ON24 (ONTF)

ON24 keeps us up at night. Its shrinking sales suggest demand is waning and its lousy free cash flow generation doesn’t do it any favors.― StockStory Analyst Team

1. News

2. Summary

Why We Think ON24 Will Underperform

Powering over 1,700 companies' virtual marketing efforts since 1998, ON24 (NYSE:ONTF) provides a cloud-based platform that enables businesses to create interactive digital experiences and capture actionable data from customer engagement.

- Software offerings aren’t resonating in this new AI paradigm as its revenue declined by 2.4% annually over the last five years

- Customers were hesitant to make long-term commitments to its software as its ARR averaged 5.3% declines over the last year

- Projected sales for the next 12 months are flat and suggest demand will be subdued

ON24 doesn’t meet our quality criteria. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than ON24

ON24’s stock price of $8.05 implies a valuation ratio of 2.5x forward price-to-sales. ON24’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. ON24 (ONTF) Research Report: Q4 CY2025 Update

Digital engagement platform ON24 (NYSE:ONTF) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 5.6% year on year to $34.64 million. Its non-GAAP profit of $0.05 per share was significantly above analysts’ consensus estimates.

ON24 (ONTF) Q4 CY2025 Highlights:

- Revenue: $34.64 million vs analyst estimates of $33.93 million (5.6% year-on-year decline, 2.1% beat)

- Adjusted EPS: $0.05 vs analyst estimates of $0.02 (significant beat)

- Adjusted Operating Income: $763,000 vs analyst estimates of -$404,670 (2.2% margin, significant beat)

- Operating Margin: -23.5%, up from -32.1% in the same quarter last year

- Free Cash Flow was -$2.21 million, down from $2.16 million in the previous quarter

- Billings: $37.16 million at quarter end, down 6.5% year on year

- Market Capitalization: $341.7 million

Company Overview

Powering over 1,700 companies' virtual marketing efforts since 1998, ON24 (NYSE:ONTF) provides a cloud-based platform that enables businesses to create interactive digital experiences and capture actionable data from customer engagement.

The company's intelligent engagement platform helps businesses convert digital interactions into revenue through a suite of products designed for creating personalized, data-rich experiences. ON24's core offerings include Elite (interactive webinars), Forums (video-based discussions), Go Live (video events), Breakouts (networking rooms), Engagement Hub (content portals), and Target (personalized landing pages).

What sets ON24 apart is its focus on capturing "first-person data" - direct engagement information from prospective customers interacting with content. This data flows into ON24 Intelligence and their AI-powered Analytics and Content Engine (ACE), allowing businesses to understand prospect behavior, personalize future interactions, and integrate insights with marketing automation and CRM systems like Salesforce and HubSpot.

A typical customer might use ON24 to host a product demonstration webinar where attendees can ask questions, participate in polls, and download resources. The platform captures each interaction, enabling the marketing team to identify the most engaged prospects, personalize follow-up communications, and provide sales teams with detailed behavior insights. This targeted approach helps business-to-business (B2B) companies move beyond simple digital marketing into more sophisticated, insight-driven customer engagement across the entire buyer journey.

4. Virtual Events Software

Online marketing and sales are expanding at a rapid pace. Compared to the offline advertising market, which has been affected by the Covid pandemic and is challenging to measure and improve, more organizations are expected to adopt data-driven digital engagement platforms to better engage their customers online.

ON24 competes with web conferencing platforms like Zoom (NASDAQ:ZM) and Microsoft Teams (NASDAQ:MSFT), virtual event solutions from Cvent (NYSE:CVT) and Notified, and marketing engagement tools from Adobe (NASDAQ:ADBE) and Cisco (NASDAQ:CSCO).

