TETRA Technologies (TTI)

TETRA Technologies keeps us up at night. Its negative returns on capital show it destroyed shareholder value by losing money.― StockStory Analyst Team

1. News

2. Summary

Why We Think TETRA Technologies Will Underperform

Operating across six continents with approximately 40,000 acres of mineral-rich brine leases in Arkansas, TETRA Technologies (NYSE:TTI) provides well completion fluids and water management services to oil and gas operators.

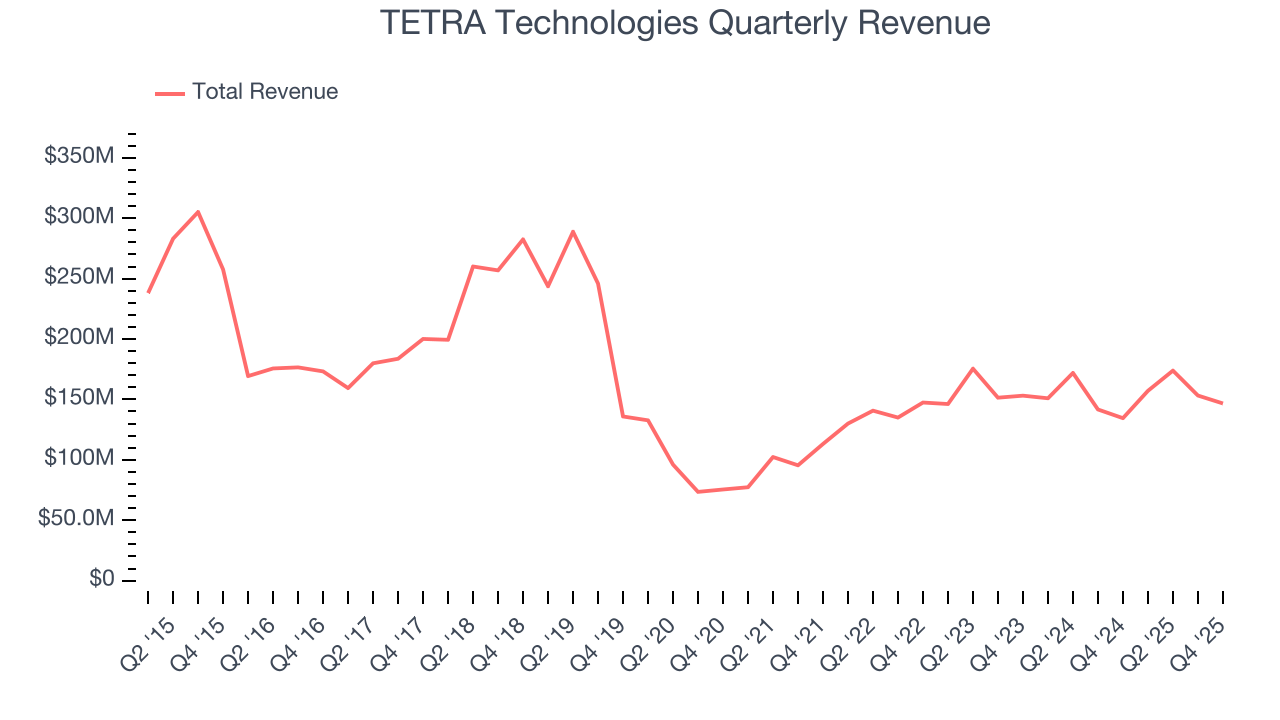

- Sales tumbled by 5.3% annually over the last ten years, showing market trends are working against its favor during this cycle

- Smaller revenue base of $630.9 million means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

- Poor expense management has led to an EBITDA margin that is below the industry average

TETRA Technologies doesn’t measure up to our expectations. There are superior opportunities elsewhere.

Why There Are Better Opportunities Than TETRA Technologies

TETRA Technologies is trading at $8.22 per share, or 36.6x forward P/E. Not only does TETRA Technologies trade at a premium to companies in the energy upstream and integrated energy space, but this multiple is also high for its top-line growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. TETRA Technologies (TTI) Research Report: Q4 CY2025 Update

Oilfield services company TETRA Technologies (NYSE:TTI) announced better-than-expected revenue in Q4 CY2025, with sales up 9.1% year on year to $146.7 million. Its non-GAAP profit of $0.02 per share was in line with analysts’ consensus estimates.

