Sportsman's Warehouse (SPWH)

Sportsman's Warehouse faces an uphill battle. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sportsman's Warehouse Will Underperform

A go-to destination for individuals passionate about hunting, fishing, camping, hiking, shooting sports, and more, Sportsman's Warehouse (NASDAQ:SPWH) is an American specialty retailer offering a diverse range of active gear, equipment, and apparel.

- Poor same-store sales performance over the past two years indicates it’s having trouble bringing new shoppers into its brick-and-mortar locations

- Products have few die-hard fans as sales have declined by 5.4% annually over the last three years

- Limited cash reserves may force the company to seek unfavorable financing terms that could dilute shareholders

Sportsman's Warehouse doesn’t fulfill our quality requirements. We’re redirecting our focus to better businesses.

Why There Are Better Opportunities Than Sportsman's Warehouse

Sportsman's Warehouse is trading at $1.35 per share, or 21x forward EV-to-EBITDA. This multiple expensive for its subpar fundamentals.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Sportsman's Warehouse (SPWH) Research Report: Q3 CY2025 Update

Outdoor specialty retailer Sportsman's Warehouse (NASDAQ:SPWH) met Wall Streets revenue expectations in Q3 CY2025, with sales up 2.2% year on year to $331.3 million. Its non-GAAP profit of $0.08 per share was in line with analysts’ consensus estimates.

Sportsman's Warehouse (SPWH) Q3 CY2025 Highlights:

- Revenue: $331.3 million vs analyst estimates of $331.1 million (2.2% year-on-year growth, in line)

- Adjusted EPS: $0.08 vs analyst estimates of $0.08 (in line)

- Adjusted EBITDA: $18.62 million vs analyst estimates of $18.4 million (5.6% margin, 1.2% beat)

- EBITDA guidance for the full year is $24 million at the midpoint, below analyst estimates of $34.61 million

- Operating Margin: 1.3%, in line with the same quarter last year

- Free Cash Flow was $8.74 million, up from -$6.16 million in the same quarter last year

- Same-Store Sales rose 2.2% year on year (-5.7% in the same quarter last year)

- Market Capitalization: $92.62 million

Company Overview

A go-to destination for individuals passionate about hunting, fishing, camping, hiking, shooting sports, and more, Sportsman's Warehouse (NASDAQ:SPWH) is an American specialty retailer offering a diverse range of active gear, equipment, and apparel.

The company was founded in 1986 and its extensive selection encompasses everything from fishing rods and camping tents to firearms and apparel designed to withstand rugged environments.

Sportsman’s Warehouse views itself as not only a retailer but also a central pillar of the outdoor community. The company often hosts workshops, seminars, and events that provide insights into outdoor activities, gear maintenance, and safety practices.

Consistent with this theme, each store is designed to promote community building and acts as a hub for like-minded individuals to gather, exchange stories, and share their love for the outdoors. The stores feature spacious layouts that showcase a wide array of products, making it easy for customers to explore and discover the right gear for their specific interests.

Sportsman's Warehouse also staffs its stores with knowledgeable associates, often experienced outdoor enthusiasts themselves, to offer personalized recommendations, answer questions, and share insights to help customers make informed decisions.

Whether customers are seasoned outdoor veterans or newcomers looking to explore the natural world, Sportsman's Warehouse Holdings offers a comprehensive selection of products and resources to elevate their outdoor experiences.

4. Sports & Outdoor Equipment Retailer

Some of us spend our leisure time vegging out, but many others take to the courts, fields, beaches, and campsites; sports equipment retailers cater to the avid sportsman as well as the weekend warrior. Shoppers can find everything from tents to lawn games to baseball bats to satisfy their athletic and leisure needs along with competitive prices and helpful store associates that can talk through brands, sizing, and product quality. This is a category that has moved rapidly online over the last few decades, so these sports and outdoor equipment retailers have needed to be nimble and aggressive with their e-commerce and omnichannel presences.

Retailers offering sporting and outdoor goods include Academy Sports and Outdoor (NASDAQ:ASO), Camping World (NYSE:CWH), Dick’s Sporting Goods (NYSE:DKS), and Hibbett (NASDAQ:HIBB).