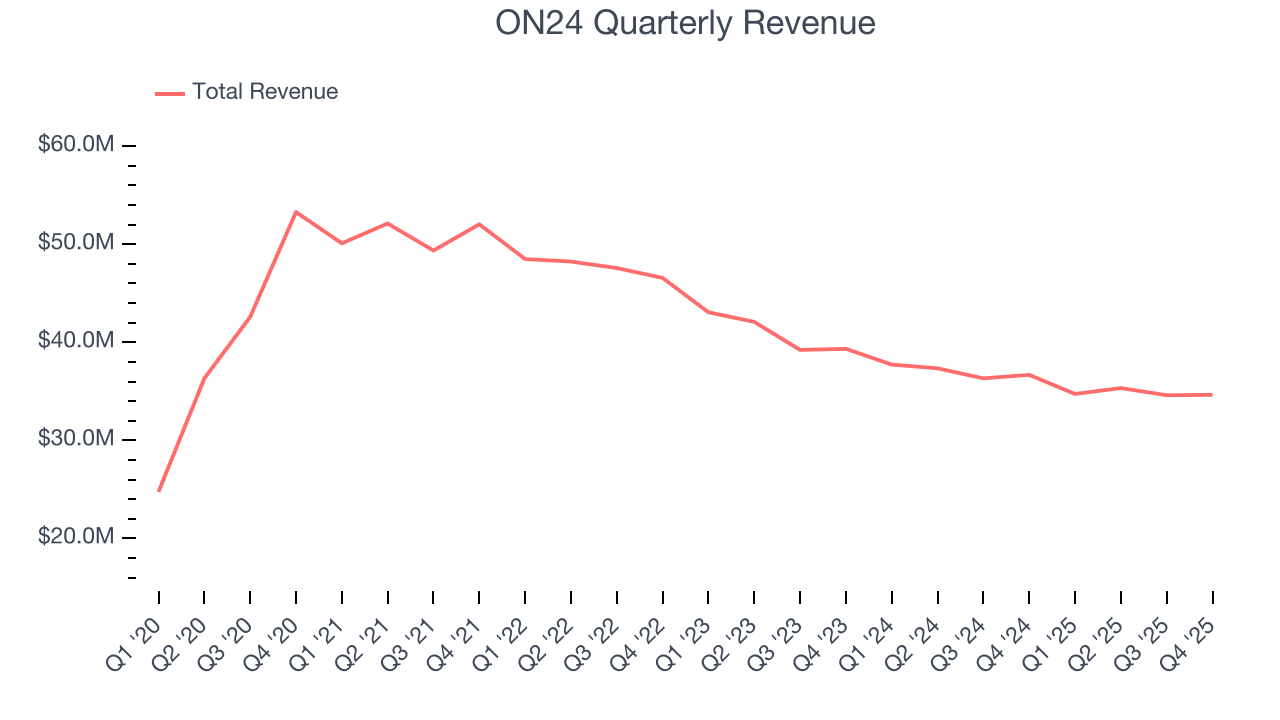

5. Revenue Growth

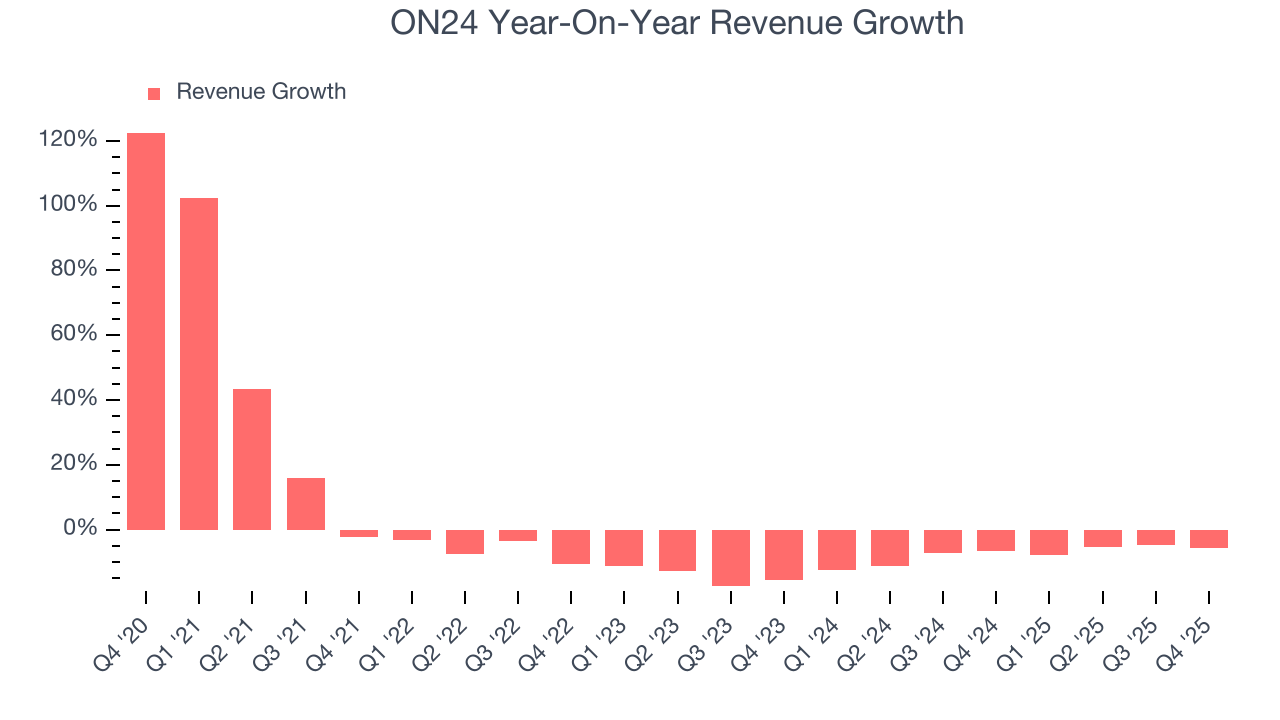

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. ON24’s demand was weak over the last five years as its sales fell at a 2.4% annual rate. This wasn’t a great result and suggests it’s a low quality business.

We at StockStory place the most emphasis on long-term growth, but within software, a half-decade historical view may miss recent innovations or disruptive industry trends. ON24’s recent performance shows its demand remained suppressed as its revenue has declined by 7.8% annually over the last two years.

This quarter, ON24’s revenue fell by 5.6% year on year to $34.64 million but beat Wall Street’s estimates by 2.1%.

Looking ahead, sell-side analysts expect revenue to decline by 3.3% over the next 12 months. While this projection is better than its two-year trend, it’s tough to feel optimistic about a company facing demand difficulties.

