Core Natural Resources (CNR)

We like Core Natural Resources. Its strong sales growth and returns on capital show it’s capable of quick and profitable expansion.― StockStory Analyst Team

1. News

2. Summary

Why We Like Core Natural Resources

Tracing its origins to 1864 and operating some mines southwest of Pittsburgh, Core Natural Resources (NYSE:CNR) mines and exports metallurgical coal used in steelmaking and thermal coal for power generation.

- Annual revenue growth of 15.1% over the last nine years was superb and indicates its market share increased during this cycle

- Impressive 36.1% annual revenue growth over the last five years indicates it’s winning market share this cycle

- ROIC punches in at 19.5%, illustrating management’s expertise in identifying profitable investments, and its returns are growing as it capitalizes on even better market opportunities

We see a bright future for Core Natural Resources. No coincidence the stock is up 1,084% over the last five years.

Is Now The Time To Buy Core Natural Resources?

Core Natural Resources’s stock price of $109.88 implies a valuation ratio of 45.4x forward P/E. There’s no denying that the lofty valuation means there’s much good news priced into the stock.

If you like the business model and believe the bull case, you can own a smaller position; our work shows that high-quality companies outperform the market over a multi-year period regardless of entry price.

3. Core Natural Resources (CNR) Research Report: Q4 CY2025 Update

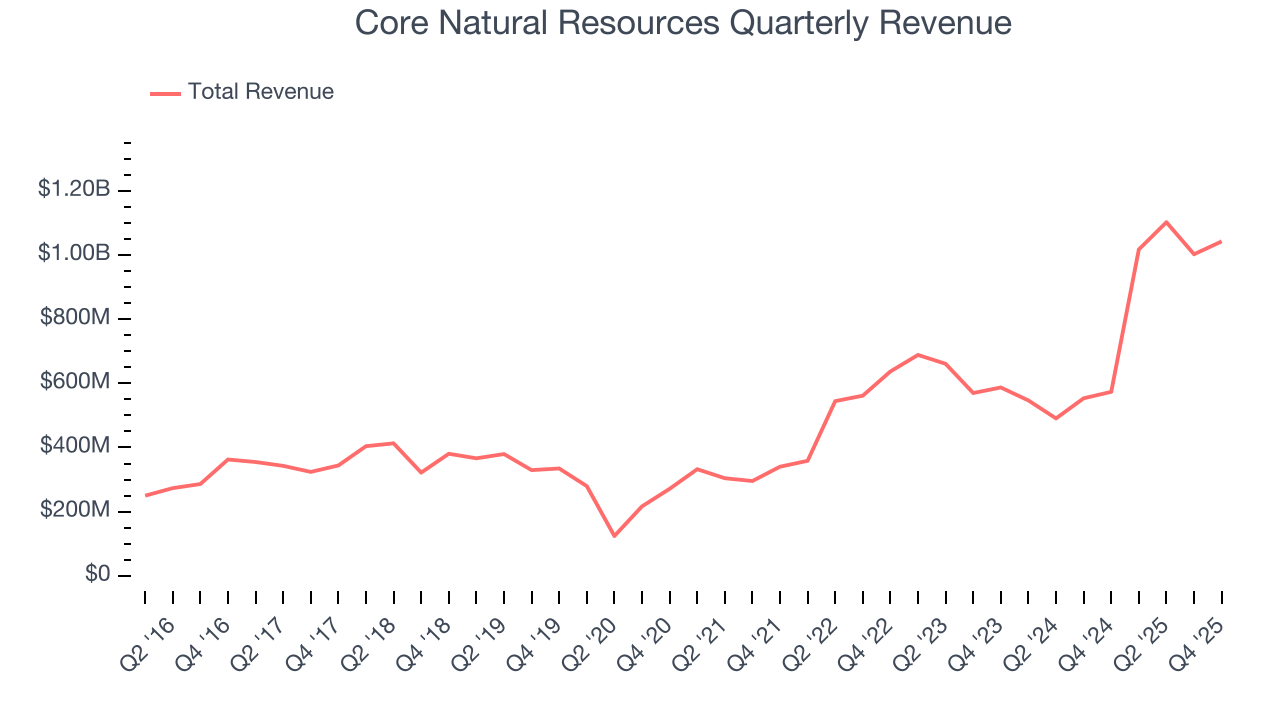

Coal producer Core Natural Resources (NYSE:CNR) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 81.8% year on year to $1.04 billion. Its non-GAAP loss of $1.15 per share was significantly below analysts’ consensus estimates.

