ProFrac (ACDC)

We’re wary of ProFrac. It not only barely produces cash but also has been less efficient lately, as seen by its falling margins.― StockStory Analyst Team

1. News

2. Summary

Why We Think ProFrac Will Underperform

Operating one of the largest electric-powered fracturing fleets in North America, ProFrac (NASDAQ:ACDC) provides hydraulic fracturing services that help oil and gas companies extract hydrocarbons from underground shale formations.

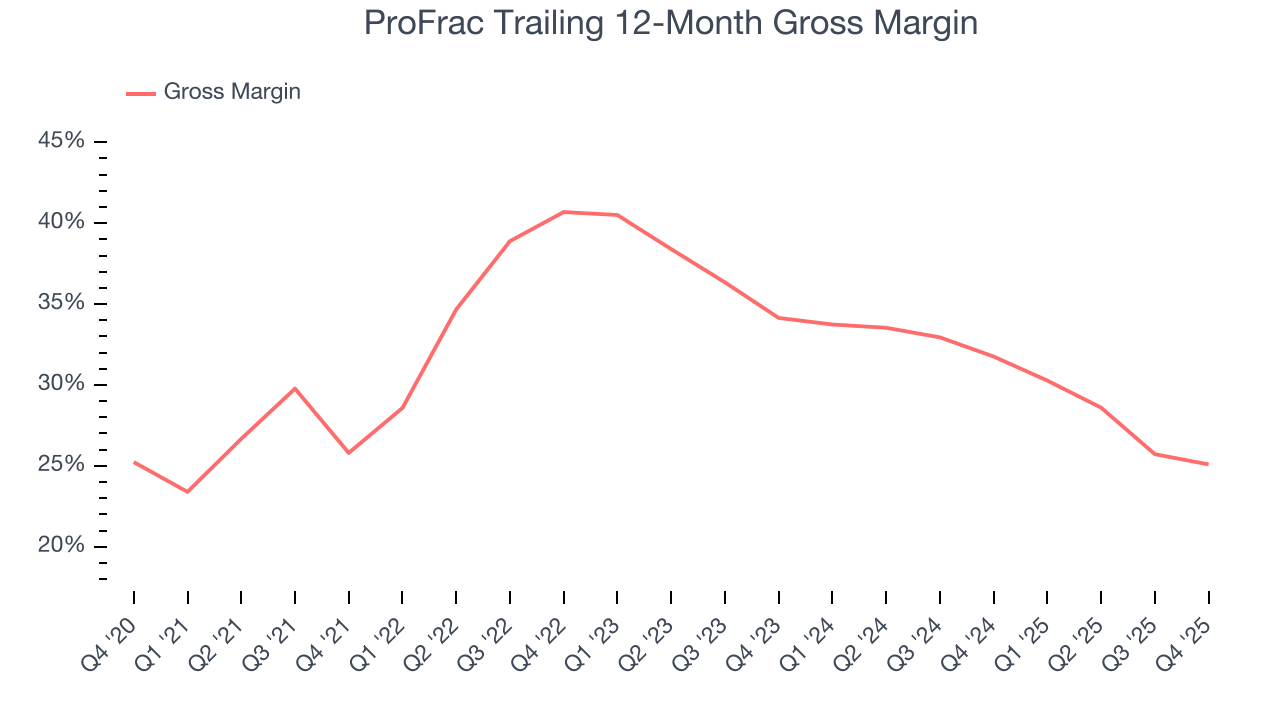

- High extraction costs and unfavorable asset economics are reflected in its low gross margin of 32.8%

- Subpar EBITDA margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- The good news is that its impressive 19.1% annual revenue growth over the last five years indicates it’s winning market share this cycle

ProFrac’s quality is insufficient. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than ProFrac

At $6.70 per share, ProFrac trades at 9.5x forward EV-to-EBITDA. While valuation is appropriate for the quality you get, we’re still not buyers.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. ProFrac (ACDC) Research Report: Q4 CY2025 Update

Hydraulic fracturing services provider ProFrac (NASDAQ:ACDC) announced better-than-expected revenue in Q4 CY2025, but sales fell by 4% year on year to $436.5 million. Its non-GAAP loss of $0.45 per share was 4.2% below analysts’ consensus estimates.

