Occidental Petroleum (OXY)

Occidental Petroleum piques our interest. Despite its slow growth, its highly profitable model gives it a margin of safety during times of stress.― StockStory Analyst Team

1. News

2. Summary

Why Occidental Petroleum Is Interesting

Backed by Warren Buffett's Berkshire Hathaway as a major shareholder, Occidental Petroleum (NYSE:OXY) explores for, develops, and produces oil, natural gas liquids, and natural gas, primarily in the United States and Middle East.

- Enormous revenue base of $22.08 billion provides significant leverage in supplier negotiations

- Strong free cash flow margin of 24.3% gives it the option to reinvest, repurchase shares, or pay dividends

- One risk is its underwhelming 4% return on capital reflects management’s difficulties in finding profitable growth opportunities

Occidental Petroleum has some noteworthy aspects. If you believe in the company, the valuation seems reasonable.

Why Is Now The Time To Buy Occidental Petroleum?

Occidental Petroleum is trading at $57.73 per share, or 27.3x forward P/E. While this multiple is higher than most energy upstream and integrated energy companies, we think the valuation is deserved for the revenue growth you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Occidental Petroleum (OXY) Research Report: Q4 CY2025 Update

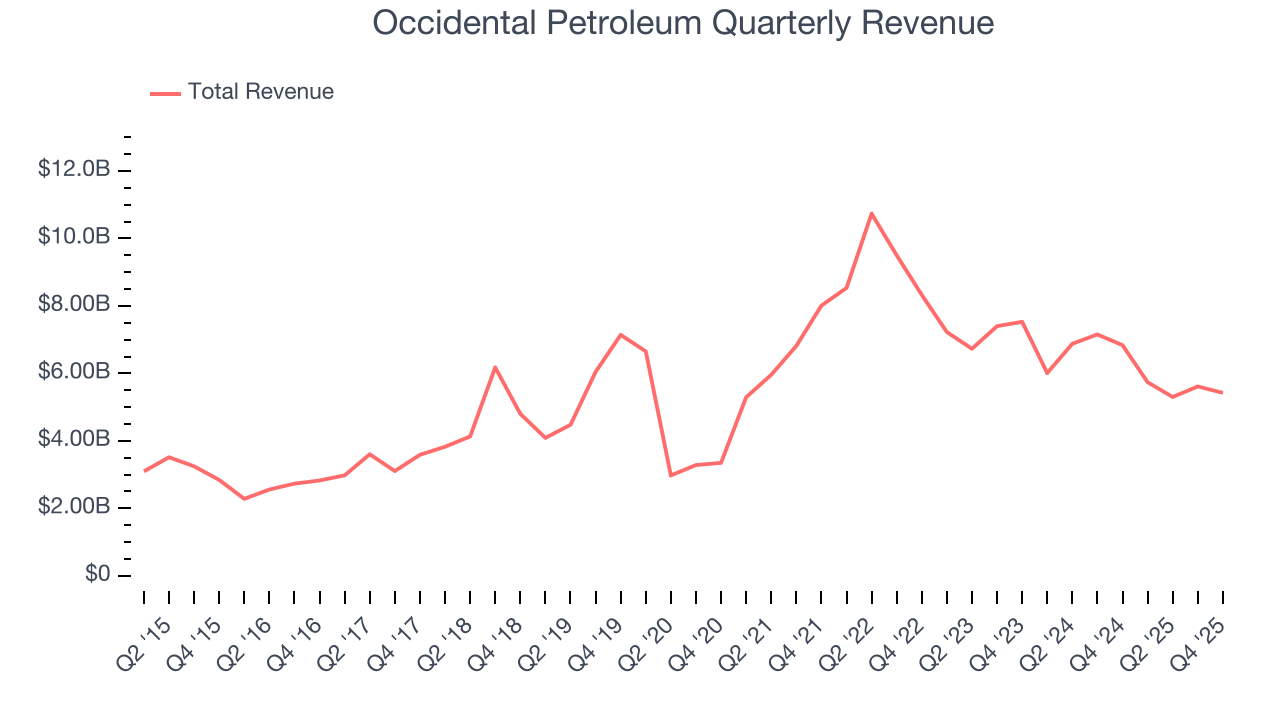

Oil and gas producer Occidental Petroleum (NYSE:OXY) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 20.7% year on year to $5.42 billion. Its non-GAAP profit of $0.31 per share was 83.8% above analysts’ consensus estimates.