Core Natural Resources (CNR) Q4 CY2025 Highlights:

- Revenue: $1.04 billion vs analyst estimates of $1.02 billion (81.8% year-on-year growth, 2% beat)

- Adjusted EPS: -$1.15 vs analyst estimates of -$0.35 (significant miss)

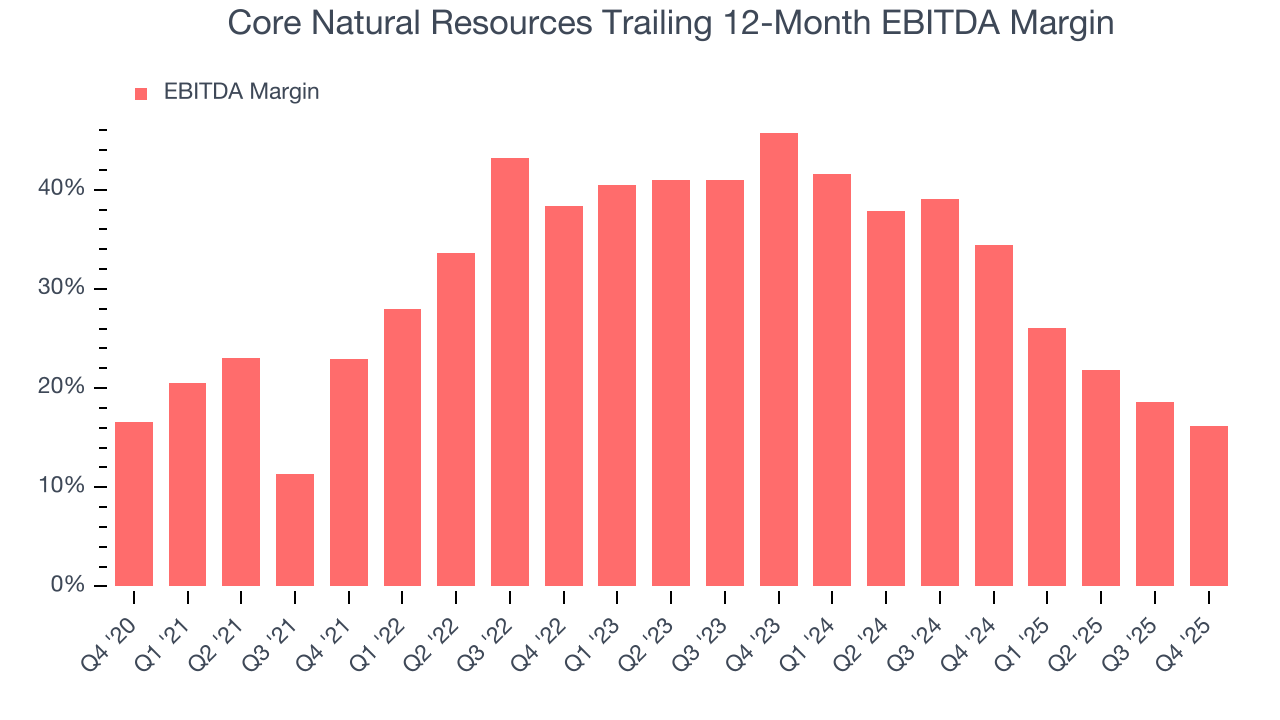

- Adjusted EBITDA: $225 million vs analyst estimates of $112.2 million (21.6% margin, significant beat)

- Operating Margin: -9.3%, down from 13% in the same quarter last year

- Free Cash Flow Margin: 2.5%, down from 14% in the same quarter last year

- Market Capitalization: $5.15 billion

Company Overview

Tracing its origins to 1864 and operating some mines southwest of Pittsburgh, Core Natural Resources (NYSE:CNR) mines and exports metallurgical coal used in steelmaking and thermal coal for power generation.

