Bath and Body Works (BBWI)

We aren’t fans of Bath and Body Works. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why Bath and Body Works Is Not Exciting

Spun off from L Brands in 2020, Bath & Body Works (NYSE:BBWI) is a personal care and home fragrance retailer where consumers can find specialty shower gels, scented candles for the home, and lotions.

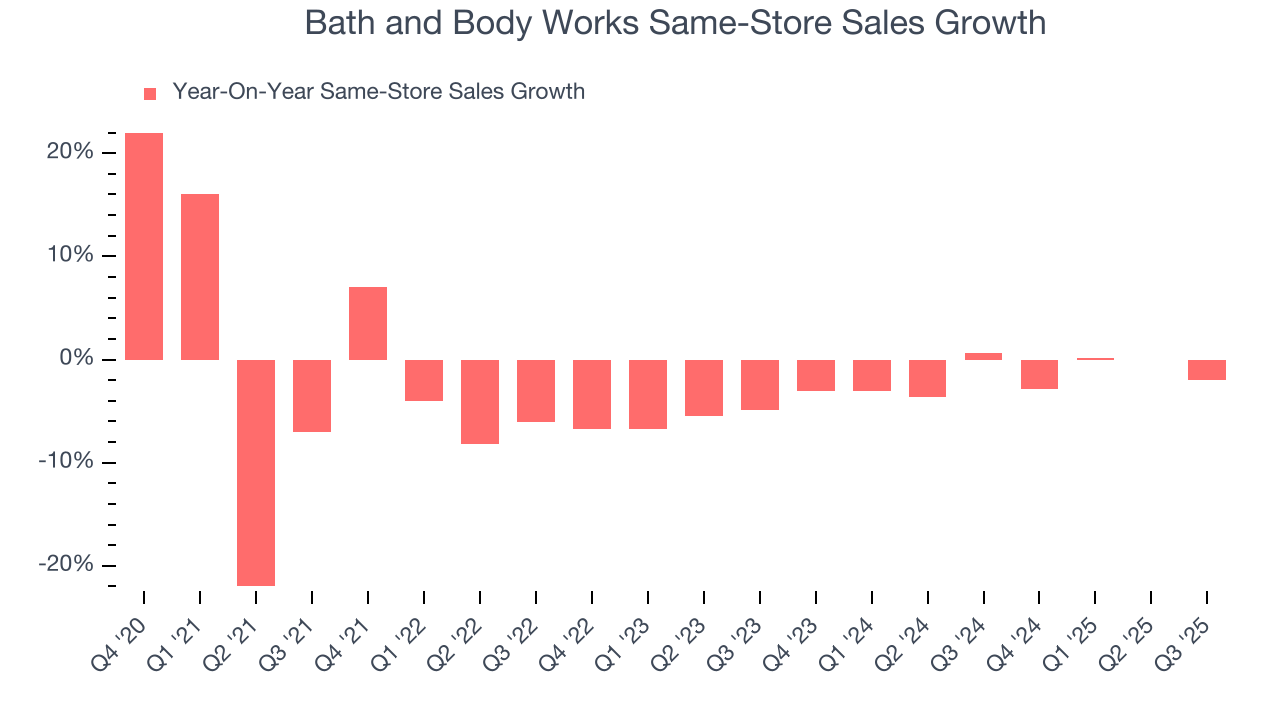

- Lagging same-store sales over the past two years suggest it might have to change its pricing and marketing strategy to stimulate demand

- Annual revenue declines of 1.2% over the last three years indicate problems with its market positioning

- The good news is that its market-beating returns on capital illustrate that management has a knack for investing in profitable ventures

Bath and Body Works falls below our quality standards. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Bath and Body Works

Bath and Body Works is trading at $18.70 per share, or 7.4x forward P/E. Bath and Body Works’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

Cheap stocks can look like a great deal at first glance, but they can be value traps. They often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. Bath and Body Works (BBWI) Research Report: Q4 CY2025 Update