Occidental Petroleum (OXY) Q4 CY2025 Highlights:

- Revenue: $5.42 billion vs analyst estimates of $5.77 billion (20.7% year-on-year decline, 6% miss)

- Adjusted EPS: $0.31 vs analyst estimates of $0.17 (83.8% beat)

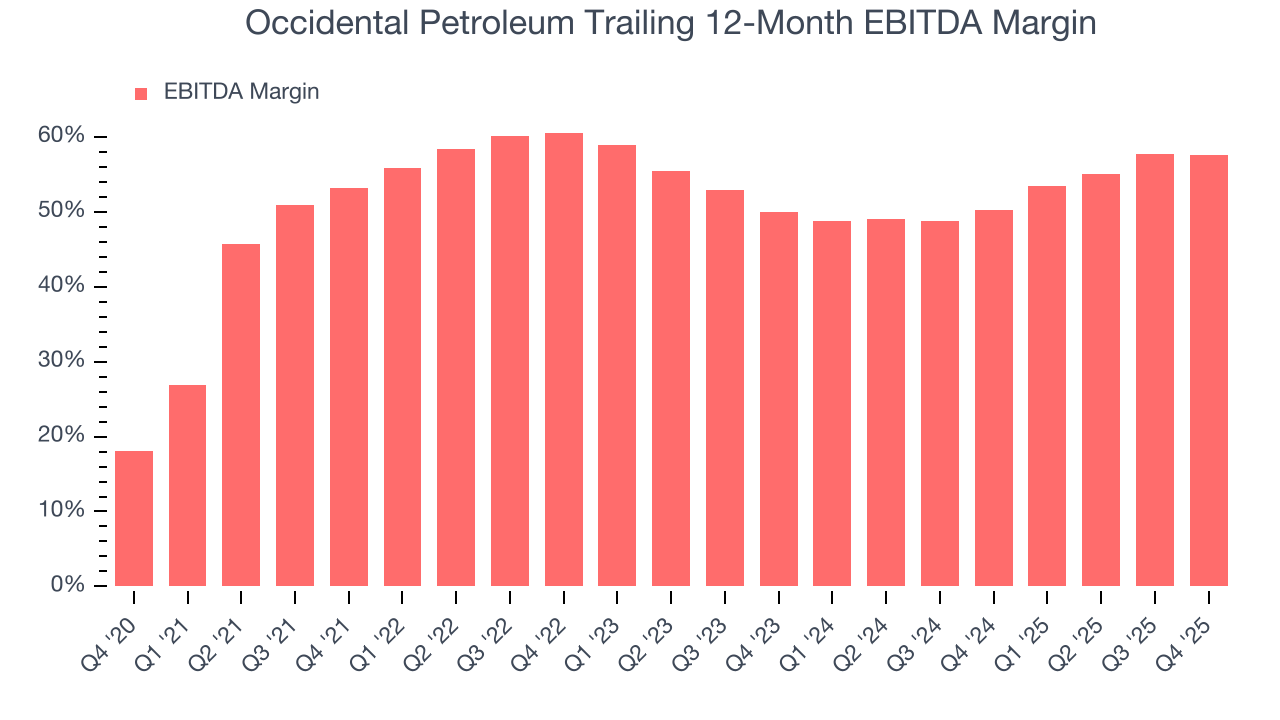

- Adjusted EBITDA: $2.6 billion vs analyst estimates of $2.76 billion (48% margin, 5.6% miss)