The company operates through two main business lines. Its metallurgical coal operations extract high-quality coking coal that steel manufacturers blend and heat to extreme temperatures to create coke, an essential ingredient in blast furnaces. Steel plants use this coke as both a fuel source and a reducing agent that removes oxygen from iron ore to produce molten iron. The company's thermal coal operations produce coal burned by power plants to generate electricity and by industrial facilities for heat and energy.

Core Natural Resources operates a portfolio of underground and surface mines concentrated in Pennsylvania, West Virginia, Wyoming, and Colorado. The Pennsylvania Mining Complex, its largest operation, uses longwall mining—a highly mechanized underground technique where a rotating drum shears coal from a long wall face—to extract coal from the Pittsburgh Seam. This complex includes three interconnected underground mines, a central preparation plant that cleans and processes coal, and dual rail connections to both Norfolk Southern and CSX railways. The company's West Virginia operations focus primarily on metallurgical-grade coal from seams like the Lower Kittanning and Pocahontas No. 3, while its Wyoming surface mine extracts thermal coal from the Wyodak seams using large-scale excavation equipment.

Beyond mining, the company owns and operates export infrastructure. Through its wholly-owned CONSOL Marine Terminal in Baltimore and a 35% stake in the Dominion Terminal in Newport News, Virginia, Core Natural Resources can load coal directly from rail cars onto ocean-going vessels. These terminals serve international steel mills and power plants in Europe, Asia, and South America, while domestic customers include electric utilities and industrial users across multiple states.

4. Mixed or Offshore Upstream E&P

This category includes smaller or niche E&P companies operating in specialized basins, geographies, or resource types outside major classifications. These firms may target unconventional resources, frontier regions, or specific commodity niches. Tailwinds include potential for outsized returns from successful exploration, acquisition opportunities during industry downturns, and specialized expertise commanding premium valuations. Headwinds include higher operational and geological risks, limited scale reducing negotiating power and cost efficiencies, and constrained capital market access during challenging commodity environments. Regulatory risks and ESG concerns may disproportionately affect smaller operators with fewer resources for compliance.

Core Natural Resources competes with other coal producers including Peabody Energy (NYSE:BTU), Arch Resources (NYSE:ARCH), Alpha Metallurgical Resources (NYSE:AMR), and Warrior Met Coal (NYSE:HCC).

5. Economies of Scale

The scale of a company’s revenue base is an important lens through which to view the topline, as it signals whether a producer has gone from a vulnerable commodity taker into a durable operating platform. Larger producers generate revenue across many wells, pads, takeaway routes, and geographies rather than relying on a single field or drilling program. Core Natural Resources’s $4.16 billion of revenue in the last year is mid-sized for the industry.

6. Revenue Growth

A company’s long-term performance can give signals about its business quality. Even a bad business, especially in a cyclical industry, can shine for a year or so, but a top-tier one should exhibit resilience through cycles. Luckily, Core Natural Resources’s sales grew at an incredible 36.1% compounded annual growth rate over the last five years. Its growth beat the average energy upstream and integrated energy company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Within Energy, a singular timeframe, even if it’s quite long-term, only sheds light on how well a company rode the last commodity cycle. To better assess whether a company compounds through cycles, we validate our view with an even longer, ten-year view. Core Natural Resources’s annualized revenue growth of 15.1% over the last nine years is below its five-year trend, but we still think the results suggest decent demand.

This quarter, Core Natural Resources reported magnificent year-on-year revenue growth of 81.8%, and its $1.04 billion of revenue beat Wall Street’s estimates by 2%.