ProFrac (ACDC) Q4 CY2025 Highlights:

- Revenue: $436.5 million vs analyst estimates of $398.9 million (4% year-on-year decline, 9.4% beat)

- Adjusted EPS: -$0.45 vs analyst expectations of -$0.44 (4.2% miss)

- Adjusted EBITDA: $61.1 million vs analyst estimates of $39.21 million (14% margin, 55.8% beat)

- Operating Margin: -24.1%, down from -10.3% in the same quarter last year

- Free Cash Flow Margin: 3%, similar to the same quarter last year

- Market Capitalization: $1.15 billion

Company Overview

Operating one of the largest electric-powered fracturing fleets in North America, ProFrac (NASDAQ:ACDC) provides hydraulic fracturing services that help oil and gas companies extract hydrocarbons from underground shale formations.

The company operates across three interconnected business segments. Its Stimulation Services segment runs hydraulic fracturing fleets that pump water, sand, and chemicals at high pressure into wells to fracture rock and release trapped oil and natural gas. As of late 2024, ProFrac operated 28 active fleets across major US oil and gas regions including the Permian Basin, Eagle Ford Shale, and Haynesville. These fleets are a mix of traditional diesel-powered equipment, dual-fuel systems, and electric-powered fleets that use natural gas generated on-site to reduce emissions and fuel costs. A typical job might involve an exploration and production company hiring ProFrac to complete a newly drilled horizontal well in West Texas, where ProFrac's equipment creates fractures thousands of feet underground to unlock oil reserves.

The Proppant Production segment mines frac sand—the material pumped into wells to prop open the fractures created during hydraulic fracturing. With eight sand mines located near major drilling areas in Texas, Louisiana, and Arkansas, ProFrac produces approximately 21.5 million tons of sand annually. This in-basin production reduces transportation costs and delivery times for customers compared to sourcing sand from distant locations.

The Manufacturing segment designs and builds the specialized equipment used in hydraulic fracturing operations. At company-owned facilities, engineers assemble new fleets, refurbish existing equipment, rebuild engines and transmissions, and manufacture critical components like pumps and fluid ends. This vertical integration allows ProFrac to control costs, customize equipment specifications, and maintain standardized fleets across regions. The company also operates Livewire Power, which provides off-grid natural gas power generation for oilfield and industrial customers requiring distributed electricity solutions.

4. Oilfield Services

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

ProFrac's hydraulic fracturing services compete with Halliburton (NYSE:HAL), Liberty Energy (NYSE:LBRT), ProPetro (NYSE:PUMP), and Patterson-UTI (NASDAQ:PTEN). Its frac sand production competes with Atlas Energy Solutions (NYSE:AESI) and U.S. Silica (NYSE:SLCA).