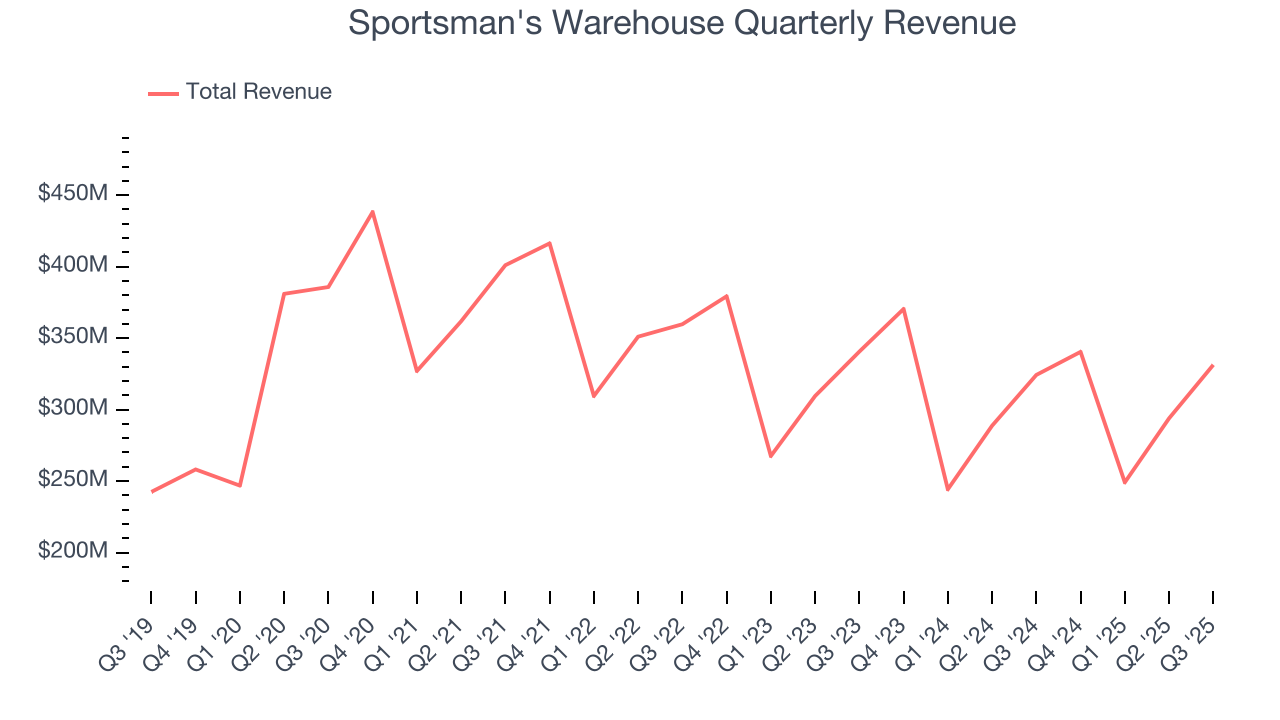

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $1.21 billion in revenue over the past 12 months, Sportsman's Warehouse is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sportsman's Warehouse’s demand was weak over the last three years (we compare to 2019 to normalize for COVID-19 impacts). Its sales fell by 5.4% annually, a rough starting point for our analysis.

This quarter, Sportsman's Warehouse grew its revenue by 2.2% year on year, and its $331.3 million of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 1.7% over the next 12 months. Although this projection implies its newer products will spur better top-line performance, it is still below average for the sector.

