WeightWatchers (WW)

We wouldn’t recommend WeightWatchers. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think WeightWatchers Will Underperform

Known by many for its old cable television commercials, WeightWatchers (NASDAQ:WW) is a wellness company offering a range of products and services promoting weight loss and healthy habits.

- Sales tumbled by 12.4% annually over the last five years, showing consumer trends are working against its favor

- Sales are expected to decline once again over the next 12 months as it continues working through a challenging demand environment

- Subpar operating margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

WeightWatchers doesn’t check our boxes. There are better opportunities in the market.

Why There Are Better Opportunities Than WeightWatchers

WeightWatchers is trading at $21.26 per share, or 4.8x forward EV-to-EBITDA. This sure is a cheap multiple, but you get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. WeightWatchers (WW) Research Report: Q4 CY2025 Update

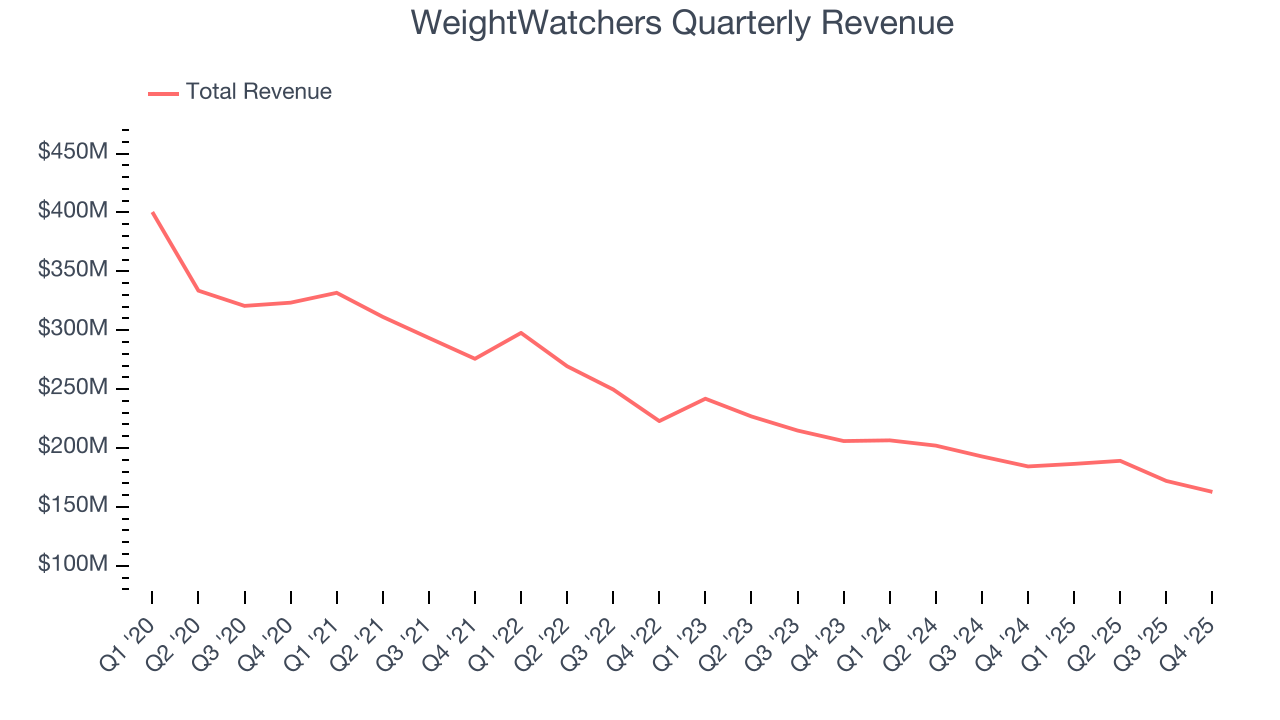

Personal wellness company WeightWatchers (NASDAQ:WW) reported Q4 CY2025 results topping the market’s revenue expectations, but sales fell by 11.7% year on year to $162.8 million. On the other hand, the company’s full-year revenue guidance of $627.5 million at the midpoint came in 0.7% below analysts’ estimates. Its GAAP loss of $0.58 per share was 71.4% above analysts’ consensus estimates.

