Kodiak Gas Services (KGS)

Kodiak Gas Services doesn’t excite us. It not only barely produces cash but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why Kodiak Gas Services Is Not Exciting

Dominating the Permian Basin with a fleet focused on large horsepower units exceeding 1,000 horsepower each, Kodiak Gas Services (NYSE:KGS) operates compression equipment that maintains natural gas pressure for production, gathering, and transportation.

- poor earning stability in the sector may keep investors up at night

- Modest revenue base of $1.31 billion gives it less fixed cost leverage and fewer distribution channels than larger companies

- A bright spot is that its healthy EBITDA margin shows it’s a well-run company with efficient processes

Kodiak Gas Services’s quality is inadequate. There are more appealing investments to be made.

Why There Are Better Opportunities Than Kodiak Gas Services

At $56.02 per share, Kodiak Gas Services trades at 27.3x forward P/E. This multiple is higher than that of energy upstream and integrated energy peers; it’s also rich for the business quality. Not a great combination.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Kodiak Gas Services (KGS) Research Report: Q4 CY2025 Update

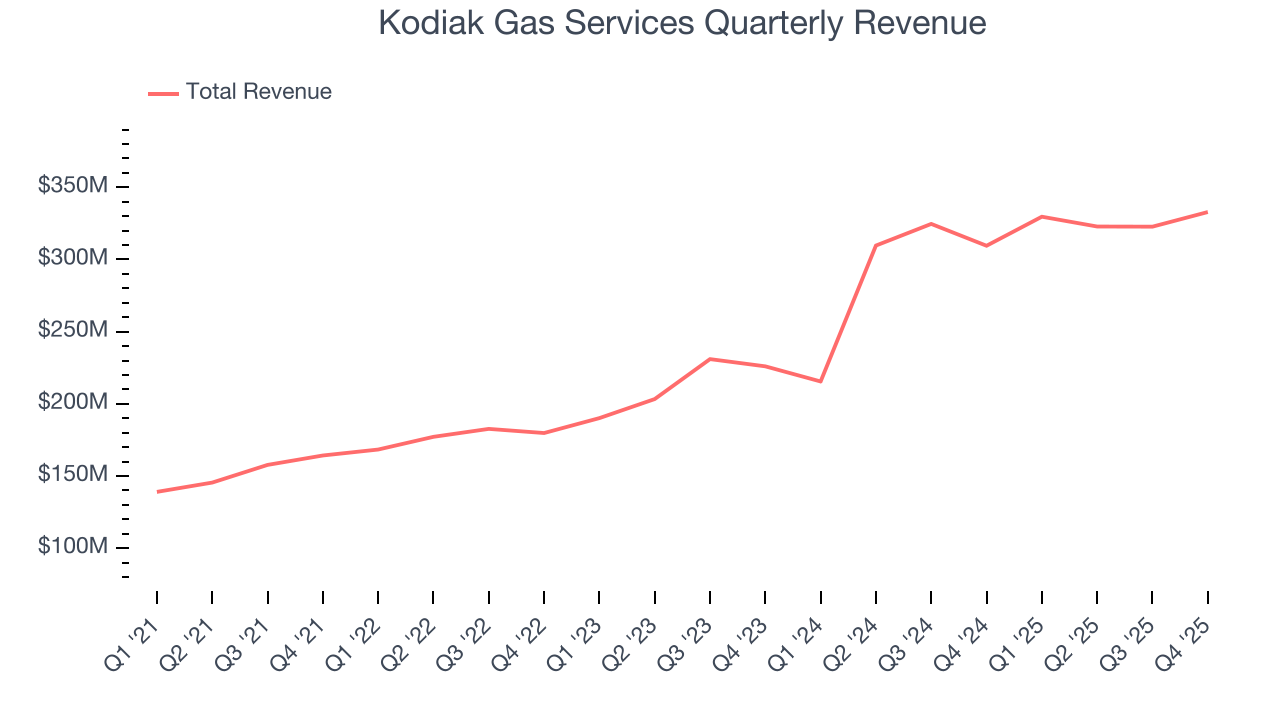

Natural gas compression provider Kodiak Gas Services (NYSE:KGS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 7.5% year on year to $332.9 million. Its non-GAAP profit of $0.35 per share was 34.3% below analysts’ consensus estimates.