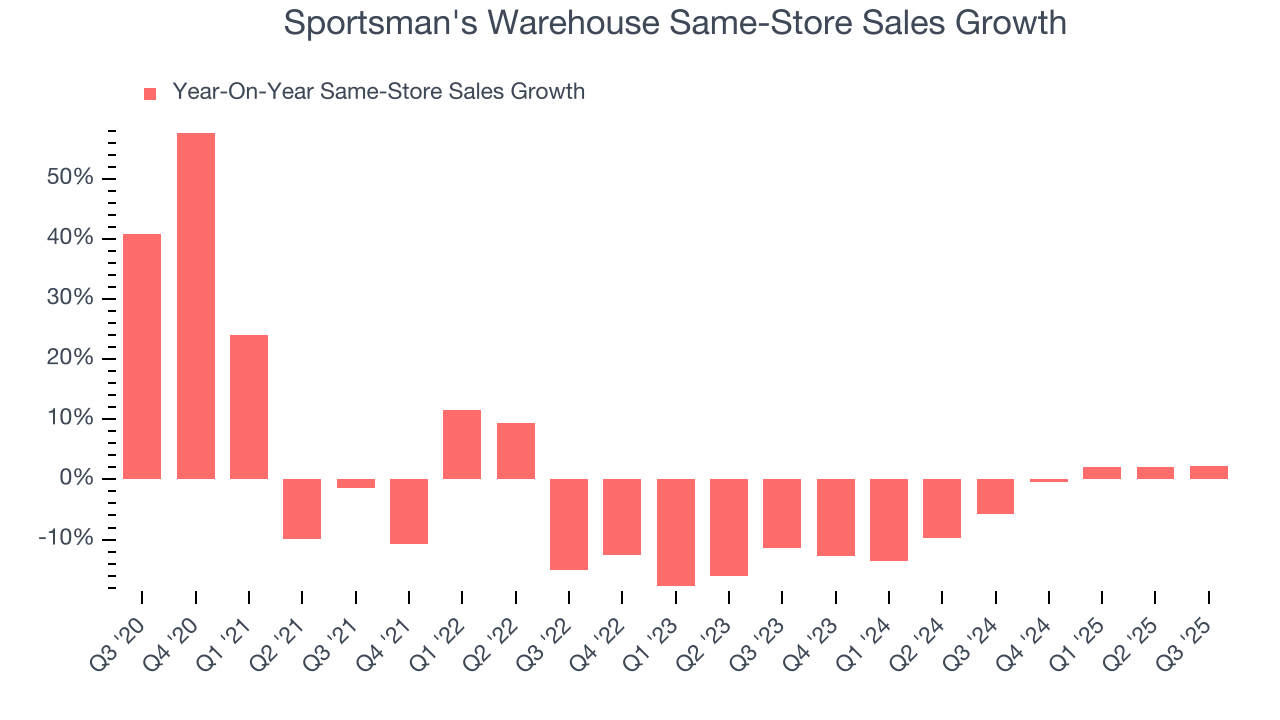

6. Same-Store Sales

Sportsman's Warehouse’s demand has been shrinking over the last two years as its same-store sales have averaged 4.5% annual declines.

In the latest quarter, Sportsman's Warehouse’s same-store sales rose 2.2% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

