Bristow Group (VTOL)

Bristow Group doesn’t excite us. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Bristow Group Will Underperform

Operating what's essentially an airborne taxi service for some of the world's most remote workplaces, Bristow Group (NYSE:VTOL) operates helicopters that transport workers to offshore oil and gas platforms and conduct search and rescue operations.

- Subpar EBITDA margin constrains its ability to invest in process improvements or effectively respond to new competitive threats

- Low returns on capital reflect management’s struggle to allocate funds effectively

- A silver lining is that its EBITDA margin expanded by 12.2 percentage points over the last five years as it scaled and became more efficient

Bristow Group’s quality doesn’t meet our expectations. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Bristow Group

At $42.70 per share, Bristow Group trades at 7.9x forward P/E. Bristow Group’s valuation may seem like a great deal, but we think there are valid reasons why it’s so cheap.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Bristow Group (VTOL) Research Report: Q4 CY2025 Update

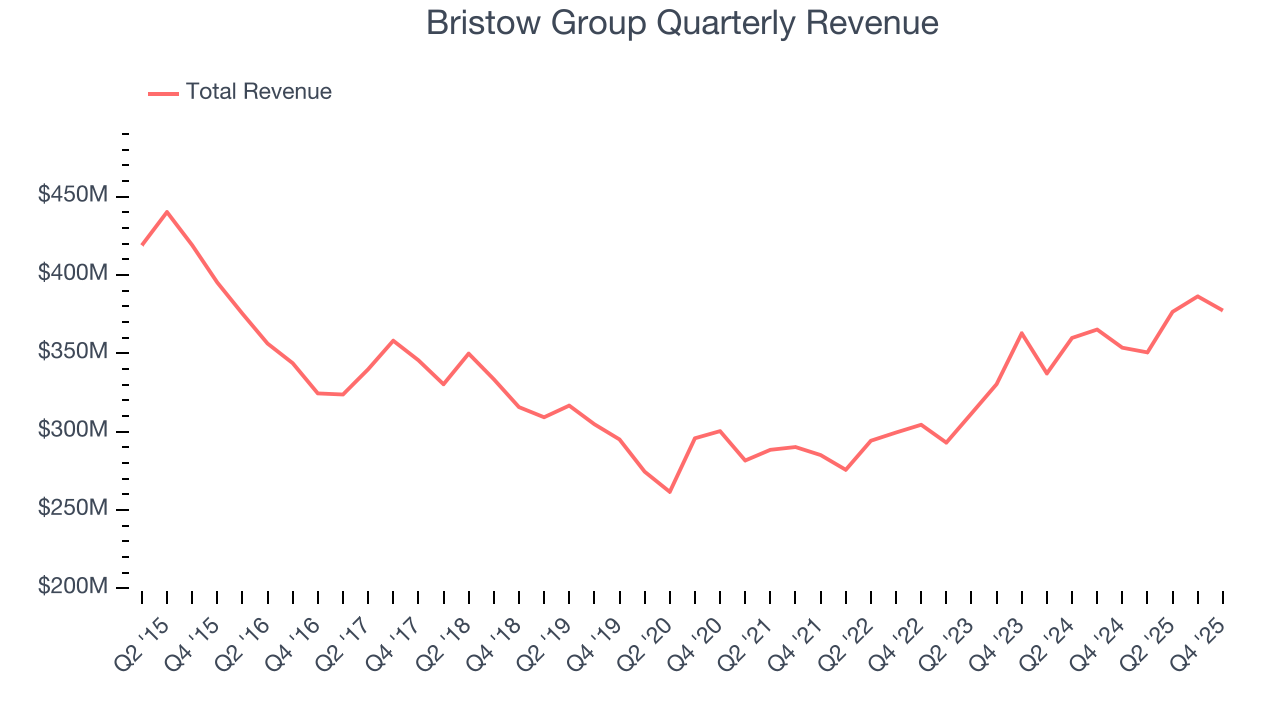

Helicopter services provider Bristow Group (NYSE:VTOL) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 6.7% year on year to $377.3 million. Its GAAP profit of $0.61 per share was 14.7% below analysts’ consensus estimates.

