higher than many business services companies.

Long-term growth is the most important, but within business services, a half-decade historical view may miss new innovations or demand cycles. TaskUs’s annualized revenue growth of 13.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, TaskUs reported year-on-year revenue growth of 14.1%, and its $313 million of revenue exceeded Wall Street’s estimates by 3%. Company management is currently guiding for a 6.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 6.7% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and suggests the market is forecasting some success for its newer products and services.

6. Operating Margin

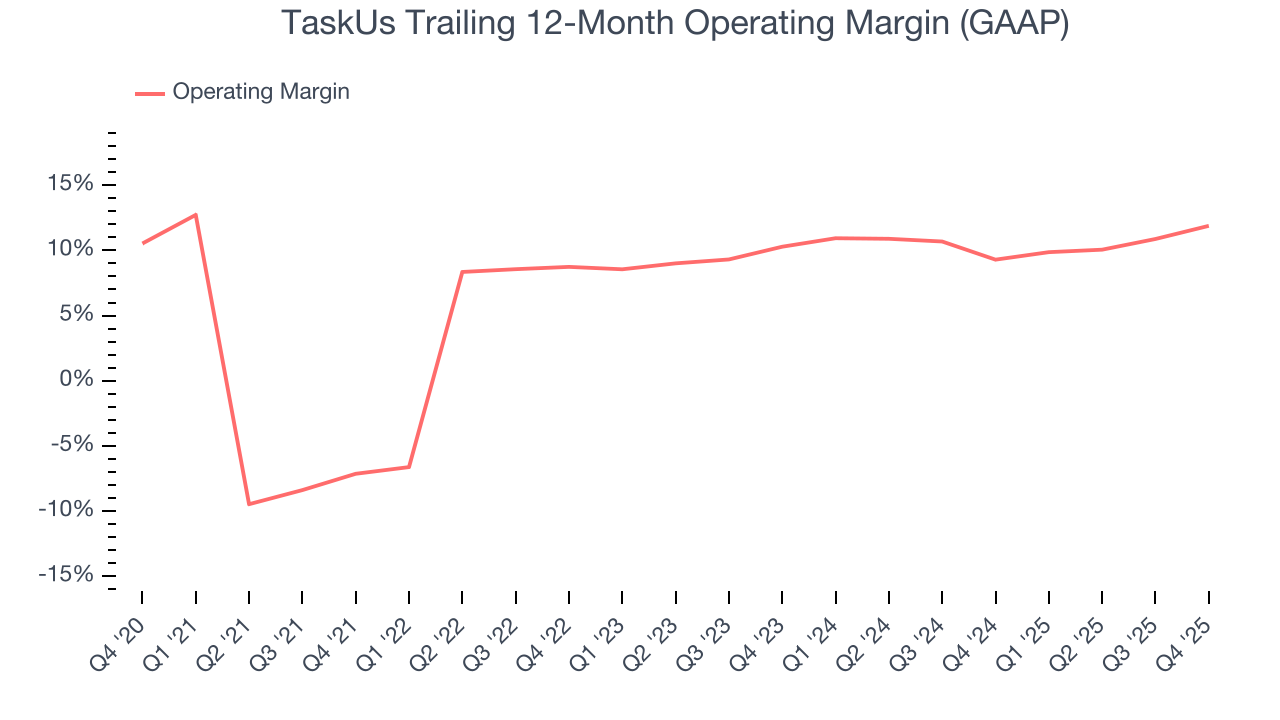

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

TaskUs was profitable over the last five years but held back by its large cost base. Its average operating margin of 7.4% was weak for a business services business.

On the plus side, TaskUs’s operating margin rose by 19 percentage points over the last five years, as its sales growth gave it immense operating leverage.

This quarter, TaskUs generated an operating margin profit margin of 12.2%, up 4.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