Kodiak Gas Services (KGS) Q4 CY2025 Highlights:

- Revenue: $332.9 million vs analyst estimates of $330.2 million (7.5% year-on-year growth, 0.8% beat)

- Adjusted EPS: $0.35 vs analyst expectations of $0.53 (34.3% miss)

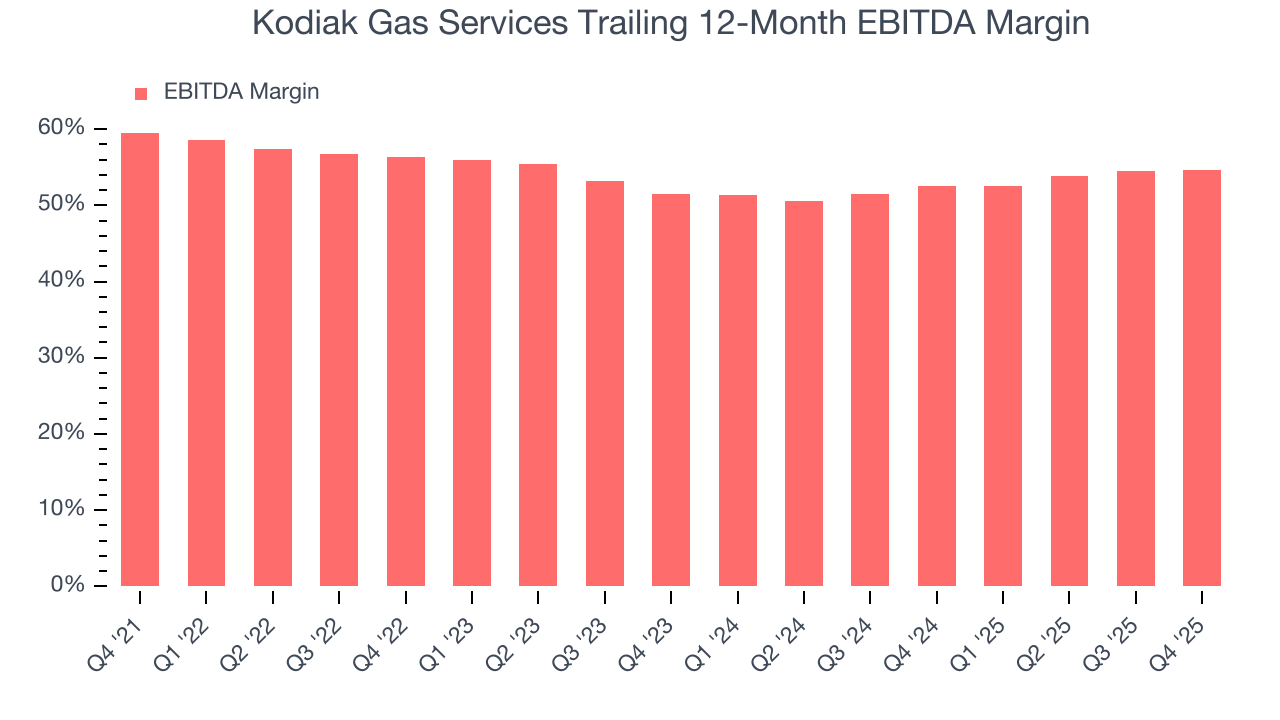

- Adjusted EBITDA: $184.5 million vs analyst estimates of $180.8 million (55.4% margin, 2% beat)

- Operating Margin: 26.1%, up from 22.3% in the same quarter last year

- Free Cash Flow Margin: 42.7%, up from 14.6% in the same quarter last year

- Market Capitalization: $4.85 billion

Company Overview

Dominating the Permian Basin with a fleet focused on large horsepower units exceeding 1,000 horsepower each, Kodiak Gas Services (NYSE:KGS) operates compression equipment that maintains natural gas pressure for production, gathering, and transportation.

Think of natural gas compression like the heart pumping blood through your body—as gas moves through wells, pipelines, and processing facilities, it loses pressure and needs a mechanical boost to keep flowing. Kodiak's compression units solve this problem by maintaining the pressure needed to move natural gas from the wellhead to market. This is particularly crucial in unconventional shale formations like the Permian Basin, where lower initial reservoir pressures mean producers need significantly more compression horsepower than traditional wells.

The company's business revolves around two segments. Contract Services, which generates the majority of revenue, involves operating compression equipment under fixed-term contracts with upstream producers and midstream pipeline operators. Rather than owning compression equipment themselves, customers outsource this infrastructure to Kodiak, allowing them to deploy their capital on drilling and production activities instead. A midstream company gathering gas from multiple well pads, for example, might contract with Kodiak to provide the compression horsepower needed to push that gas into a processing plant or transmission pipeline. The Other Services segment provides ancillary offerings like equipment maintenance, station construction, parts sales, and freight services, often sold alongside compression contracts.