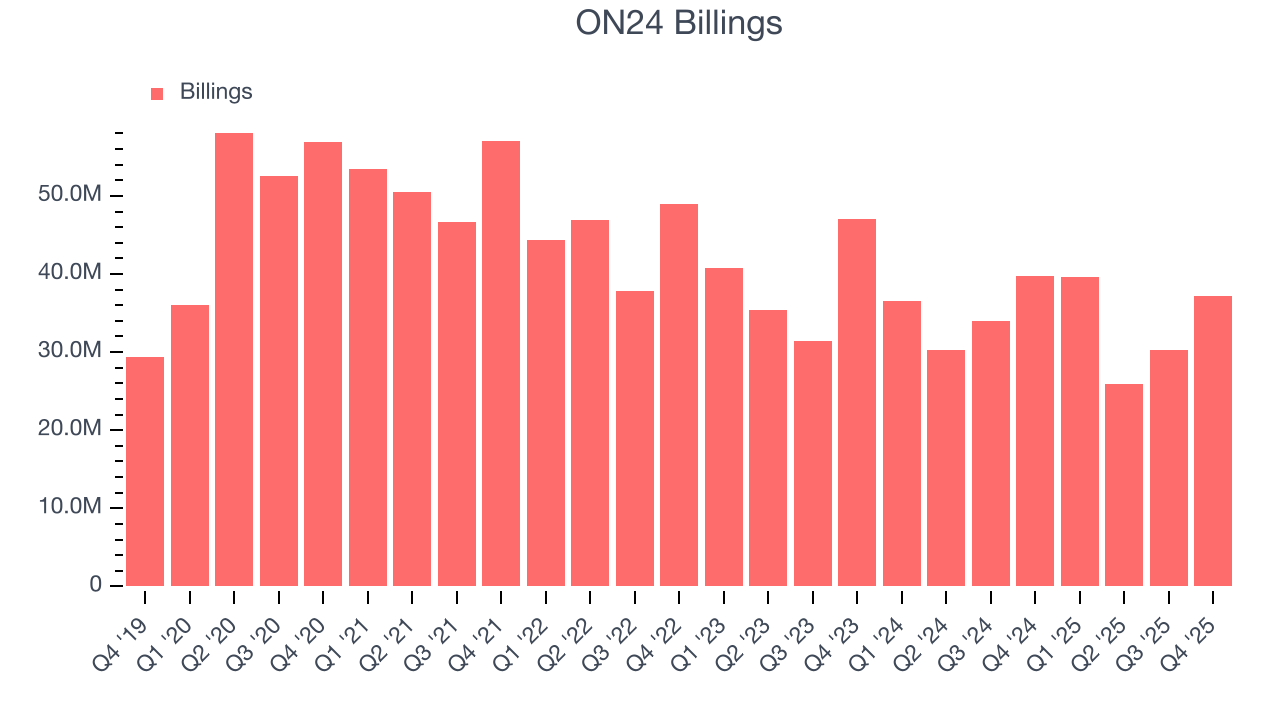

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

ON24’s billings came in at $37.16 million in Q4, and it averaged 5.8% year-on-year declines over the last four quarters. This performance mirrored its total sales and shows the company faced challenges in acquiring and retaining customers. It also suggests there may be increasing competition or market saturation.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for ON24 to acquire new customers as its CAC payback period checked in at 386.6 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