5. Revenue Scale

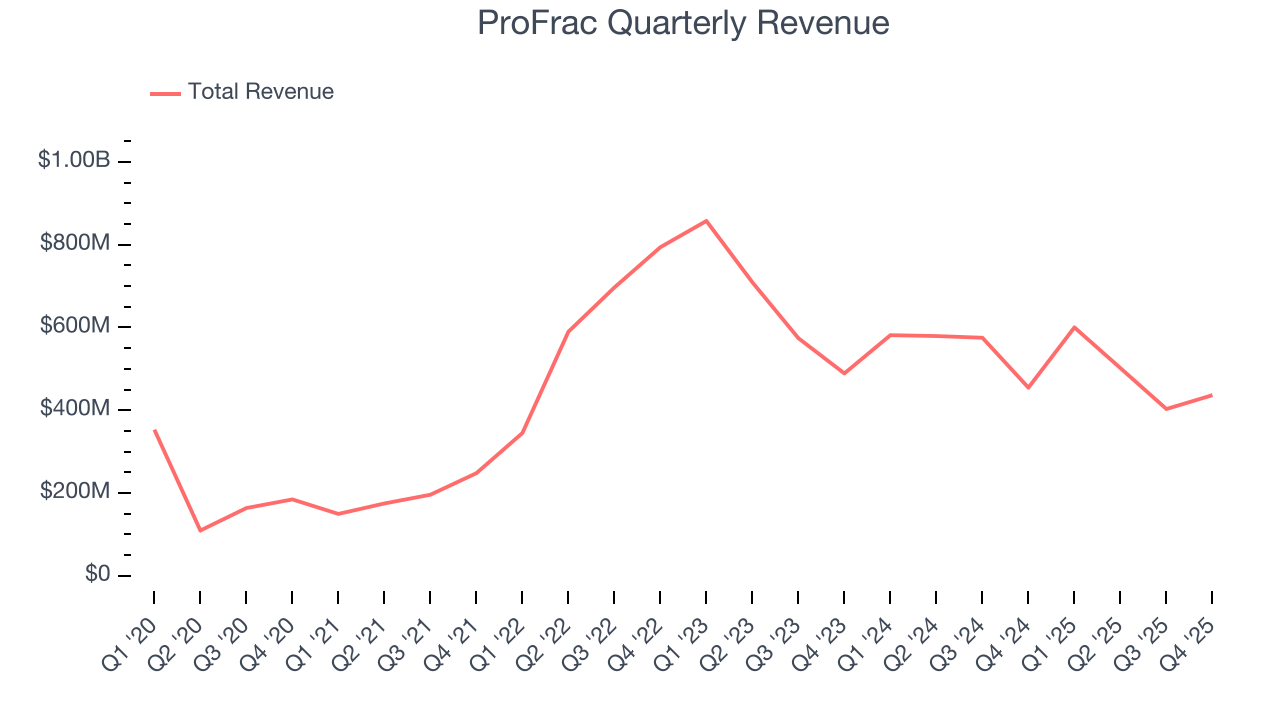

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program. ProFrac’s $1.94 billion of revenue in the last year is pretty small for the industry, suggesting the company is subscale business in an industry where scale matters.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, ProFrac grew its sales at an excellent 19.1% compounded annual growth rate. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

This quarter, ProFrac’s revenue fell by 4% year on year to $436.5 million but beat Wall Street’s estimates by 9.4%.

7. Gross Margin

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

ProFrac, which averaged 32.8% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

In Q4, ProFrac produced a 22.9% gross profit margin, down 2.8 percentage points year on year.

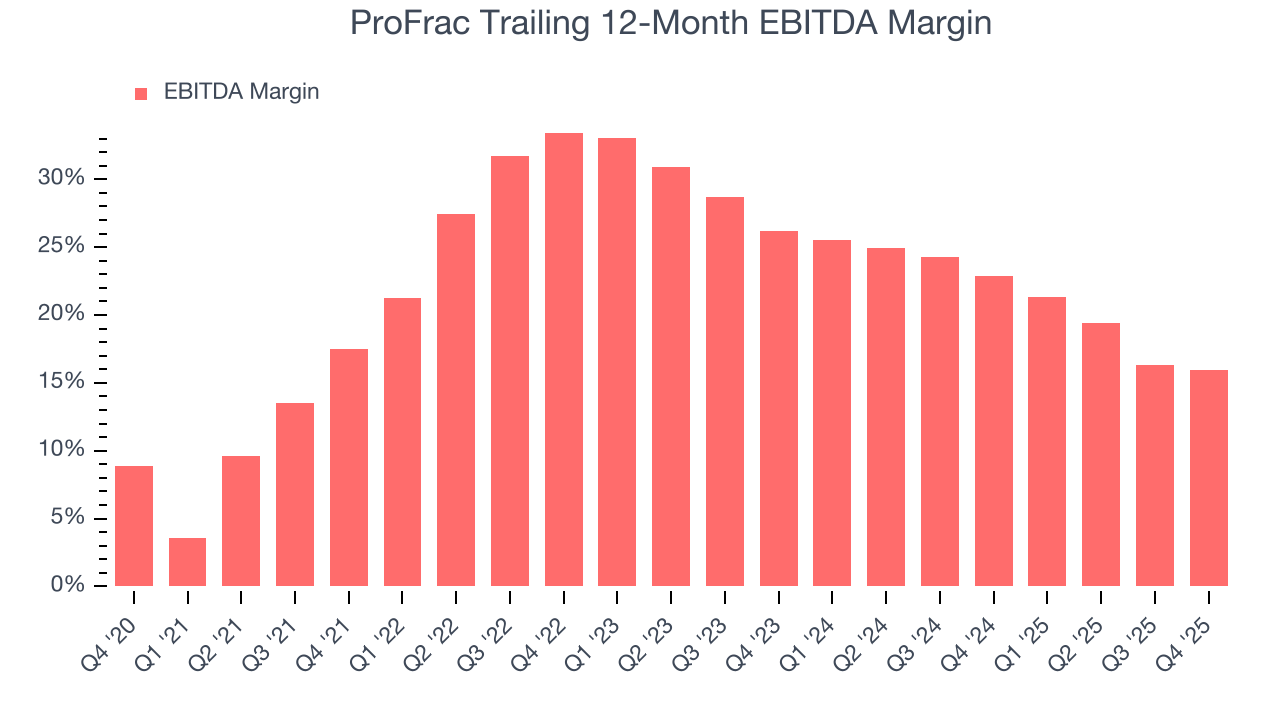

8. Adjusted EBITDA Margin

ProFrac was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 24.6% was weak for an upstream and integrated energy business.