Kodiak strategically concentrates its operations where demand is strongest. Approximately 82% of its compression assets are deployed in the Permian Basin and Eagle Ford Shale, two of America's most prolific oil and gas producing regions. The company's fleet emphasizes large horsepower units—defined as individual units providing more than 1,000 horsepower—which account for roughly 78% of its 4.4 million horsepower fleet. These larger units align with industry trends toward multi-well pad drilling and high-volume gathering systems, and they offer better unit economics and lower emissions per horsepower compared to smaller equipment.

4. Infrastructure

Energy infrastructure companies build, own, and operate assets including pipelines, storage facilities, and processing plants that transport and handle oil, natural gas, and related products. These businesses often generate fee-based revenues providing cash flow stability. Tailwinds include growing production volumes requiring expanded takeaway capacity and export infrastructure demand. Long-term contracts with creditworthy counterparties reduce commodity price exposure. Headwinds include permitting and regulatory challenges delaying new projects, environmental opposition to pipeline construction, and potential long-term demand decline from energy transition. High capital intensity and interest rate sensitivity affecting financing costs present additional considerations.

Kodiak Gas Services competes with other compression service providers including USA Compression Partners (NYSE:USAC), Atlas Energy Solutions (NYSE:AESI), and privately held companies like Exterran Corporation and Archrock.

5. Revenue Scale

In Energy, scale separates fragile single-asset producers from platform-style businesses that generate revenue across entire basins and infrastructure networks. Kodiak Gas Services’s $1.31 billion of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Over the last four years, Kodiak Gas Services grew its sales at an excellent 21.2% compounded annual growth rate. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

This quarter, Kodiak Gas Services reported year-on-year revenue growth of 7.5%, and its $332.9 million of revenue exceeded Wall Street’s estimates by 0.8%.

7. Gross Margin

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

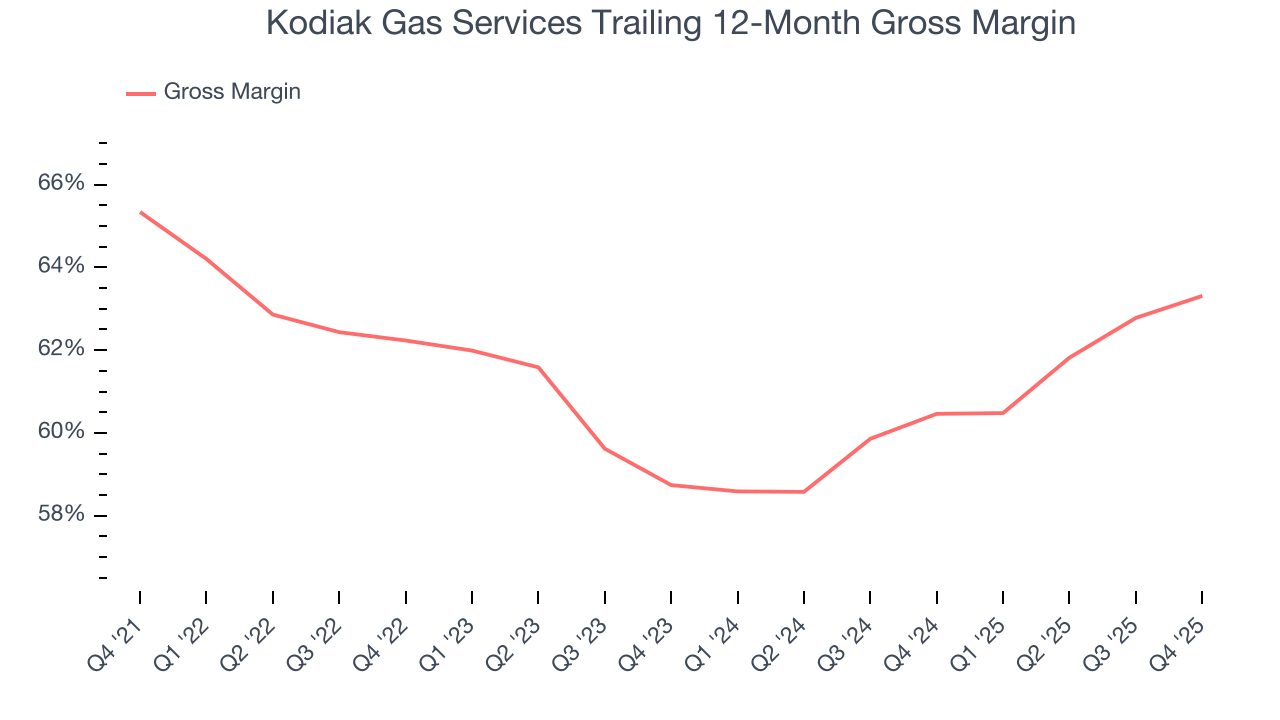

Kodiak Gas Services, which averaged 61.9% gross margin over the last five years, exhibits good unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an encouraging starting point for ultimate operating profits and free cash flow generation.

