HighPeak Energy (HPK)

We’re skeptical of HighPeak Energy. It not only burned cash historically but also has been less efficient lately. No need to stick around here.― StockStory Analyst Team

1. News

2. Summary

Why HighPeak Energy Is Not Exciting

Operating in the oil-rich northeastern corner of the Midland Basin where Howard and Borden counties meet, HighPeak Energy (NASDAQ:HPK) explores for, develops, and produces crude oil, natural gas liquids, and natural gas.

- Efficiency has decreased over the last five years as its EBITDA margin fell by 12.3 percentage points

- Cash-burning tendencies make us wonder if it can sustainably generate shareholder value

- A positive is that its market share has increased this cycle as its 104% annual revenue growth over the last five years was exceptional

HighPeak Energy falls below our quality standards. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than HighPeak Energy

At $6.86 per share, HighPeak Energy trades at 3.6x forward EV-to-EBITDA. HighPeak Energy’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. HighPeak Energy (HPK) Research Report: Q4 CY2025 Update

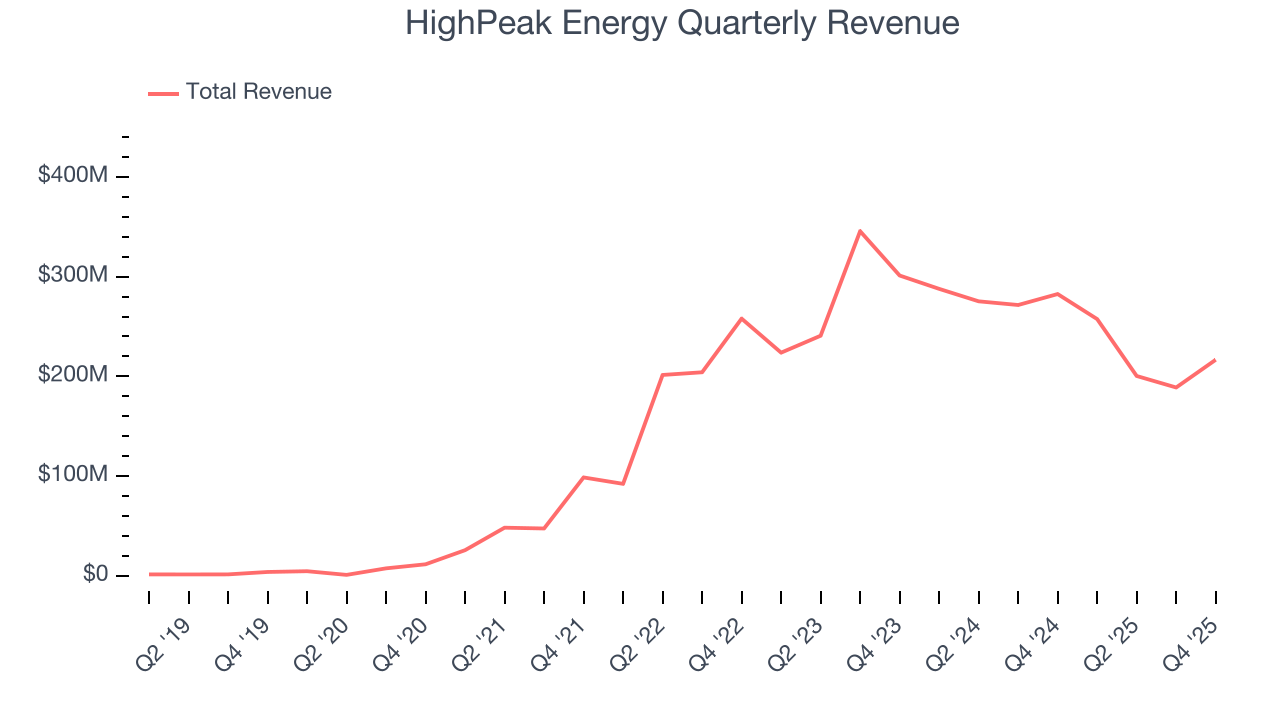

Oil and gas producer HighPeak Energy (NASDAQ:HPK) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 23.3% year on year to $216.6 million. Its non-GAAP loss of $0.20 per share was significantly below analysts’ consensus estimates.