Analyzing the trend in its profitability, ProFrac’s EBITDA margin decreased by 1.6 percentage points over the last year. ProFrac’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

In Q4, ProFrac generated an EBITDA margin profit margin of 14%, down 1.6 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable. This adjusted EBITDA beat Wall Street’s estimates by 55.8%.

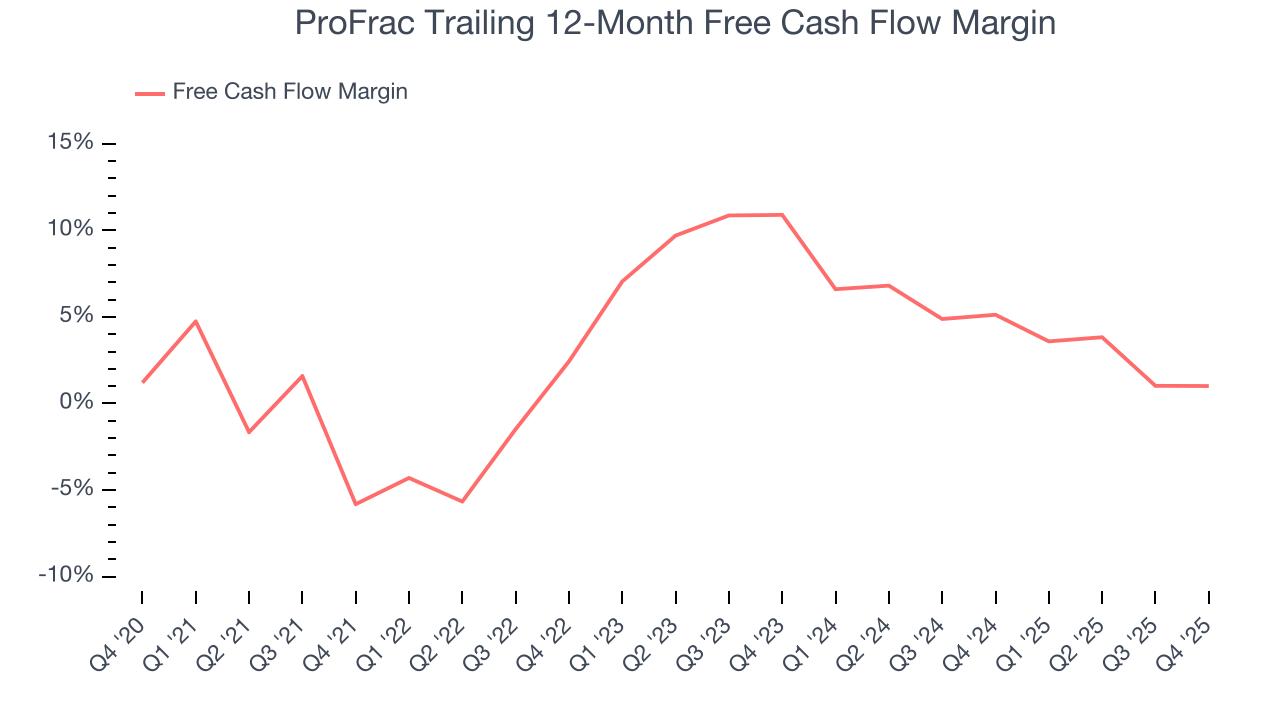

9. Cash Is King

As mentioned above, adjusted EBITDA ignores capital structure and drilling expenditure decisions. These are two huge aspects of an Energy producer, so in order to understand a comprehensive picture of business quality, an investor needs to account for these. Said differently, adjusted EBITDA margins could be solid but free cash flow is abysmal because decline rates of the asset are extreme and the drilling is expensive. Free cash flow tells you about not only the economics of the production that has happened but how much it costs to stay in business as well (further drilling or extraction).