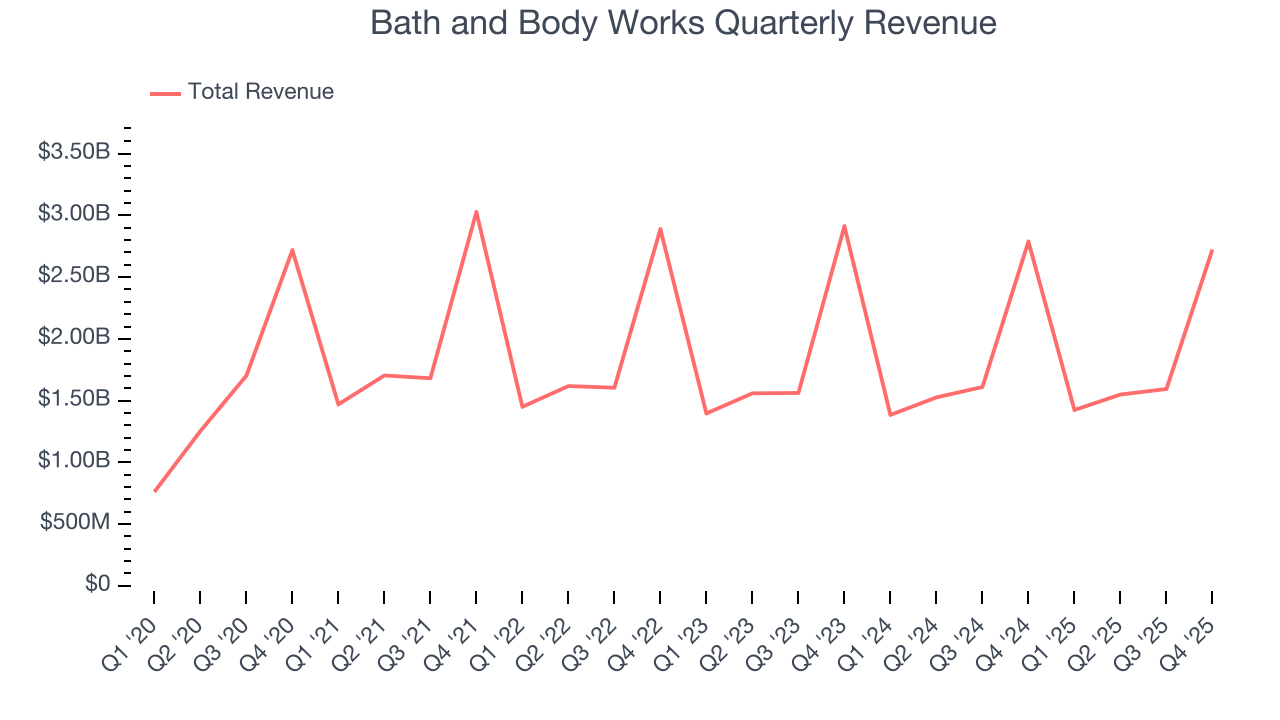

Personal care and home fragrance retailer Bath & Body Works (NYSE:BBWI) announced better-than-expected revenue in Q4 CY2025, but sales fell by 2.3% year on year to $2.72 billion. Guidance for next quarter’s revenue was better than expected at $1.35 billion at the midpoint, 0.6% above analysts’ estimates. Its GAAP profit of $1.99 per share was 14.2% above analysts’ consensus estimates.

Bath and Body Works (BBWI) Q4 CY2025 Highlights:

- Revenue: $2.72 billion vs analyst estimates of $2.61 billion (2.3% year-on-year decline, 4.3% beat)

- EPS (GAAP): $1.99 vs analyst estimates of $1.74 (14.2% beat)

- Adjusted EBITDA: $668 million vs analyst estimates of $607.9 million (24.5% margin, 9.9% beat)

- Revenue Guidance for Q1 CY2026 is $1.35 billion at the midpoint, roughly in line with what analysts were expecting

- EPS (GAAP) guidance for the upcoming financial year 2026 is $3.13 at the midpoint, beating analyst estimates by 20.4%