Bristow Group (VTOL) Q4 CY2025 Highlights:

- Revenue: $377.3 million vs analyst estimates of $380.3 million (6.7% year-on-year growth, 0.8% miss)

- EPS (GAAP): $0.61 vs analyst expectations of $0.72 (14.7% miss)

- Adjusted EBITDA: $50.51 million vs analyst estimates of $63.97 million (13.4% margin, 21% miss)

- Operating Margin: 11.4%, down from 13.5% in the same quarter last year

- Free Cash Flow Margin: 18.8%, up from 14.4% in the same quarter last year

- Market Capitalization: $1.3 billion

Company Overview

Operating what's essentially an airborne taxi service for some of the world's most remote workplaces, Bristow Group (NYSE:VTOL) operates helicopters that transport workers to offshore oil and gas platforms and conduct search and rescue operations.

The company's business splits into three main areas. Offshore energy services, representing about two-thirds of revenues, involves flying workers between shore bases and offshore installations—oil platforms, drilling rigs, and production facilities—often located dozens or hundreds of miles from land. For example, an oil company operating a deepwater platform in the U.S. Gulf of Mexico might contract Bristow to shuttle crews on and off the platform during shift changes, using heavy twin-engine helicopters capable of carrying 16-19 passengers across distances exceeding 500 miles. The company operates across major offshore energy regions including the North Sea (both UK and Norway), U.S. Gulf of Mexico, Brazil's deepwater fields, Nigeria, Trinidad, and Suriname.

Government services, accounting for roughly a quarter of revenues, provides emergency response capabilities to public agencies. The company operates the UK's nationwide search and rescue helicopter service under a 10-year contract with the Department for Transport, maintaining bases across Britain ready to respond to maritime emergencies, mountain rescues, and medical evacuations. Similar contracts exist in Ireland, the Netherlands, and the Dutch Caribbean, offering governments specialized aviation capabilities without maintaining their own fleets.

The remaining business includes Airnorth, a regional airline in northern Australia serving mining and energy customers with fixed-wing aircraft, plus dry-leasing arrangements where Bristow rents helicopters to operators in markets like India, Chile, and Mexico. The company manages its fleet—consisting of heavy, medium, and light helicopters—based on customer requirements, with deeper offshore operations demanding the more capable heavy aircraft. Bristow generates revenue primarily through master service agreements that combine fixed monthly fees with additional charges based on flight hours, though contract structures vary from long-term government deals to day-to-day charter arrangements.

4. Oilfield Services

Oilfield services companies provide equipment, technology, and services enabling exploration and production activities, including drilling, completion, well intervention, and reservoir evaluation. Their fortunes closely track upstream capital spending cycles. Tailwinds include increased drilling activity during favorable commodity environments, demand for efficiency-enhancing technologies, and growing offshore and unconventional resource development. Headwinds include significant revenue volatility tied to oil and gas price swings and producer spending discipline. Intense competition pressures pricing and margins, while the energy transition may structurally reduce long-term demand. Workforce availability and technological disruption require continuous adaptation.

Bristow Group's main competitors include CHC Group, NHV Group, Omni Helicopters International, and PHI, all privately held helicopter service providers operating in offshore energy and related markets.

5. Revenue Scale

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. Bristow Group’s $1.49 billion of revenue in the last year is pretty small for the industry, suggesting the type of diversification that reduces operational risk. is a small company in an industry where scale matters.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Regrettably, Bristow Group’s sales grew at a sluggish 5.7% compounded annual growth rate over the last five years. This was below our standard for the energy upstream and integrated energy sector and is a tough starting point for our analysis.

Energy cycles can be long enough that a single five-year period can still reflect one price environment, which is why an additional, decade-long view can help capture through-cycle performance. Bristow Group’s performance shows it grew in the past five-year but relinquished its gains over the last ten years, as its revenue fell by 1.1% annually.

This quarter, Bristow Group’s revenue grew by 6.7% year on year to $377.3 million, missing Wall Street’s estimates.