TETRA Technologies (TTI) Q4 CY2025 Highlights:

- Revenue: $146.7 million vs analyst estimates of $141.2 million (9.1% year-on-year growth, 3.9% beat)

- Adjusted EPS: $0.02 vs analyst estimates of $0.02 (in line)

- Adjusted EBITDA: $20.4 million vs analyst estimates of $18.28 million (13.9% margin, 11.6% beat)

- Operating Margin: 1.7%, down from 6% in the same quarter last year

- Free Cash Flow was $5.05 million, up from -$9.74 million in the same quarter last year

- Market Capitalization: $1.1 billion

Company Overview

Operating across six continents with approximately 40,000 acres of mineral-rich brine leases in Arkansas, TETRA Technologies (NYSE:TTI) provides well completion fluids and water management services to oil and gas operators.

The business is organized into two main divisions. The Completion Fluids & Products Division manufactures clear brine fluids (CBFs), which are dense salt solutions used to control pressure during oil and gas well drilling, completion, and workover operations. When an operator drills into a reservoir containing high-pressure oil or gas, they need fluids of specific densities to prevent uncontrolled blowouts while avoiding damage to the formation. TETRA produces various CBFs including calcium chloride, calcium bromide, zinc bromide, and sodium bromide solutions that can be blended to achieve the precise density and chemical properties required. The division also offers buy-back programs where customers can sell used fluids back to TETRA for reconditioning and recycling, reducing their net cost and disposal burden. Beyond energy applications, the division sells calcium chloride to water treatment, food processing, road maintenance, ice melt, and agricultural markets.

The Water & Flowback Services Division manages the large volumes of water involved in hydraulic fracturing operations. This includes sourcing, treating, recycling, storing, and transferring water to and from well sites, as well as handling the flowback fluids that return to the surface after fracturing. For instance, an operator completing a well in the Permian Basin might use TETRA's services to recycle produced water for reuse in subsequent fracking operations, reducing freshwater consumption. The division also provides specialized equipment for production testing, which helps operators evaluate reservoir performance and optimize production rates.

TETRA is expanding into low-carbon energy markets by leveraging its chemistry expertise and Arkansas brine resources. The company produces ultra-pure zinc bromide (TETRA PureFlow) as an electrolyte for zinc-bromine flow batteries used in long-duration energy storage systems. It has also conducted resource assessments for lithium extraction from its Arkansas leases and recently launched a desalination technology for treating produced water for beneficial reuse.

4. Oilfield Services

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

TETRA Technologies faces competition from Select Energy Services (NYSE:WTTR) in water management and from Occidental Chemical Corporation and various regional service providers across its completion fluids business.

5. Revenue Scale

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program. TETRA Technologies’s $630.9 million of revenue in the last year is pretty small for the industry, suggesting the type of diversification that reduces operational risk.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Over the last five years, TETRA Technologies grew its sales at a decent 10.8% compounded annual growth rate. Its growth was slightly above the average energy upstream and integrated energy company and shows its offerings resonate with customers.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. TETRA Technologies’s ten year performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 5.3% over the last ten years.