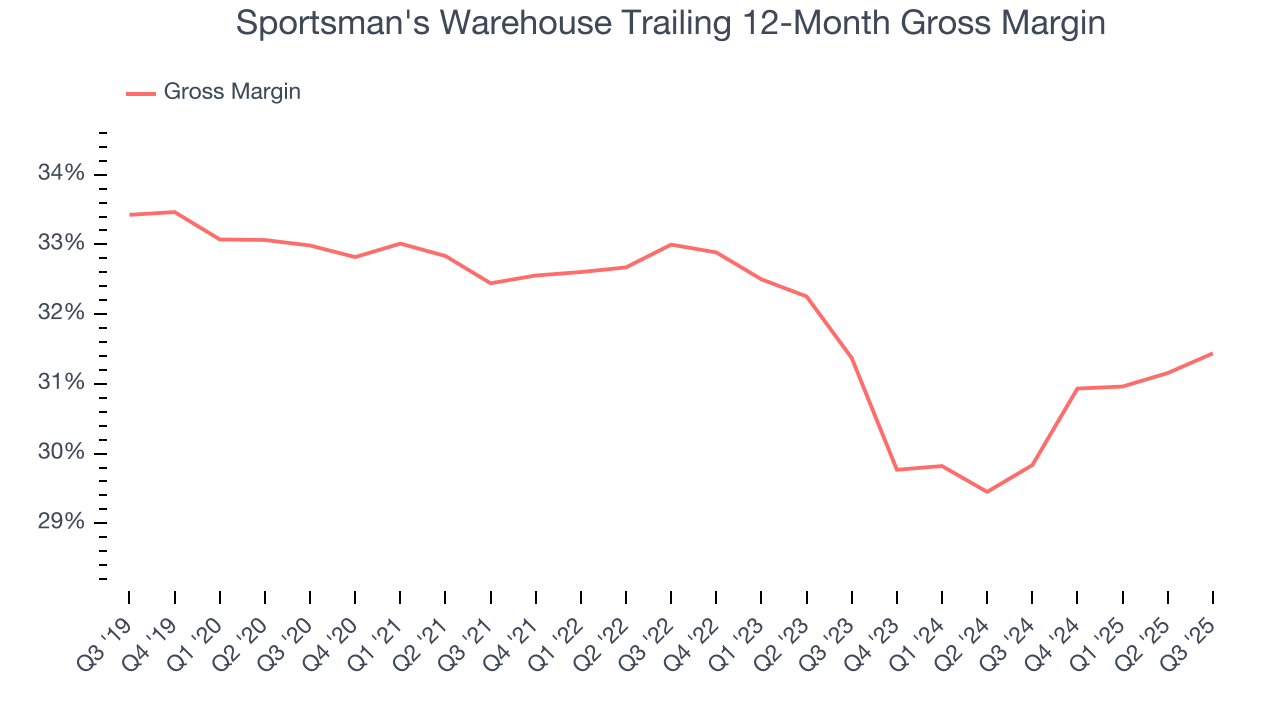

7. Gross Margin & Pricing Power

Sportsman's Warehouse has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 30.6% gross margin over the last two years. That means Sportsman's Warehouse paid its suppliers a lot of money ($69.37 for every $100 in revenue) to run its business.

Sportsman's Warehouse produced a 32.8% gross profit margin in Q3, marking a 1 percentage point increase from 31.8% in the same quarter last year. Sportsman's Warehouse’s full-year margin has also been trending up over the past 12 months, increasing by 1.6 percentage points. If this move continues, it could suggest better unit economics due to more leverage from its growing sales on the fixed portion of its cost of goods sold.