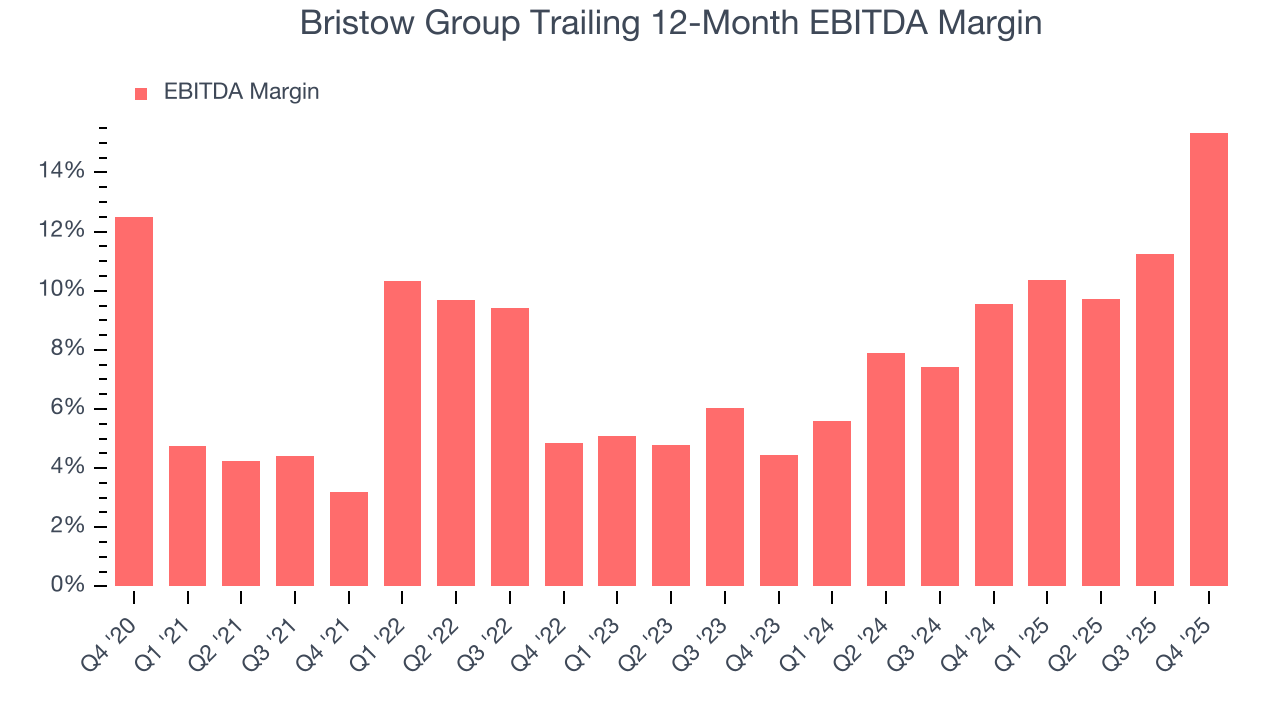

7. Adjusted EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Bristow Group was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 7.9% was among the worst in the energy upstream and integrated energy sector.

On the plus side, Bristow Group’s EBITDA margin rose by 12.2 percentage points over the last year.

In Q4, Bristow Group generated an EBITDA margin profit margin of 13.4%, up 17.2 percentage points year on year. This increase was a welcome development and shows it was more efficient. This adjusted EBITDA fell short of Wall Street’s estimates.

8. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Bristow Group has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 8.4% over the last five years, slightly better than the broader energy upstream and integrated energy sector.

The level of free cash flow is important, but its durability across cycles is just as critical. Consistent margins are far more valuable than volatile swings driven by commodity prices.

Bristow Group’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 6.9 (lower is better), indicating great insulation from commodity swings. indicating that its cash generation is relatively insulated from swings in commodity prices compared with most peers. This resilience supports access to capital in downturns and positions the company to act as a consolidator when distressed assets come to market at attractive prices.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Bristow Group? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Bristow Group’s free cash flow clocked in at $70.87 million in Q4, equivalent to a 18.8% margin. This result was good as its margin was 4.3 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends trump fluctuations.

9. Return on Invested Capital (ROIC)

Free cash flow shows how much money a producer generated, while ROIC shows how efficiently that money was earned. ROIC measures the operating profit produced for each dollar of capital invested, whether from debt or equity. Cash generation measures quantity while ROIC measures the quality of value creation.