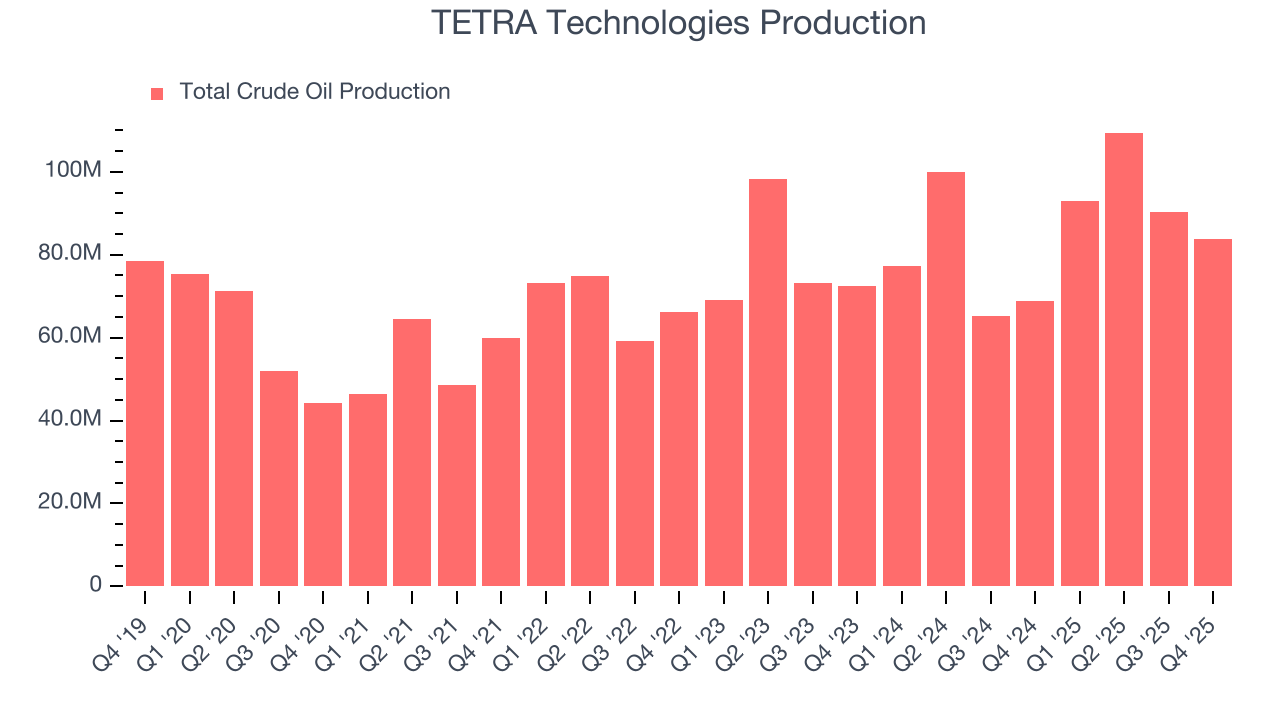

While looking at revenue is important, it can also introduce noise around commodity prices and M&A. Analyzing production, on the other hand, highlights what is happening inside the asset base and whether the economic footprint of a company is expanding. Over the last two years, TETRA Technologies’s total oil volume per day - Upstream averaged 10.9% year-on-year growth while natural gas volume per day - Upstream averaged 9.7% year-on-year growth, which was good.

This quarter, TETRA Technologies reported year-on-year revenue growth of 9.1%, and its $146.7 million of revenue exceeded Wall Street’s estimates by 3.9%. This quarter, TETRA Technologies reported robust year-on-year production growth of 21.6%, and its 83,727 Mboe (thousand barrels of oil equivalent) of production topped Wall Street estimates by 3.4%.