HighPeak Energy (HPK) Q4 CY2025 Highlights:

- Revenue: $216.6 million vs analyst estimates of $190.6 million (23.3% year-on-year decline, 13.7% beat)

- Adjusted EPS: -$0.20 vs analyst estimates of -$0.07 (significant miss)

- Adjusted EBITDA: $94.32 million vs analyst estimates of $129.6 million (43.5% margin, 27.2% miss)

- Operating Margin: -7.6%, down from 26.1% in the same quarter last year

- Free Cash Flow was -$30.16 million compared to -$17.64 million in the same quarter last year

- Market Capitalization: $868.1 million

Company Overview

Operating in the oil-rich northeastern corner of the Midland Basin where Howard and Borden counties meet, HighPeak Energy (NASDAQ:HPK) explores for, develops, and produces crude oil, natural gas liquids, and natural gas.

The company controls approximately 154,000 gross acres across two core areas: Flat Top, located primarily in northern Howard County extending into southern Borden County, and Signal Peak in southern Howard County. With a 92% average working interest and operational control over 97% of its net acreage, HighPeak Energy maintains significant decision-making authority over its drilling and production activities.

HighPeak Energy's drilling strategy centers on tapping into the Wolfcamp A and Lower Spraberry formations, geological layers within the Permian Basin known for their hydrocarbon content. The company employs multi-well pad development, a technique where multiple wells are drilled from a single surface location, which reduces the time needed to drill and complete wells while allowing shared use of infrastructure like pipelines and processing facilities across multiple wells.

The company's production involves crude oil, natural gas liquids (which include propane, butane, and ethane), and natural gas. In Flat Top, crude oil is transported via pipeline to buyers, while in Signal Peak it moves by truck. Natural gas flows to third-party processors who extract the valuable liquids before selling both the liquids and remaining dry gas into regional markets. HighPeak Energy's customers include oil marketers and traders such as Delek and Energy Transfer Crude Marketing. The company's contiguous acreage position allows for connected infrastructure, including salt-water disposal wells and pipeline systems that handle the water produced alongside oil and gas.

4. U.S. Shale E&P

US shale oil producers extract crude from tight rock formations using horizontal drilling and hydraulic fracturing (fracking) techniques, primarily in basins like the Permian, Bakken, and Eagle Ford. Tailwinds include short-cycle investment flexibility allowing rapid production adjustments, technological improvements enhancing well productivity, and proximity to refining and export infrastructure. Capital discipline has improved financial returns. Headwinds include commodity price sensitivity affecting drilling economics, accelerating well decline rates requiring continuous capital investment, and increasing regulatory and ESG scrutiny. Water usage, induced seismicity concerns, and evolving environmental regulations present ongoing operational challenges.

HighPeak Energy competes with other Permian Basin producers including Diamondback Energy (NASDAQ:FANG), Matador Resources (NYSE:MTDR), Callon Petroleum (NYSE:CPE), and numerous private operators in the region.

5. Revenue Scale

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program. HighPeak Energy’s $863.4 million of revenue in the last year is pretty small for the industry, suggesting the company hasn’t hit a level of diversification where investors can sleep easy at night.

6. Revenue Growth

Cyclical sectors like Energy often flatter weaker operators during favorable price environments, but a longer-term lens separates those from businesses that can consistently perform across market cycles. Thankfully, HighPeak Energy’s 104% annualized revenue growth over the last five years was incredible. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers.

This quarter, HighPeak Energy’s revenue fell by 23.3% year on year to $216.6 million but beat Wall Street’s estimates by 13.7%.