- Operating Margin: 22%, down from 24.3% in the same quarter last year

- Free Cash Flow Margin: 29.9%, down from 32.1% in the same quarter last year

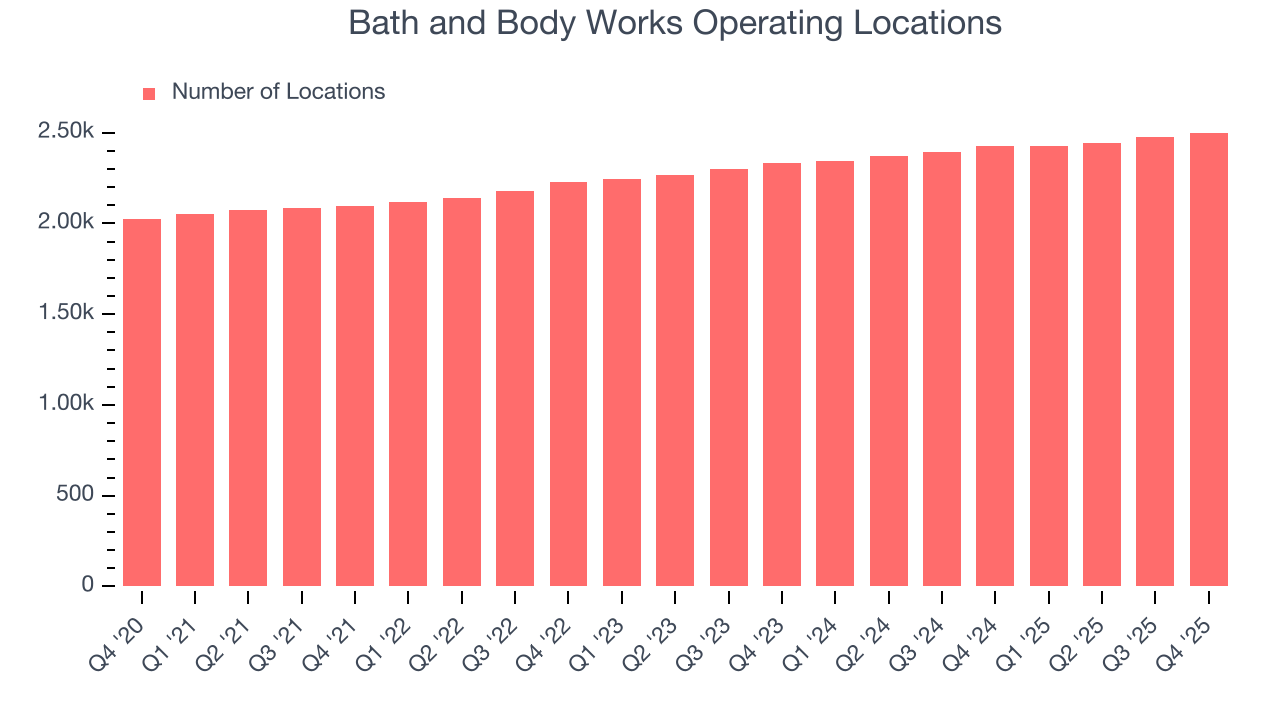

- Locations: 2,500 at quarter end, up from 2,424 in the same quarter last year

- Market Capitalization: $4.59 billion

Company Overview

Spun off from L Brands in 2020, Bath & Body Works (NYSE:BBWI) is a personal care and home fragrance retailer where consumers can find specialty shower gels, scented candles for the home, and lotions.

While many retailers define themselves based on visuals and aesthetics, Bath & Body Works relies on the scents of their products. These scents are unique and diverse in range, and the company aims to rotate and update them on a seasonal basis in order to have fresh product every few months.

The core customer of Bath & Body Works is typically female, aged 18-45, who values self-care and indulgence. While consumers can buy generic or private label personal care products, the Bath & Body Works customer prefers the affordable luxury of higher-quality, specialty bath gels and moisturizers, for example.