7. Gross Margin

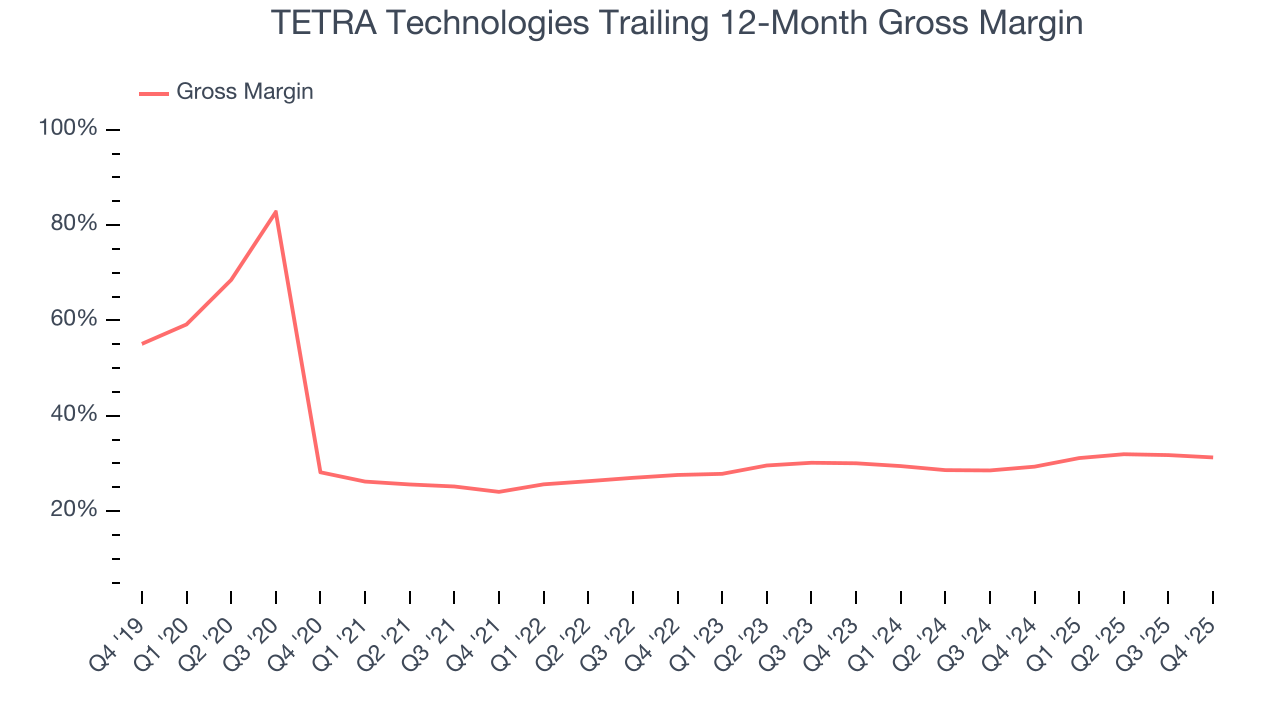

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

TETRA Technologies, which averaged 28.8% gross margin over the last five years, exhibits bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

This quarter, TETRA Technologies’s gross profit margin was 28.1% , marking a 2 percentage point decrease from 30.1% in the same quarter last year. Note that energy margins can be volatile due to commodity price changes.

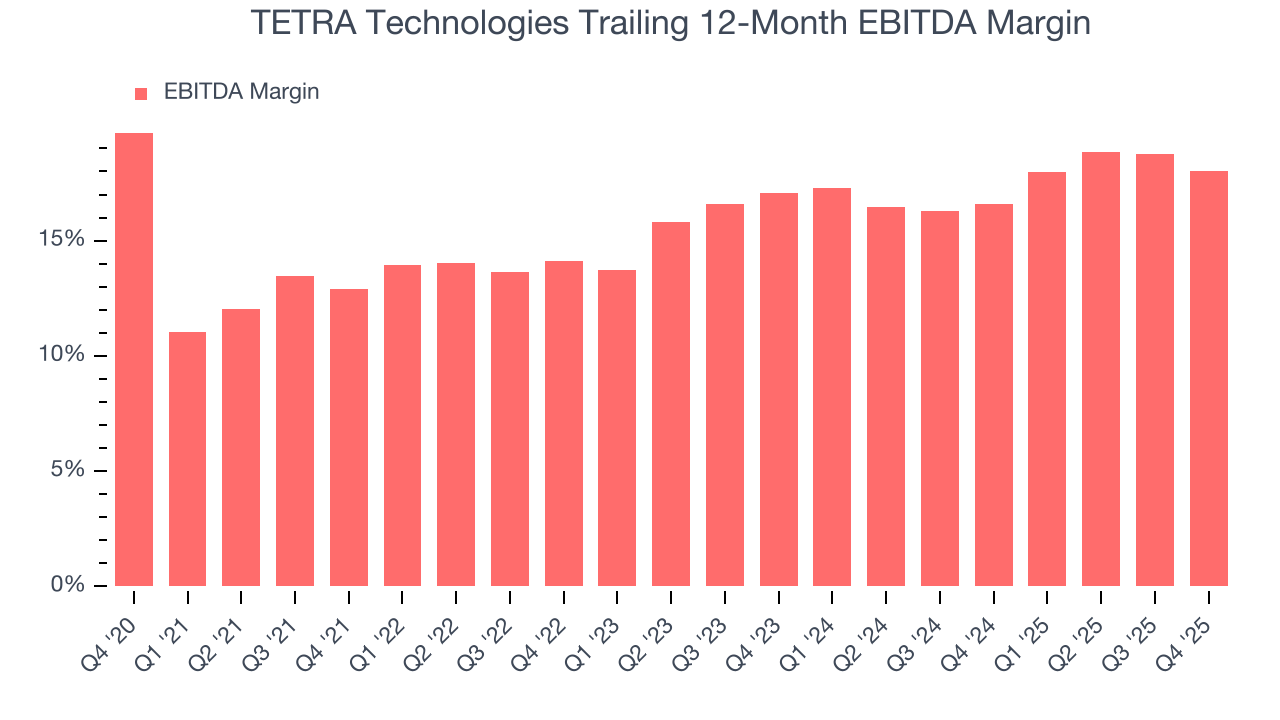

8. Adjusted EBITDA Margin

TETRA Technologies was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 16% was among the worst in the energy upstream and integrated energy sector.