7. Gross Margin

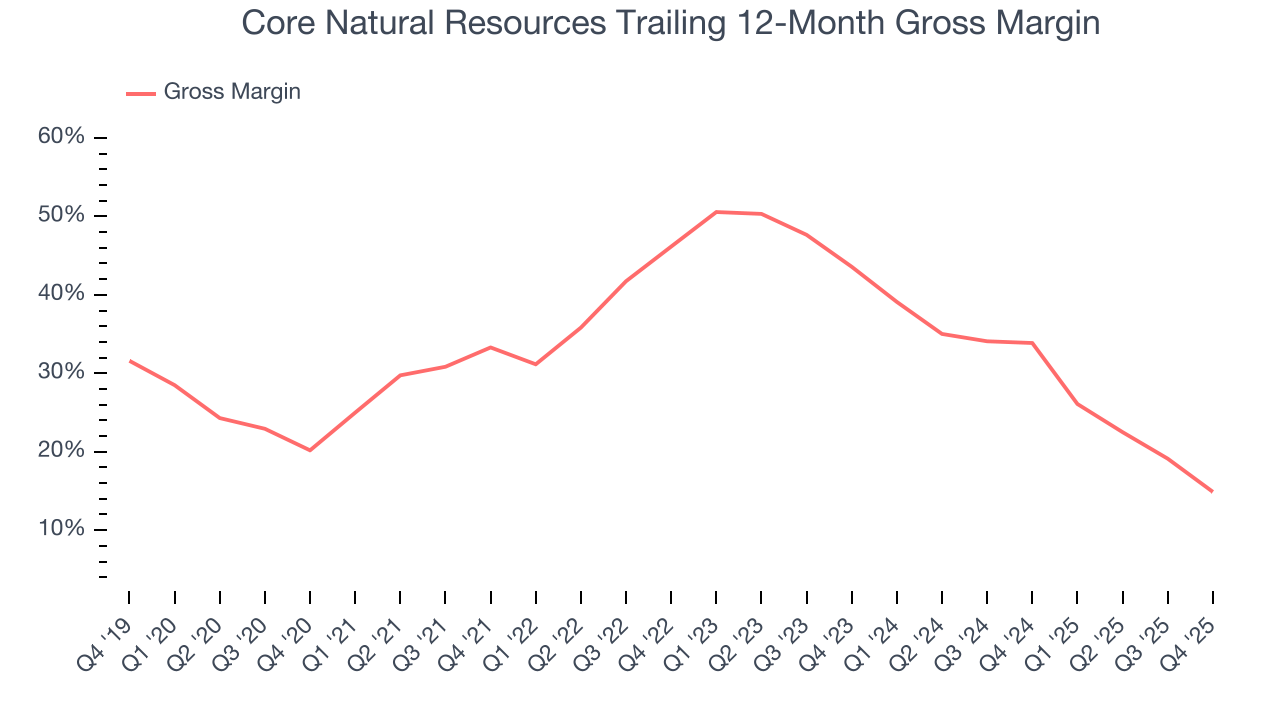

In any given year, energy gross margins are heavily influenced by prices, hedging, and cost inflation, but over a full cycle these gross margins reveal which producers are structurally advantaged through superior “rock” quality, infrastructure access, and cost position.

Core Natural Resources, which averaged 31.4% gross margin over the last five years, exhibiting bottom-tier unit economics in the sector. It means the company will struggle at higher commodity prices than peers with better gross margins.

Core Natural Resources produced a 10.4% gross profit margin in Q4, down 23.6 percentage points year on year.

8. Adjusted EBITDA Margin

Adjusted EBITDA margin strips out accounting distortions tied to depletion and historical drilling spend, providing a clearer view of the cash-generating power of the underlying asset base before financing and reinvestment decisions.

Core Natural Resources was profitable over the last five years but held back by its large cost base. Its average EBITDA margin of 30% was weak for an upstream and integrated energy business.

Looking at the trend in its profitability, Core Natural Resources’s EBITDA margin decreased by 6.7 percentage points over the last year. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Core Natural Resources’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Core Natural Resources generated an EBITDA margin profit margin of 21.6%, down 19.5 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue. This adjusted EBITDA beat Wall Street’s estimates by 100%.