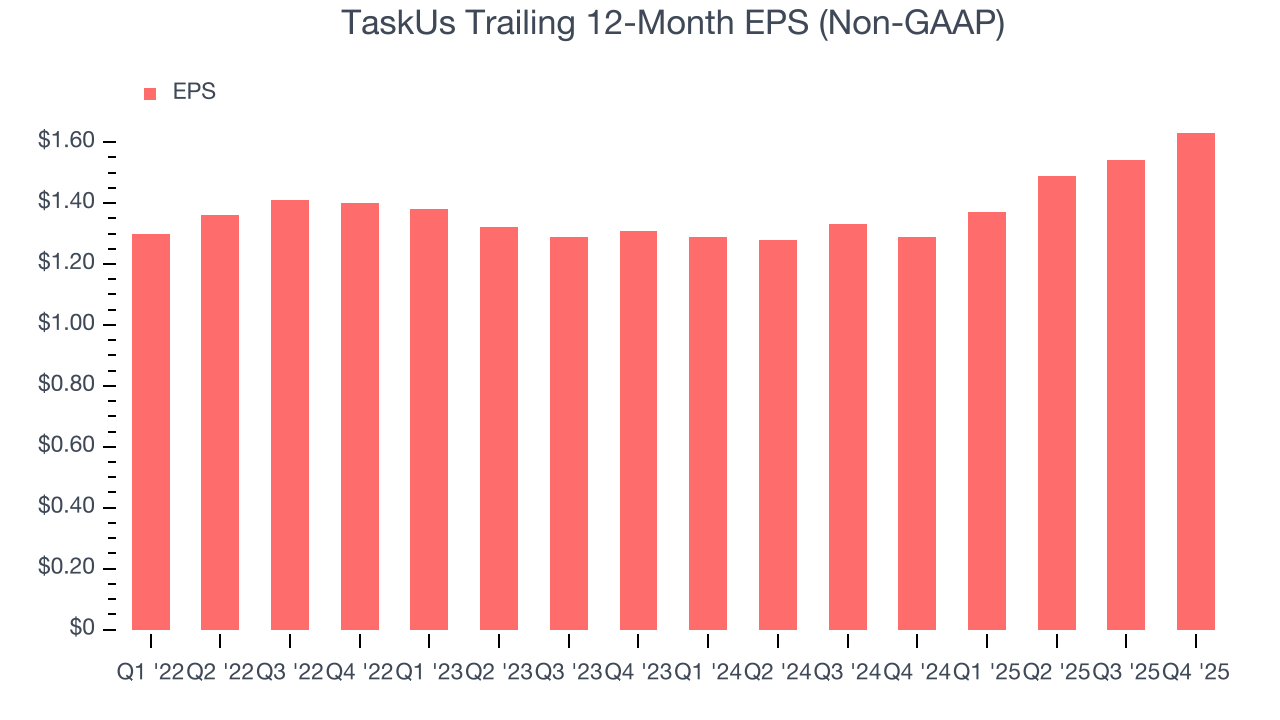

TaskUs’s full-year EPS grew at an unimpressive 6.8% compounded annual growth rate over the last four years, in line with the broader business services sector.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

TaskUs’s decent 11.5% annual EPS growth over the last two years aligns with its revenue trend. This tells us it maintained its per-share profitability as it expanded.

In Q4, TaskUs reported adjusted EPS of $0.40, up from $0.31 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects TaskUs’s full-year EPS of $1.63 to shrink by 3.6%.