The average Bath & Body Works store is around 3,000 square feet and typically located in shopping malls and strip shopping centers alongside other retailers. While stores are designed to be visually appealing, the main draw is the ability to test products and experience their scents. Bath & Body Works has an e-commerce presence, which was launched relatively late in 2006 when compared to other prominent retailers. The omnichannel approach gives the customer various options for shopping, returns, and exchanges. The e-commerce platform also features online-only promotions and customer reviews.

4. Beauty and Cosmetics Retailer

Beauty and cosmetics retailers understand that beauty is in the eye of the beholder, but a little lipstick, nail polish, and glowing skin also help the cause. These stores—which mostly cater to consumers but can also garner the attention of salon pros—aim to be a one-stop personal care and beauty products shop with many brands across many categories. E-commerce is changing how consumers buy cosmetics, so these retailers are constantly evolving to meet the customer where and how they want to shop.

Retailers offering specialized personal care products include Ulta Beauty (NASDAQ:ULTA) and Victoria’s Secret (NYSE:VSCO) as well as department stores such as Macy’s (NYSE:M) and Kohl’s (NYSE:KSS).

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $7.29 billion in revenue over the past 12 months, Bath and Body Works is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Bath and Body Works’s revenue declined by 1.2% per year over the last three years despite opening new stores. This implies its underperformance was driven by lower sales at existing, established locations.

This quarter, Bath and Body Works’s revenue fell by 2.3% year on year to $2.72 billion but beat Wall Street’s estimates by 4.3%. Company management is currently guiding for a 5% year-on-year decline in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to decline by 3.9% over the next 12 months, a slight deceleration versus the last three years. This projection is underwhelming and indicates its products will face some demand challenges.

6. Store Performance

Number of Stores

The number of stores a retailer operates is a critical driver of how quickly company-level sales can grow.

Bath and Body Works operated 2,500 locations in the latest quarter. It has opened new stores quickly over the last two years, averaging 3.7% annual growth, faster than the broader consumer retail sector.

When a retailer opens new stores, it usually means it’s investing for growth because demand is greater than supply, especially in areas where consumers may not have a store within reasonable driving distance.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Bath and Body Works’s demand has been shrinking over the last two years as its same-store sales have averaged 1.6% annual declines. This performance is concerning - it shows Bath and Body Works artificially boosts its revenue by building new stores. We’d like to see a company’s same-store sales rise before it takes on the costly, capital-intensive endeavor of expanding its store base.

Note that Bath and Body Works reports its same-store sales intermittently, so some data points are missing in the chart below.