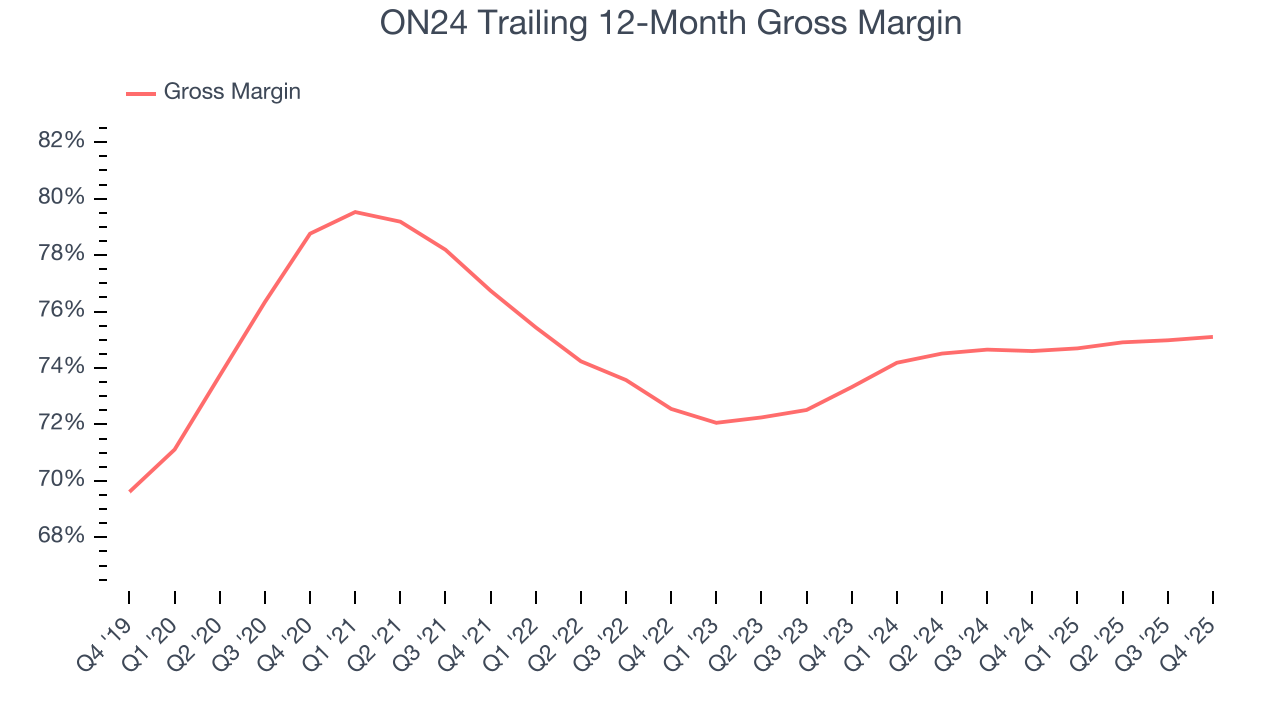

8. Gross Margin & Pricing Power

For software companies like ON24, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

ON24’s gross margin is good for a software business and points to its solid unit economics, competitive products and services, and lack of meaningful pricing pressure. As you can see below, it averaged an impressive 75.1% gross margin over the last year. Said differently, ON24 paid its providers $24.90 for every $100 in revenue.

The market not only cares about gross margin levels but also how they change over time because expansion creates firepower for profitability and free cash generation. ON24 has seen gross margins improve by 1.8 percentage points over the last 2 year, which is solid in the software space.

ON24’s gross profit margin came in at 75% this quarter, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