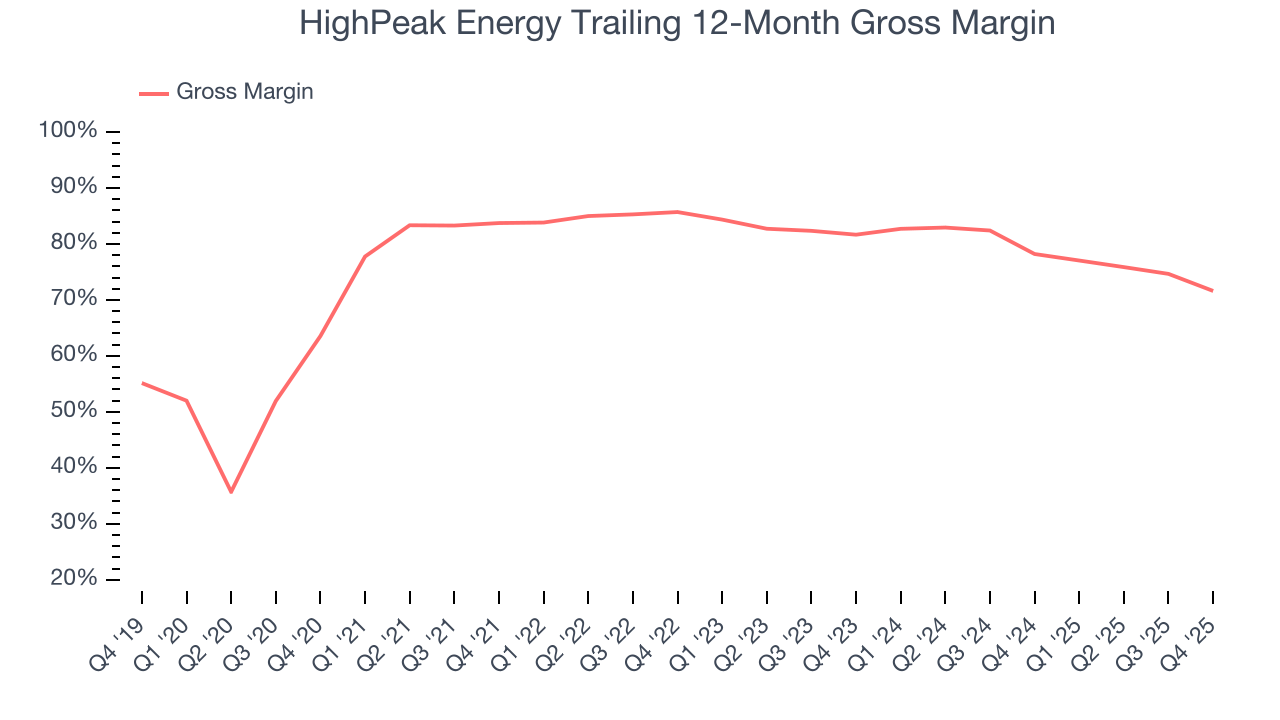

7. Gross Margin

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

HighPeak Energy, which averaged 79.4% gross margin over the last five years, exhibits impressive unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an excellent starting point for ultimate operating profits and free cash flow generation.

HighPeak Energy’s gross profit margin came in at 51.6% this quarter, down 14.7 percentage points year on year.

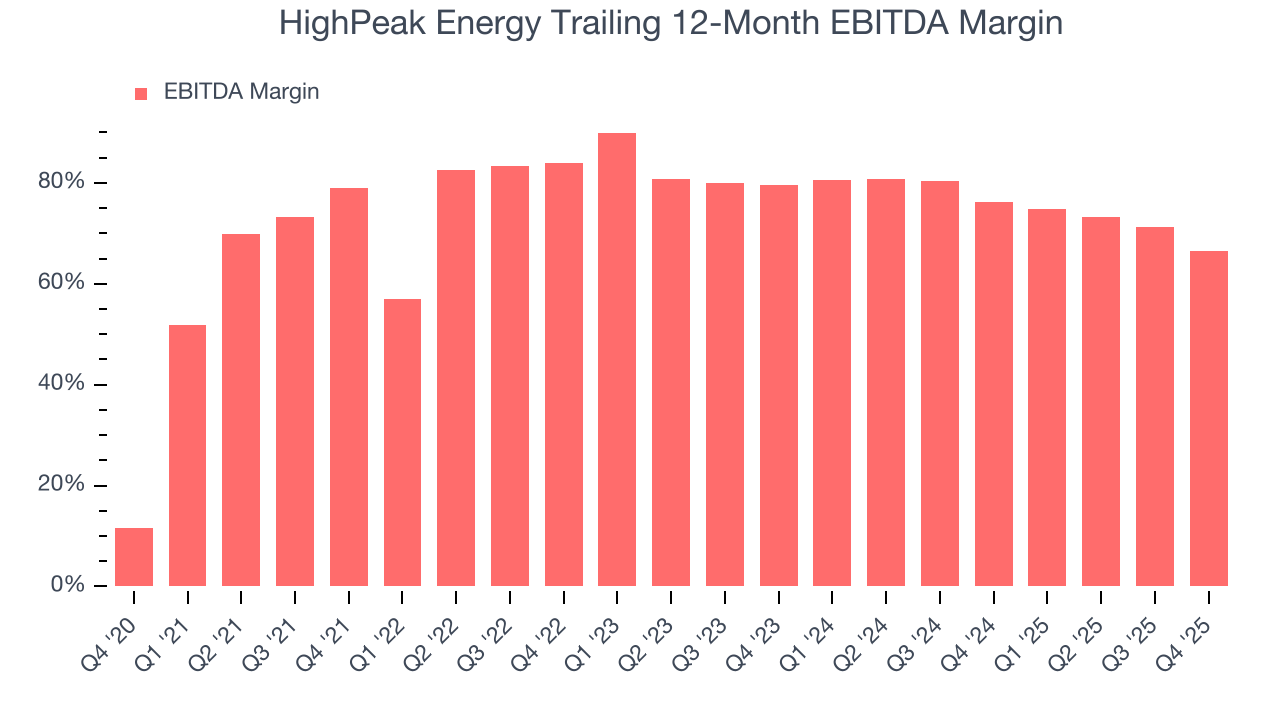

8. Adjusted EBITDA Margin

HighPeak Energy has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 76.6%.