- Operating Margin: 15.1%, up from 0.1% in the same quarter last year

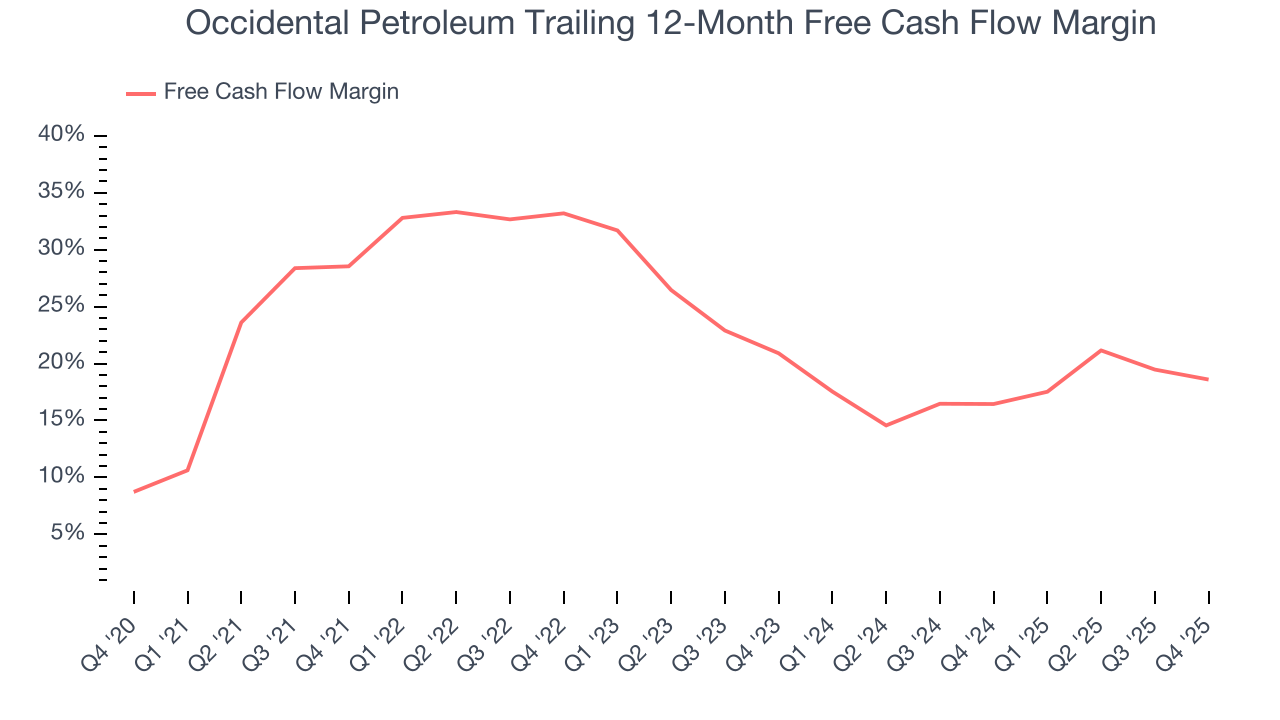

- Free Cash Flow Margin: 20.4%, down from 23% in the same quarter last year

- Market Capitalization: $56.46 billion

Company Overview

Backed by Warren Buffett's Berkshire Hathaway as a major shareholder, Occidental Petroleum (NYSE:OXY) explores for, develops, and produces oil, natural gas liquids, and natural gas, primarily in the United States and Middle East.

Occidental operates its business through three distinct segments. The oil and gas segment represents its core operations, with primary activity concentrated in the Permian Basin of Texas and New Mexico, as well as international operations in Algeria, Oman, Qatar, and the United Arab Emirates. The company also maintains offshore production in the Gulf of Mexico. In 2024, Occidental expanded its Permian Basin footprint through the acquisition of CrownRock, adding additional production capacity and drilling inventory to its portfolio.

The chemical segment, operating as OxyChem, manufactures basic chemicals and vinyls at over 20 manufacturing plants across the United States and internationally. Its product portfolio includes chlorine, caustic soda (used in manufacturing and water treatment), and polyvinyl chloride (PVC), a common plastic used in construction materials like pipes and vinyl siding. For example, a construction company building residential homes might purchase OxyChem's PVC resin to manufacture vinyl window frames and plumbing pipes.

The midstream and marketing segment supports the company's core operations by gathering, processing, transporting, and storing hydrocarbons. It also includes low-carbon ventures focused on carbon capture, utilization, and storage (CCUS) technologies. This includes direct air capture (DAC), a technology that removes carbon dioxide directly from the atmosphere. The segment holds investments in Western Midstream Partners and Dolphin Energy Limited, which operate pipeline and processing infrastructure that connects gas fields to end markets in the Middle East.