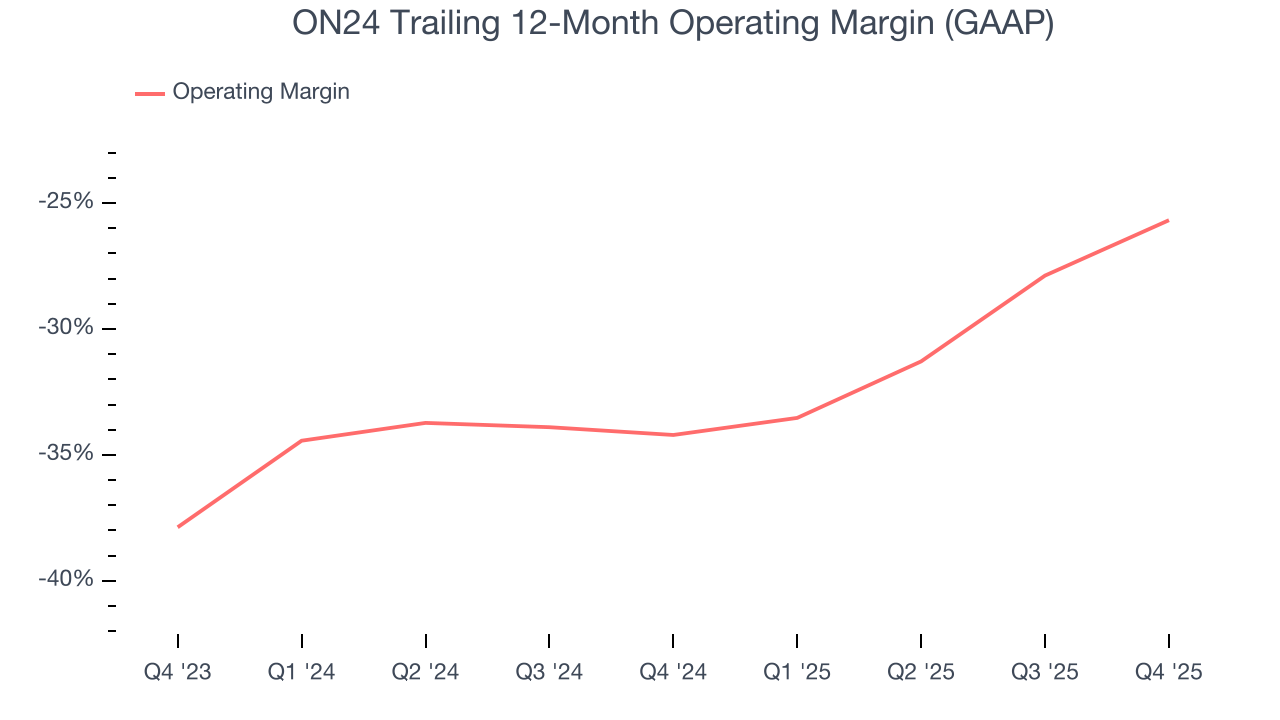

9. Operating Margin

ON24’s expensive cost structure has contributed to an average operating margin of negative 25.7% over the last year. Unprofitable software companies require extra attention because they spend heaps of money to capture market share. As seen in its historically underwhelming revenue performance, this strategy hasn’t worked so far, and it’s unclear what would happen if ON24 reeled back its investments. Wall Street seems to think it will face some obstacles, and we tend to agree.

On the plus side, ON24’s operating margin rose by 8.5 percentage points over the last two years. Still, it will take much more for the company to reach long-term profitability.

In Q4, ON24 generated a negative 23.5% operating margin. The company's consistent lack of profits raise a flag.

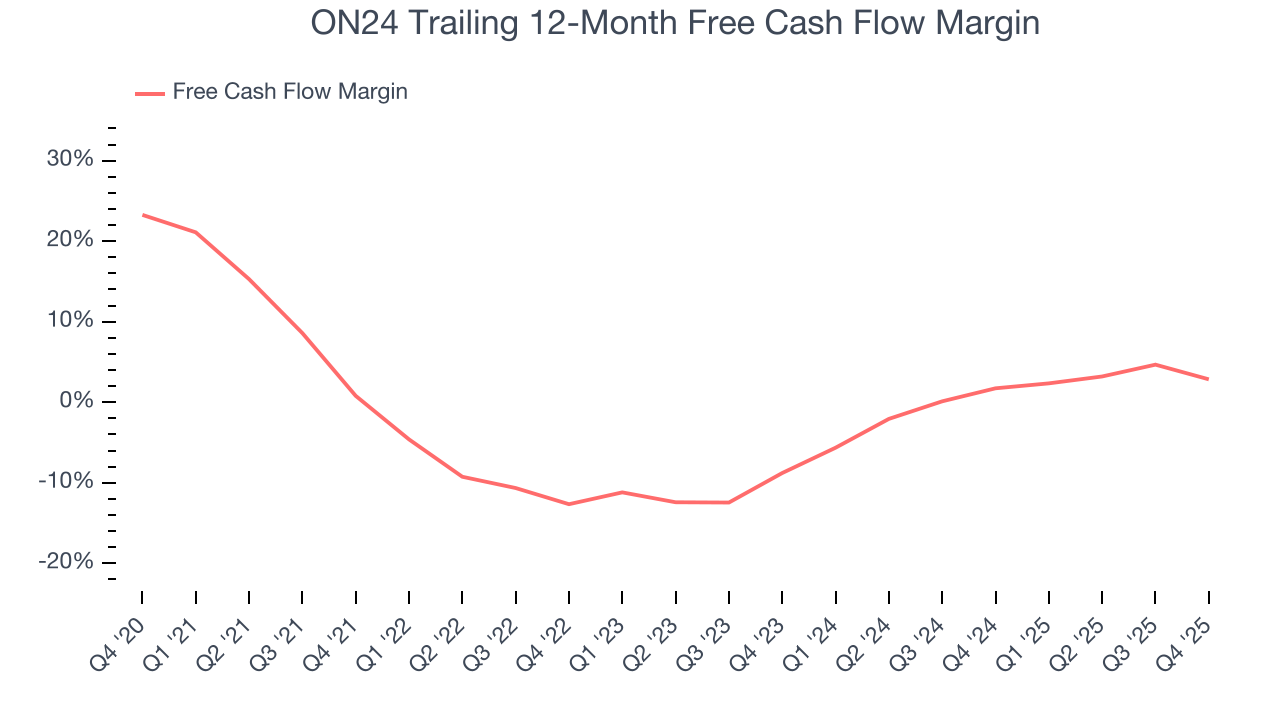

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

ON24 has shown poor cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 2.8%, lousy for a software business.