Analyzing the trend in its profitability, HighPeak Energy’s EBITDA margin decreased by 12.3 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see HighPeak Energy become more profitable in the future.

In Q4, HighPeak Energy generated an EBITDA margin profit margin of 43.5%, down 20.4 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

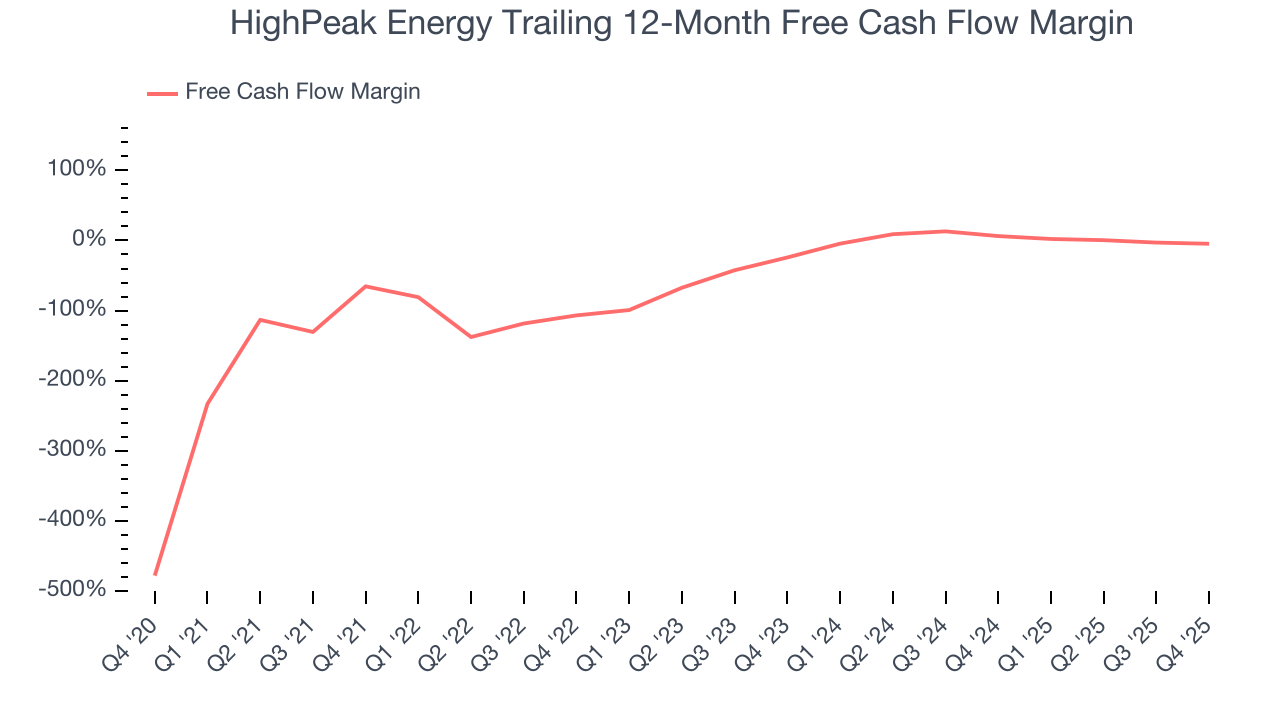

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing wells are before financing and reinvestment decisions, but free cash flow shows how much value remains after paying the cost of replacing those wells. In upstream energy, production naturally declines over time, so companies must continuously reinvest just to stand still. A producer can report strong EBITDA margins yet generate little or no free cash flow if its wells decline quickly or if new drilling is expensive. Free cash flow therefore captures not only how efficiently a company produces hydrocarbons today, but also how costly it is to sustain that production into the future.

HighPeak Energy’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 29.2%, meaning it lit $29.25 of cash on fire for every $100 in revenue.

While the level of free cash flow margins is important, their consistency matters just as much.