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

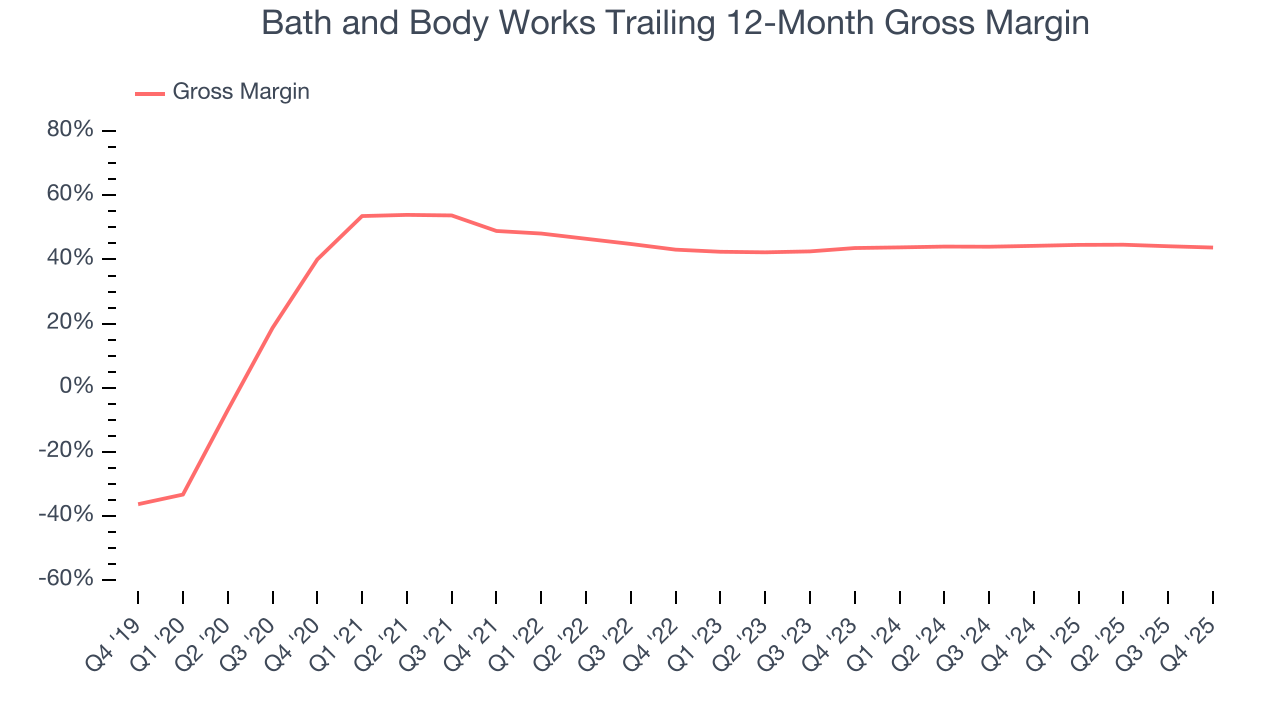

Bath and Body Works has good unit economics for a retailer, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 44% gross margin over the last two years. That means for every $100 in revenue, $56.01 went towards paying for inventory, transportation, and distribution.

This quarter, Bath and Body Works’s gross profit margin was 45.7%, down 1 percentage points year on year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