4. Diversified Upstream E&P

Large cap diversified exploration and production (E&P) companies operate global portfolios spanning multiple basins and resource types, providing geographic and commodity diversification. Scale enables operational efficiencies, capital market access, and investment in advanced technologies. Tailwinds include disciplined capital allocation improving shareholder returns, diversified production bases reducing single-asset risk, and strong balance sheets supporting dividend programs. Headwinds include commodity price volatility affecting earnings, regulatory and geopolitical risks across operating regions, and ESG pressures challenging long-term investment theses. The energy transition creates strategic uncertainty around reserve life and future demand trajectories.

Occidental Petroleum's competitors in oil and gas exploration and production include ExxonMobil (NYSE:XOM), Chevron (NYSE:CVX), ConocoPhillips (NYSE:COP), EOG Resources (NYSE:EOG), Devon Energy (NYSE:DVN), and Diamondback Energy (NASDAQ:FANG).

5. Economies of Scale

The size of the revenue base is a way to assess topline, and it tells an investor whether an Energy producer has crossed the line between being a more vulnerable commodity taker and a durable operating platform. Scaled businesses tend to produce and generate revenue from many wells, pads, takeaway routes, and geographies, not just a single field or drilling program. Occidental Petroleum’s $22.08 billion of revenue in the last year is top-tier for the industry, suggesting the company has hit a level of diversification where investors can sleep easy at night.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Regrettably, Occidental Petroleum’s sales grew at a sluggish 6.3% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the energy upstream and integrated energy sector, but there are still things to like about Occidental Petroleum.

Even a long stretch in Energy can be shaped by a single commodity cycle, so extending the view to ten years adds another perspective and reveals which companies are built to grow regardless of the pricing regime. Occidental Petroleum’s annualized revenue growth of 5.7% over the last ten years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Occidental Petroleum missed Wall Street’s estimates and reported a rather uninspiring 20.7% year-on-year revenue decline, generating $5.42 billion of revenue.