HighPeak Energy’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 11 (lower is better), indicating that its cash generation is far more sensitive to commodity-price swings than most peers. This elevated volatility limits its access to capital in downturns and makes it unlikely to act as a consolidator when weaker competitors come under pressure.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of HighPeak Energy? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

HighPeak Energy burned through $30.16 million of cash in Q4, equivalent to a negative 13.9% margin. The company’s cash burn was similar to its $17.64 million of lost cash in the same quarter last year.

10. Balance Sheet Assessment

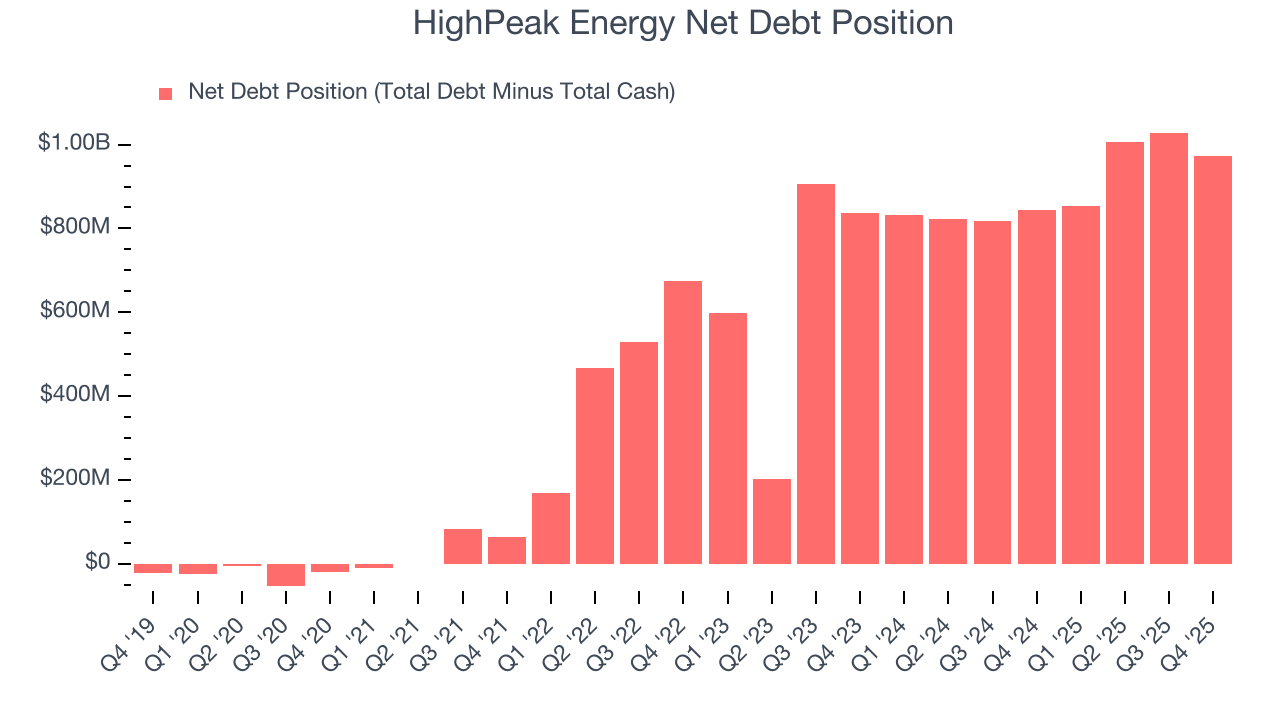

HighPeak Energy reported $162.1 million of cash and $1.13 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $574.9 million of EBITDA over the last 12 months, we view HighPeak Energy’s 1.7× net-debt-to-EBITDA ratio as safe. We also see its $143.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from HighPeak Energy’s Q4 Results

We were impressed by how significantly HighPeak Energy blew past analysts’ revenue expectations this quarter. On the other hand, its EBITDA missed and its EPS fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $6.90 immediately following the results.

12. Is Now The Time To Buy HighPeak Energy?

Updated: March 20, 2026 at 12:46 AM EDT

Before making an investment decision, investors should account for HighPeak Energy’s business fundamentals and valuation in addition to what happened in the latest quarter.

HighPeak Energy isn’t a terrible business, but it doesn’t pass our quality test. Although its revenue growth over the last five years was top-tier for the sector, it’s expected to deteriorate over the next 12 months and its cash burn raises the question of whether it can sustainably maintain growth. And while the company’s admirable gross margin indicates excellent unit economics, the downside is its declining EBITDA margin shows the business has become less efficient.

HighPeak Energy’s EV-to-EBITDA ratio based on the next 12 months is 3.6x. This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $7.88 on the company (compared to the current share price of $6.86).