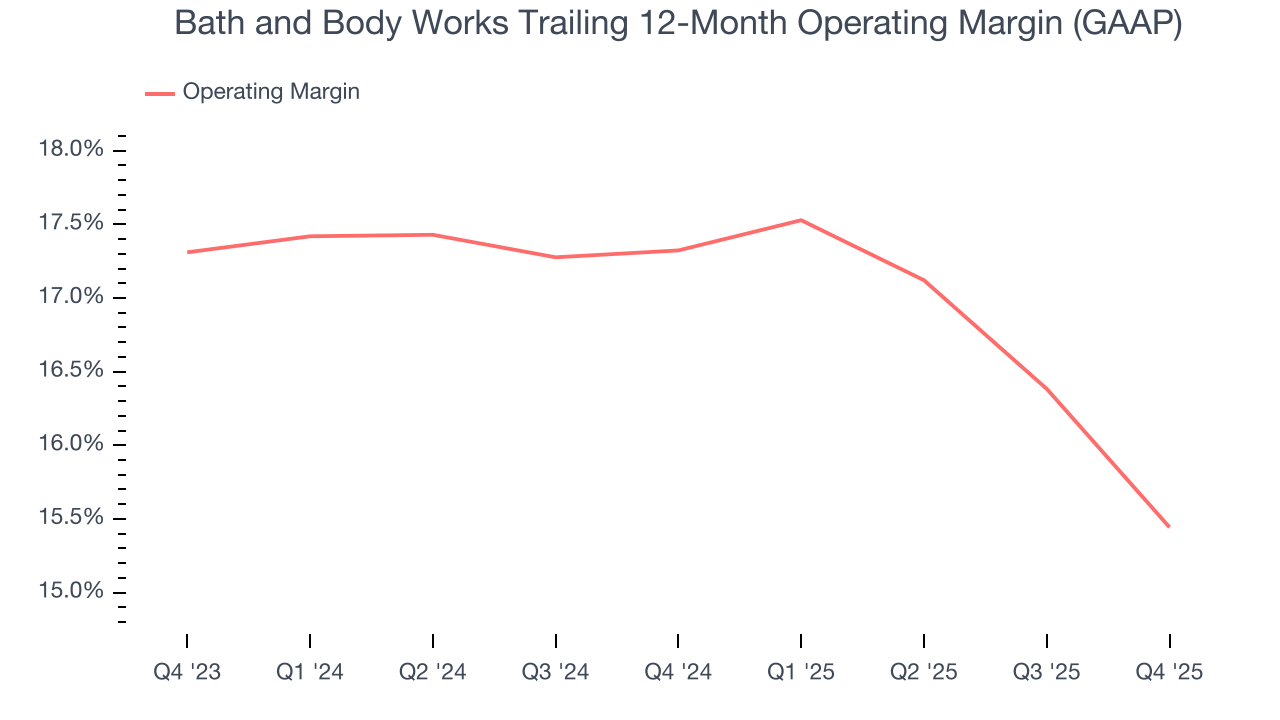

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Bath and Body Works has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer retail business, boasting an average operating margin of 16.4%. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Bath and Body Works’s operating margin decreased by 1.9 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Bath and Body Works become more profitable in the future.

In Q4, Bath and Body Works generated an operating margin profit margin of 22%, down 2.3 percentage points year on year. Since Bath and Body Works’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

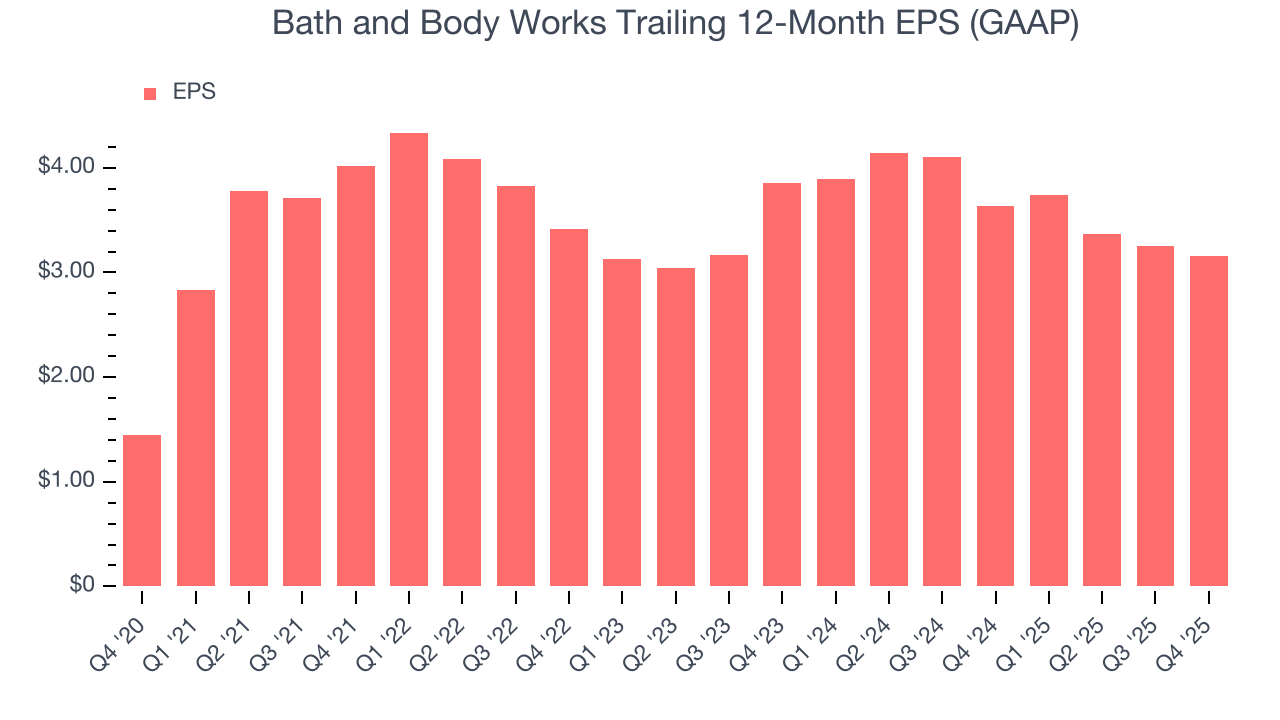

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Bath and Body Works, its EPS and revenue declined by 2.6% and 1.2% annually over the last three years. In a mature sector such as consumer retail, we tend to steer our readers away from companies with falling EPS because it could imply changing secular trends and preferences. If the tide turns unexpectedly, Bath and Body Works’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Bath and Body Works reported EPS of $1.99, down from $2.09 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Bath and Body Works’s full-year EPS of $3.16 to shrink by 18.8%.