7. Gross Margin

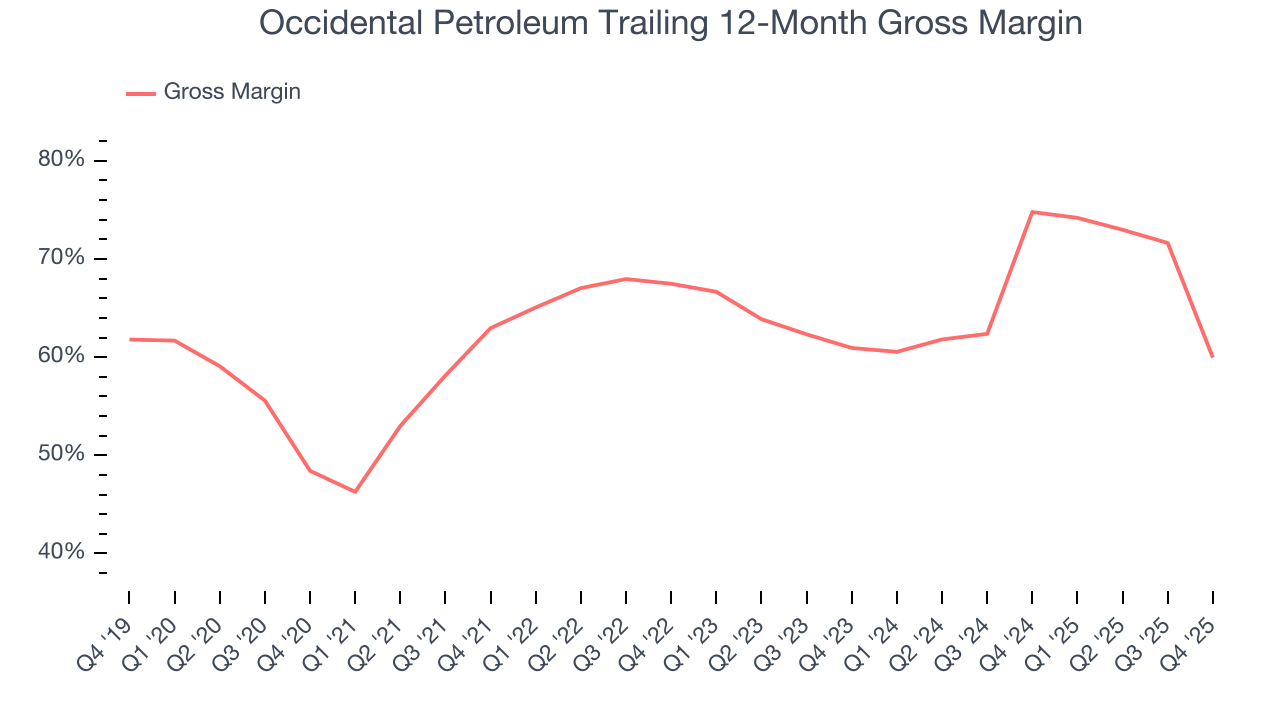

In a single quarter or year, gross margins in the sector can swing wildly due to commodity prices, hedging, or changes in labor costs. Over a multi-year period across different points in the cycle, gross margin differences can signal whether a company is a structurally-advantaged producer (“rock” quality, takeaway, operating costs) or not.

Occidental Petroleum, which averaged 65.5% gross margin over the last five years, exhibits good unit economics in the sector. It means the company will remain profitable at lower commodity prices than peers with inferior gross margins and serves as an encouraging starting point for ultimate operating profits and free cash flow generation.

In Q4, Occidental Petroleum produced a 70.2% gross profit margin, down 38 percentage points year on year.

8. Adjusted EBITDA Margin

Occidental Petroleum has been a well-oiled machine over the last five years. It demonstrated elite profitability for an upstream and integrated energy business, boasting an average EBITDA margin of 54.6%.

Looking at the trend in its profitability, Occidental Petroleum’s EBITDA margin rose by 4.4 percentage points over the last year, as its sales growth gave it operating leverage.

This quarter, Occidental Petroleum generated an EBITDA margin profit margin of 48%, down 2.6 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue. This adjusted EBITDA fell short of Wall Street’s estimates.

9. Cash Is King

As mentioned above, adjusted EBITDA ignores capital structure and drilling expenditure decisions. These are two huge aspects of an Energy producer, so in order to understand a comprehensive picture of business quality, an investor needs to account for these. Said differently, adjusted EBITDA margins could be solid but free cash flow is abysmal because decline rates of the asset are extreme and the drilling is expensive. Free cash flow tells you about not only the economics of the production that has happened but how much it costs to stay in business as well (further drilling or extraction).

Occidental Petroleum has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the energy upstream and integrated energy sector, averaging 24.3% over the last five years.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Occidental Petroleum’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 3.7 (lower is better), indicating excellent insulation from commodity swings. This stability supports superior capital access in downturns and positions Occidental Petroleum to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI Crude prices in the case of Occidental Petroleum? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Occidental Petroleum’s free cash flow clocked in at $1.11 billion in Q4, equivalent to a 20.4% margin. The company’s cash profitability regressed as it was 2.6 percentage points lower than in the same quarter last year, which isn’t ideal considering its longer-term trend.

10. Return on Invested Capital (ROIC)

Free cash flow tells investors how much money an Energy producer made, and ROIC takes this one step further by telling investors how well and effectively the business made it. ROIC illustrates how much operating profit a producer generated relative to the money it has raised (debt and equity).

We at StockStory like to look at ROIC over a ten-year period because energy investment cycles can involve up to five years of ramping production and another five years of harvesting. A decade view captures buying, extracting, and monetizing rather than just part of that picture. Although Occidental Petroleum has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its ten-year average ROIC was 4%, lower than the typical cost of capital (how much it costs to raise money) for energy upstream and integrated energy companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Occidental Petroleum’s ROIC has decreased over the last few years. If its returns keep falling, it could suggest its profitable growth opportunities are drying up. We’ll keep a close eye.