We at StockStory like to look at ROIC over a ten-year period because energy investment cycles can involve up to five years of ramping production and another five years of harvesting. A decade view captures buying, extracting, and monetizing rather than just part of that picture. Bristow Group historically did a mediocre job investing in profitable growth initiatives. Its ten-year average ROIC was 2.7%, lower than the typical cost of capital (how much it costs to raise money) for energy upstream and integrated energy companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Bristow Group’s ROIC has increased. This is a good sign, and we hope the company can continue improving.

10. Balance Sheet Assessment

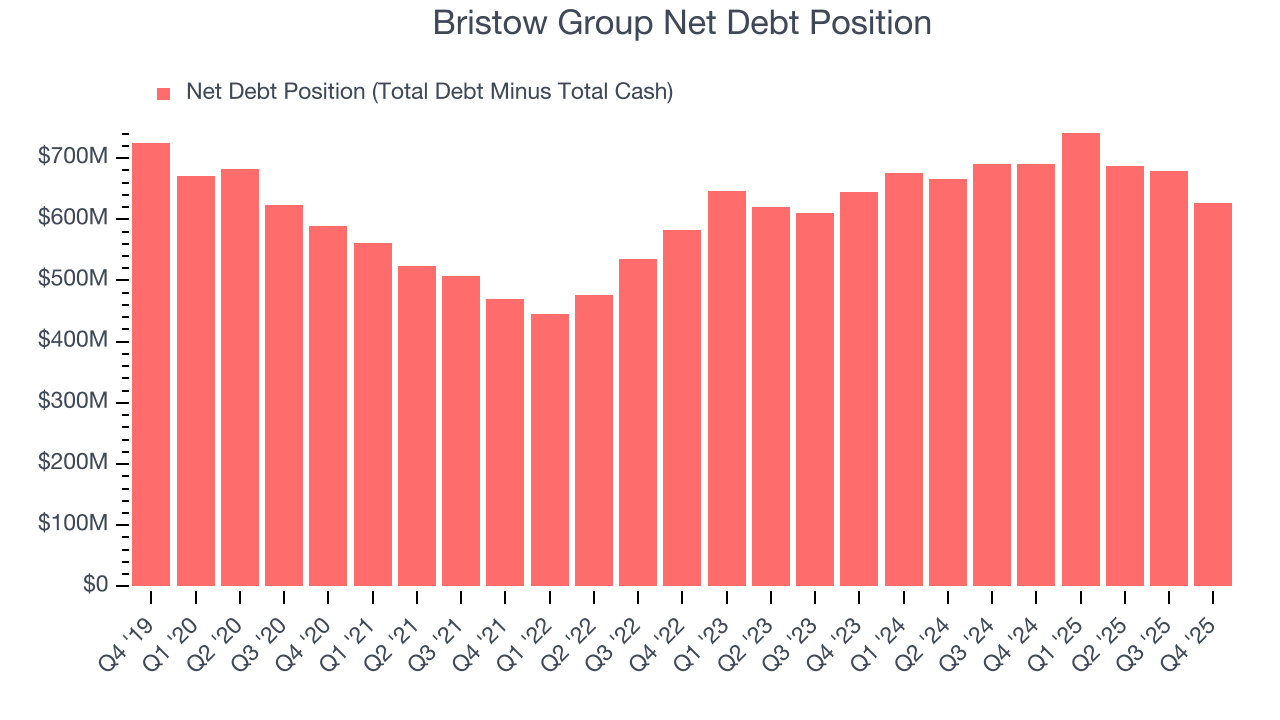

Bristow Group reported $286.2 million of cash and $913 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $228.8 million of EBITDA over the last 12 months, we view Bristow Group’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $30.56 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Bristow Group’s Q4 Results

We struggled to find many positives in these results. Its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $45.01 immediately following the results.

12. Is Now The Time To Buy Bristow Group?

Updated: March 16, 2026 at 1:12 AM EDT

Before deciding whether to buy Bristow Group or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Bristow Group isn’t a terrible business, but it isn’t one of our picks. First off, its revenue growth over the last five years was bottom-tier for the sector. While its expanding EBITDA margin shows the business has become more efficient, the downside is its EBITDA margins reveal bottom-tier profitability compared to other energy upstream and integrated energy companies. On top of that, its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Bristow Group’s P/E ratio based on the next 12 months is 7.9x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $60.67 on the company (compared to the current share price of $42.70).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.