Kodiak Gas Services produced a 64% gross profit margin in Q4 , marking a 2.2 percentage point increase from 61.8% in the same quarter last year. Note that energy margins can be volatile due to commodity price changes.

8. Adjusted EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Kodiak Gas Services has been an efficient company over the last five years. It was one of the more profitable businesses in the energy upstream and integrated energy sector, boasting an average EBITDA margin of 54.5%.

Looking at the trend in its profitability, Kodiak Gas Services’s EBITDA margin decreased by 4.9 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see Kodiak Gas Services become more profitable in the future.

This quarter, Kodiak Gas Services generated an EBITDA margin profit margin of 55.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable. This adjusted EBITDA beat Wall Street’s estimates by 2%.

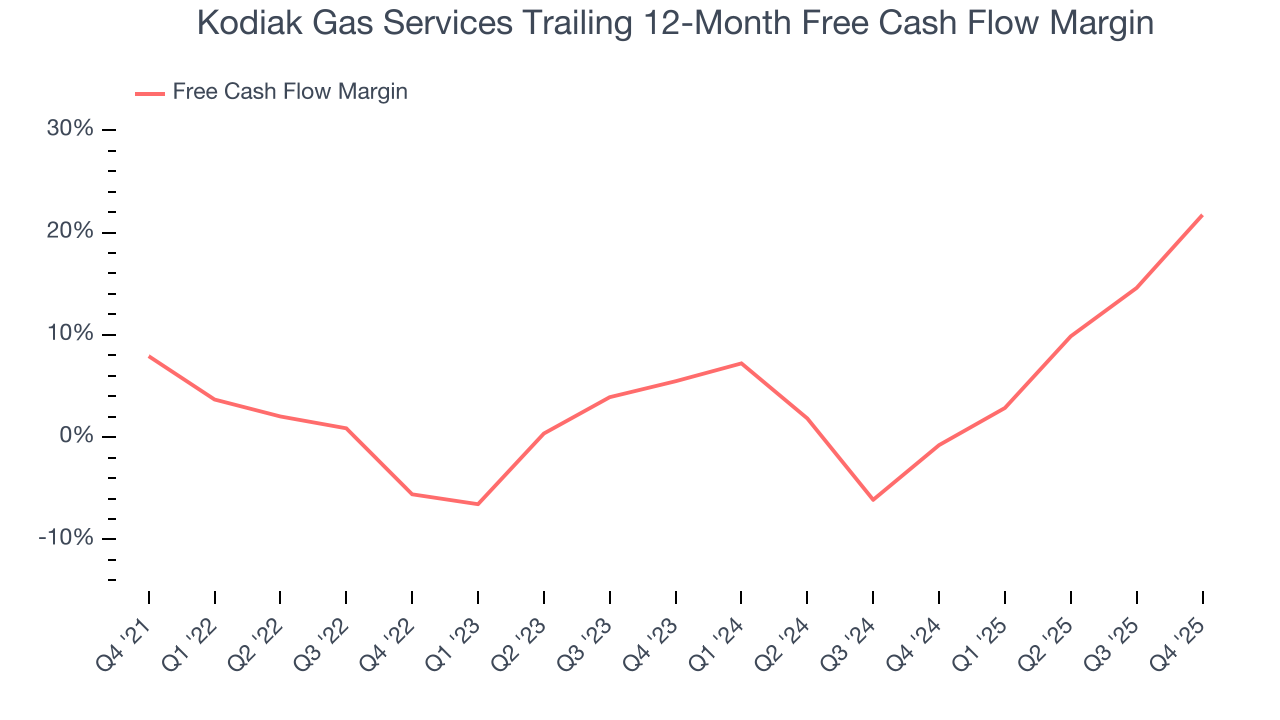

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

Kodiak Gas Services has shown mediocre cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 7.1%, below what we’d expect for an upstream and integrated energy business.

While the level of free cash flow margins is important, their consistency matters just as much.