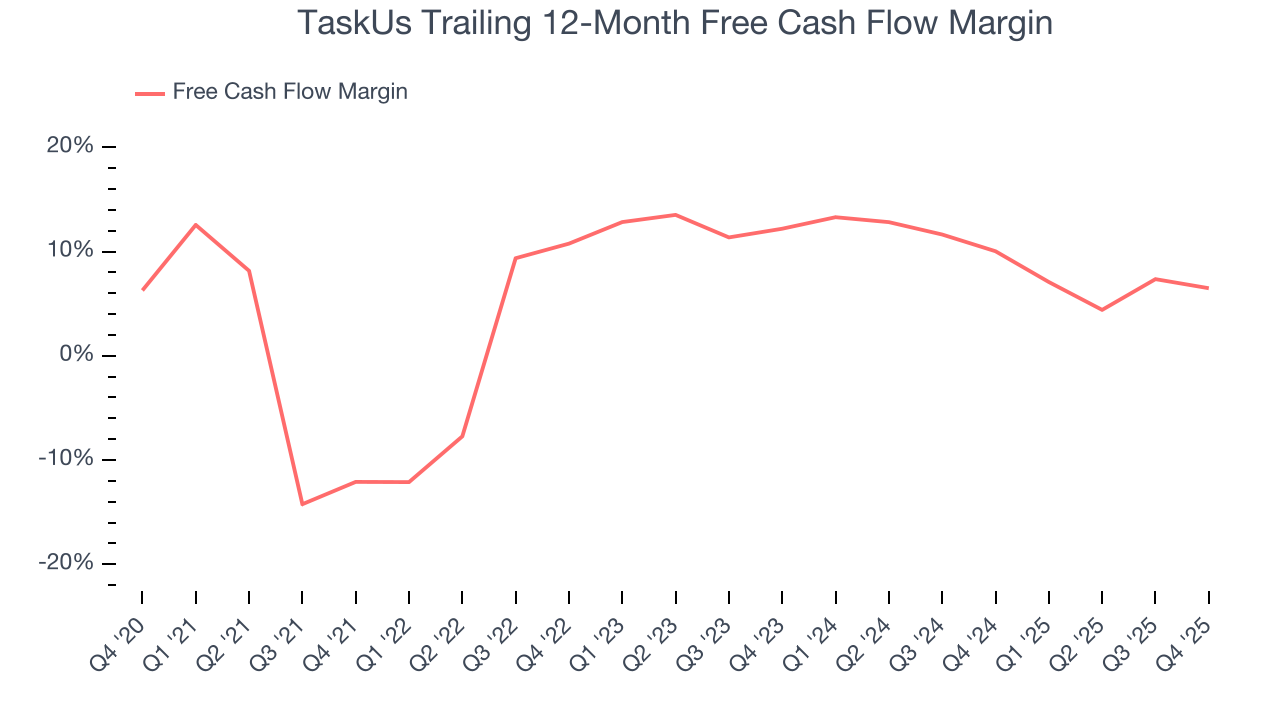

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

TaskUs has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.2% over the last five years, slightly better than the broader business services sector.

Taking a step back, we can see that TaskUs’s margin expanded by 18.6 percentage points during that time. This is encouraging because it gives the company more optionality.

TaskUs’s free cash flow clocked in at $12.91 million in Q4, equivalent to a 4.1% margin. The company’s cash profitability regressed as it was 3.3 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

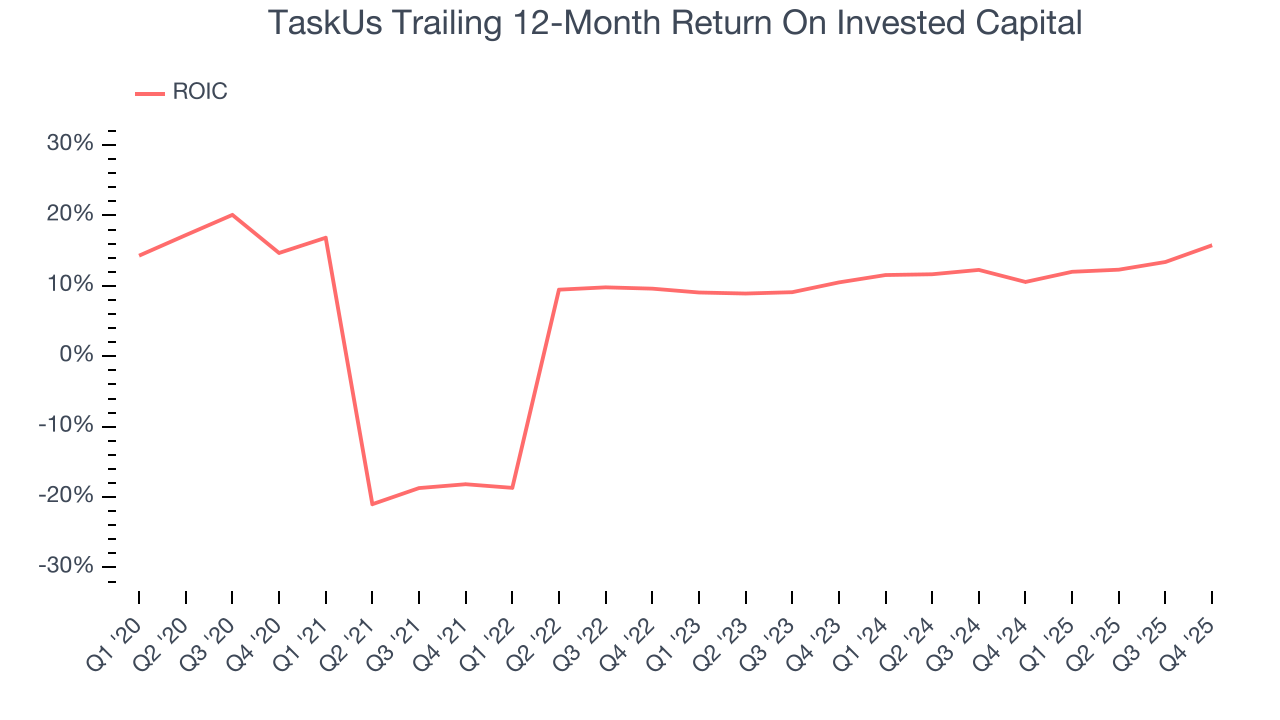

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although TaskUs has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.6%, somewhat low compared to the best business services companies that consistently pump out 25%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, TaskUs’s ROIC has increased. This is a good sign, but we recognize its lack of profitable growth during the COVID era was the primary reason for the change.