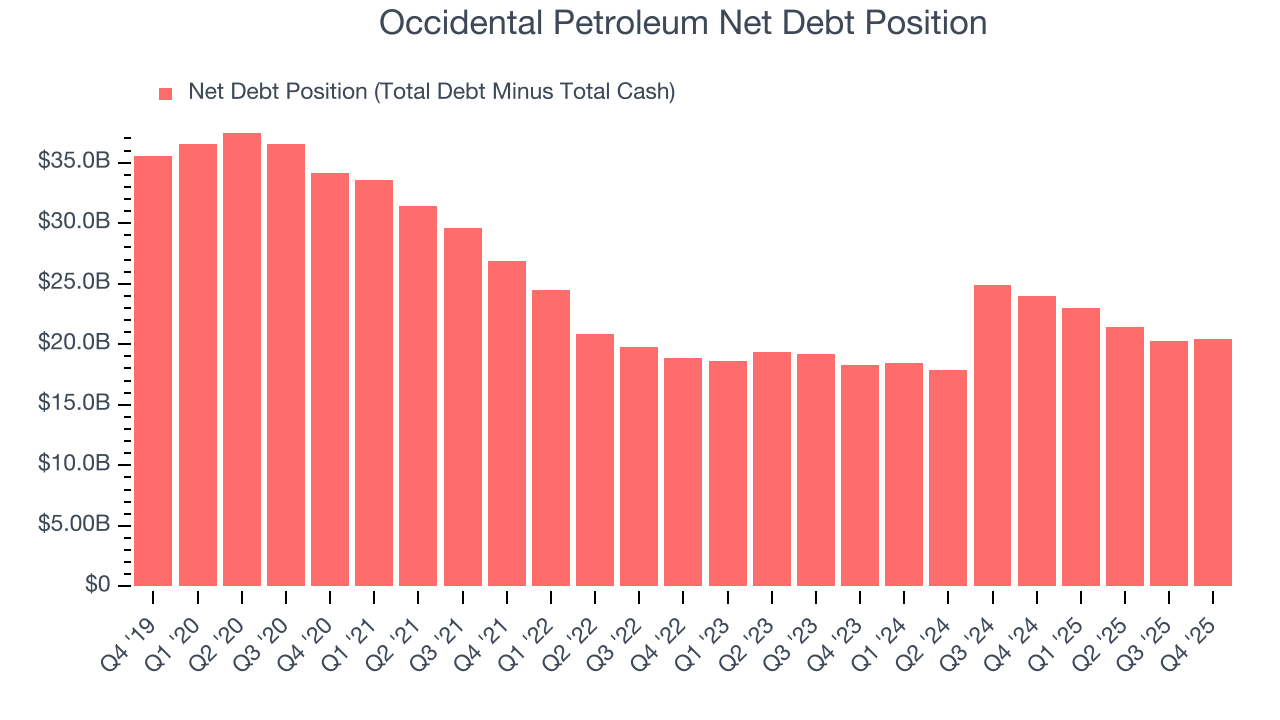

11. Balance Sheet Assessment

Occidental Petroleum reported $1.97 billion of cash and $22.4 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $12.71 billion of EBITDA over the last 12 months, we view Occidental Petroleum’s 1.6× net-debt-to-EBITDA ratio as safe. We also see its $876 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Occidental Petroleum’s Q4 Results

It was good to see Occidental Petroleum beat analysts’ EPS expectations this quarter. On the other hand, its revenue missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded up 1.4% to $58.08 immediately after reporting.

13. Is Now The Time To Buy Occidental Petroleum?

Updated: March 18, 2026 at 1:00 AM EDT

When considering an investment in Occidental Petroleum, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

There’s plenty to admire about Occidental Petroleum. Although its revenue growth was quite poor over the last five years and analysts expect growth to slow over the next 12 months, its top-tier scale enables operational efficiencies, capital market access, and investment in advanced technologies. And while its relatively low ROIC suggests management has struggled to find compelling investment opportunities, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Occidental Petroleum’s P/E ratio based on the next 12 months is 27.3x. Looking at the energy upstream and integrated energy space right now, Occidental Petroleum trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $54.68 on the company (compared to the current share price of $57.73).