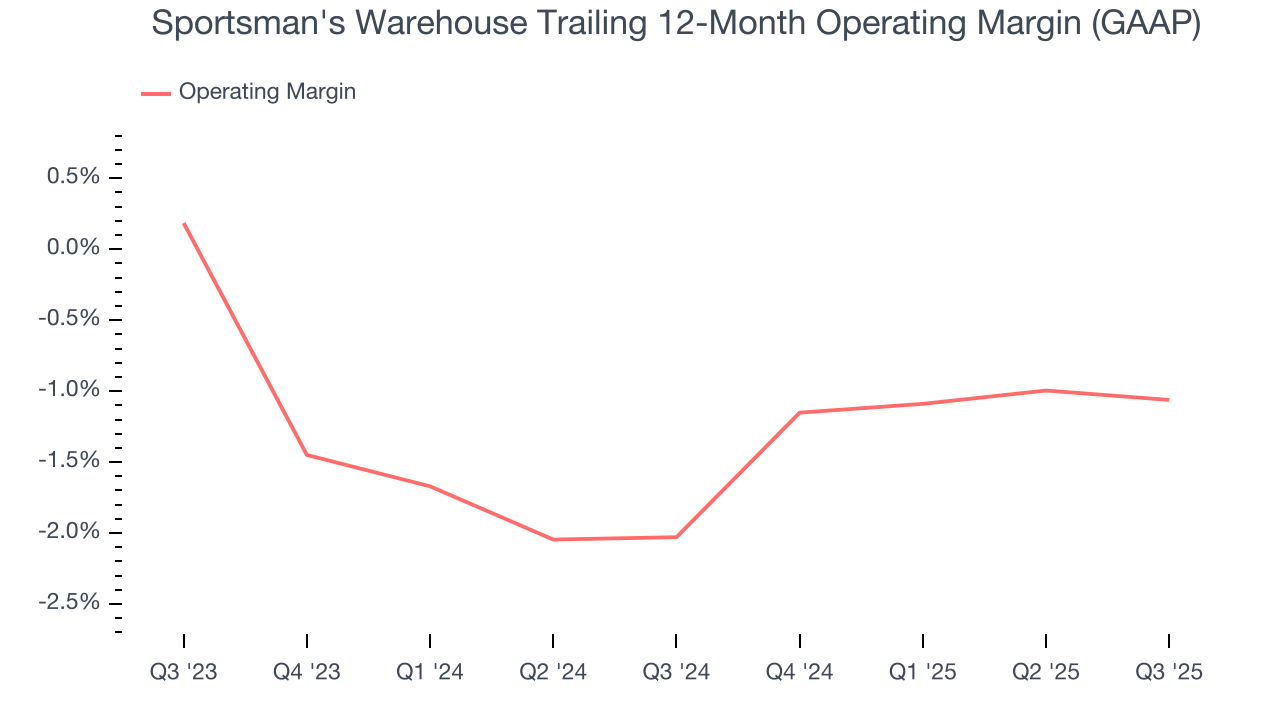

8. Operating Margin

Sportsman's Warehouse’s operating margin might fluctuated slightly over the last 12 months but has remained more or less the same, averaging negative 1.5% over the last two years. Unprofitable consumer retail companies that fail to improve their losses or grow sales rapidly deserve extra scrutiny. For the time being, it’s unclear if Sportsman's Warehouse’s business model is sustainable.

Looking at the trend in its profitability, Sportsman's Warehouse’s operating margin might fluctuated slightly but has generally stayed the same over the last year, meaning it will take a fundamental shift in the business model to change.

This quarter, Sportsman's Warehouse generated an operating margin profit margin of 1.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

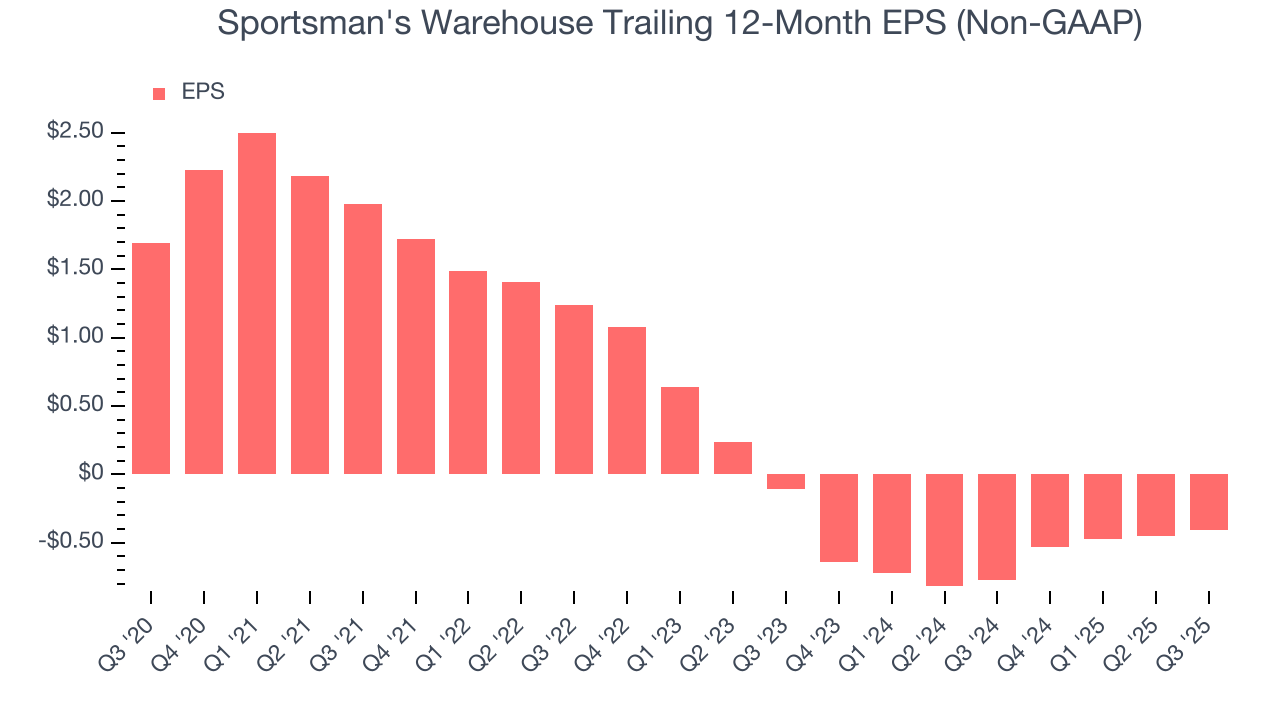

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Sportsman's Warehouse, its EPS declined by 32.6% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q3, Sportsman's Warehouse reported adjusted EPS of $0.08, up from $0.04 in the same quarter last year. This print beat analysts’ estimates by 5.3%. Over the next 12 months, Wall Street expects Sportsman's Warehouse to perform poorly. Analysts forecast its full-year EPS of negative $0.41 will tumble to negative $0.69.