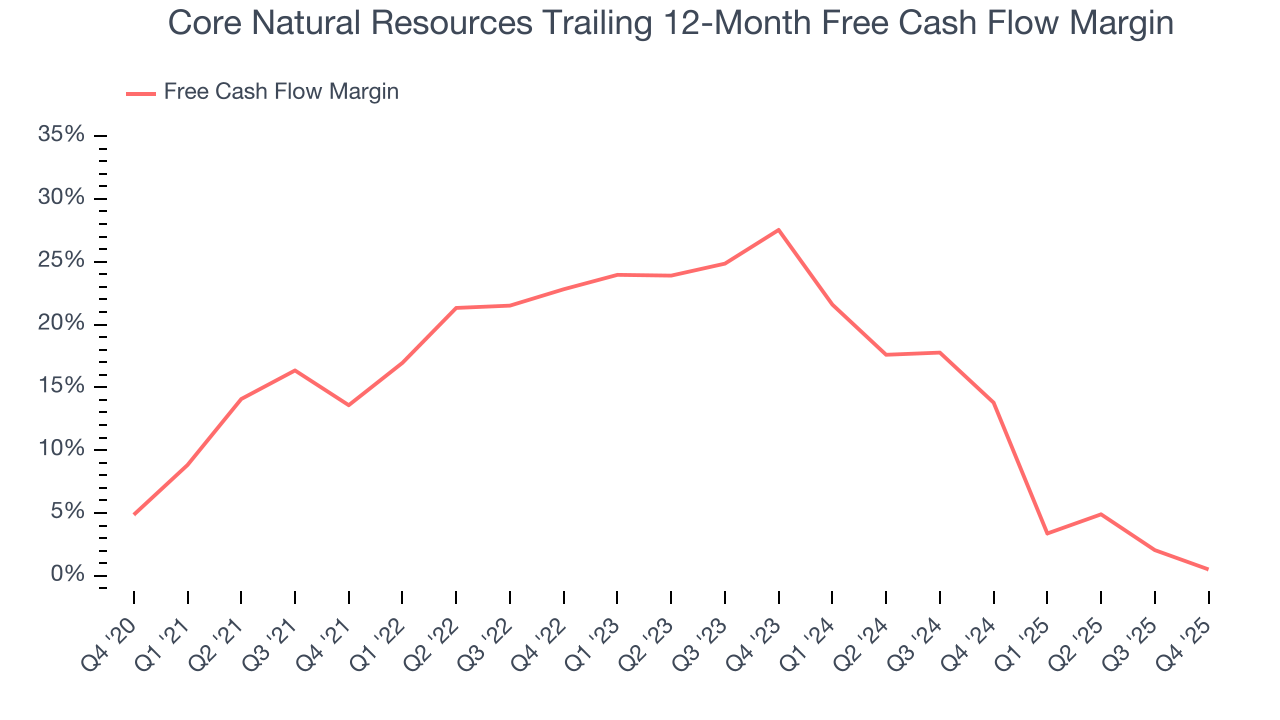

9. Cash Is King

Adjusted EBITDA shows how profitable a company’s existing “rock” is before financing and reinvestment, while free cash flow shows how much value remains after paying to replace those wells. Because production declines over time, strong EBITDA can coexist with weak FCF if drilling is expensive or declines are steep. FCF therefore captures both operating efficiency and the cost of sustaining production.

Core Natural Resources has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 13.6% over the last five years, quite impressive for an upstream and integrated energy business.

Absolute FCF margin levels matter but so does stability of free cash flow. All else equal, we’d prefer a 25.0% average free cash flow margin that is quite steady no matter how commodity prices behave rather than extremely high margins when times are good and negative ones when they’re tough.

Core Natural Resources’s ratio of quarterly free cash flow volatility to WTI crude price volatility over the past five years was 6.2 (lower is better), indicating excellent insulation from commodity swings. This stability supports capital access in downturns and positions Core Natural Resources to act as a consolidator when weaker peers are forced to retrench.

You may be asking why we wait until the free cash flow line to perform this stability analysis versus commodity prices. Why not compare revenue or EBITDA to WTI in the case of Core Natural Resources? Because what ultimately matters is not how much revenue or profit you earn when prices are high but how much cash you can generate when prices are low. Free cash flow is the superior metric because it includes everything from hedging prowess to growth and maintenance capex to management behavior during good times and bad.

Core Natural Resources’s free cash flow clocked in at $26.03 million in Q4, equivalent to a 2.5% margin. The company’s cash profitability regressed as it was 11.5 percentage points lower than in the same quarter last year, which isn’t ideal considering its longer-term trend.

10. Return on Invested Capital (ROIC)

Free cash flow shows how much money a producer generated, while ROIC shows how efficiently that money was earned. ROIC measures the operating profit produced for each dollar of capital invested, whether from debt or equity. Cash generation measures quantity while ROIC measures the quality of value creation.