Kodiak Gas Services’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 16.4 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Kodiak Gas Services? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Kodiak Gas Services’s free cash flow clocked in at $142 million in Q4, equivalent to a 42.7% margin. This result was good as its margin was 28 percentage points higher than in the same quarter last year, building on its favorable historical trend.

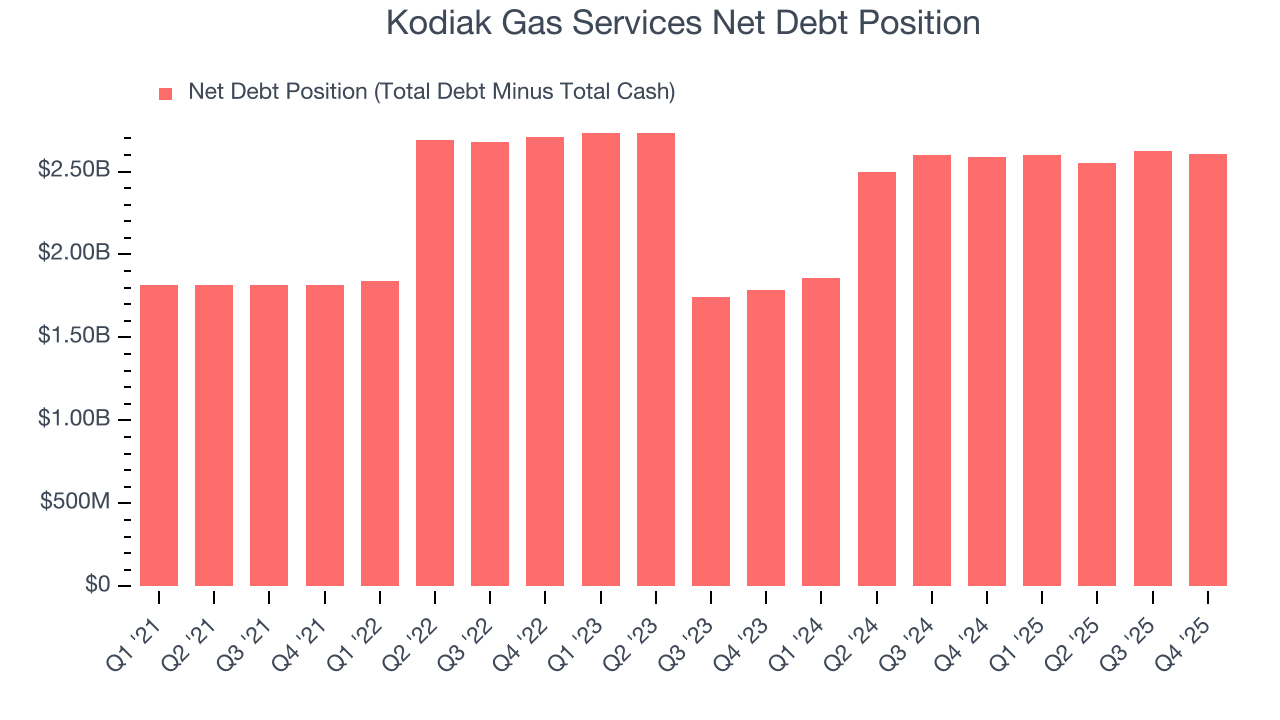

10. Balance Sheet Assessment

Kodiak Gas Services reported $3.18 million of cash and $2.61 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $715 million of EBITDA over the last 12 months, we view Kodiak Gas Services’s 3.6× net-debt-to-EBITDA ratio as safe. We also see its $198.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Kodiak Gas Services’s Q4 Results

It was good to see Kodiak Gas Services narrowly top analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, this quarter could have been better. The stock remained flat at $56.68 immediately following the results.

12. Is Now The Time To Buy Kodiak Gas Services?

Updated: March 21, 2026 at 1:17 AM EDT

When considering an investment in Kodiak Gas Services, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Kodiak Gas Services isn’t a terrible business, but it doesn’t pass our bar. Although its revenue growth over the last four years was impressive for the sector, it’s expected to deteriorate over the next 12 months and its free cash flow volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow. And while the company’s impressive EBITDA margins show it has a highly efficient business model, the downside is its subscale operations hasn't hit a level of diversification where investors can sleep easy at night.

Kodiak Gas Services’s P/E ratio based on the next 12 months is 27.3x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $53.08 on the company (compared to the current share price of $56.02), implying they don’t see much short-term potential in Kodiak Gas Services.