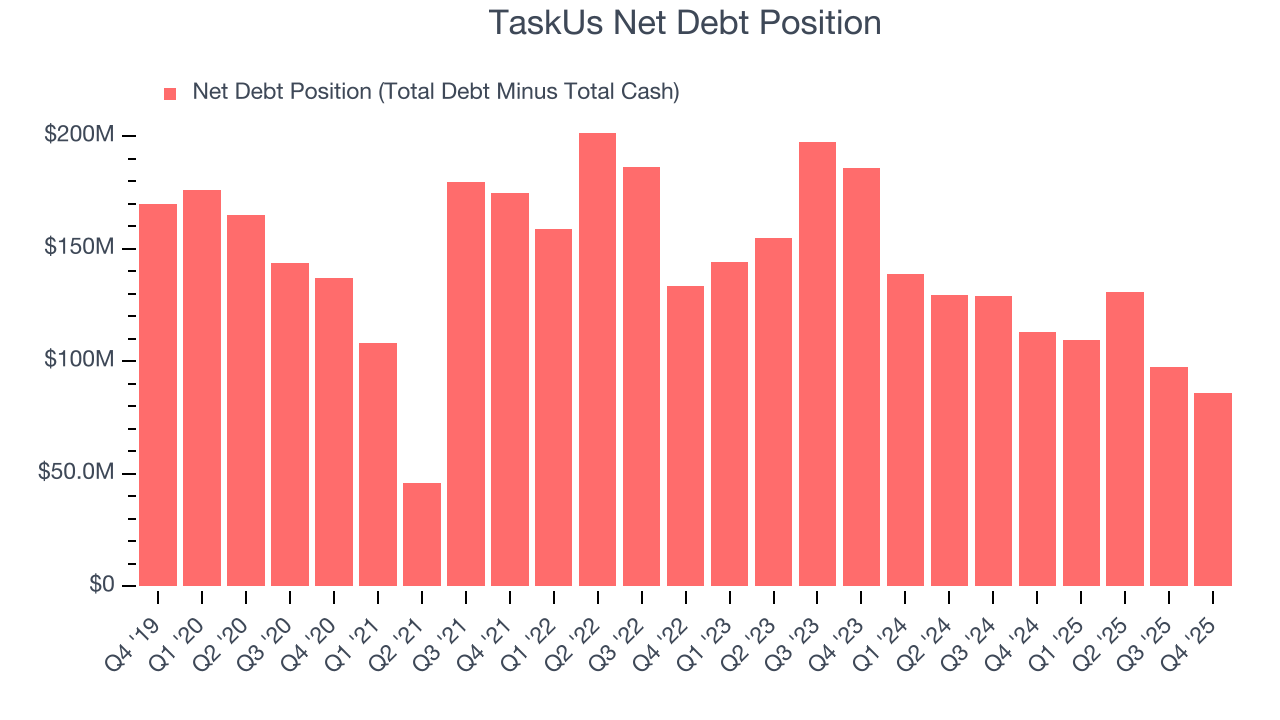

10. Balance Sheet Assessment

TaskUs reported $211.7 million of cash and $297.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $249.1 million of EBITDA over the last 12 months, we view TaskUs’s 0.3× net-debt-to-EBITDA ratio as safe. We also see its $7.87 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from TaskUs’s Q4 Results

It was good to see TaskUs beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed. Overall, this print had some key positives. The stock traded up 7.3% to $11.29 immediately following the results.

12. Is Now The Time To Buy TaskUs?

Updated: March 17, 2026 at 12:35 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

TaskUs is a fine business. To kick things off, its revenue growth was exceptional over the last five years. And while its projected EPS for the next year is lacking, its rising cash profitability gives it more optionality. On top of that, its rising returns show management's prior bets are starting to pay off.

TaskUs’s P/E ratio based on the next 12 months is 7.5x. When scanning the business services space, TaskUs trades at a fair valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $13.67 on the company (compared to the current share price of $10.60), implying they see 29% upside in buying TaskUs in the short term.