WeightWatchers (WW) Q4 CY2025 Highlights:

- Revenue: $162.8 million vs analyst estimates of $149.8 million (11.7% year-on-year decline, 8.7% beat)

- EPS (GAAP): -$0.58 vs analyst estimates of -$2.03 (71.4% beat)

- Adjusted EBITDA: $18.04 million vs analyst estimates of $12.11 million (11.1% margin, 48.9% beat)

- EBITDA guidance for the upcoming financial year 2026 is $110 million at the midpoint, below analyst estimates of $115.1 million

- Operating Margin: -7.9%, down from 8.7% in the same quarter last year

- Free Cash Flow Margin: 0.7%, down from 2.4% in the same quarter last year

- Market Capitalization: $210.5 million

Company Overview

Known by many for its old cable television commercials, WeightWatchers (NASDAQ:WW) is a wellness company offering a range of products and services promoting weight loss and healthy habits.

WW began as a weight loss-focused organization with Weight Watchers and has since rebranded into a comprehensive wellness brand. The company originally gained traction through its approach to weight management, combining dietary advice with group support meetings. This approach provided a community and accountability that differentiated it from other diet programs.

Initially, WW's member growth was fueled by in-person group meetings and public speaking events, enticing members to join. The company then expanded by franchising the Weight Watcher program to its graduates.

Today, WW's products include cookbooks, prepared food lines, and more, catering to a broader range of consumers. Its offerings are primarily subscription-based, and customers can participate both digitally and in person, receiving individualized support and coaching. WW also generates income from branded services and products, such as magazines, food guides, and licensing fees.

4. Consumer Discretionary - Specialized Consumer Services

The Consumer Discretionary sector, by definition, is made up of companies selling non-essential goods and services. When economic conditions deteriorate or tastes shift, consumers can easily cut back or eliminate these purchases. For long-term investors with five-year holding periods, this creates a structural challenge: the sector is inherently hit-driven, with low switching costs and fickle customers. As a result, only a handful of companies can reliably grow demand and compound earnings over long periods, which is why our bar is high and High Quality ratings are rare.

Some consumer discretionary companies don’t fall neatly into a category because their products or services are unique. Although their offerings may be niche, these companies have often found more efficient or technology-enabled ways of doing or selling something that has existed for a while. Technology can be a double-edged sword, though, as it may lower the barriers to entry for new competitors and allow them to do serve customers better.

WeightWatchers's fitness and wellness peers include BODi (NYSE:BODY), MyFitnessPal, Noom, Cult.fit, and Trainerize.