ProFrac has shown weak cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 4.3%, below what we’d expect for an upstream and integrated energy business.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

ProFrac’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 12.7 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of ProFrac? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

ProFrac’s free cash flow clocked in at $12.9 million in Q4, equivalent to a 3% margin. This cash profitability was in line with the comparable period last year but below its five-year average. In a silo, this isn’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

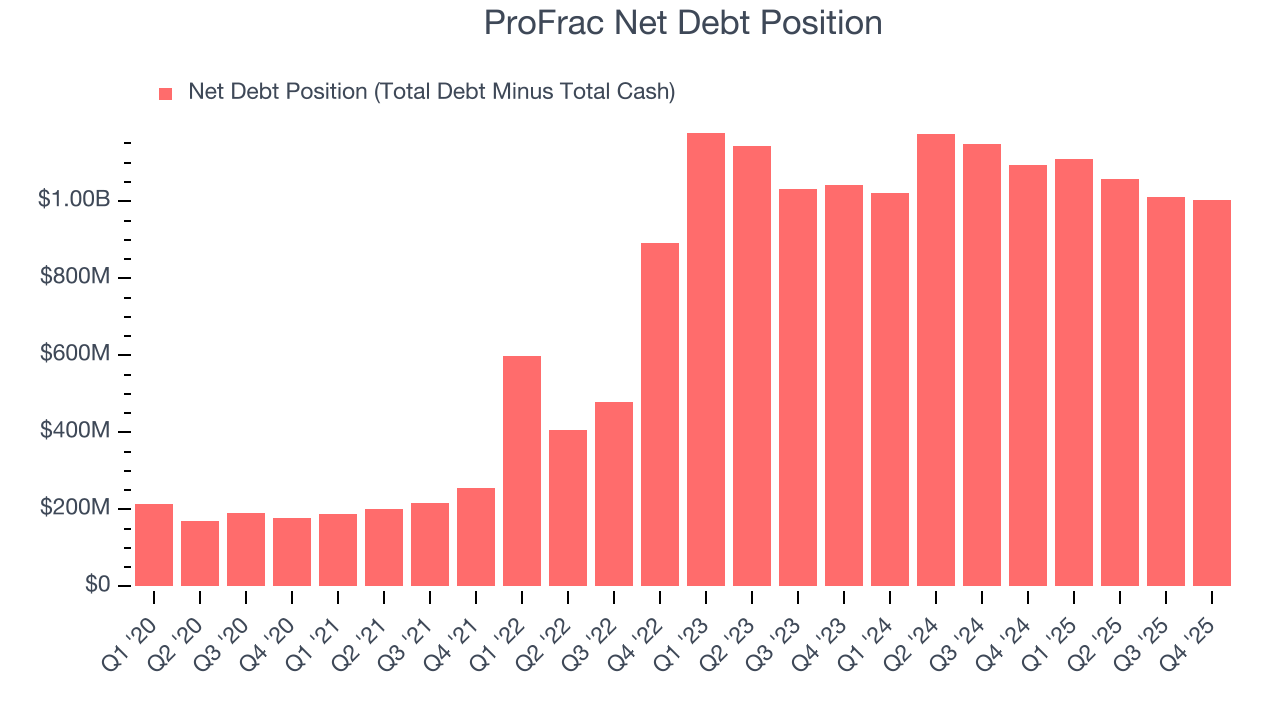

10. Balance Sheet Assessment

ProFrac reported $22.9 million of cash and $1.03 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $310.1 million of EBITDA over the last 12 months, we view ProFrac’s 3.2× net-debt-to-EBITDA ratio as safe. We also see its $138.8 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from ProFrac’s Q4 Results

We were impressed by how significantly ProFrac blew past analysts’ EBITDA expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its EPS missed. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $6.29 immediately after reporting.

12. Is Now The Time To Buy ProFrac?

Updated: March 18, 2026 at 1:04 AM EDT

Before making an investment decision, investors should account for ProFrac’s business fundamentals and valuation in addition to what happened in the latest quarter.

ProFrac’s business quality ultimately falls short of our standards. Although its revenue growth over the last five years was impressive for the sector, it’s expected to deteriorate over the next 12 months and its gross margins show its business model is much less lucrative than other companies. On top of that, the company’s EBITDA margins reveal bottom-tier profitability compared to other energy upstream and integrated energy companies.

ProFrac’s EV-to-EBITDA ratio based on the next 12 months is 9.5x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $3.80 on the company (compared to the current share price of $6.70).