10. Cash Is King

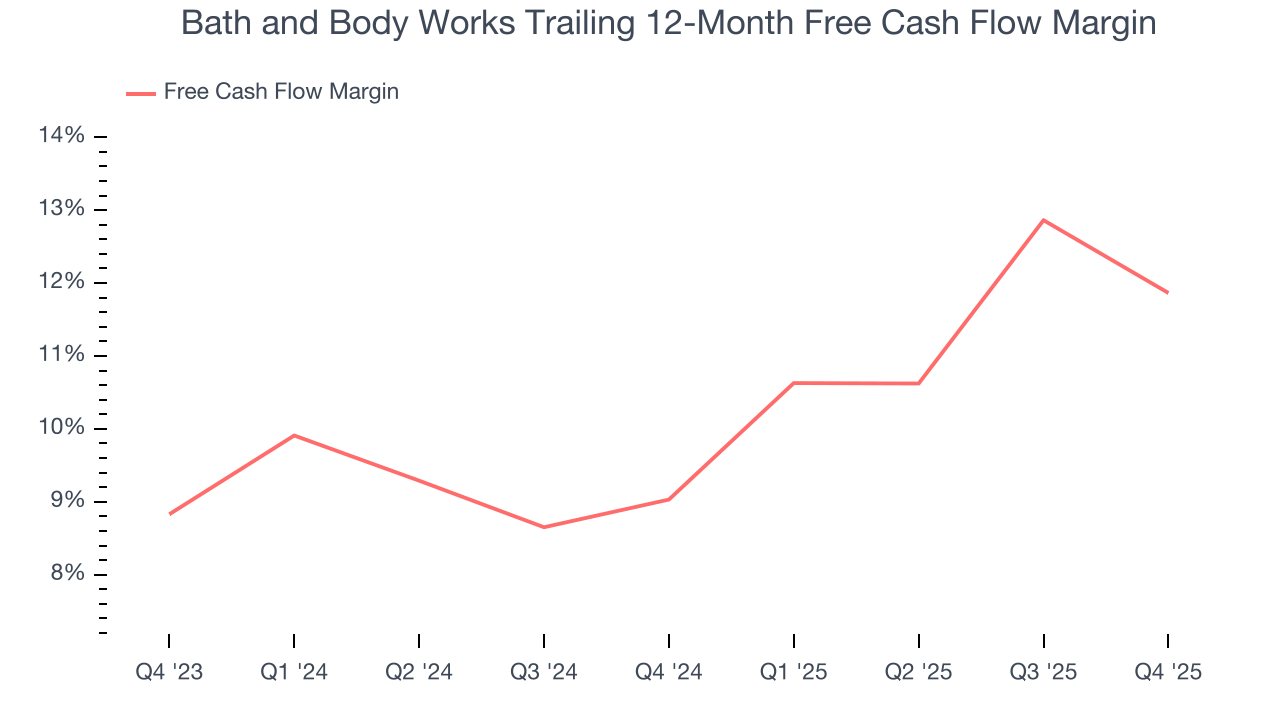

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Bath and Body Works has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer retail sector, averaging 10.4% over the last two years. Bath and Body Works has shown terrific cash profitability relative to peers over the last two years, giving the company fewer opportunities to return capital to shareholders.

Taking a step back, we can see that Bath and Body Works’s margin expanded by 2.8 percentage points over the last year. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Bath and Body Works’s free cash flow clocked in at $814 million in Q4, equivalent to a 29.9% margin. The company’s cash profitability regressed as it was 2.2 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Bath and Body Works hasn’t been the highest-quality company lately because of its poor top-line performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 46.3%, splendid for a consumer retail business.