5. Revenue Growth

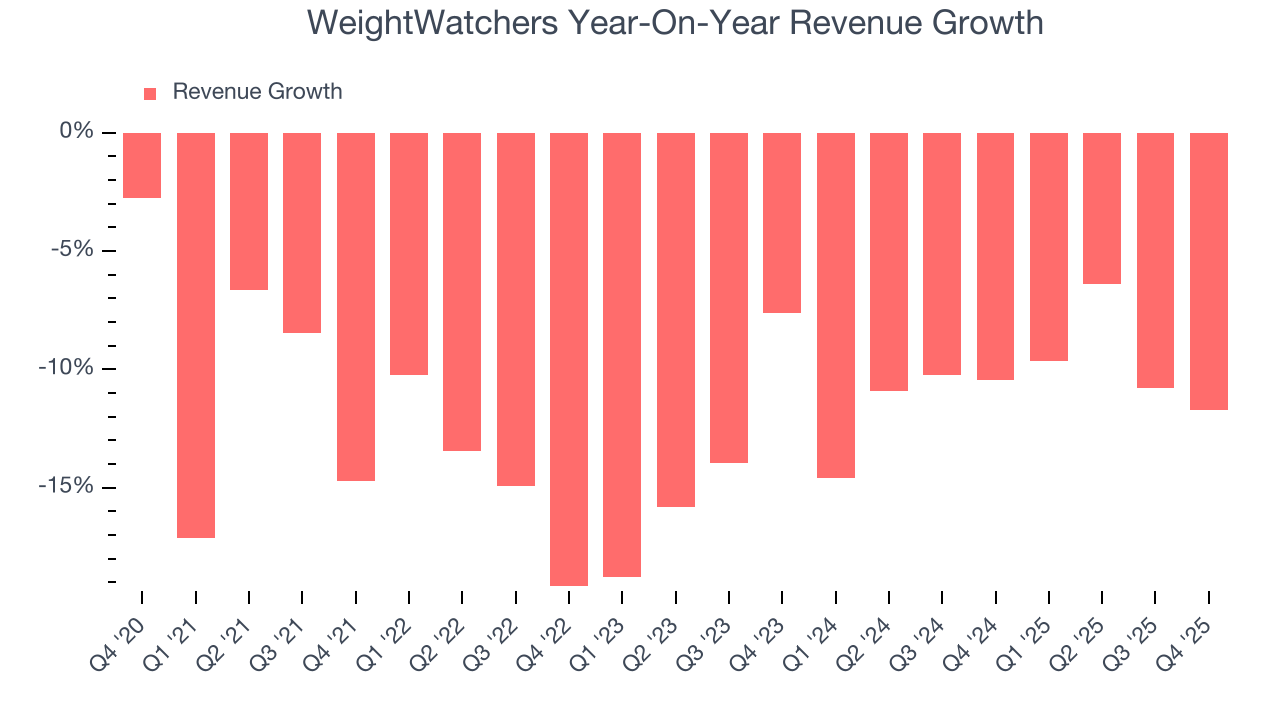

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, WeightWatchers’s demand was weak and its revenue declined by 12.4% per year. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. WeightWatchers’s annualized revenue declines of 10.6% over the last two years suggest its demand continued shrinking.

This quarter, WeightWatchers’s revenue fell by 11.7% year on year to $162.8 million but beat Wall Street’s estimates by 8.7%.

Looking ahead, sell-side analysts expect revenue to decline by 10.8% over the next 12 months, similar to its two-year rate. This projection is underwhelming and implies its newer products and services will not accelerate its top-line performance yet.