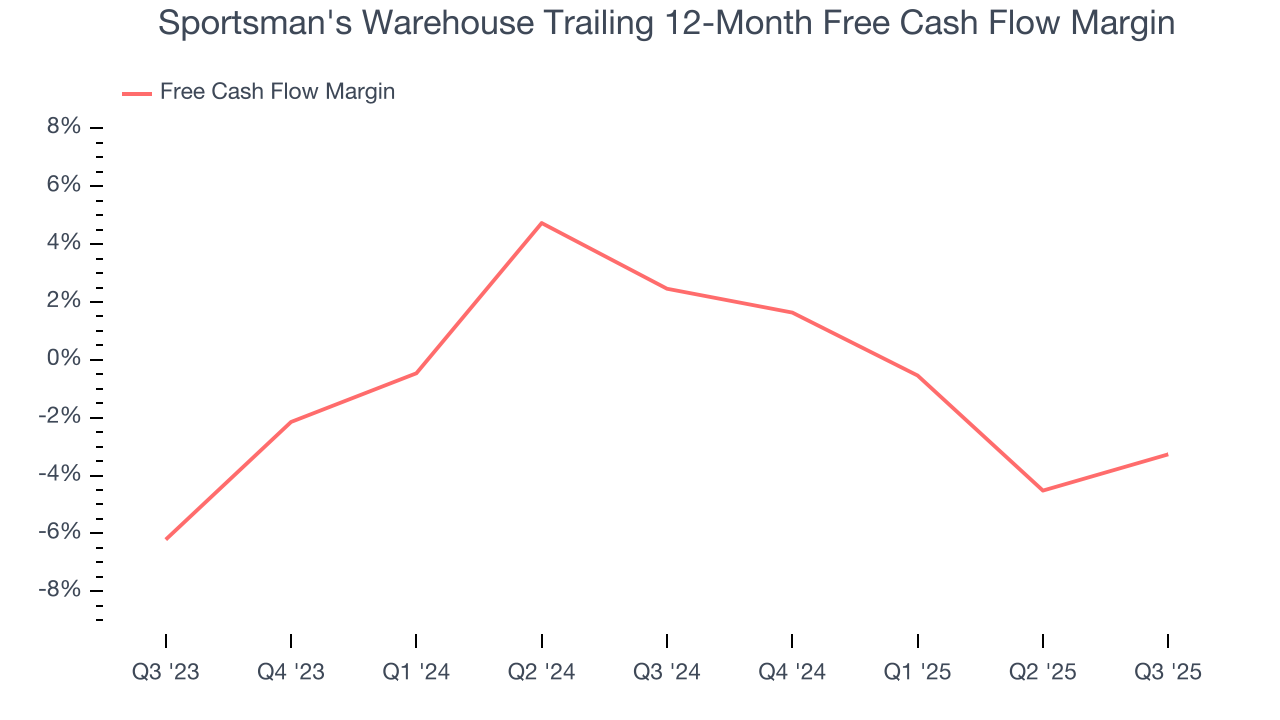

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Sportsman's Warehouse broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Sportsman's Warehouse’s margin dropped by 5.7 percentage points over the last year. This decrease warrants extra caution because Sportsman's Warehouse failed to grow its same-store sales. Its cash profitability could decay further if it tries to reignite growth by opening new stores.

Sportsman's Warehouse’s free cash flow clocked in at $8.74 million in Q3, equivalent to a 2.6% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Sportsman's Warehouse historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.3%, lower than the typical cost of capital (how much it costs to raise money) for consumer retail companies.