On the plus side, TETRA Technologies’s EBITDA margin rose by 5.1 percentage points over the last year.

This quarter, TETRA Technologies generated an EBITDA margin profit margin of 13.9%, down 3.1 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA beat Wall Street’s estimates by 11.6%.

9. Cash Is King

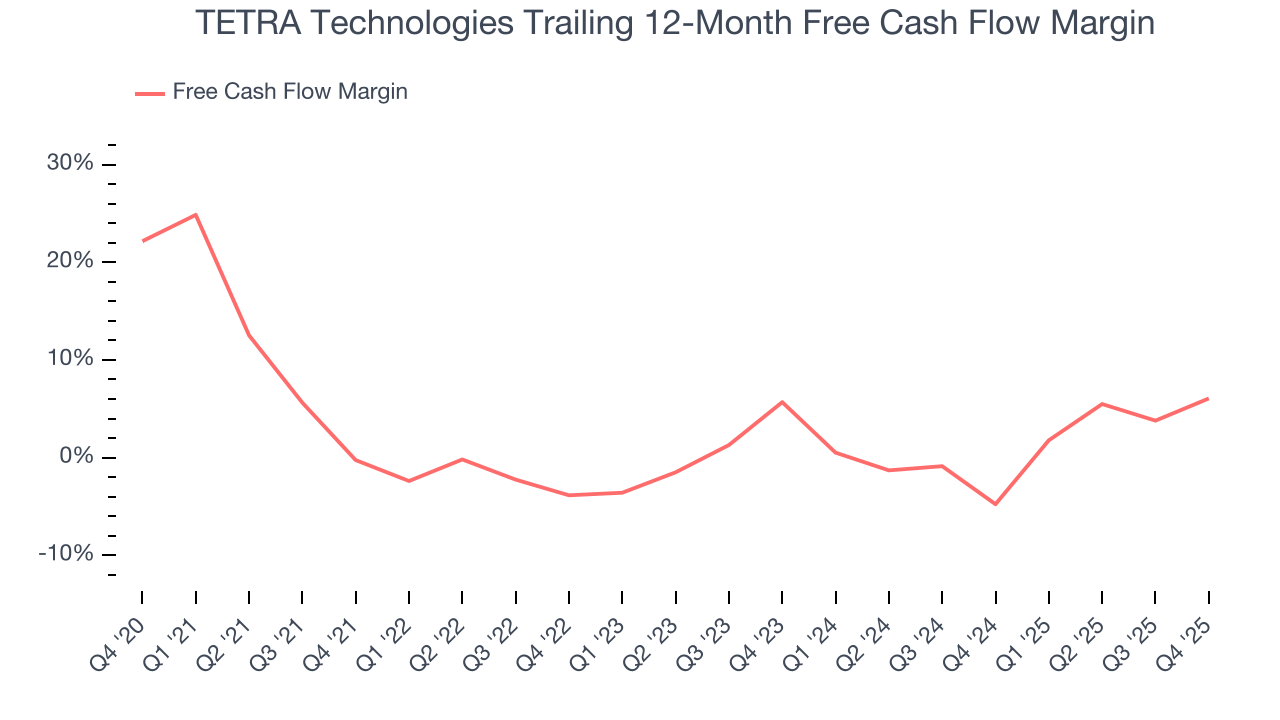

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

TETRA Technologies broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

TETRA Technologies’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 69.1 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of TETRA Technologies? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

TETRA Technologies’s free cash flow clocked in at $5.05 million in Q4, equivalent to a 3.4% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

10. Return on Invested Capital (ROIC)

Free cash flow tells investors how much money an Energy producer made, and ROIC takes this one step further by telling investors how well and effectively the business made it. ROIC illustrates how much operating profit a producer generated relative to the money it has raised (debt and equity).