12. Balance Sheet Assessment

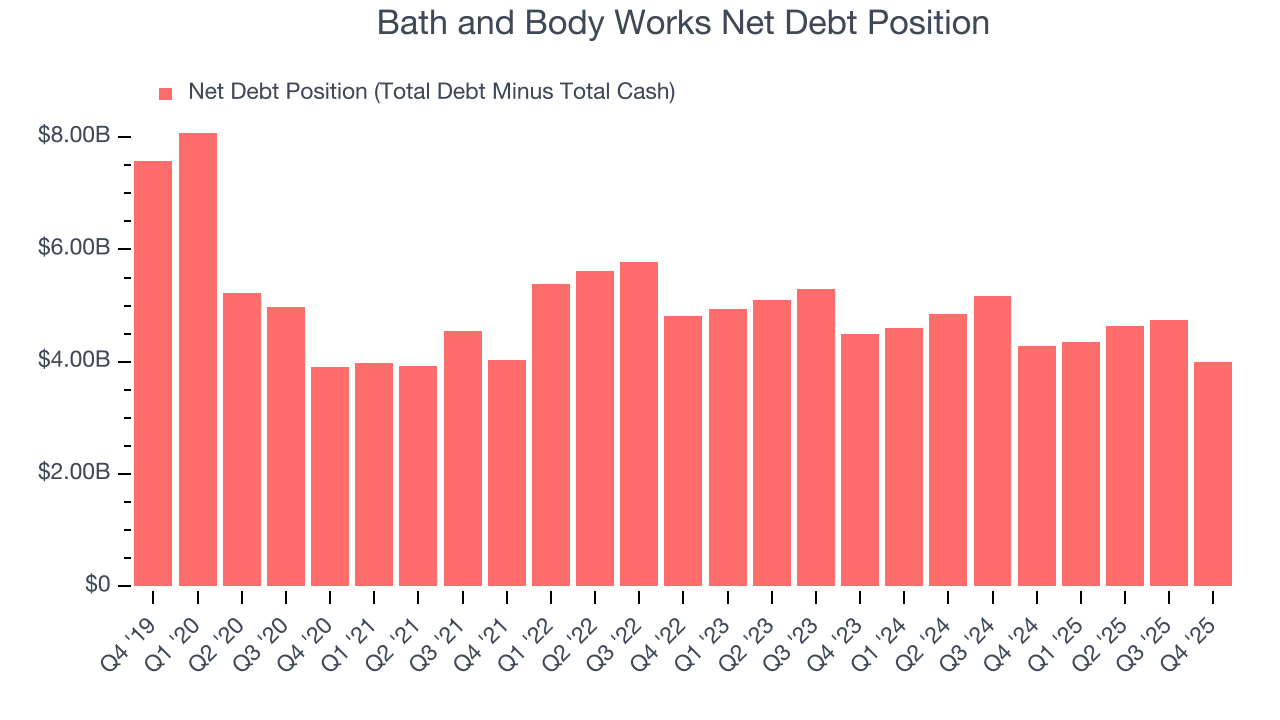

Bath and Body Works reported $953 million of cash and $4.95 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.40 billion of EBITDA over the last 12 months, we view Bath and Body Works’s 2.9× net-debt-to-EBITDA ratio as safe. We also see its $139 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Bath and Body Works’s Q4 Results

We were impressed by Bath and Body Works’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 2.5% to $23 immediately following the results.

14. Is Now The Time To Buy Bath and Body Works?

Updated: March 23, 2026 at 10:40 PM EDT

Before deciding whether to buy Bath and Body Works or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Bath and Body Works isn’t a terrible business, but it doesn’t pass our quality test. To kick things off, its revenue has declined over the last three years, and analysts expect its demand to deteriorate over the next 12 months. While its stellar ROIC suggests it has been a well-run company historically, the downside is its shrinking same-store sales tell us it will need to change its strategy to succeed. On top of that, its projected EPS for the next year is lacking.

Bath and Body Works’s P/E ratio based on the next 12 months is 7.4x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $27.62 on the company (compared to the current share price of $18.70).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.