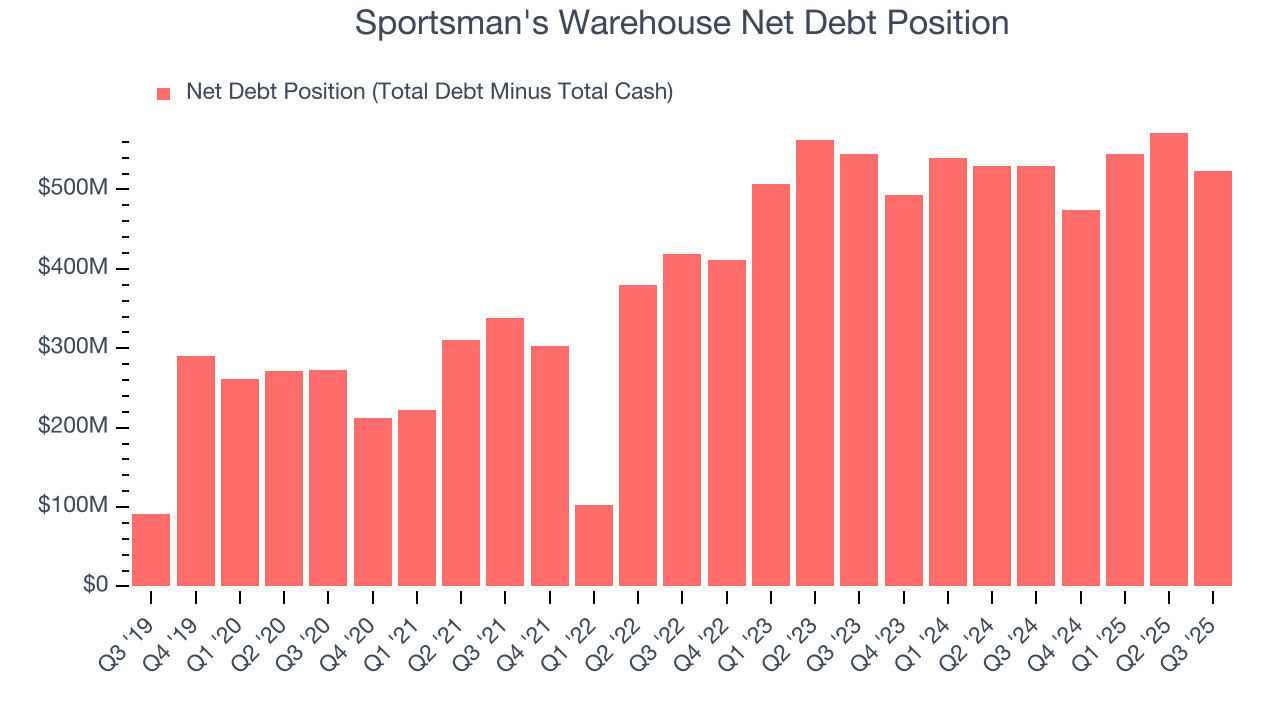

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Sportsman's Warehouse burned through $39.67 million of cash over the last year, and its $525.1 million of debt exceeds the $2.25 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Sportsman's Warehouse’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Sportsman's Warehouse until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

13. Key Takeaways from Sportsman's Warehouse’s Q3 Results

It was encouraging to see Sportsman's Warehouse beat analysts’ gross margin expectations this quarter. We were also glad its EPS was in line with Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, this was a weaker quarter. The stock traded down 6.8% to $2.34 immediately after reporting.

14. Is Now The Time To Buy Sportsman's Warehouse?

Updated: March 20, 2026 at 10:50 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Sportsman's Warehouse, you should also grasp the company’s longer-term business quality and valuation.

We cheer for all companies serving everyday consumers, but in the case of Sportsman's Warehouse, we’ll be cheering from the sidelines. For starters, its revenue has declined over the last three years. On top of that, Sportsman's Warehouse’s declining EPS over the last three years makes it a less attractive asset to the public markets, and its projected EPS for the next year is lacking.

Sportsman's Warehouse’s EV-to-EBITDA ratio based on the next 12 months is 21x. This multiple tells us a lot of good news is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $3.19 on the company (compared to the current share price of $1.35).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.