We at StockStory like to look at ROIC over a ten-year period because energy investment cycles can involve up to five years of ramping production and another five years of harvesting. A decade view captures buying, extracting, and monetizing rather than just part of that picture. Core Natural Resources’s nine-year average ROIC was 19%, beating other energy upstream and integrated energy companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Core Natural Resources’s ROIC has unfortunately decreased significantly. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

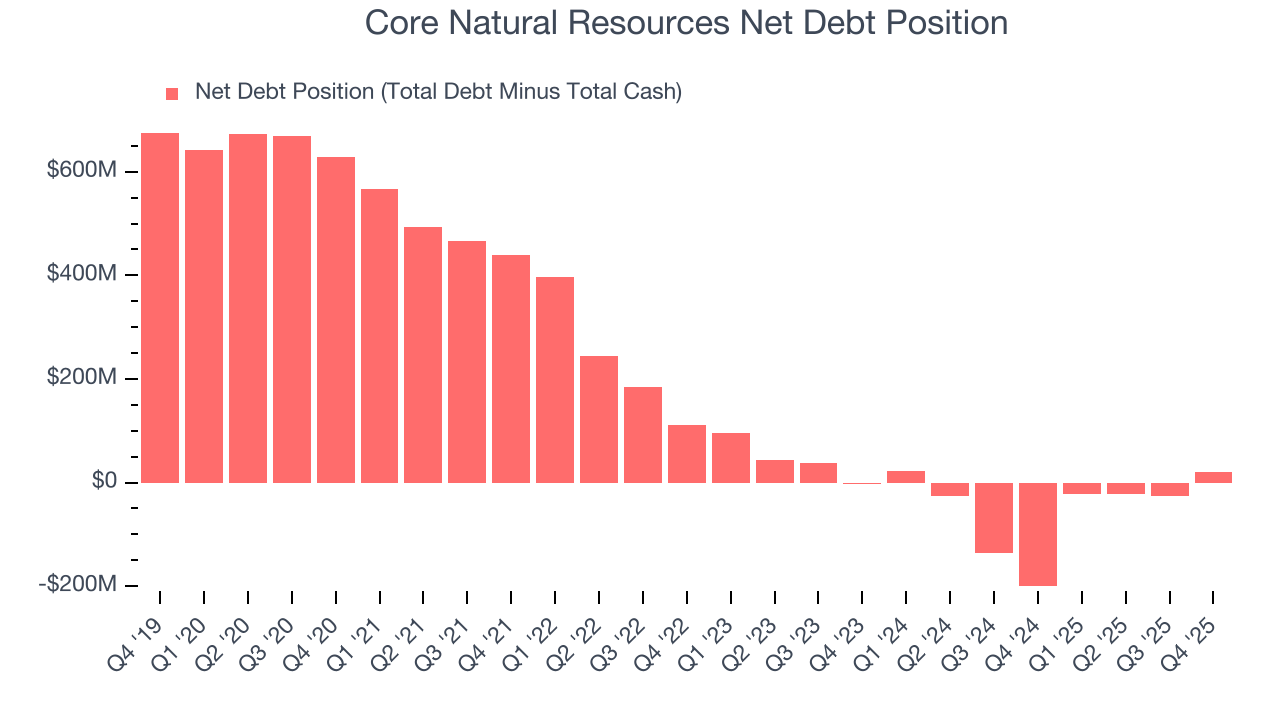

11. Balance Sheet Assessment

Core Natural Resources reported $432.2 million of cash and $452.5 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $675.2 million of EBITDA over the last 12 months, we view Core Natural Resources’s 0.0× net-debt-to-EBITDA ratio as safe. We also see its $14.23 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Core Natural Resources’s Q4 Results

We were impressed by how significantly Core Natural Resources blew past analysts’ EBITDA expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, this print had some key positives. The stock remained flat at $101.06 immediately after reporting.

13. Is Now The Time To Buy Core Natural Resources?

Updated: March 25, 2026 at 12:55 AM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

There are definitely a lot of things to like about Core Natural Resources. First off, its revenue growth over the last five years was top-tier for the sector. And while its declining EBITDA margin shows the business has become less efficient, its revenue growth over the last nine years was top-tier for the sector. On top of that, its stellar ROIC suggests it has been a well-run company historically.

Core Natural Resources’s P/E ratio based on the next 12 months is 45.4x. A lot of good news is certainly baked in given its premium multiple, but we’ll happily own Core Natural Resources as its fundamentals really stand out. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany high valuations.

Wall Street analysts have a consensus one-year price target of $111 on the company (compared to the current share price of $109.88).