ON24 burned through $2.21 million of cash in Q4, equivalent to a negative 6.4% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

Over the next year, analysts predict ON24’s cash conversion will improve. Their consensus estimates imply its free cash flow margin of 2.8% for the last 12 months will increase to 4.9%, giving it more flexibility for investments, share buybacks, and dividends.

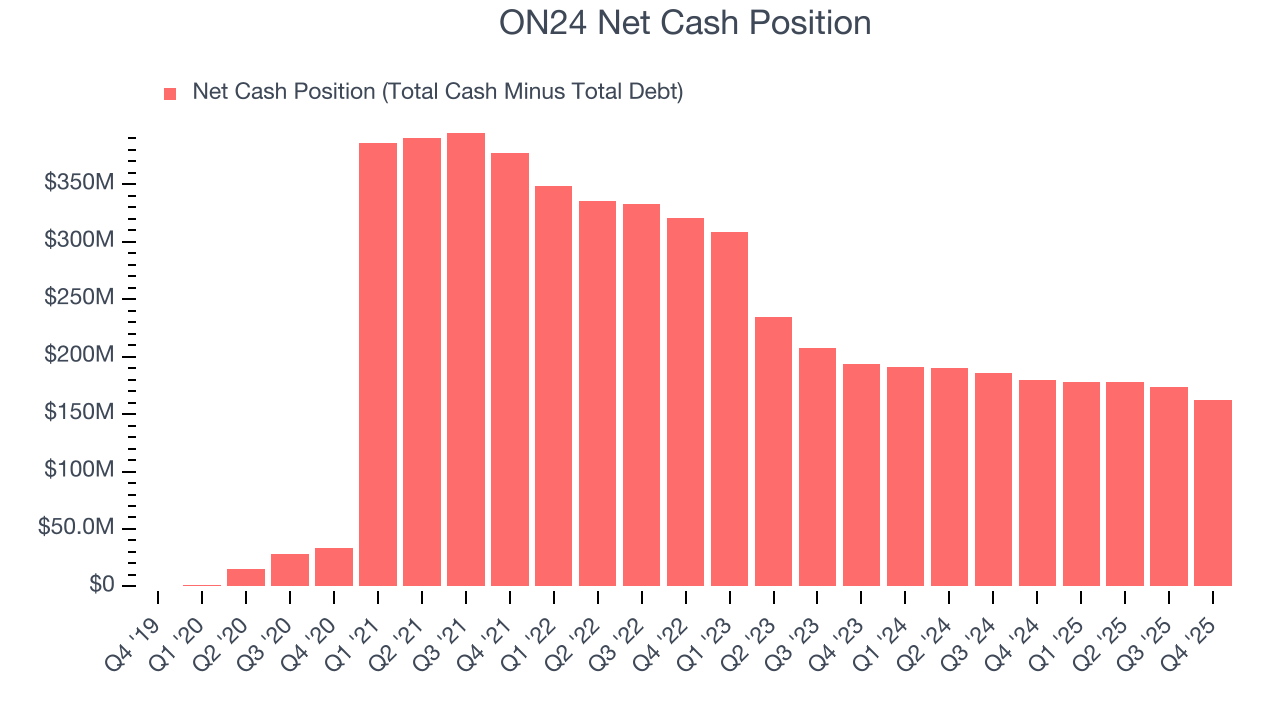

11. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

ON24 is a well-capitalized company with $167.5 million of cash and $5.57 million of debt on its balance sheet. This $162 million net cash position is 47.4% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from ON24’s Q4 Results

It was encouraging to see ON24 beat analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed and its billings fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $8.01 immediately after reporting.

13. Is Now The Time To Buy ON24?

Updated: March 17, 2026 at 10:18 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

ON24 falls short of our quality standards. To begin with, its revenue has declined over the last five years. While its gross margin suggests it can generate sustainable profits, the downside is its ARR has disappointed and shows the company is having difficulty retaining customers and their spending. On top of that, its operating margins reveal poor profitability compared to other software companies.

ON24’s price-to-sales ratio based on the next 12 months is 2.5x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $8.10 on the company (compared to the current share price of $8.06).