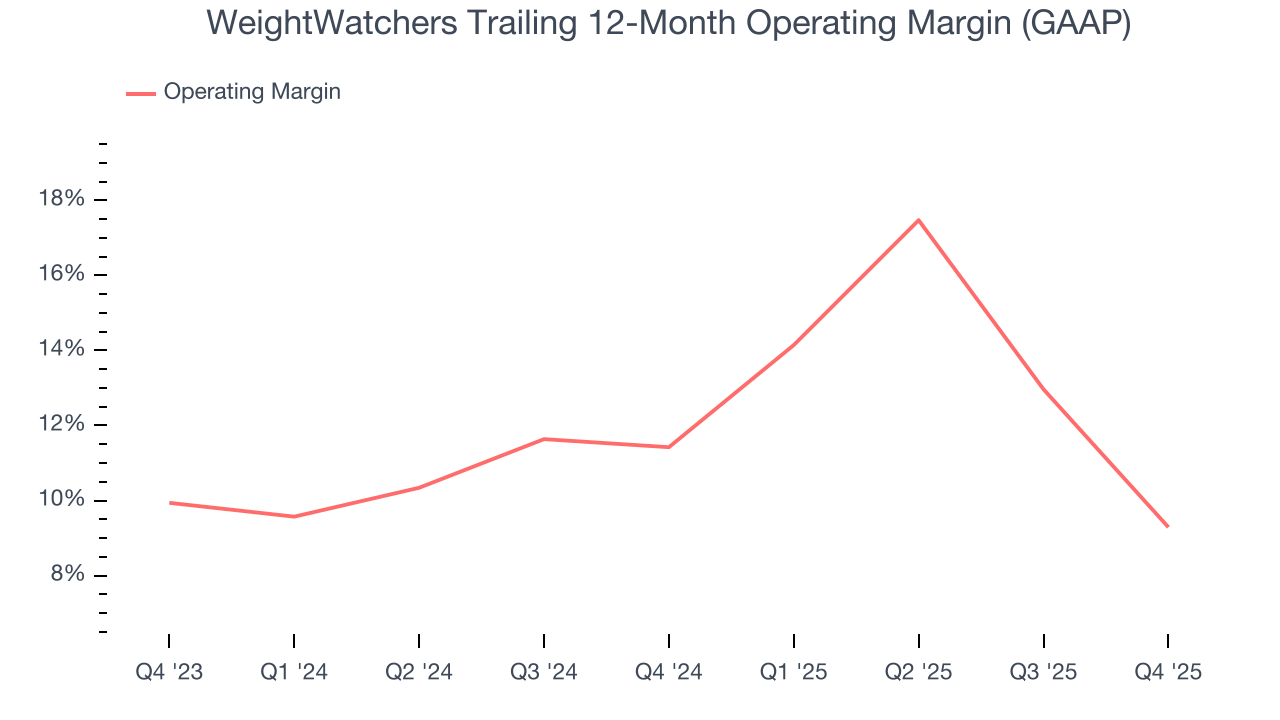

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

WeightWatchers’s operating margin has shrunk over the last 12 months and averaged 10.4% over the last two years. The company’s profitability was mediocre for a consumer discretionary business and shows it couldn’t pass its higher operating expenses onto its customers.

In Q4, WeightWatchers generated an operating margin profit margin of negative 7.9%, down 16.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

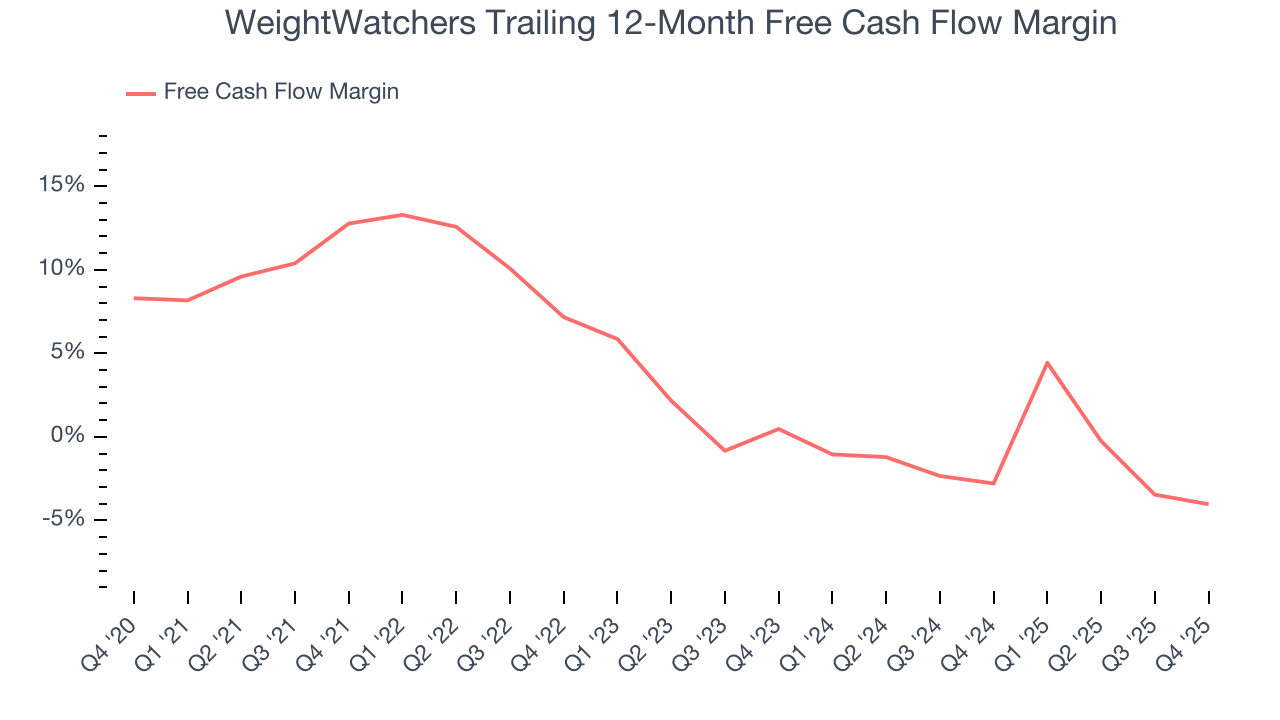

7. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

While WeightWatchers’s free cash flow broke even this quarter, the broader story hasn’t been so clean. Over the last two years, WeightWatchers’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 3.4%, meaning it lit $3.37 of cash on fire for every $100 in revenue.

WeightWatchers broke even from a free cash flow perspective in Q4. The company’s cash profitability regressed as it was 1.7 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, causing short-term swings. Long-term trends trump temporary fluctuations.