We at StockStory like to look at ROIC over a ten-year period because energy investment cycles can involve up to five years of ramping production and another five years of harvesting. A decade view captures buying, extracting, and monetizing rather than just part of that picture. TETRA Technologies’s ten-year average ROIC was negative 4.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the energy upstream and integrated energy sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. TETRA Technologies’s ROIC has increased significantly over the last few years. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

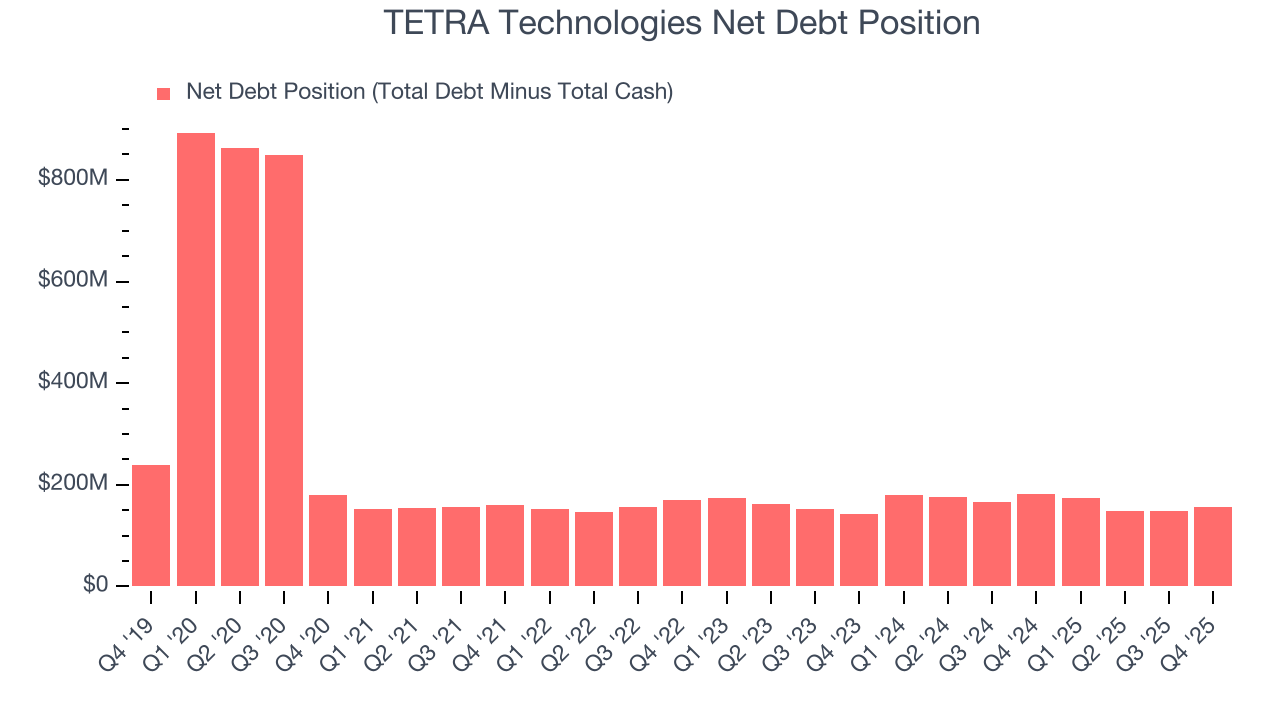

TETRA Technologies reported $72.63 million of cash and $229.7 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $113.6 million of EBITDA over the last 12 months, we view TETRA Technologies’s 1.4× net-debt-to-EBITDA ratio as safe. We also see its $17.33 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from TETRA Technologies’s Q4 Results

We enjoyed seeing TETRA Technologies beat analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. Investors were likely hoping for more, and shares traded down 1.4% to $8.05 immediately after reporting.

13. Is Now The Time To Buy TETRA Technologies?

Updated: March 20, 2026 at 1:09 AM EDT

Before deciding whether to buy TETRA Technologies or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

TETRA Technologies doesn’t pass our quality test. Although its revenue growth over the last five years was average for the sector, it’s expected to deteriorate over the next 12 months and its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s rising returns show management's prior bets are at least better than before, the downside is its free cash flow volatility compared to commodity price volatility is bottom-tier in the sector, leading to highly volatile free cash flow.

TETRA Technologies’s P/E ratio based on the next 12 months is 36.6x. This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $12.75 on the company (compared to the current share price of $8.22).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.