Looking forward, analysts predict WeightWatchers will generate cash on a full-year basis. Their consensus estimates imply its free cash flow margin of negative 4% for the last 12 months will increase to positive 9.1%, giving it more money to invest.

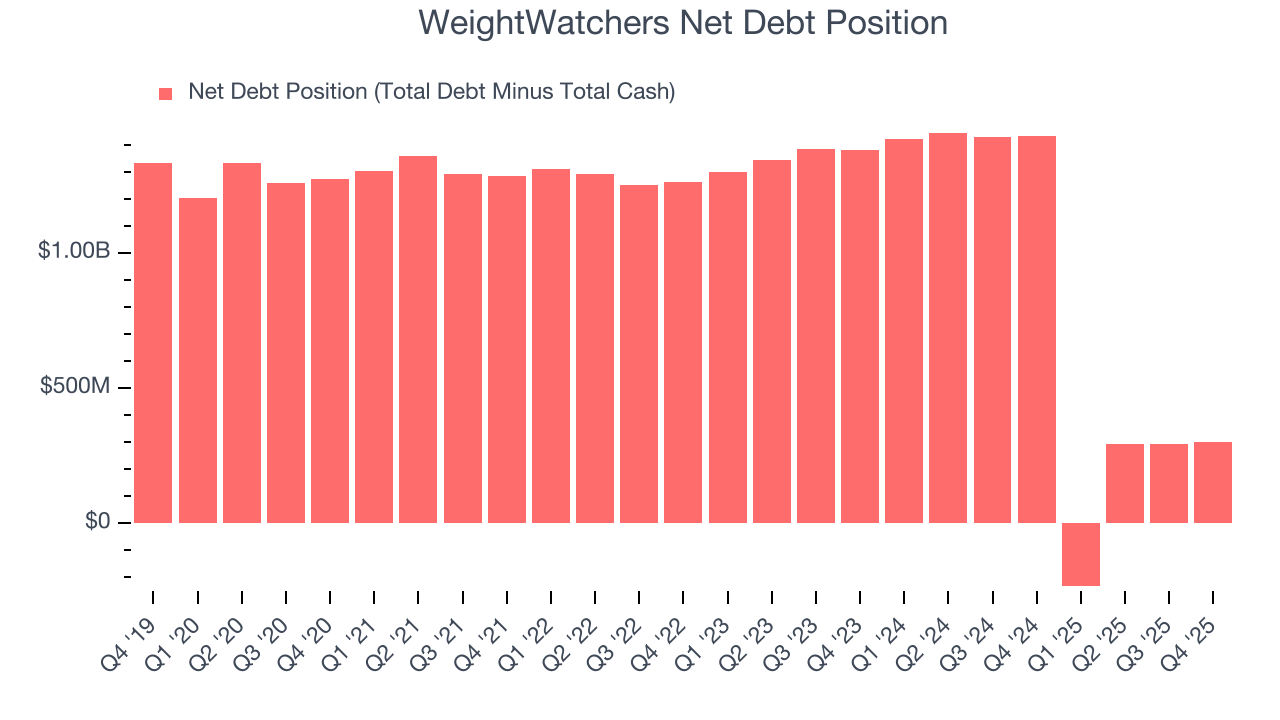

8. Balance Sheet Assessment

WeightWatchers reported $166.6 million of cash and $468.6 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $139.9 million of EBITDA over the last 12 months, we view WeightWatchers’s 2.2× net-debt-to-EBITDA ratio as safe. We also see its $39.87 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

9. Key Takeaways from WeightWatchers’s Q4 Results

It was good to see WeightWatchers beat analysts’ EPS expectations this quarter. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its full-year EBITDA guidance missed and its full-year revenue guidance fell slightly short of Wall Street’s estimates. Overall, this print was mixed. The stock traded up 2.7% to $21.67 immediately following the results.

10. Is Now The Time To Buy WeightWatchers?

Updated: March 16, 2026 at 11:04 PM EDT

Are you wondering whether to buy WeightWatchers or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

WeightWatchers doesn’t pass our quality test. While its Forecasted free cash flow margin suggests the company will have more capital to invest or return to shareholders next year, the downside is its number of members has disappointed. On top of that, its projected EPS for the next year is lacking.

WeightWatchers’s EV-to-EBITDA ratio based on the next 12 months is 4.8x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $42.83 on the company (compared to the current share price of $21.26).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.